Inaccurate information on your credit report can damage your financial future. The Fair Credit Reporting Act gives you the right to challenge errors, but many people file weak disputes that get rejected.

We at Hays Cauley, P.C. help South Carolina residents navigate the FCRA dispute process effectively. This guide shows you exactly how to build a strong dispute that credit bureaus must take seriously.

Understanding Your Rights Under the FCRA – Serving South Carolina, Including Greenville, Columbia and Charleston

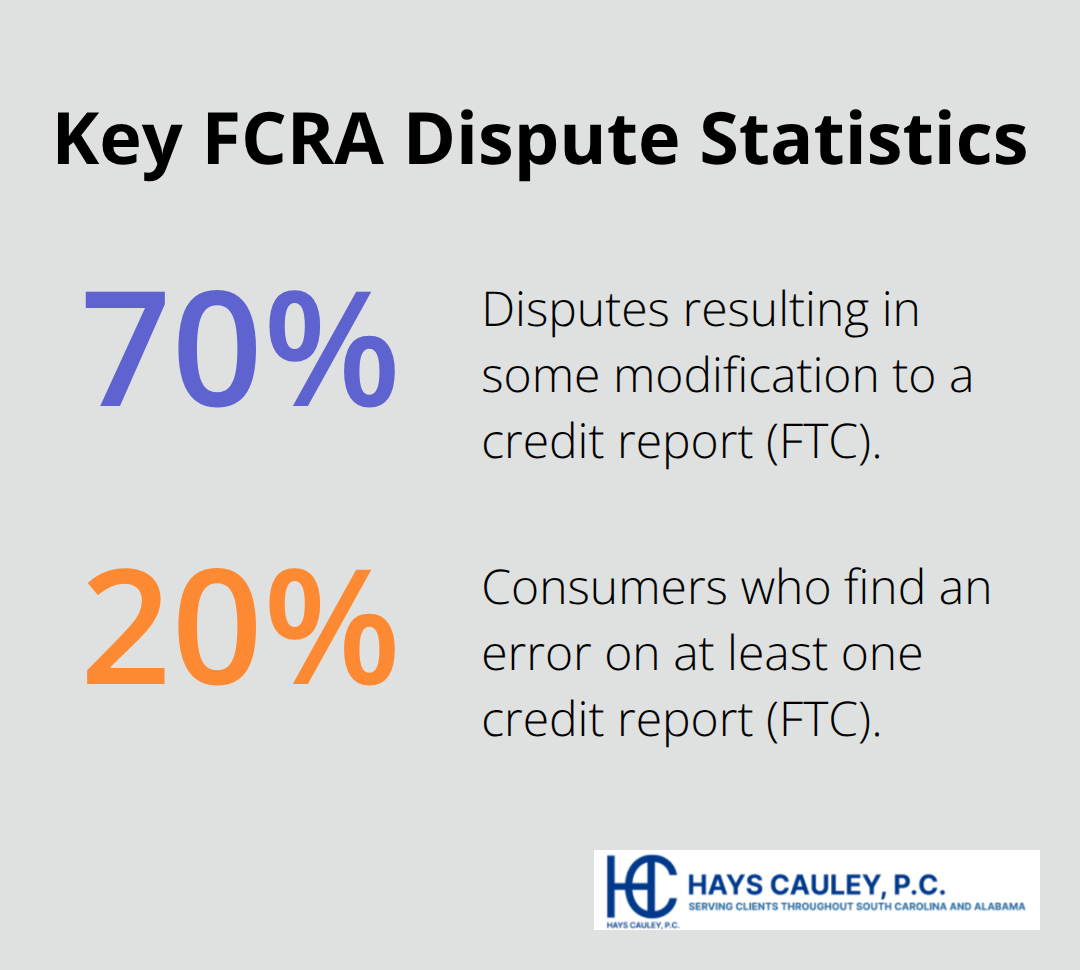

The Fair Credit Reporting Act is federal law with teeth, and credit bureaus know it. The FCRA gives you the right to dispute any information on your credit report that you believe is inaccurate, and the bureau must investigate your claim within 30 days. This isn’t optional for them-it’s mandatory. If they fail to investigate or ignore your dispute, you have grounds for legal action. The CFPB reported over 175,000 credit reporting complaints in 2020, and that number has exploded since then. In 2025, credit reporting complaints reached approximately 2.36 million in the second half of the year alone, with incorrect information on reports accounting for roughly 1.4 million of those complaints. This surge tells you something important: errors are common, and people are fighting back.

When you file a dispute, the bureau must also contact the furnisher-the company that reported the inaccurate data-and ask them to investigate. If the furnisher finds the information is wrong, they must notify all three major bureaus to correct it. You have the right to add a brief statement to your file if you disagree with the investigation results, and you can request an updated copy of your report to confirm corrections were made.

What You Can Challenge

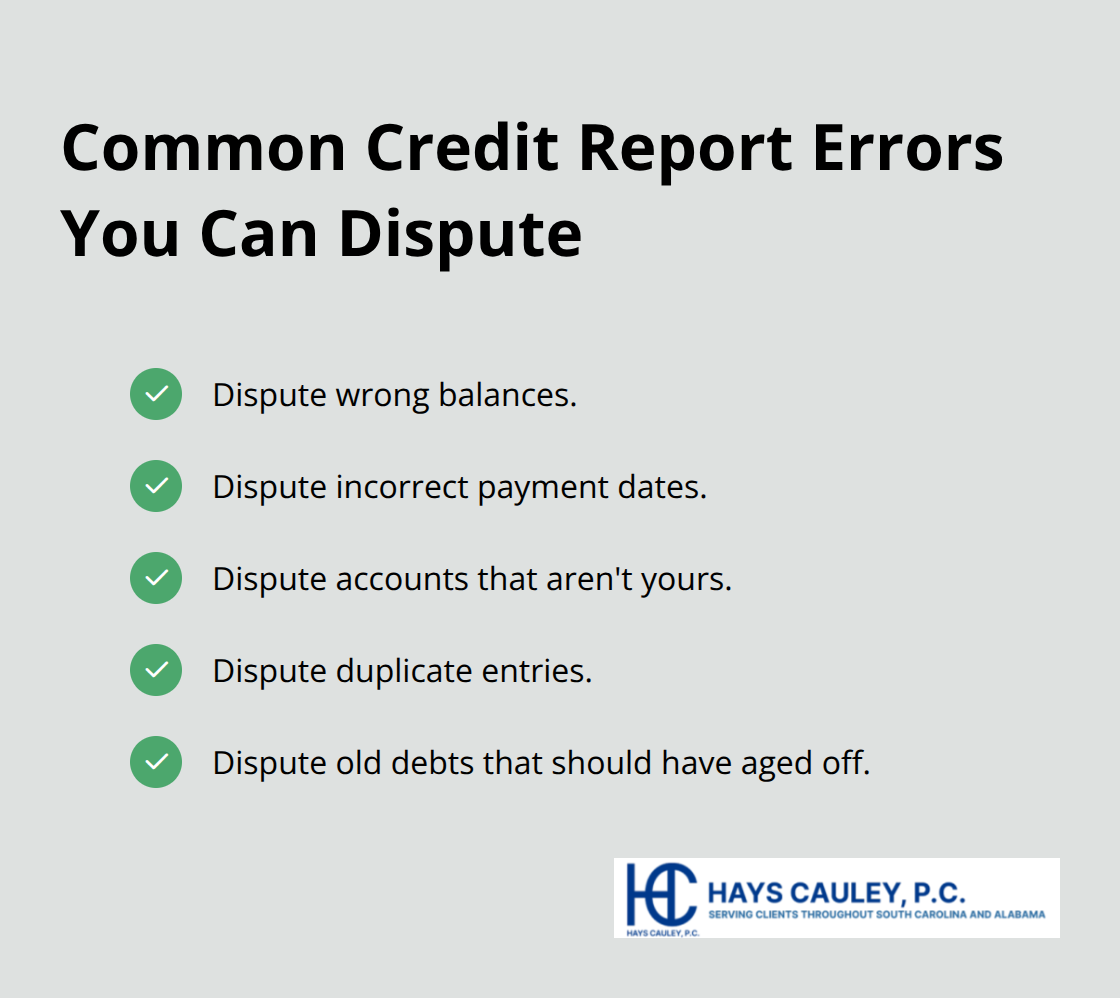

You can dispute anything that affects your creditworthiness: wrong balances, incorrect payment dates, accounts that aren’t yours, duplicate entries, or old debts that should have aged off. The FCRA is clear that furnishers must conduct a reasonable investigation of direct disputes if the error relates to your liability, account terms, payment performance, or other information affecting your credit. A Federal Trade Commission study found that about 20% of consumers discover an error on at least one credit report, so you’re not alone if you find problems.

How to Build Strong Evidence

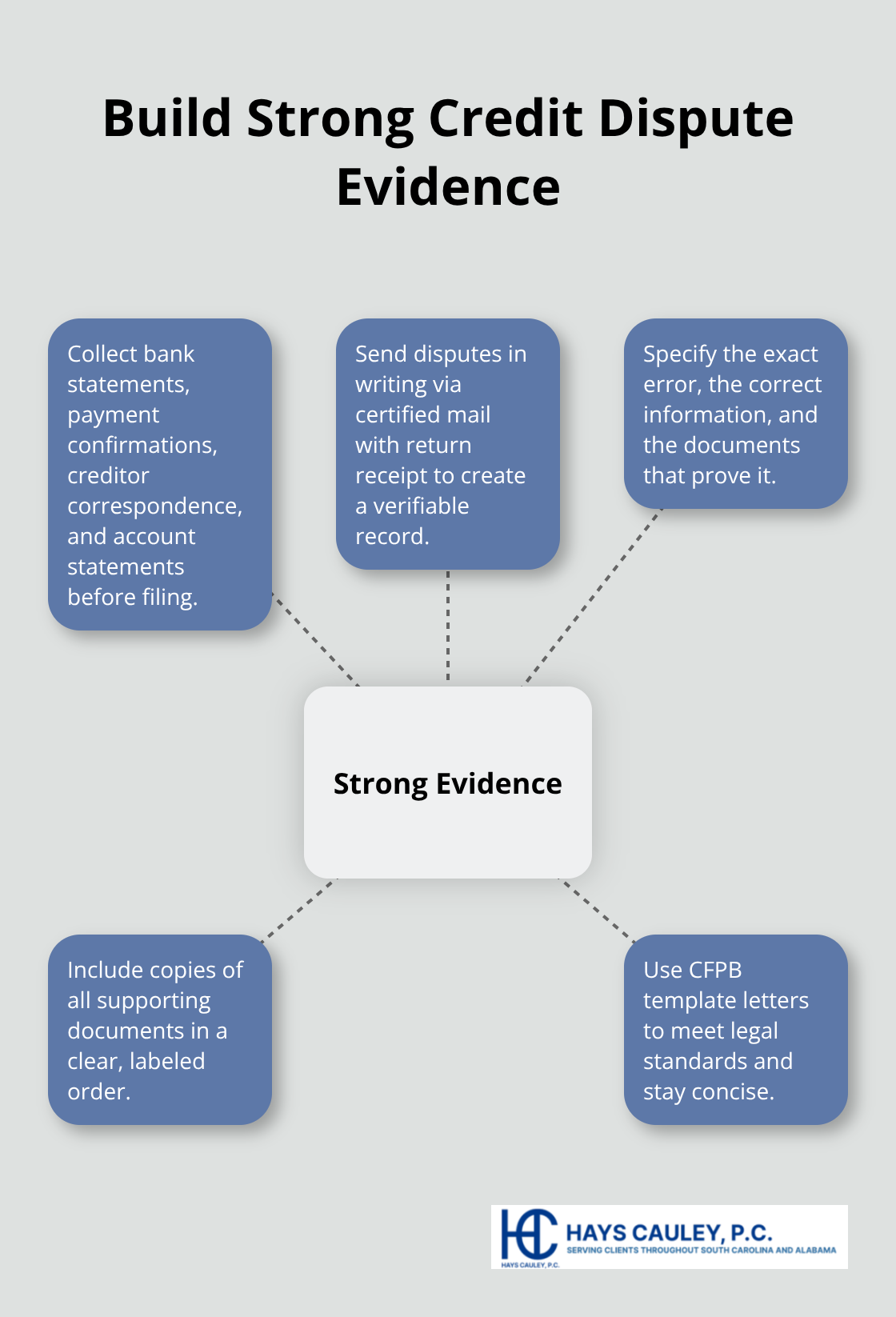

Strong evidence matters more than emotion. Collect bank statements, payment confirmations, creditor correspondence, and account statements before you file. About 70% of disputes result in some modification to a credit report, according to the FTC, though persistence matters-many cases remain unresolved on the first attempt. Send your dispute in writing via certified mail with return receipt, not by phone. Written records are stronger and easier to track. Include copies of your supporting documents and specify exactly what’s wrong and why.

The CFPB provides template letters to help you craft complete disputes that meet legal standards.

What Happens After You File

Credit bureaus have 30 days to investigate and send you results in writing. They must review all information you supplied with your dispute, and if they find inaccurate data, they must promptly notify each bureau they reported to and provide corrections. If a dispute is frivolous or irrelevant, they can skip the investigation but must notify you within five business days with their reasons. This is rare if you provide solid documentation.

If the investigation doesn’t resolve your issue, escalate by disputing directly with the furnisher. Send more detailed follow-up documentation. If the furnisher disputes your claim and the item remains on your report, you have options: add a brief explanatory statement to your file, file a complaint with the CFPB or FTC, or contact a consumer protection attorney. FCRA litigation rose 30.7% from 2024 to 2025, with lawsuits reaching 6,053 cases in the first nine months of 2025 alone. This trend shows that courts actively enforce FCRA rights when bureaus and furnishers fail to act properly. When errors persist despite your efforts, understanding your legal options becomes the next critical step in protecting your financial future.

Building Your Dispute Step by Step

Pull Your Reports and Create Your Baseline

You need to obtain your credit reports from all three bureaus-Equifax, Experian, and TransUnion-through AnnualCreditReport.com, the only authorized source for free annual reports. Save each report as a PDF or print it, then create a separate folder for each bureau. This baseline becomes your reference point for tracking what changes after you file your dispute.

Identify the Exact Error With Precision

Vague disputes get rejected or dismissed as frivolous. You must identify the specific error with clarity. Note the creditor name as it appears on the report, your account number, the specific field that’s inaccurate (such as a late payment date, balance, or status), and what the correct information should be. This precision matters because credit bureaus use it to locate the exact item in their system and investigate it properly.

Gather Your Supporting Documents

Pull bank statements showing payments you made, creditor correspondence confirming account status, payment confirmations from your bank or the creditor, and account statements from the creditor. If identity theft applies, include identity theft reports as well. The FTC found that about 70% of disputes result in some modification to a credit report, but disputes with solid documentation succeed faster and more completely than those without proof. Organize these documents in order by date, with each document labeled clearly.

Write and Submit Your Dispute Letter

You should write your dispute letter in plain language, not legalese. State the problem in one paragraph: identify the account, explain what’s inaccurate, and state what the correct information is. Keep it factual and short. Include your full name, current address, a copy of your government ID, and proof of address. Attach a highlighted copy of the report page showing the error, then attach your supporting documents in the order they occurred. Do not dispute everything at once without proof; overbroad disputes can be rejected.

Send your dispute via certified mail with return receipt to the bureau’s dispute address, and keep a copy of everything you send. Then send the same dispute package directly to the furnisher-the company that reported the information-using their designated direct-dispute address if they have one listed, or their business address if not. Furnishers must conduct a reasonable investigation of direct disputes and complete it before the credit bureau’s 30-day deadline expires. This parallel approach speeds correction because you apply pressure from both sides.

Track Your Progress and Verify Results

Document your submission date, save your certified mail receipt or delivery confirmation, and set a calendar reminder to check your reports 45 days after filing to verify corrections were made. Credit bureaus have 30 days to investigate and send you results in writing. They must review all information you supplied with your dispute, and if they find inaccurate data, they must promptly notify each bureau they reported to and provide corrections. If the investigation doesn’t resolve your issue, you have options that require understanding what happens when bureaus and furnishers fail to act properly.

What Weakens Your Dispute and How to Avoid It

Vague Language Gives Bureaus an Excuse to Reject Your Claim

Weak disputes fail because they lack precision and proof. The most common mistake is writing vague language that gives credit bureaus an excuse to dismiss your claim as frivolous. Instead of saying the balance is wrong, you must state the exact balance shown on your report, the correct balance you can prove, and the date of the supporting document showing the correction. If your dispute letter says only that a payment date is inaccurate without specifying which payment or providing bank statements to back it up, the bureau can reject it within five business days without investigating. The CFPB data from 2025 shows that incorrect information on reports drove roughly 1.4 million of 2.36 million complaints, yet many of these disputes fail on the first attempt because consumers don’t document the specific error clearly enough for the bureau to locate and investigate the exact item in their system.

Missing Supporting Documentation Slows Resolution

Missing supporting documentation is the second reason disputes fail. Sending a dispute letter without bank statements, creditor correspondence, or payment confirmations is like asking someone to fix a problem without showing them what’s broken. You must attach copies of the exact documents that prove the error and show what the correct information should be. If you claim a late payment was reported incorrectly, include the bank statement showing the payment was made on time, the creditor’s own account statement confirming the payment date, or a letter from the creditor acknowledging the correction. The FTC found that about 70% of disputes result in some modification to a credit report, but this statistic masks a harder truth: disputes with solid documentation resolve faster and more completely than those without proof.

Passive Waiting After Submission Costs You Momentum

Failing to follow up after submission costs you momentum and proof. Many people file a dispute and then wait passively, hoping the bureau will correct it. Instead, you must track when you submitted your dispute, verify that the bureau received it, and check your credit report 45 days later to confirm corrections were made. If the item remains unchanged, send a second dispute directly to the furnisher with even more detailed documentation. Keep dated records of every submission, every response letter, and every follow-up attempt. This paper trail becomes critical if you later need to file a complaint with the CFPB or FTC or if you need to work with a consumer protection attorney to enforce your rights.

Final Thoughts

Filing a strong FCRA dispute process requires precision, documentation, and persistence. You now understand that vague claims get rejected, missing evidence slows resolution, and passive waiting costs you momentum. The steps we’ve outlined-pulling your reports, identifying exact errors, gathering supporting documents, writing clear dispute letters, and tracking results-form a proven path to correcting inaccurate information on your credit report.

Credit bureaus and furnishers count on consumers giving up after the first attempt. About 70% of disputes result in some modification to a credit report, but many people never reach that outcome because they don’t follow through. The CFPB received 2.36 million credit reporting complaints in the second half of 2025 alone, with incorrect information driving roughly 1.4 million of those complaints. This tells you that errors are widespread and that fighting back works when you do it correctly.

When errors persist despite your documented efforts, or when identity theft complicates your situation, working with a consumer protection attorney becomes the logical next step. We at Hays Cauley, P.C. help South Carolina residents navigate credit reporting disputes and enforce their rights under federal law. If you’ve filed disputes and the bureaus or furnishers have failed to investigate properly, ignored your claims, or refused to correct errors, contact Hays Cauley, P.C. to discuss your situation and explore whether your rights under the FCRA were violated.