Your credit report shapes your financial life, yet many people don’t understand their rights under the Fair Credit Reporting Act. Errors on your report can cost you thousands in higher interest rates or denied loans.

We at Hays Cauley, P.C. created this guide to show you exactly what protections the law gives you, what you’re responsible for, and how to fight back when things go wrong. Serving South Carolina, including Greenville, Columbia and Charleston, we help people reclaim control of their credit information.

What the Fair Credit Reporting Act Actually Protects

Three Core Rights That Shape Your Financial Future

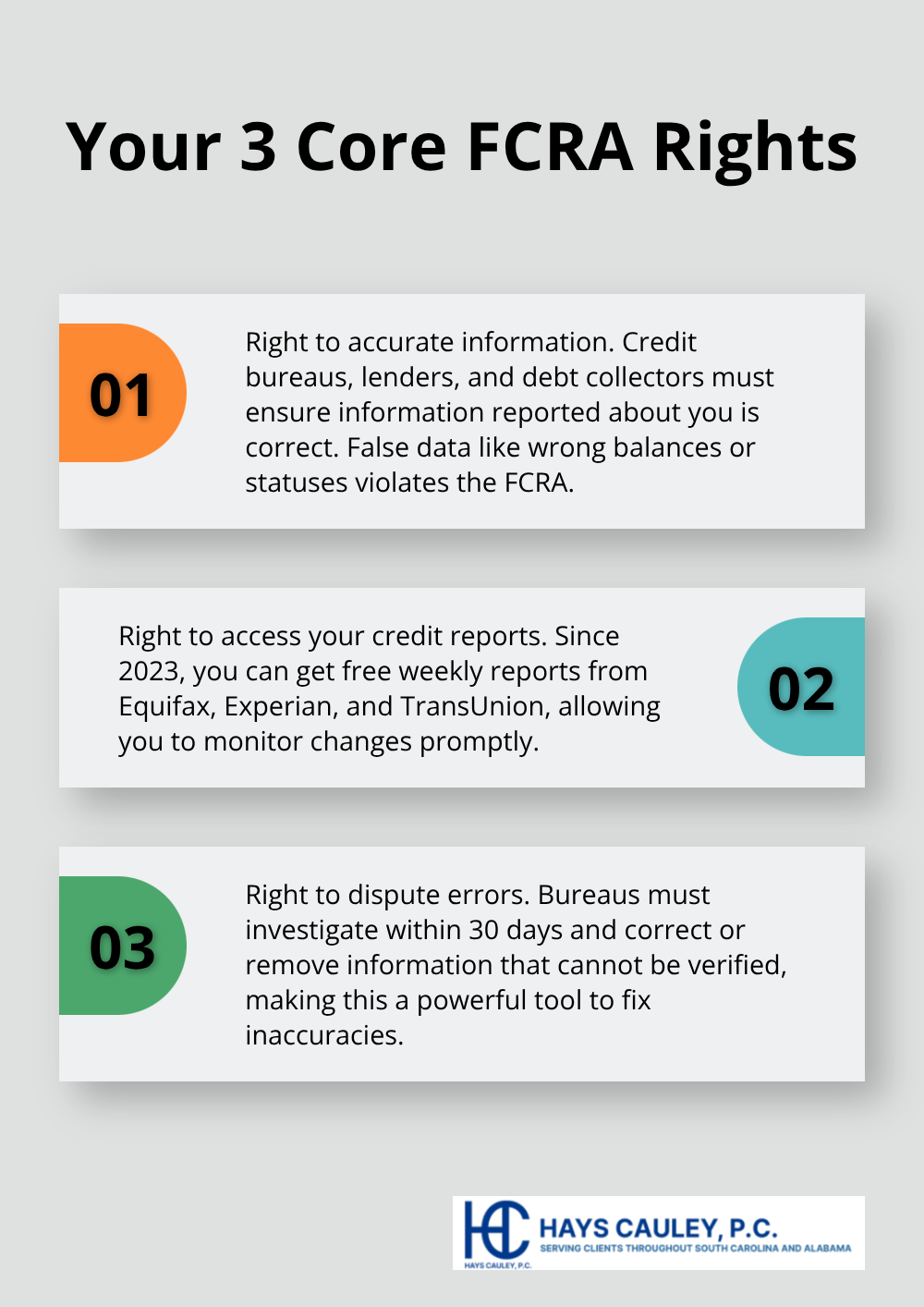

The Fair Credit Reporting Act, enacted in 1970, gives you three concrete protections that directly affect your financial health. First, you have the right to accurate credit information. Lenders, credit bureaus, and debt collectors cannot report false data about you. If Equifax, Experian, or TransUnion includes wrong account balances, incorrect delinquency statuses, or settled debts still marked as active, those are violations. Second, you have the right to access your credit report. Since 2023, the three major credit bureaus offer free weekly reports, not just the annual report mandated by law. Third, you have the right to dispute errors. When you find inaccurate information, the credit bureau must investigate within 30 days and remove or correct anything that cannot be verified. This requirement is not optional for them-it is a legal obligation.

Why Accuracy Directly Impacts Your Wallet

Accuracy matters because your credit report determines whether you get loans, what interest rates you pay, and sometimes whether you get hired. A single wrong entry costs you thousands in higher interest rates or triggers loan denials. The FCRA restricts who can access your report to those with a legitimate purpose-lenders evaluating credit applications, employers with your written consent, landlords conducting tenant screenings, and insurers assessing risk. If someone accesses your report without authorization, that violates the law. Negative information typically stays on your report for seven years, giving you a clear window for recovery. If an error appears, disputing it immediately prevents long-term damage to your creditworthiness.

The Adverse Action Notification Requirement

The law requires that if a credit decision against you is based on your report, the creditor must notify you of the adverse action and tell you which bureau provided the information. This notification gives you the chance to review the data and correct inaccuracies before they harm future applications. You can pull your reports at AnnualCreditReport.com or call 1-877-322-8228 to monitor what lenders and employers see about you. Taking action on errors quickly prevents them from compounding over months or years. Understanding these three protections forms the foundation for knowing when violations occur and what remedies you can pursue.

Your Responsibilities Under the Fair Credit Reporting Act: Serving South Carolina, including Greenville, Columbia and Charleston

Provide Accurate Information From the Start

The FCRA gives you strong protections, but you also carry responsibilities that directly shape how your credit report looks and functions. The most critical responsibility is providing accurate information to creditors from the beginning. When you apply for credit, the information you submit becomes part of your financial record. If you intentionally provide false income, employment history, or personal details on a credit application, you create a foundation for errors that cascade through your credit file. More importantly, inaccurate information you provide gives creditors and bureaus bad data to report, which then requires you to spend time disputing later.

The FTC reports that incorrect personal information like wrong addresses or misspelled names accounts for a significant portion of credit report disputes. You control what goes into your initial application, so accuracy at that stage prevents months of correction work later. When creditors report your account activity to the bureaus, they rely on the data you provided during application. If your Social Security number is wrong or your employment information is false, the bureau cannot match it correctly to your file, creating duplicate accounts or merged records that are nearly impossible to untangle.

Check Your Reports Every Four Weeks

Monitoring your credit report regularly is not optional if you want to catch errors before they damage your score. Pull your free weekly reports from AnnualCreditReport.com and check three specific areas: your personal information for wrong addresses or names, your account history for accounts you did not open or incorrect balances, and your inquiries for unauthorized access attempts. The Consumer Financial Protection Bureau receives thousands of credit reporting complaints annually, with many stemming from errors that went undetected for months or years.

When you wait six months to review your report, inaccurate information has already affected multiple credit decisions. Set a calendar reminder to check one bureau every four weeks so you rotate through all three and catch problems quickly. This simple habit prevents small errors from becoming major obstacles to loans, housing, or employment.

Know Who Accesses Your Credit Information and Why

Understanding how your credit information is used means knowing that lenders see your full report, employers with your written consent see it, landlords pull it during tenant screening, and insurance companies access it to set rates. Each of these entities makes decisions based on what the bureaus report, so a single error affects your loan terms, job prospects, housing options, and insurance costs simultaneously. The FCRA places the burden on you to monitor and dispute, not on creditors to volunteer corrections.

When you understand these responsibilities, you recognize that errors do not fix themselves. The bureaus will not contact you to correct mistakes, and creditors will not alert you to inaccurate reporting. You must take action. This active role in protecting your credit information becomes your strongest defense against the financial damage that inaccurate reports cause. Once you understand what you must do, you need to know what happens when violations occur and what remedies the law provides to you.

Remedies Available When Your Rights Are Violated

File a Dispute Directly With the Credit Bureau

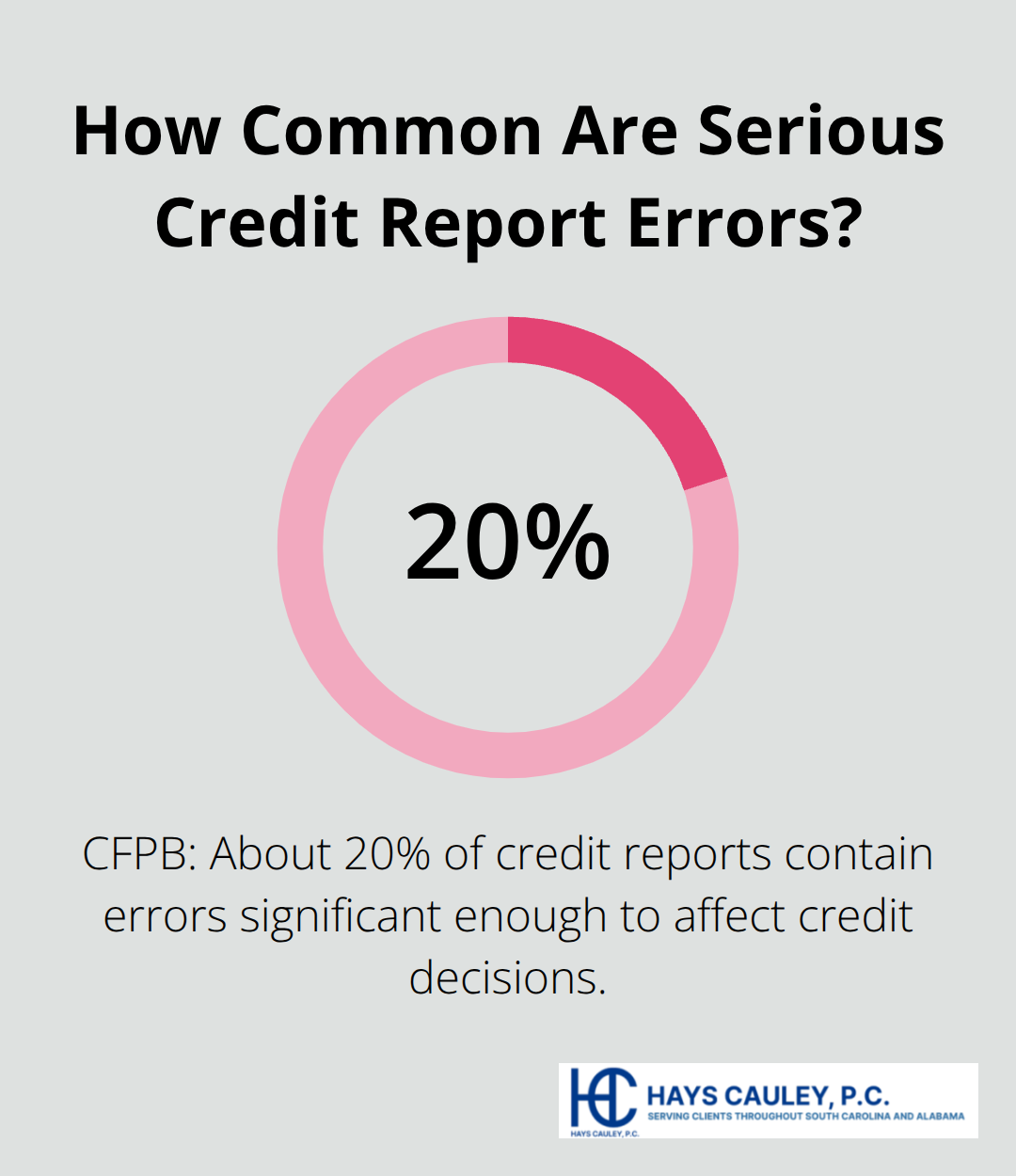

When a credit bureau reports inaccurate information, your first step is filing a dispute directly with the bureau that posted the error. Contact Equifax, Experian, or TransUnion through their online dispute centers and provide specific details about what is wrong. The FCRA requires them to investigate within 30 days and remove anything they cannot verify. Upload supporting documents like account statements, payment receipts, or correspondence showing the account was paid or closed. Track your dispute status through their portal because bureaus often delay investigations. If the bureau does not correct the error within 30 days, send a written follow-up letter via certified mail demanding reinvestigation. Many consumers stop after the first dispute attempt, but persistence works. The Consumer Financial Protection Bureau reports that about 20 percent of credit reports contain errors significant enough to affect credit decisions, so pushing back on inaccurate entries directly protects your financial future.

Escalate Your Case to the Consumer Financial Protection Bureau

If the bureau refuses to correct verifiable errors or ignores your dispute entirely, file a complaint with the Consumer Financial Protection Bureau at consumerfinance.gov. The CFPB investigates violations and compiles data showing which bureaus and creditors violate the FCRA most frequently. Include your dispute documentation, proof the error remains on your report, and a clear explanation of financial harm you suffered from the inaccuracy. The CFPB takes these complaints seriously because they track patterns of violations across thousands of consumers.

Pursue Legal Action for Substantial Damages

When disputes and CFPB complaints do not resolve violations, legal action becomes necessary. Willful violations under the FCRA allow you to recover statutory damages of $100 to $1,000 per violation plus actual damages, punitive damages, and attorney fees. Negligent violations allow recovery of actual damages and attorney fees. You can file suit in federal or state court, and the statute of limitations gives you two years from discovery of the violation or five years from the violation date, whichever is sooner. Courts have ordered settlements exceeding hundreds of thousands of dollars in cases where bureaus systematically reported false information or ignored disputes.

Build a Strong Legal Case With Documentation

The strongest cases involve documented proof of inaccuracy, evidence the bureau failed to investigate your dispute properly, and clear financial harm from the reporting error. If you face repeated FCRA violations or systematic errors across multiple accounts, legal remedies often provide the leverage needed to force correction and compensation that disputes alone cannot achieve. A consumer protection law firm understands that taking legal action requires understanding exactly what damages you qualify for and how courts calculate compensation.

Final Thoughts

Your credit report controls access to loans, employment, housing, and insurance rates, making accuracy non-negotiable under the Fair Credit Reporting Act. Pull your free weekly reports from AnnualCreditReport.com and check for wrong addresses, unauthorized accounts, and incorrect balances every four weeks. When you find errors, dispute them immediately with the credit bureau and document everything.

Legal action becomes your strongest option when disputes fail. Willful violations under the Fair Credit Reporting Act allow you to recover statutory damages of $100 to $1,000 per violation plus actual damages, punitive damages, and attorney fees. Courts have ordered settlements exceeding hundreds of thousands of dollars in cases where bureaus systematically reported false information, and you have two years from discovery of the violation or five years from the violation date to file suit.

If you face credit reporting violations or need guidance navigating disputes, Hays Cauley, P.C. helps consumers with credit reporting, identity theft, and debt-related issues. We serve South Carolina, including Greenville, Columbia, and Charleston. Contact us today to protect your financial future.