Your credit report affects your ability to borrow money, rent an apartment, and sometimes even get a job. Errors on that report can damage your finances for years.

To understand credit reporting rights under the Fair Credit Reporting Act, you need to know what protections actually apply to you. We at Hays Cauley, P.C. help South Carolina residents-including those in Greenville, Columbia, and Charleston-fight back against credit reporting violations and inaccuracies.

What the FCRA Actually Protects

The Fair Credit Reporting Act covers far more than just your credit score. Enacted in 1970, the FCRA regulates how consumer reporting agencies-primarily Equifax, Experian, and TransUnion-collect, maintain, and distribute information about you. These agencies must follow strict rules about what data they can include, who can access it, and how long they can keep it.

Your Right to Access Your Credit Report

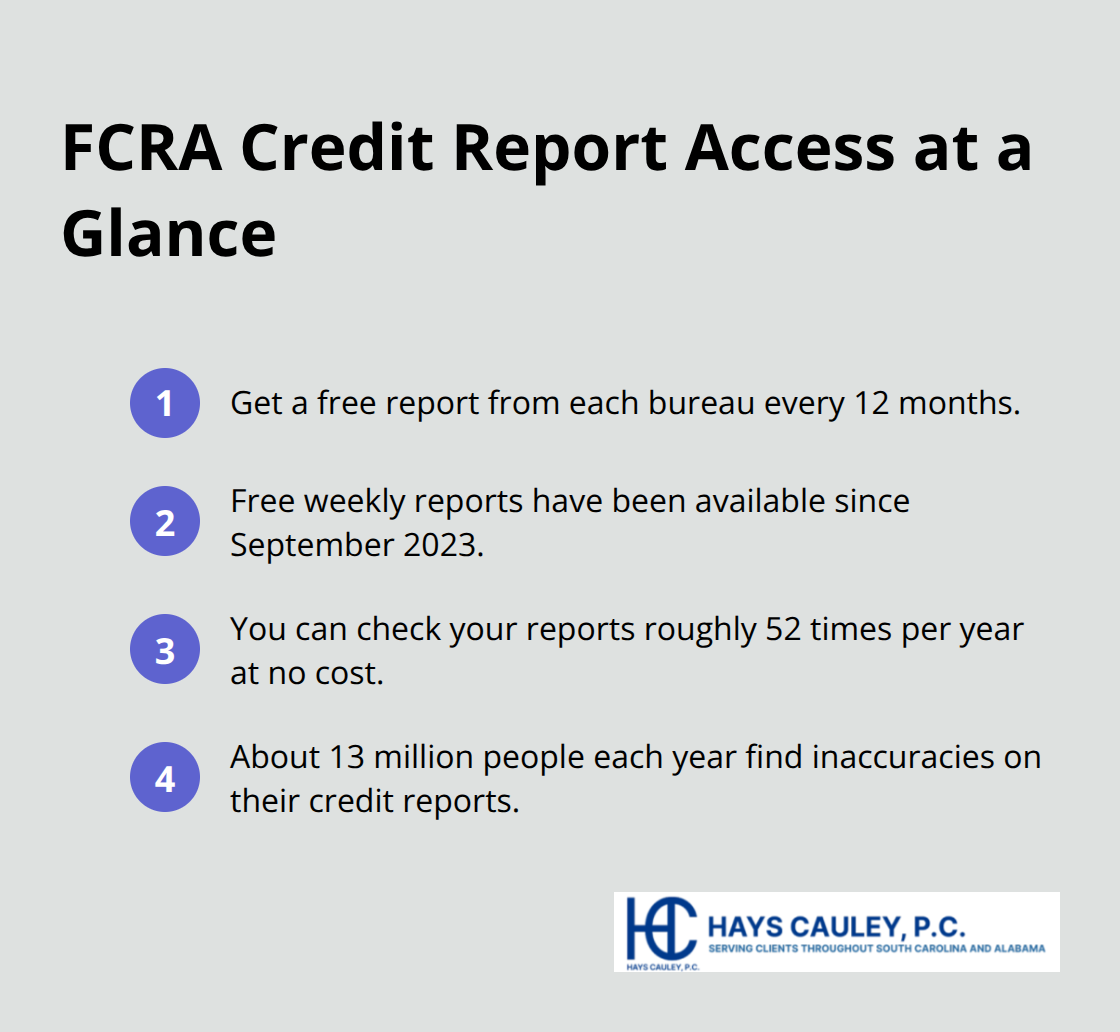

You have a legal right to access your credit report from each bureau once every 12 months for free through AnnualCreditReport.com. Since September 2023, these agencies have offered free weekly reports to encourage ongoing monitoring. This means you can check your file roughly 52 times per year at no cost. An estimated 13 million people per year find inaccuracies on their credit reports, and many never catch them because they fail to check regularly.

How Long Negative Information Stays on Your Report

Late payments remain on your file for seven years and can drop your score by 100 or more points (depending on your starting score), making regular monitoring essential to catch errors before they damage your finances. The FCRA also gives you the power to dispute inaccurate information and requires the bureaus to investigate within 30 days. Most negative items cannot stay on your report beyond seven years, though tax liens and certain judgments may have longer reporting periods.

What Creditors Can Actually Report

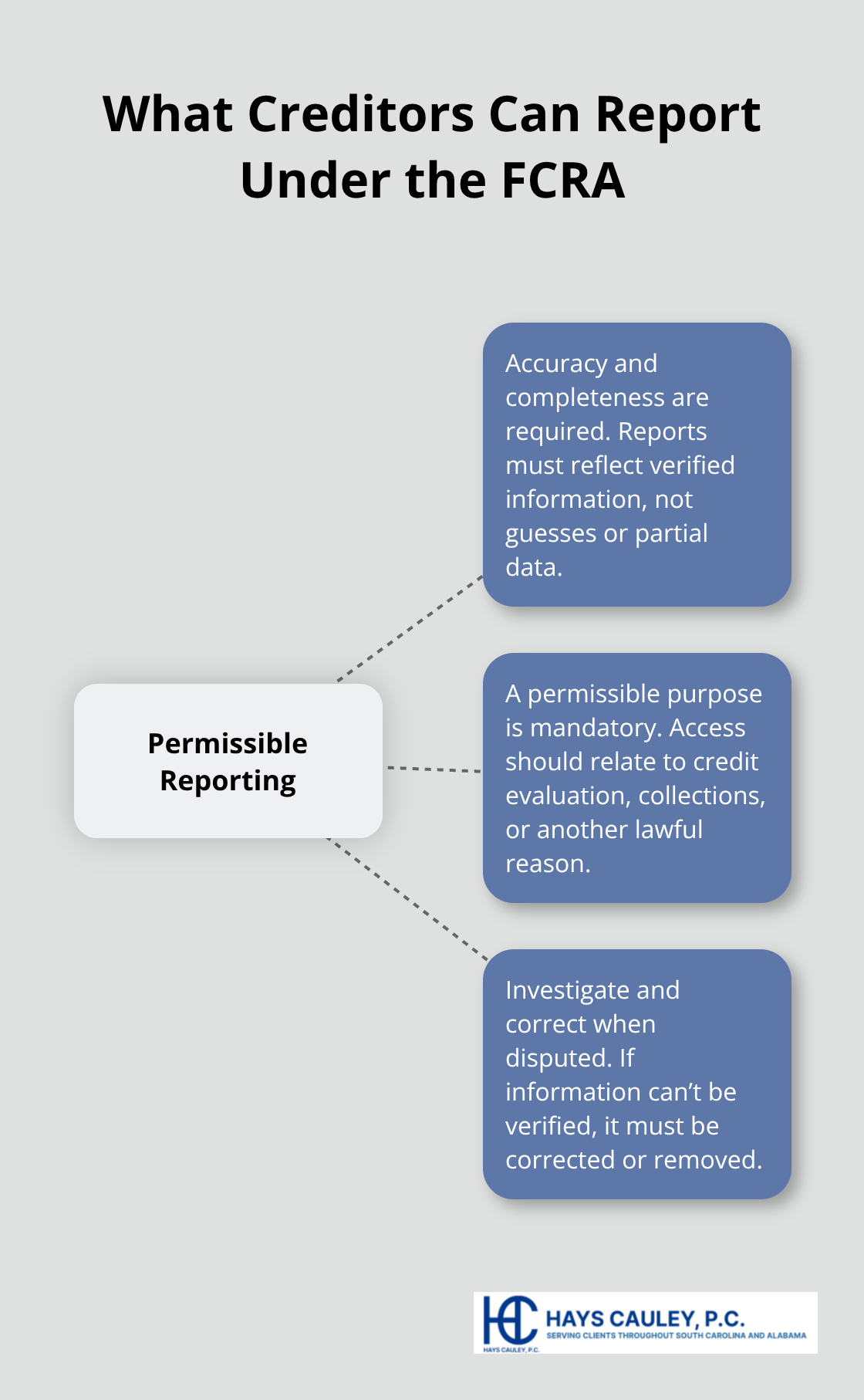

Creditors and other furnishers-banks, landlords, collection agencies-can only report information that is accurate and complete. They cannot report information without a permissible purpose, meaning they need a legitimate reason like evaluating your creditworthiness or collecting a debt. If a creditor reports something inaccurate, they must investigate when you dispute it and correct or remove it if they cannot verify the information.

How to Hold Creditors Accountable

Many creditors ignore their investigation obligations, which is why written disputes sent by certified mail create a paper trail. You should dispute directly with the furnisher, not just the bureau, because furnishers often respond faster than the agencies themselves. The key point is understanding that creditors have legal duties just like the bureaus-they cannot simply ignore your dispute or refuse to investigate. When you spot violations in how creditors report or handle your disputes, you need to know how to identify them and what steps to take next.

Common Credit Reporting Violations and How to Spot Them

Outdated and Inaccurate Information on Your Report

Credit bureaus and creditors regularly violate FCRA requirements, and many violations go undetected because consumers don’t know what to look for. One of the most common violations occurs when bureaus report information that should have been removed or corrected years ago. Late payments from 2018 should not appear on your 2026 report, yet the Consumer Financial Protection Bureau receives thousands of complaints annually about outdated negative items still showing on files. If you see a charge-off, collection account, or late payment with a date older than seven years from when it was first reported, that item violates the law and must be removed immediately.

Inaccurate information causes equal damage-wrong account balances, accounts listed twice, payment dates shifted by months, or accounts that belong to someone else entirely. These errors happen frequently because creditors use automated systems to report to bureaus without manual verification, and bureaus often fail to catch duplicates or inconsistencies. When you dispute an error, the bureau must investigate within 30 days and contact the furnisher to verify the information. If the furnisher cannot verify the account within that window, the bureau must remove it. However, many bureaus skip this step or conduct perfunctory investigations that take only days instead of thoroughly reviewing your dispute.

Unauthorized Access to Your Credit File

The second major violation involves unauthorized access to your credit file. The FCRA restricts who can pull your report to those with a permissible purpose-lenders evaluating credit applications, landlords screening tenants, employers checking background, or insurers assessing risk. Debt collectors, marketing firms, or creditors you’ve never done business with should not have access to your report. If you see hard inquiries from companies you didn’t contact, that’s a red flag.

Additionally, creditors must notify you within a reasonable time if they take adverse action based on your credit report, such as denying you credit or offering worse terms. Many creditors skip this notification entirely, leaving you unaware that your report caused the decision. This failure to notify violates your rights under federal law and prevents you from understanding what information harmed your application.

Failure to Investigate Your Disputes

A third violation occurs when creditors and bureaus fail to investigate disputes properly. Some furnishers respond to disputes with form letters stating the account is verified without actually reviewing your documentation or checking their records. Others ignore dispute letters entirely. The FCRA gives furnishers 30 days to investigate, but many blow past that deadline.

When you send a certified dispute letter to a creditor and receive no response within 45 days, that constitutes a violation. You should document everything-the date you mailed the dispute, the tracking number, and any responses received. If the creditor fails to investigate or the bureau fails to report results back to you within the required timeframe, you have grounds for a claim under federal law. These violations often stack up, and identifying them correctly positions you to take action.

Taking Action Against Credit Reporting Errors: Serving South Carolina, including Greenville, Columbia and Charleston

Gather Documentation That Supports Your Dispute

Start with your credit reports from all three bureaus through AnnualCreditReport.com and print them immediately, circling or highlighting each error with a pen. Collect bank statements showing correct payment dates, creditor letters confirming account closure or settlement, receipts proving you paid disputed charges, and any correspondence with the creditor about the account. Organize these materials by date and account number so your dispute letter tells a clear story.

The CFPB recommends including your full name and contact information, the confirmation number from your credit report if available, each disputed account number, a specific explanation of what’s wrong and why, your requested action (remove or correct), a copy of your report with errors marked, and copies (never originals) of supporting documents. Send this package to both the credit bureau and the furnisher at the same time through certified mail with return receipt-the bureau must forward your dispute to the creditor within five days, but sending directly to the furnisher accelerates their investigation since they often respond faster than the bureaus.

Track Your Dispute and Document All Responses

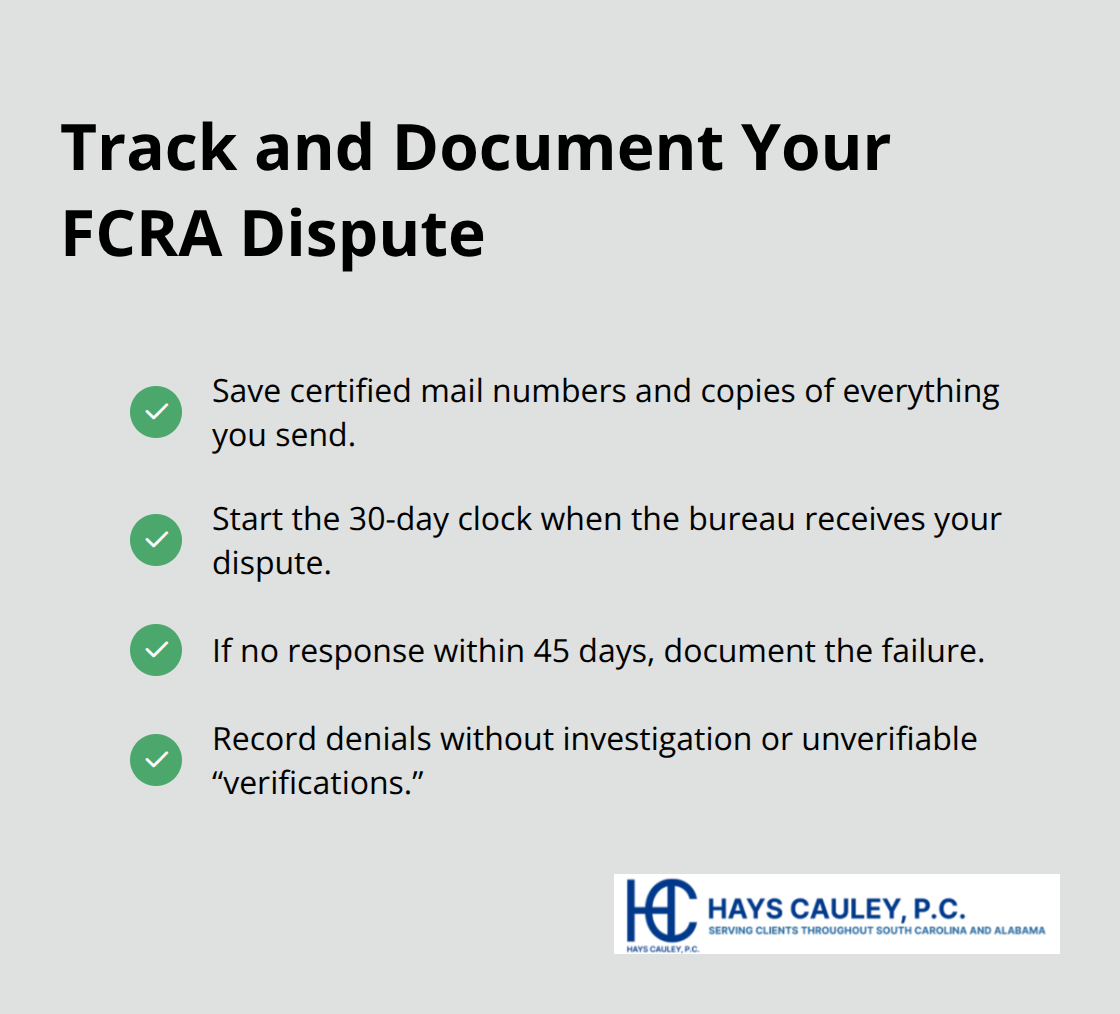

Track your certified mail number and keep copies of everything you send. The 30-day investigation window starts when the bureau receives your dispute, but many furnishers and bureaus ignore this deadline entirely. If you don’t receive a response within 45 days, document that failure because it strengthens your legal position. If the bureau or furnisher denies your dispute without investigating, or if they verify inaccurate information without actually checking their records, those violations give you grounds to pursue a claim.

Understand Your Legal Options When Disputes Fail

The FCRA allows you to recover actual damages (money you lost from higher interest rates or denied credit), statutory damages of up to $1,000 per violation, and attorney fees. In cases where a creditor refuses to correct a legitimate error after judgment, federal law permits additional damages. If disputes stall after 60 days or if you receive form-letter responses without genuine investigation, a consumer protection law firm can evaluate whether legal action makes financial sense. Many violations occur in clusters-one creditor reporting inaccurate information plus one bureau failing to investigate properly equals two separate violations that compound your damages.

Final Thoughts

The FCRA gives you real legal protections, and those protections have teeth. Credit bureaus and creditors cannot ignore your disputes, report outdated information, or fail to investigate your claims without facing consequences. Acting quickly matters because the longer inaccurate information stays on your report, the more damage it costs you in higher interest rates and denied opportunities.

We at Hays Cauley, P.C. help South Carolina residents understand credit reporting rights and fight back against violations. Our team knows how creditors and bureaus operate, what violations look like, and how to build a case that leads to correction or compensation. If your disputes have stalled, if you received form-letter denials without real investigation, or if you spotted multiple violations on your file, contact us to discuss your situation.

We handle credit reporting cases for consumers across South Carolina, including Greenville, Columbia, and Charleston, and many violations are worth pursuing. Your credit report controls access to loans, housing, and financial opportunity, and you deserve accuracy. Federal courts have awarded millions to consumers who caught violations and pursued claims, and your case may be one of them.