Credit Reporting Error Resolution: Your Path to Accuracy

A credit reporting error can tank your financial opportunities without warning. Lenders, landlords, and employers all rely on your credit report to make decisions about you.

We at Hays Cauley, P.C. help South Carolina residents tackle credit reporting error resolution head-on. This guide walks you through identifying errors, disputing them, and knowing when legal help makes sense.

Why Credit Reporting Errors Happen

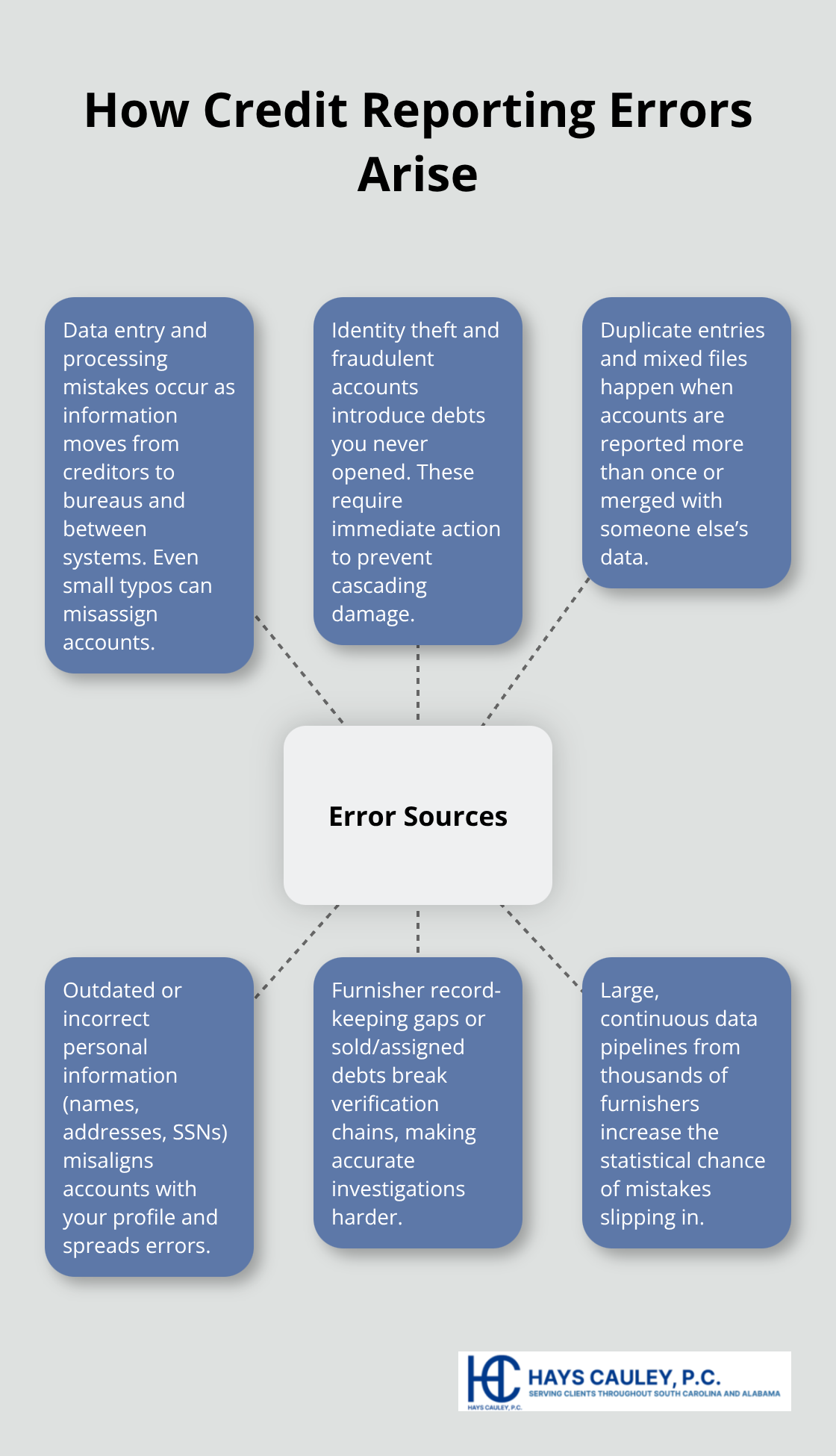

How Errors Enter the System

Credit reporting errors stem from multiple sources, and understanding where they originate helps you spot them faster. The three major credit bureaus-Equifax, Experian, and TransUnion-receive data from thousands of creditors, lenders, and collection agencies. Each data submission creates an opportunity for mistakes.

Equifax reported U.S. consumer credit report accuracy at 99.81% in February 2026, which sounds reassuring until you realize that even 0.19% error rate affects millions of people. The Federal Trade Commission found that roughly 1 in 5 consumers discovers an error on at least one credit report, making this far from a rare problem. When you consider that a single error can add roughly $103,626 in interest costs over a 30-year mortgage (according to Zillow’s analysis), accuracy matters enormously.

Common Types of Inaccurate Information

Inaccurate personal information ranks among the most common culprits-creditors enter wrong names, outdated addresses, or mismatched Social Security numbers into the system. These details may seem minor, but they cascade through your entire credit profile and confuse the bureaus about which accounts belong to you. Fraudulent accounts and identity theft create far more serious damage because they involve someone else opening credit in your name. If you spot unfamiliar accounts on your report, that’s a red flag for identity theft.

Duplicate Entries and Data Mixing

Duplicate entries and data mixing happen when the same debt appears multiple times or when accounts get merged with someone else’s information due to name similarities or matching Social Security numbers. These errors don’t disappear on their own-they require active intervention.

The Rising Complaint Trend

The CFPB received over 175,000 credit reporting complaints in 2020, and complaints have surged to nearly 5 million by 2025, signaling rising friction in the system. This surge reflects growing awareness among consumers that errors exist and that action produces results. About 70% of disputes result in some modification to your credit report, though many issues remain partially unresolved, making persistence essential throughout the process.

What Disputing Actually Takes

The dispute process can take 60 to 90 days or longer, especially if you’re dealing with multiple errors across all three bureaus. When disputing, you’ll need supporting documents like bank statements, receipts, and creditor correspondence organized by error. File disputes in writing using certified mail with return receipt to create a paper trail that protects you under the Fair Credit Reporting Act. The bureaus must investigate within 30 days, but furnishers (the businesses that reported the information) often drag their feet. If an item is unverifiable after investigation, the bureau must remove it entirely. Understanding these timelines and requirements positions you to move forward with confidence-and knowing when legal guidance helps accelerates your path to correction.

Steps to Identify and Dispute Credit Reporting Errors: Serving South Carolina, Including Greenville, Columbia and Charleston

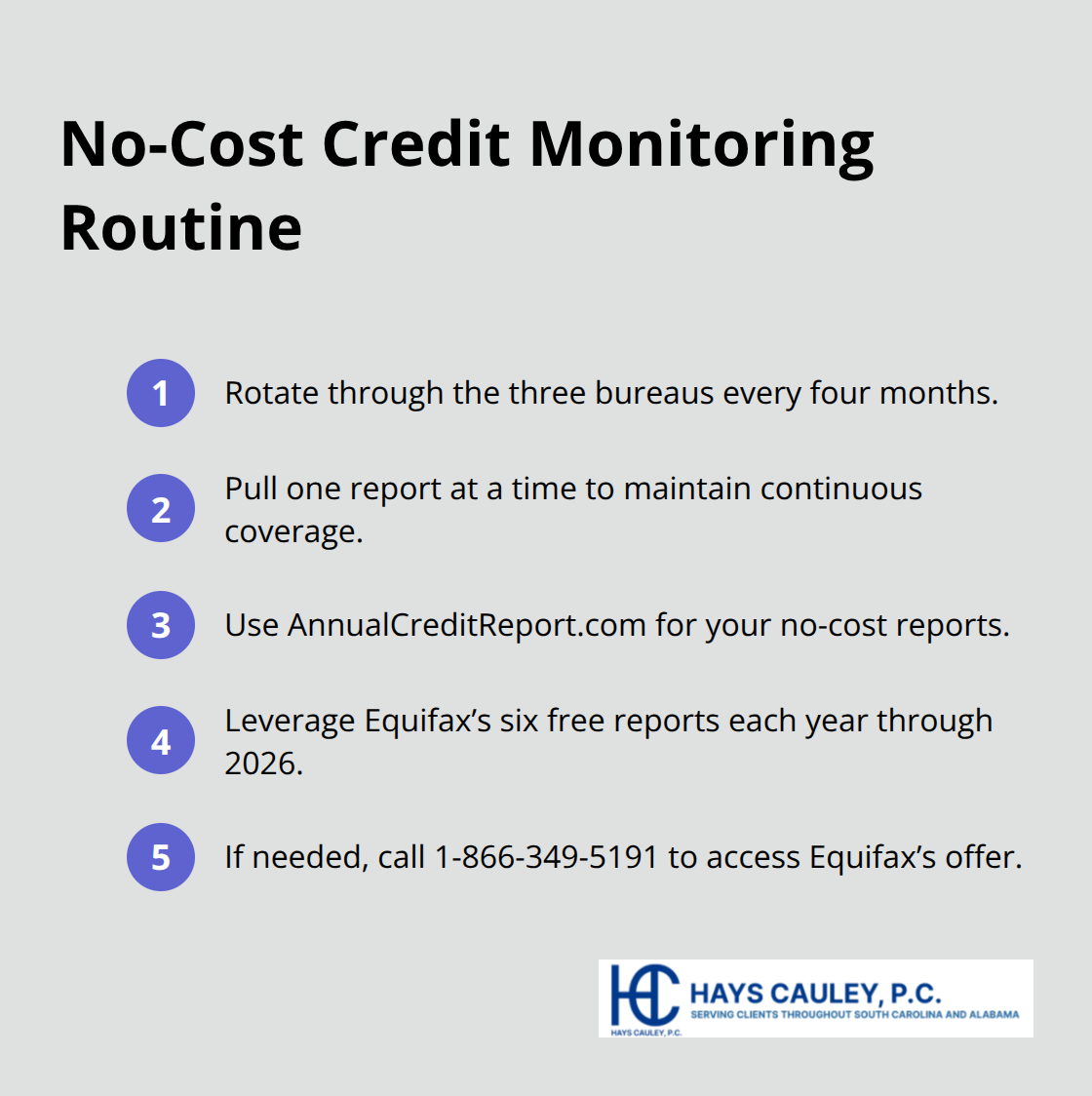

Request Your Free Annual Credit Report

Start by obtaining your credit reports from all three bureaus at annualcreditreport.com, which provides one free report per year from Equifax, Experian, and TransUnion. Waiting a full year between checks leaves errors undetected for months. Instead, rotate through the bureaus every four months, pulling one report at a time so you review your credit continuously without paying anything. Equifax has extended a program offering six free reports annually through 2026, accessible via their website or by calling 1-866-349-5191. These free options eliminate any barrier to action. You have no reason to skip this step.

Review Your Report for Inaccuracies

When your reports arrive, scan for unfamiliar accounts first, then check personal details like your name spelling, addresses, and Social Security number. Look at payment histories, balances, and credit limits closely. You should prioritize anything that doesn’t match your memory of your financial life. The Federal Trade Commission found roughly 1 in 5 consumers discovers an error on at least one report, so assume you might be one of them. Errors hide in plain sight, which is why careful review matters.

File a Dispute with the Credit Bureau

Once you identify an error, file your dispute in writing using certified mail with return receipt requested. This action creates a documented trail that protects you under the Fair Credit Reporting Act. You must gather supporting documents like bank statements, receipts, and correspondence from creditors, organizing each document by the specific error you challenge. The Consumer Financial Protection Bureau provides template letters that clearly identify each inaccuracy and state your requested correction. You should address your dispute to the bureau that holds the incorrect information, but also file with all three bureaus if the error appears on multiple reports.

Understand the Investigation Timeline and Results

The bureau must investigate within 30 days and report results in writing. If the furnisher cannot verify the information, the bureau must remove it entirely. About 70 percent of disputes lead to some modification of your report according to the CFPB, but many issues remain partially unresolved, which is why follow-up matters intensely. After you receive the investigation results, request an updated copy of your credit report to verify the correction actually appeared.

If the outcome isn’t fully satisfactory, you can add a brief statement to your credit report explaining your side of the story.

Know When to Escalate Your Dispute

If errors persist after initial disputes, you have options beyond the standard process. You can dispute directly with the furnisher and, if needed, seek legal assistance under the FCRA. If a bureau delays or fails to investigate as required, file a complaint with the Consumer Financial Protection Bureau. These escalation paths exist because some errors require more aggressive action than others-and that’s where understanding your legal rights becomes essential.

Working with a Consumer Protection Attorney: Serving South Carolina, Including Greenville, Columbia and Charleston

When Legal Help Becomes Necessary

Most credit reporting errors resolve through the standard dispute process, but some situations demand immediate legal intervention. If a bureau fails to investigate within 30 days, if corrected information reappears on your report, or if unverifiable items remain after investigation, you’ve hit a wall that requires professional guidance. The Fair Credit Reporting Act grants you specific legal remedies when bureaus or furnishers violate these requirements. Under the FCRA, willful violations entitle you to recover up to three times your actual damages or $3,000 per incident, plus reasonable attorney fees. Negligent violations may yield actual damages or at least $1,000, plus fees. These aren’t theoretical protections-they exist because Congress recognized that credit reporting errors cause real financial harm.

A consumer protection law firm understands how to document violations, build a case, and pressure bureaus and furnishers to comply with federal law. Identity theft situations also warrant immediate legal action. If you’ve placed a fraud alert on your reports and filed a police report, an attorney can coordinate these steps with formal dispute letters that signal serious intent. The CFPB reported nearly 5 million credit reporting complaints in 2025, yet many consumers never escalate beyond DIY disputes because they don’t understand when legal help actually pays off. Hiring representation costs money upfront, but recovering statutory damages, actual losses, and attorney fees often makes the investment worthwhile.

How Furnishers Must Respond to Your Disputes

Furnishers-the creditors, lenders, and collection agencies that reported information to bureaus-have legal obligations that most consumers never leverage. When a bureau forwards your dispute, the furnisher must conduct a reasonable investigation and report back within a specific timeframe. If they cannot verify the information, they must tell the bureau to remove it. Many furnishers ignore disputes or conduct perfunctory reviews, banking on the fact that consumers won’t pursue legal action. An attorney sends dispute letters that reference specific FCRA sections and document every violation, making clear that inaction carries legal consequences.

The furnisher’s investigation process often breaks down when they fail to maintain adequate records or when they’ve already sold the debt to another entity. These gaps in accountability create opportunities for legal action. A consumer protection law firm identifies where furnishers fall short and holds them accountable under federal law.

Your Rights Under Federal Law

The Fair Credit Reporting Act is your shield against inaccurate reporting and bureau negligence. You have the right to dispute errors, receive written investigation results, and demand removal of unverifiable items-these aren’t suggestions, they’re enforceable legal rights. If bureaus delay investigations, provide inadequate results, or fail to remove incorrect information, federal law allows you to pursue compensation. Many consumers settle disputes without realizing they could have recovered damages for the harm caused during the months their credit remained damaged.

Understanding your FCRA rights means recognizing when persistence alone won’t work and when legal representation becomes the practical choice. A consumer protection law firm helps South Carolina residents navigate these obstacles by understanding how furnisher systems work and where accountability gaps exist.

Final Thoughts

Credit reporting error resolution starts with action, not waiting. You now understand how errors enter the system, how to spot them, and what steps move you toward correction. The dispute process works-about 70 percent of disputes result in some modification to your credit report-but it demands persistence and documentation that you maintain throughout the entire process.

Your next step depends on where you stand right now. If you haven’t reviewed your reports in the past four months, pull them today and scan for unfamiliar accounts, wrong personal details, and payment histories that don’t match your records. If you’ve already spotted errors, file written disputes with certified mail and gather supporting documents to strengthen your case.

If disputes have stalled or if bureaus ignored your investigation requests, that’s when legal guidance becomes practical rather than optional. We at Hays Cauley, P.C. help South Carolina residents navigate credit reporting disputes and hold bureaus accountable when they violate federal law.