A mistake on your credit report can cost you thousands of dollars in higher interest rates and rejected loan applications. Yet many people don’t realize their files contain errors until they apply for a mortgage or car loan.

We at Hays Cauley, P.C. help South Carolina residents get credit reporting accuracy help by challenging inaccurate information and holding bureaus accountable. This guide walks you through your rights and the concrete steps to fix mistakes on your file.

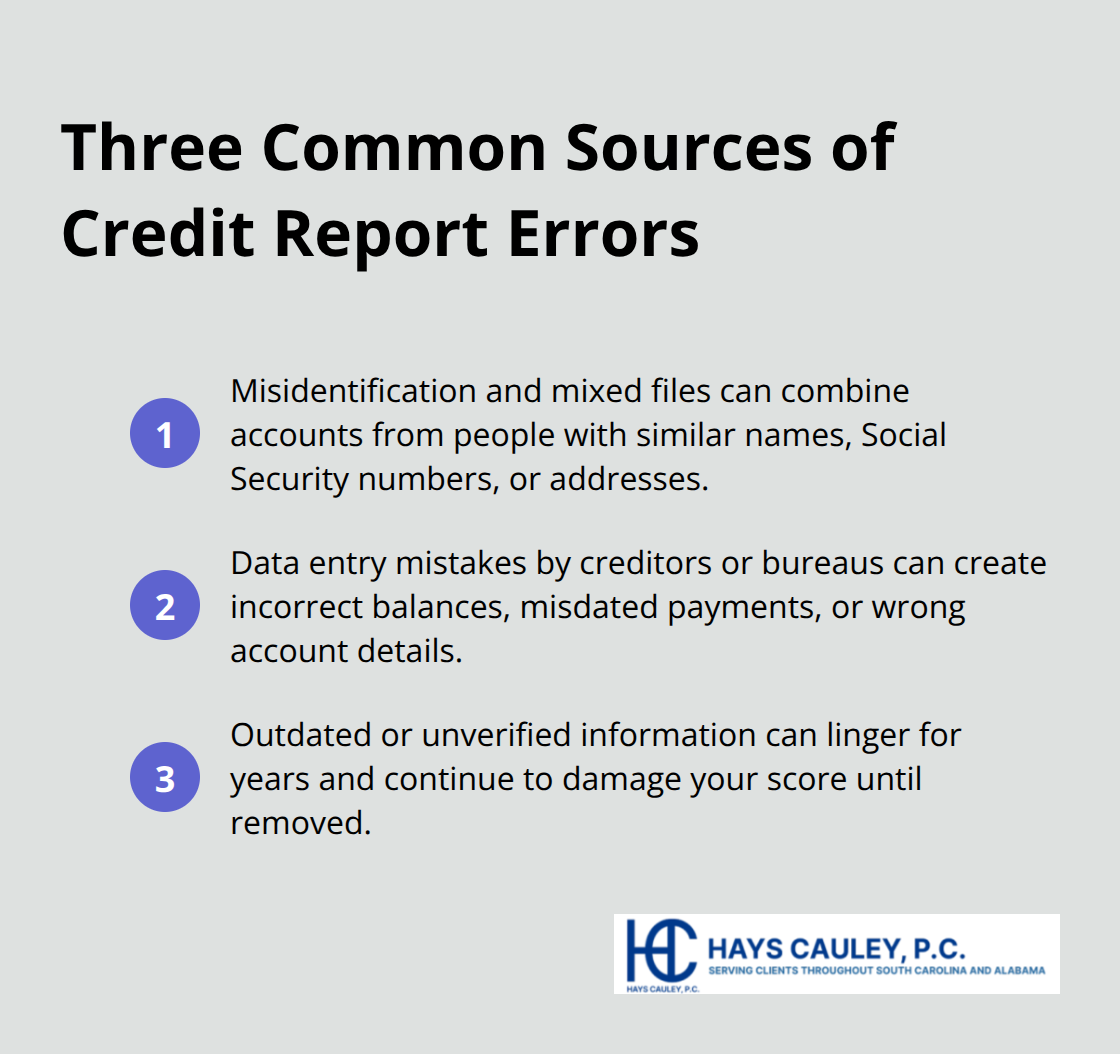

Where Credit Report Errors Come From

Misidentification and Mixed Files Create Confusion

Misidentification and mixed files occur when credit bureaus combine accounts belonging to people with similar names, Social Security numbers, or addresses into a single file. The Consumer Financial Protection Bureau reported over 800,000 credit and consumer reporting complaints in under two years, with many stemming from inaccurate information that should never have appeared on someone’s file in the first place. A mixed file might show accounts opened by someone else or delinquencies that belong to another person entirely. These errors are particularly damaging because they’re harder to catch-you might not recognize an account number or creditor name if it belongs to someone with a name similar to yours.

Data Entry Mistakes Introduce Wrong Information

Data entry mistakes by creditors and bureaus happen far more often than most people realize. When a creditor reports information to Equifax, Experian, or TransUnion, manual entry errors create wrong account numbers, incorrect balances, or misdated payments. A payment made on time gets recorded as late. A closed account shows as open. A credit limit gets entered as half the actual amount. These mistakes compound because creditors rarely verify what they report before sending it to the bureaus.

Outdated Information Lingers and Damages Your Score

Outdated or unverified information lingers on your file and creates additional problems. Negative information can stay for seven years, and bureaus aren’t always diligent about removing entries once they’re outdated. If a debt was paid off years ago but still shows as delinquent, or if a closed account continues reporting activity, that information damages your score and loan eligibility. The longer inaccurate information remains, the harder it becomes to fix and the more financial harm it causes. Acting quickly to identify and dispute these errors limits the lasting damage to your credit profile.

Understanding these three error sources prepares you to spot problems on your own file and take action immediately. Your next step involves obtaining your credit report and reviewing it with a careful eye for these specific mistakes.

Steps to Correct Credit Report Errors Serving South Carolina, including Greenville, Columbia and Charleston

Request Your Free Credit Report and Review It Carefully

Obtain your free credit report from AnnualCreditReport.com, the official source for annual reports from Equifax, Experian, and TransUnion. You receive one free report per bureau per year, and the process takes about five minutes. Equifax offers six free reports per year through 2026, which gives you more frequent monitoring opportunities. Once you have your report in hand, review it section by section with careful attention to detail.

Start with your personal information-your name, address, and Social Security number must match your records exactly, because errors here can lead to loan denials. Next, examine your account history carefully. Verify that payment dates are correct, balances match what you owe, and accounts you never opened don’t appear on your file. Look for closed accounts that incorrectly show as open, or accounts where you’re listed as owner when you should only be an authorized user.

Document Every Error You Find

Create a clear record of all mistakes on your report. Circle errors on printed copies or take screenshots of online errors. Build a spreadsheet that lists each issue, the correct information, and which accounts are affected. Gather supporting evidence before you dispute-payment confirmations, proof of closed accounts with zero balance, and identification documents if personal information is wrong. This documentation becomes your foundation for the dispute process.

File a Dispute with Each Credit Bureau

Contact each credit bureau that has inaccurate information on your file. You can dispute online, by phone, or via certified mail with return receipt. The certified mail approach is stronger because it creates a verifiable record of submission. Reach out to Equifax at 866-349-5191, Experian at 888-397-3742, and TransUnion at 800-916-8800.

When you file, include copies (never originals) of your credit report with circled errors and supporting documents that back your position.

The credit reporting company must investigate within 30 to 45 days and inform the furnisher-the creditor or company that reported the information. If the bureau cannot verify the information, it must correct or remove it from your file.

Contact the Furnisher Directly

Don’t stop at the bureau alone. Contact the furnisher directly in writing, preferably by certified mail, and dispute with them using the same documentation. Furnishers must investigate and respond within 30 days. If they refuse to investigate, that can violate the Fair Credit Reporting Act. When the furnisher corrects or removes the information, the credit reporting companies must update your credit reports accordingly.

Monitor Your Reports and Escalate if Needed

After the investigation, monitor your reports to verify corrections appear. If disputes are ignored after 30 days, file a complaint with the Consumer Financial Protection Bureau. This agency will forward your complaint to the company, provide you with a tracking number, and keep you updated on the status. Your persistence throughout this process matters-many disputes resolve only when consumers follow up consistently and document each step.

Once you understand your rights in this process, you gain the power to hold bureaus and furnishers accountable for the information they report about you.

Your Legal Rights Against Credit Bureaus Serving South Carolina, including Greenville, Columbia and Charleston

Federal Law Protects You From Inaccurate Reporting

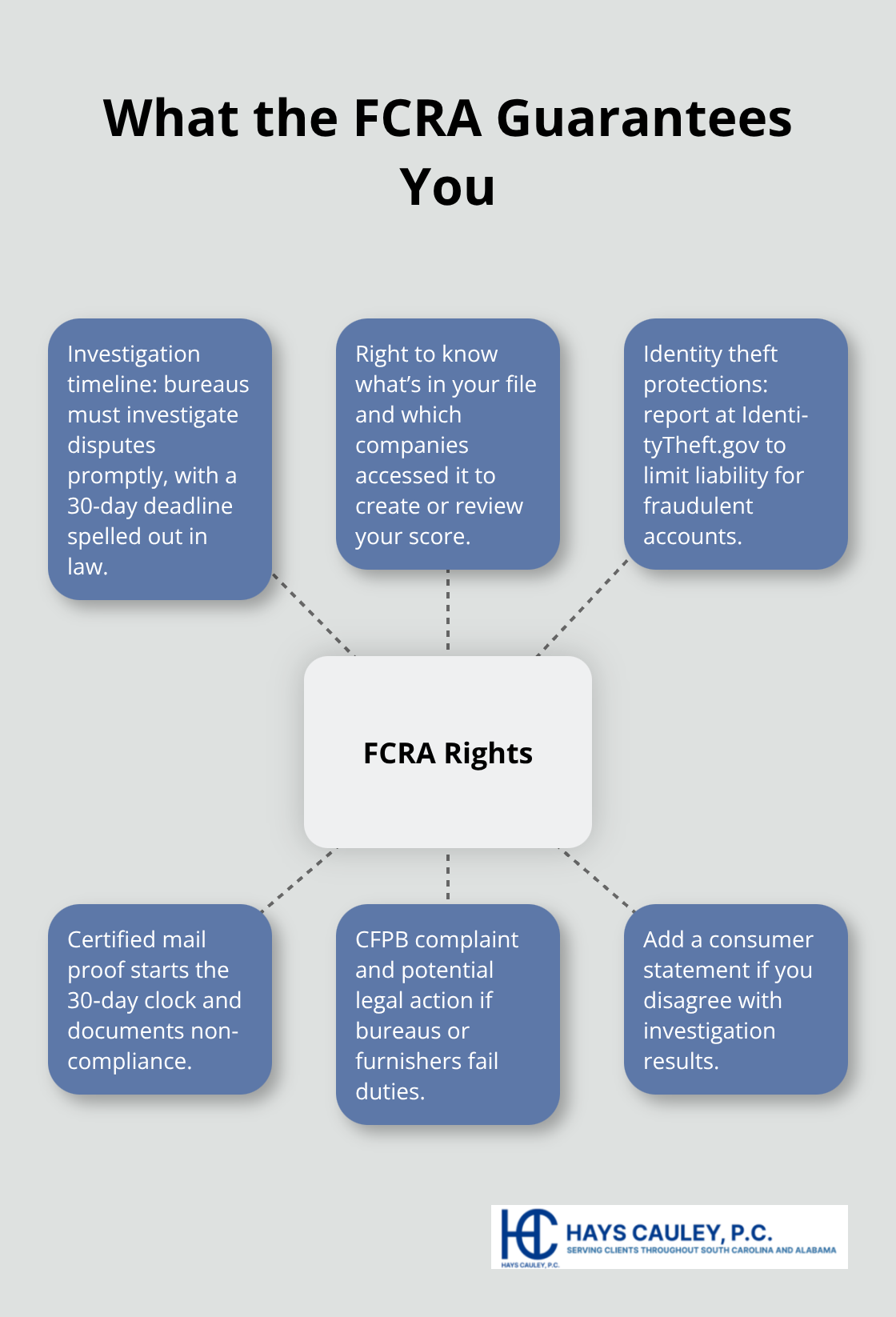

Federal law grants you specific rights when you fight credit report errors. The Fair Credit Reporting Act requires credit bureaus to investigate your dispute within 30 days and correct any information they cannot verify. This deadline is absolute-not a suggestion. If Equifax, Experian, or TransUnion fail to investigate or respond within this window, you have grounds to file a complaint with the Consumer Financial Protection Bureau or pursue legal action. You also have the right to know exactly what information the bureaus use to create your credit score and which companies access your file. When you request your credit report, you exercise this right.

The bureaus must disclose every account, payment history, collection, and inquiry on your file.

Identity Theft Protection and Furnisher Accountability

If information appears on your file that you didn’t authorize-such as accounts opened fraudulently-federal law protects you from liability once you report the identity theft at IdentityTheft.gov. The furnisher, the company that reported the error, holds equal responsibility for accuracy. If a creditor reports false information knowing it’s false, they violate the Fair Credit Reporting Act and can face legal consequences. This means when you contact a furnisher in writing and they ignore your dispute or refuse to investigate, that refusal itself may violate your rights.

Documentation Creates Verifiable Proof

The practical value of these protections lies in how you enforce them. Sending disputes by certified mail with return receipt creates documented proof that you submitted your claim on a specific date. The 30-day investigation clock starts when the bureau receives your dispute, so proof of receipt matters. If the bureau doesn’t respond within 30 days, you have evidence of non-compliance. Document every contact you make-dates, names of representatives, what was said, and what you sent. Keep copies of all dispute letters, supporting documents, and responses. This documentation transforms your complaint from a he-said-she-said situation into a verifiable record.

Escalation to the CFPB Increases Pressure

If disputes stall after 30 days with no resolution, file a CFPB complaint immediately. The CFPB received over 800,000 complaints related to credit and consumer reporting in under two years, and they track patterns of non-compliance by specific bureaus and furnishers. Your complaint becomes part of that record and increases pressure on the company to respond. Federal law also grants you the right to add a consumer statement to your file if you disagree with investigation results-a brief explanation of your position that appears alongside the disputed information. This statement doesn’t remove the error, but it signals to lenders that you contested the accuracy.

Build a Strong Position Through Multiple Actions

The strength of your position increases significantly when you combine three elements: thorough documentation, certified mail proof, and escalation to the CFPB when needed. These protections exist whether you handle disputes alone or work with a consumer protection law firm. The Fair Credit Reporting Act creates accountability at every stage of the dispute process, from the initial investigation to the final correction.

Final Thoughts

Credit report errors don’t fix themselves, and the longer inaccurate information sits on your file, the more damage it causes to your interest rates, loan approvals, and financial stability. You now understand where errors originate, how to spot them, and exactly what steps to take to correct them. The Fair Credit Reporting Act gives you concrete legal protections, and the 30-day investigation deadline creates real accountability for credit bureaus and furnishers.

Start this week by pulling your free credit report from AnnualCreditReport.com and review it carefully for misidentification, data entry mistakes, and outdated information. Document what you find, gather supporting evidence, and file disputes with each bureau by certified mail while also contacting the furnisher directly. Follow up consistently, and if disputes stall beyond 30 days, file a complaint with the Consumer Financial Protection Bureau.

Many credit reporting accuracy help situations resolve when consumers take these steps themselves, but some disputes become complicated when bureaus ignore deadlines, furnishers refuse to investigate, or errors persist across multiple attempts. If you’ve filed disputes and seen no progress, or if identity theft has damaged your file, we at Hays Cauley, P.C. can help you pressure unresponsive bureaus and hold furnishers accountable under federal law.