SC Credit Fraud Attorney: Legal Guidance for Fraud Victims

Credit fraud can destroy your financial life in weeks. Criminals open accounts in your name, rack up debt, and damage your credit score while you’re left to clean up the mess.

We at Hays Cauley, P.C. help fraud victims fight back and recover what they’ve lost. As an SC credit fraud attorney, we know the legal tools available to you and how to use them effectively.

How Credit Fraud Damages Your Financial Life and What You Can Do About It

Identity Theft Destroys More Than Your Bank Account

Identity thieves don’t just steal money-they destroy your creditworthiness. When someone opens accounts in your name, those fraudulent accounts appear on your credit report as if you created them. Each missed payment tanks your score further. The Federal Trade Commission reported that identity theft victims lost an average of $5,000 in 2023, but the real damage extends far beyond immediate financial loss.

Your credit score determines whether you’ll qualify for mortgages, car loans, and even job opportunities. A single fraud case can reduce your score by 100 points or more, making it nearly impossible to borrow at reasonable rates for years.

How Fraudsters Attack Your Accounts

Credit card fraud happens within minutes and spreads across multiple merchants before you even notice. Criminals use stolen card numbers for purchases at dozens of locations simultaneously, making detection difficult.

Account takeover fraud is worse. Fraudsters change your password and contact information, locking you out of your own accounts while they drain funds or apply for new credit lines in your name. Check fraud using your personal information presents another threat-criminals deposit counterfeit checks into accounts, and the fraud moves through the banking system slowly, giving them time to withdraw funds before the scheme surfaces.

South Carolina Law Protects You More Than You Know

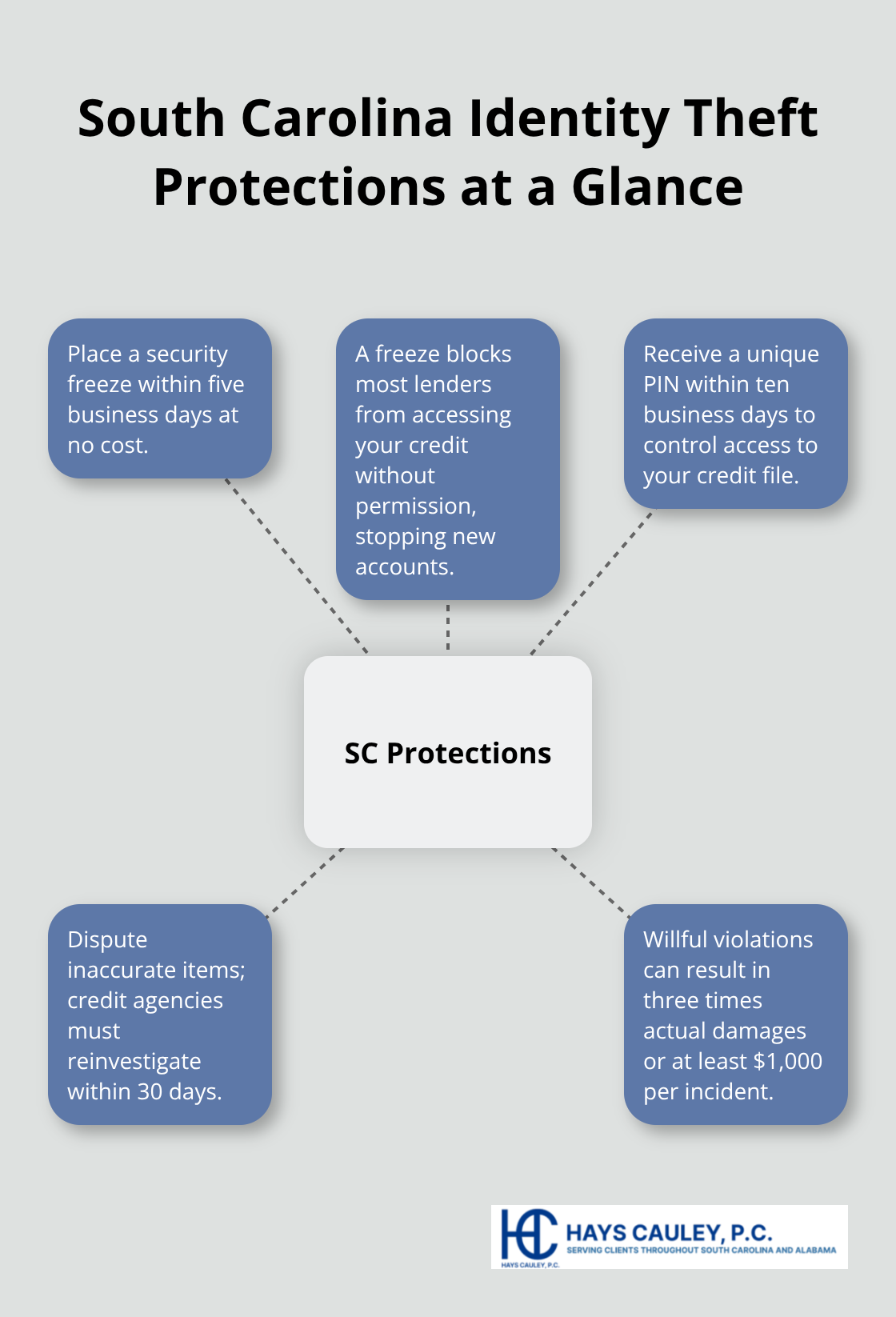

South Carolina law gives fraud victims specific protections that most people never use. Under the South Carolina Identity Theft Protection Act, you have the right to place a security freeze on your credit file within five business days of a written request, and it costs nothing. This freeze blocks most lenders from accessing your credit without your permission, which stops fraudsters from opening new accounts in your name.

After you request a freeze, you receive a unique PIN within ten business days that lets you control access to your file. You can also dispute inaccurate items on your credit report, and credit agencies must reinvestigate within 30 days. If they find an item inaccurate, they must correct it and notify previous recipients. Willful violations can result in three times your actual damages or at least $1,000 per incident.

Federal Protections Work Alongside State Law

The Fair Credit Reporting Act gives you the right to file complaints directly with the Federal Trade Commission, which tracks fraud trends and shares data with law enforcement agencies. South Carolina law also allows you to file police reports and petition for expedited judicial determination of factual innocence if the identity thief was arrested using your identity.

These protections exist, but using them effectively requires understanding which steps to take first and in what order. The next section walks you through the immediate actions that stop the bleeding and protect your future.

What to Do in the First 48 Hours After Discovering Fraud

Act Fast to Limit Your Losses

The moment you realize fraud has hit your accounts, speed matters more than panic. Most fraud victims who act within 48 hours limit their losses significantly, while those who wait weeks face exponentially larger damage. The Federal Trade Commission found that victims who reported fraud within one day of discovery recovered an average of 50% more of their losses compared to those who waited a week. Your first move should be calling your credit card companies and banks directly-not using numbers from statements or emails, which could be fraudulent.

Ask them to freeze your accounts immediately and cancel compromised cards.

Secure Your Debit and Credit Cards

For debit cards, log into your online banking and turn the card off through your settings, then call your bank’s cardholder services to report the loss and request a replacement, which typically arrives in seven to ten business days. For credit cards, contact your issuer’s fraud department and request new cards with different account numbers. Close affected accounts at all financial institutions involved in the fraud, and contact lenders to reverse unauthorized charges and work toward resolution.

Alert the Credit Bureaus and File Reports

Contact all three credit bureaus-Equifax at 888-836-6351, Experian at 888-397-3742, and TransUnion-to place fraud alerts on your file. Once you notify one bureau, the others receive automatic notification, so you only need to make one call. A fraud alert tells lenders to verify your identity before opening new accounts, which blocks most fraudsters from using your stolen information. The alert lasts one year and costs nothing.

After placing the alert, request free credit reports from each bureau through annualcreditreport.com and examine them for unauthorized accounts or inquiries.

File a report with your local police department immediately, as you’ll need a copy for creditors and the Federal Trade Commission. Report the fraud to the FTC through their online complaint form or by calling 877-438-4338, and if the fraud involved online activity, report it to the Internet Crime Complaint Center at ic3.gov.

Document Everything and Build Your Record

Keep detailed records of every fraudulent transaction, including dates, times, amounts, and the names of people you spoke with at each institution. Document everything in a spreadsheet or notebook because you’ll reference this information repeatedly when disputing charges and working with creditors. This documentation becomes critical evidence if you need to pursue legal action or negotiate with creditors later.

Lock Down Your Credit with a Security Freeze

South Carolina law gives you the power to place a security freeze on your credit file within five business days of a written request, and it costs nothing. This freeze blocks lenders from accessing your credit without your permission-the strongest tool available to stop new account fraud. You receive a unique PIN within ten business days that lets you control who accesses your file. With your accounts secured, your reports filed, and your credit frozen, you’ve stopped the immediate bleeding. The next phase involves working with creditors and credit bureaus to dispute fraudulent charges and restore your credit profile-a process where legal guidance can make a significant difference in your recovery timeline and final outcome.

How We at Hays Cauley, P.C. Help Fraud Victims Recover

Investigating Your Case and Building Evidence

Recovering from credit fraud requires more than placing fraud alerts and disputing charges on your own. Creditors and credit bureaus count on most victims giving up after the initial shock wears off, which is why many fraudulent accounts remain on credit reports for years. We at Hays Cauley, P.C. investigate your case systematically and gather evidence that creditors cannot ignore. This means requesting detailed transaction records from financial institutions, tracking the timeline of when fraudulent accounts opened, and identifying patterns that prove you did not authorize the charges. We examine whether creditors followed proper verification procedures before opening accounts in your name, because South Carolina law requires issuers to verify address changes before issuing new cards or opening new accounts. When a creditor skips this step and a fraudster uses your stolen information to create an account, that creditor bears responsibility for the fraud.

We document these failures because they form the foundation of your recovery claim. Many victims discover that creditors violated the Fair Credit Reporting Act by failing to investigate disputes within the required 30-day window, or by refusing to correct inaccurate information after reinvestigation. These violations carry real consequences, including damages of three times your actual losses or at least $1,000 per incident for willful violations.

Negotiating with Creditors and Credit Bureaus

Negotiating with creditors directly rarely works because they have no incentive to reverse charges without pressure. We contact creditors on your behalf with detailed evidence showing the fraud and demand they remove fraudulent accounts from your credit report and reverse unauthorized charges. Most creditors respond differently to an attorney than to a victim calling alone. When we present documentation that shows a creditor failed to verify your identity or ignored your dispute, they typically reverse charges and remove accounts rather than face potential litigation.

We also work with credit bureaus to challenge inaccurate information on your report and file disputes that force them to reinvestigate within 30 days. If they find items inaccurate, they must notify previous recipients of your credit report, which corrects the damage to your borrowing history.

Protecting You from Creditor Retaliation and Lawsuits

Our representation protects your legal rights throughout this process because creditors sometimes retaliate against fraud victims by reporting them to collection agencies or continuing to pursue fraudulent debt. We stop this harassment and represent you in disputes where creditors refuse to acknowledge the fraud. If a creditor sues you for an unpaid fraudulent account, we defend you and prove the account was opened without your authorization, which should result in dismissal. This legal protection matters because many fraud victims face lawsuits from creditors who claim the debt is legitimate, and without proper defense, you could lose a judgment and face wage garnishment. We hold creditors accountable for their role in the fraud rather than leaving you to fight alone.

Final Thoughts

Credit fraud recovery doesn’t end when you place fraud alerts and freeze your credit. Protecting yourself from future fraud means staying vigilant about your accounts and understanding that criminals constantly develop new tactics to steal identities. Review your credit reports quarterly through annualcreditreport.com, monitor your accounts regularly through online banking, and set up account alerts that notify you of unusual activity.

Prevention alone isn’t enough if fraud has already damaged your credit and finances. An SC credit fraud attorney can investigate whether creditors and credit bureaus violated your rights under South Carolina and federal law, negotiate with institutions that refuse to acknowledge fraud, and represent you if creditors sue you for fraudulent debt. Many victims spend months or years trying to resolve fraud on their own, only to discover that creditors ignored their disputes or that credit bureaus failed to reinvestigate inaccurate information within the required timeframe.

We at Hays Cauley, P.C. help fraud victims throughout South Carolina, including Greenville, Columbia, and Charleston, recover from identity theft and credit fraud. Contact Hays Cauley, P.C. today to discuss your case and learn what legal options are available to you. Our team understands how to use South Carolina’s consumer protection laws to force institutions to correct fraudulent accounts and reverse unauthorized charges.