Identity theft victims in SC face a daunting road to recovery, but the process is manageable when you know the right steps. We at Hays Cauley, P.C. have helped countless South Carolinians reclaim their credit and financial security.

This guide walks you through the immediate actions you need to take, how to repair the damage, and how to protect yourself going forward.

Act Fast to Stop the Damage

The first 24 to 48 hours after discovering identity theft are critical. Contact the Federal Trade Commission at IdentityTheft.gov to file an official identity theft report. This report creates a documented record that protects you legally and signals to creditors that you are a victim, not a deadbeat borrower. The FTC does not investigate individual cases, but your report becomes part of the FTC’s database and gives you legal standing to dispute fraudulent accounts. After filing, you will receive an Identity Theft Report number-save this number because you will need it for every dispute and communication with creditors and credit bureaus.

Place a Fraud Alert Immediately

Call one of the three major credit bureaus-Equifax, Experian, or TransUnion-and request a fraud alert on your credit file. You only need to contact one bureau; that bureau must notify the other two. A fraud alert tells lenders to verify your identity before opening new accounts or issuing credit, which stops most thieves cold since they will not pass identity verification. The initial fraud alert lasts one year at no cost. If you want stronger protection, request an extended fraud alert, which lasts seven years and requires written confirmation. Some fraud victims also file a police report with local law enforcement; while police rarely pursue individual identity theft cases, a police report number strengthens your credibility with creditors and credit bureaus when disputing fraudulent accounts.

Freeze Your Credit Before Anything Else

A credit freeze is your most powerful defense. Contact Equifax, Experian, and TransUnion separately to freeze your credit file with each bureau. A freeze blocks access to your credit report, making it nearly impossible for thieves to open new accounts in your name because lenders cannot see your credit file to approve new credit. Freezes are free in South Carolina and take effect within one business day. You will receive a PIN or password for each bureau-write these down and store them securely because you will need them later to unfreeze your credit when you apply for legitimate new accounts.

Do not skip this step thinking a fraud alert is enough; freezes are far more effective at preventing new account fraud, which is the most common damage identity thieves cause.

Document Everything and Gather Evidence

Start collecting documentation immediately. Gather copies of your FTC Identity Theft Report, police reports (if filed), and all correspondence with credit bureaus and creditors. Take screenshots of unauthorized accounts and fraudulent charges appearing on your statements. Write down dates, times, and names of anyone you speak with at financial institutions or credit bureaus, along with what they told you. This documentation becomes essential if you later need to pursue legal action or file disputes with creditors. The paper trail you create now will support your claims and demonstrate that you took prompt action to stop the fraud.

Repair Your Credit Report and Remove Fraudulent Accounts

Get Your Credit Reports from the Right Source

Request your free credit reports from Equifax, Experian, and TransUnion immediately at AnnualCreditReport.com, the only authorized source for free reports under federal law. Third-party sites that offer free reports often bundle credit monitoring services you do not need and complicate your recovery process. When your reports arrive, print them and read every entry carefully. Look for accounts you did not open, credit inquiries you did not authorize, and balances that do not match your records.

The Federal Trade Commission reports that inaccurate information appears on roughly one in five credit reports, but identity theft victims see far worse damage. Highlight every fraudulent entry with a pen and create a separate document listing the account number, creditor name, fraudulent balance, and the date you discovered it. This list becomes your roadmap for disputing.

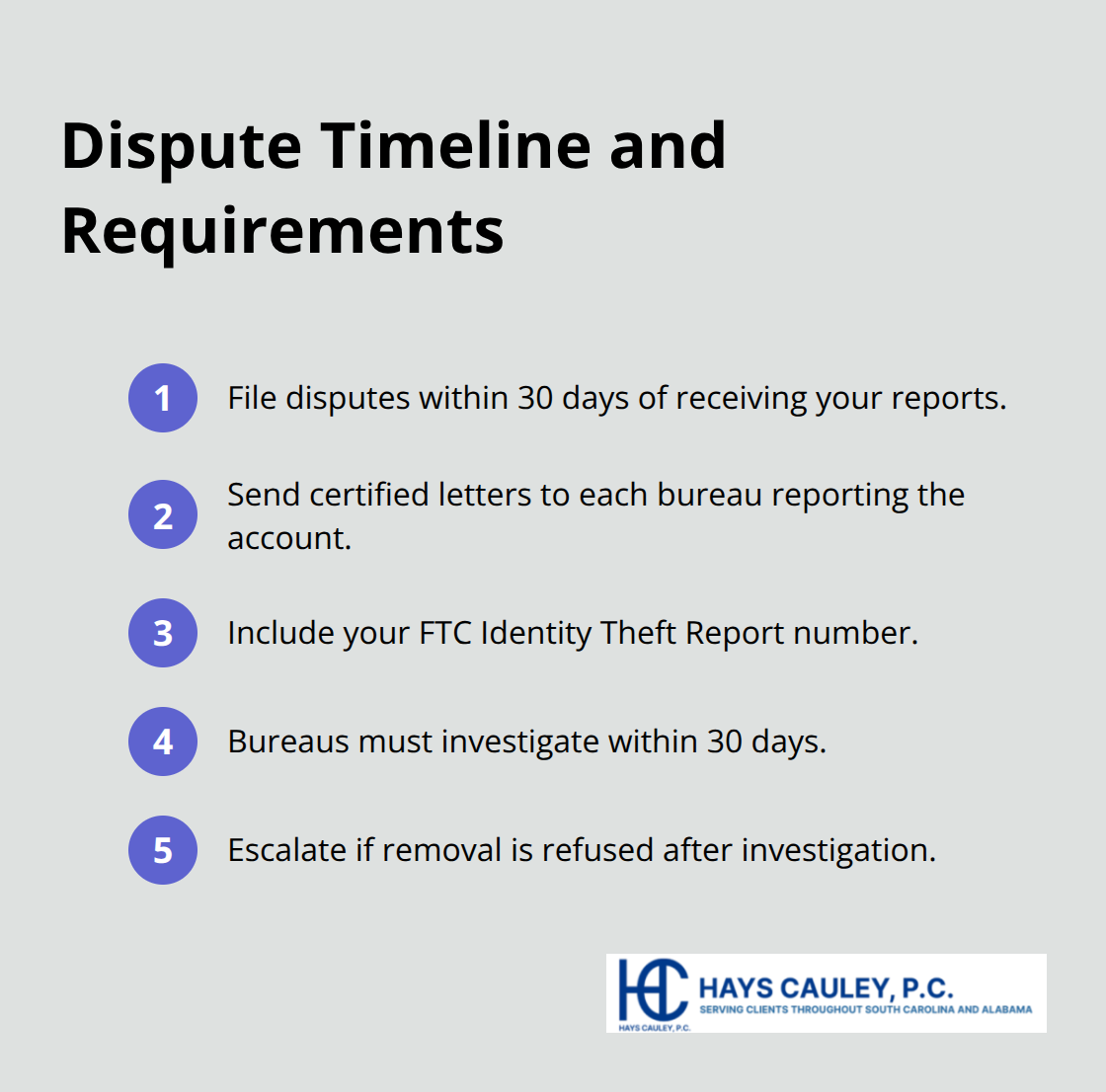

File Written Disputes Within 30 Days

Start disputes with the credit bureaus within 30 days of receiving your reports; the Fair Credit Reporting Act gives you 30 days from when you receive your report to file disputes, and acting within this window strengthens your legal position. Send written disputes to each bureau that shows the fraudulent account, not phone calls or emails. Certified mail with return receipt is non-negotiable because you need proof the bureau received your dispute.

In your letter, state that you did not authorize the account and that it is fraudulent due to identity theft. Include a copy of your FTC Identity Theft Report number. The credit bureau must investigate within 30 days and remove unverified accounts from your report. If a bureau drags its feet or refuses to remove a clearly fraudulent account after investigation, that creditor or bureau may face liability under the Fair Credit Reporting Act.

Contact Creditors Directly in Writing

Simultaneously, contact the creditor directly in writing and state that the account is fraudulent. Send the same certified letter with your FTC report number. Many creditors will close fraudulent accounts without much pushback because they know liability exposure when they see it. Do not expect the creditor to remove the account from your credit report immediately; the creditor reports to the bureaus, and the bureaus must update your report after they verify the account is fraudulent.

This process typically takes 30 to 90 days per account. If you have multiple fraudulent accounts, stagger your dispute filings by a week or two so you can track which bureau is responding to which dispute.

When Creditors Refuse to Correct Errors

If a creditor or bureau refuses to correct a verified fraudulent account, you may have grounds to pursue a civil claim in South Carolina courts. The Fair Credit Reporting Act and South Carolina’s identity theft statutes provide remedies including actual damages, statutory penalties, and legal costs. Willful or malicious conduct can result in punitive damages as well. Hays Cauley, P.C. handles disputes at every stage, from drafting letters to pursuing legal claims against creditors or bureaus that refuse to correct verified errors.

Protecting Your Credit While You Recover

Monitor Your Credit Reports and Accounts Regularly

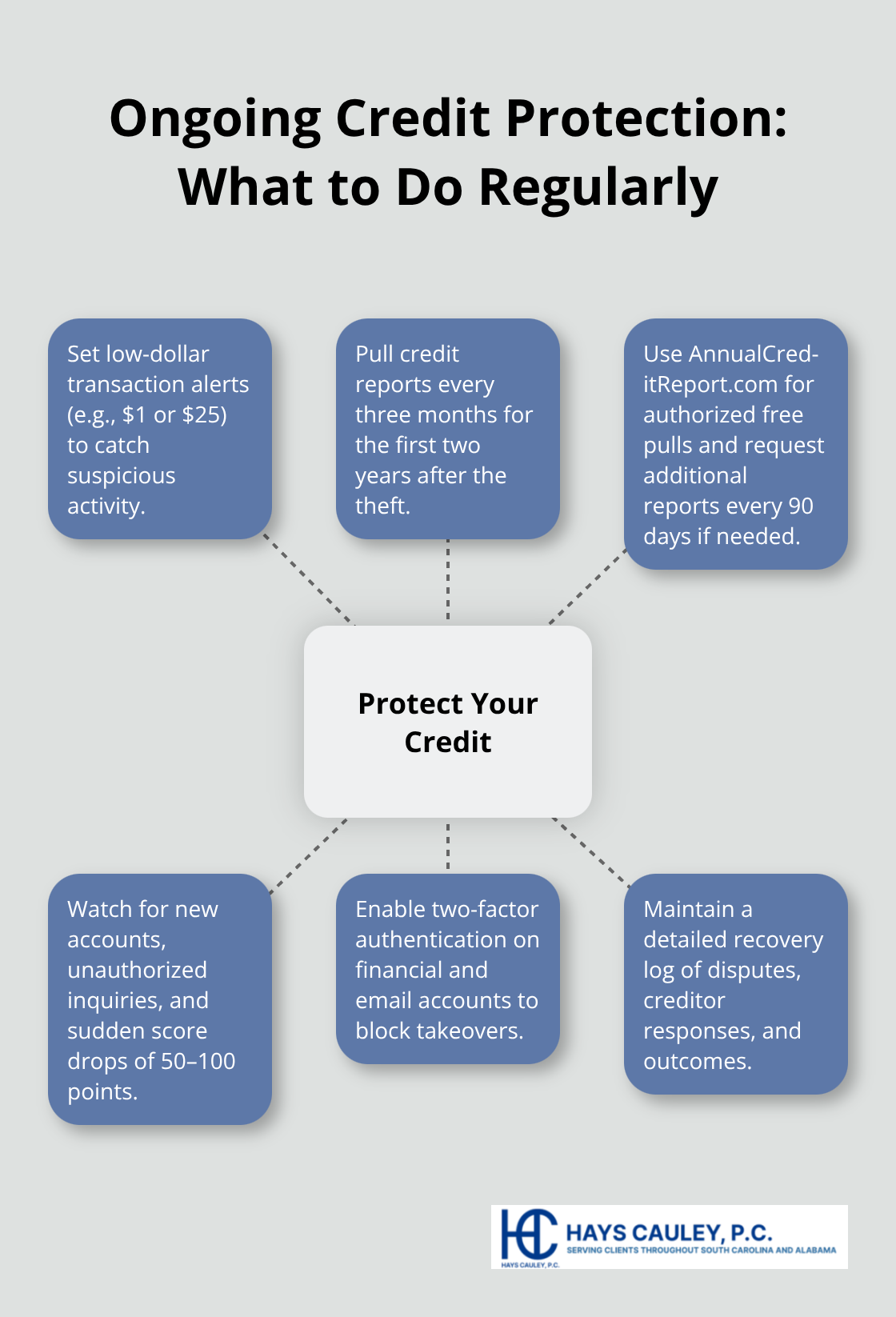

Credit monitoring acts as your early warning system for new fraud. Set up account alerts with your bank and credit card issuers so you receive notifications for any transaction over a small amount, typically $1 or $25 depending on the bank. The Federal Trade Commission recommends checking your credit reports at least once per year, but identity theft victims should pull reports every three months for the first two years after the theft. Use AnnualCreditReport.com for free pulls; you are entitled to one free report per bureau annually, but victims can request additional reports every 90 days without penalty.

Watch for new accounts you did not open, new inquiries from lenders you never contacted, and sudden drops in your credit score. A score drop of 50 to 100 points signals fraudulent activity, particularly when paired with new accounts or late payments on accounts you know you paid on time.

Strengthen Your Passwords and Enable Two-Factor Authentication

Passwords are the gatekeepers to your financial life, yet most people reuse the same weak password across multiple sites. Change every password for your bank, credit card company, email, and any financial account immediately after discovering identity theft. Make passwords at least 16 characters long and include uppercase letters, numbers, and symbols-thieves using common password-cracking software cannot break these quickly.

Enable two-factor authentication on every account that offers it, including your email, bank, and credit card portals. Two-factor authentication means a thief needs both your password and a code sent to your phone or generated by an authenticator app like Google Authenticator or Authy, making account takeover far harder. The National Institute of Standards and Technology now recommends authenticator apps over text messages because text messages can be intercepted through SIM swap attacks.

Seek Legal Help When Creditors Resist

If your case involves multiple fraudulent accounts, significant financial loss, or creditors refusing to remove verified fraud from your report, working with a consumer protection attorney becomes necessary. Hays Cauley, P.C. handles these cases from start to finish, negotiating with creditors and pursuing legal claims when creditors or bureaus refuse to correct errors. Serving South Carolina, including Greenville, Columbia and Charleston, we understand the state-specific laws that give you leverage in recovery. Contact us for a confidential case review if you face resistance from creditors or need guidance on whether to pursue legal action.

Final Thoughts

Recovery from identity theft takes months, not weeks, and identity theft victims in SC should expect credit score improvement to take six months to two years depending on the extent of the fraud. Keep a recovery log that documents every dispute you file, every creditor you contact, and every response you receive, including dates, names, reference numbers, and outcomes. This log becomes invaluable if you need to prove you acted diligently or if you later pursue legal claims against creditors or bureaus that fail to correct errors.

Your credit score will not bounce back overnight, but fraudulent accounts lose their impact over time as you build positive payment history. Most victims see meaningful score recovery within 12 to 18 months of removing fraudulent accounts, assuming no new fraud occurs. Set monthly check-ins to review your credit reports and track progress, celebrating small wins like seeing a fraudulent account removed or watching your score climb 20 points.

Prevention protects you after recovery ends. Do not carry your Social Security number in your wallet, shred pre-approved credit card offers before disposal, and use strong passwords with two-factor authentication on all accounts going forward (monitor your credit reports quarterly for two years, then annually after that). If creditors or bureaus resist your efforts to correct fraud, Hays Cauley, P.C. can guide you through the legal process and hold negligent parties accountable.