Identity theft affects millions of Americans each year, and criminals are constantly finding new ways to steal personal information. We at Hays Cauley, P.C. have created this guide to help you understand the risks and take action.

Whether you’re looking for identity theft articles or practical protection strategies, this resource covers everything from prevention to recovery steps if you become a victim.

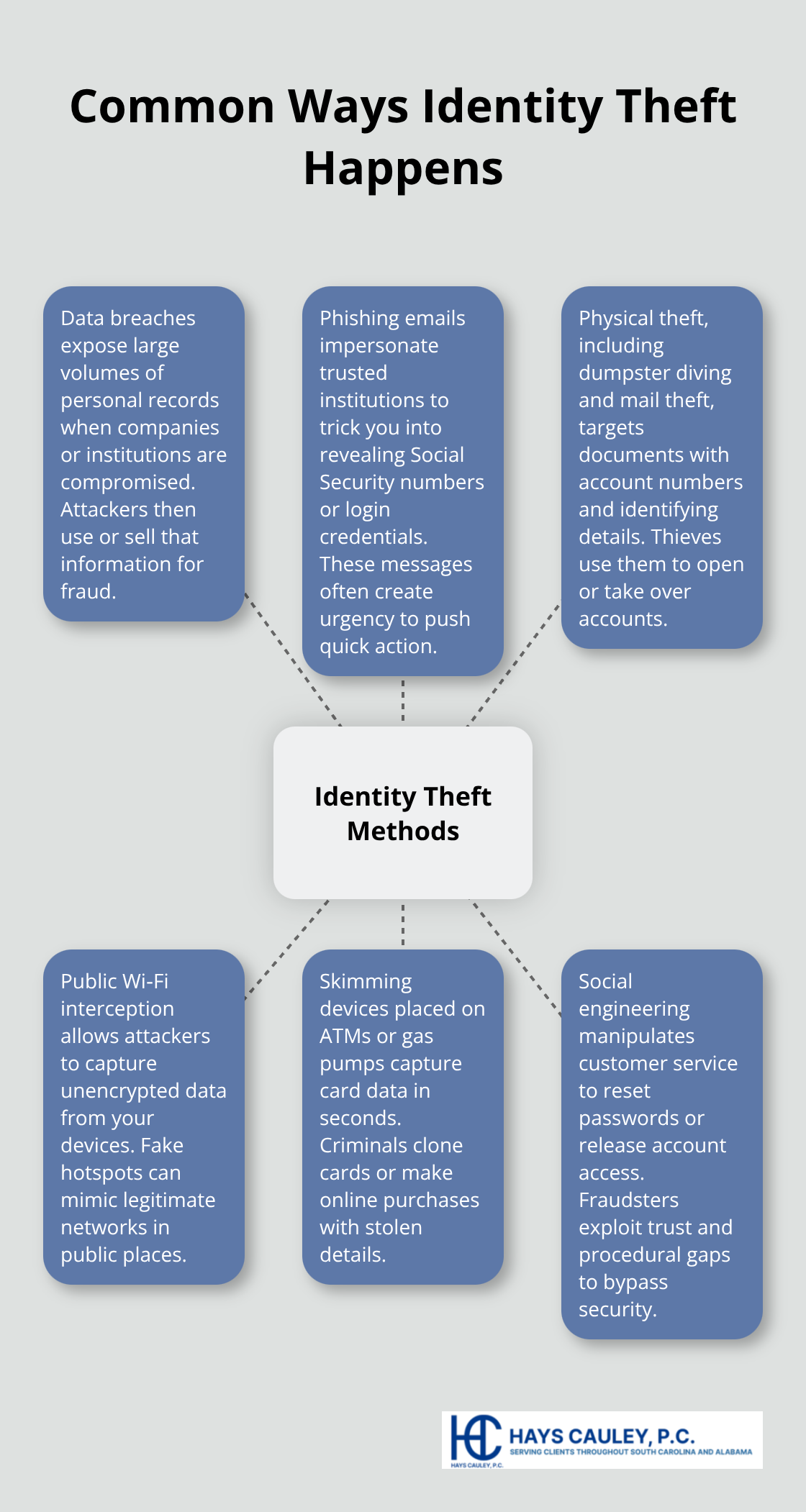

How Identity Theft Happens

Criminals steal personal information through methods that range from low-tech to sophisticated. Data breaches expose millions of records annually-the Identity Theft Resource Center reported over 3,205 breaches in 2023 alone. Phishing emails trick you into revealing Social Security numbers or login credentials by impersonating banks or government agencies. Dumpster diving and mail theft give criminals access to physical documents containing account numbers and identifying information. Public Wi-Fi networks are hunting grounds where hackers intercept unencrypted data from your devices. Skimming devices attached to ATMs or gas pumps capture credit card information in seconds. Social engineering tactics manipulate customer service representatives into resetting passwords or releasing account access.

The Federal Trade Commission reports that identity theft complaints exceeded 2.6 million in 2023, making it one of the most common consumer complaints filed annually.

Warning Signs You’re Being Targeted

Unfamiliar charges on your bank or credit card statements are the clearest warning signal. A changed billing address on accounts you didn’t modify indicates someone accessed your information. Calls from debt collectors about debts you never incurred mean fraudsters opened accounts in your name. Mail from credit card companies or banks you never applied to shows criminals are attempting to establish credit. Denied credit applications when your history is solid suggest someone damaged your credit profile.

How to Spot Identity Theft Early

Check your credit reports from Experian, TransUnion, and Equifax at least annually through annualcreditreport.com to spot unfamiliar accounts before they cause serious damage. Missing bills or statements arriving late can signal address changes made by identity thieves preparing to intercept future communications.

Tax-related identity theft appears as IRS notices about income you didn’t earn or tax refunds you never received. Acting quickly when you notice these signs prevents further unauthorized accounts and reduces recovery time significantly.

The sooner you detect identity theft, the faster you can take action to stop it. Your next step involves understanding what immediate actions protect your accounts and credit profile from additional damage.

How to Stop Identity Theft Before It Starts

Secure Your Physical Documents and Information

Protecting your personal information requires active steps, not passive hope. Store physical documents like bank statements, Social Security cards, and tax returns in a locked safe or safe deposit box at home, not scattered across your desk or filing cabinet. Most people carry their Social Security card in their wallet, which is a serious mistake-leave it at home unless you visit a government office or healthcare provider that specifically requests it. A cross-cut shredder tears documents into confetti-sized pieces rather than long strips that criminals can reassemble, so use one before throwing away sensitive papers. When companies ask for your Social Security number, ask three questions: Why do you need it, what happens if I don’t provide it, and can I use a different identifier instead. Many businesses accept driver’s license numbers or customer ID numbers instead. Limit what you carry daily-one credit card for online purchases works better than multiple cards, and a debit card should stay home since debit card fraud can drain your checking account directly while credit card fraud provides liability protection under federal law.

Reduce Mail Theft and Prescreened Offers

Mail theft remains a common entry point for identity thieves hunting for credit offers and financial statements. Call 1-888-567-8688 or visit optoutprescreen.com to opt out of prescreened credit offers, which reduces the volume of credit offers in your mailbox that criminals target. Retrieve your mail promptly each day and use a secure mailbox to prevent theft. This simple habit eliminates a major source of personal information that thieves exploit.

Monitor Your Credit Reports and Accounts

Your credit monitoring habits matter more than any single prevention step. Pull your free credit reports from annualcreditreport.com quarterly rather than waiting until annual reviews catch problems months after they occur. Place a credit freeze with all three bureaus-Experian, TransUnion, and Equifax-which prevents new accounts from being opened in your name and costs nothing to place or lift. Check your bank and credit card statements weekly for charges you didn’t authorize; waiting until monthly statements arrive means criminals have had weeks to make additional purchases.

Strengthen Your Online Security

Enable two-factor authentication on every account that offers it, particularly email and banking platforms, since email access gives criminals the ability to reset passwords on other accounts. Use unique, complex passwords containing uppercase letters, numbers, and symbols for each account, and consider a password manager to track them. Avoid public Wi-Fi networks entirely for accessing financial information, checking email, or logging into accounts-criminals set up fake networks in coffee shops and airports specifically to intercept unencrypted data.

Verify Unexpected Communications

When you receive unexpected emails claiming to be from your bank, credit card company, or government agency, never click links or download attachments. Instead, call the organization directly using the phone number on your official statement or website to verify the request is legitimate. This verification step stops phishing attacks before they compromise your accounts. Taking these preventative measures significantly reduces your risk, but if identity theft does occur, knowing the immediate steps to take determines how quickly you regain control of your financial life.

What to Do Immediately After Identity Theft

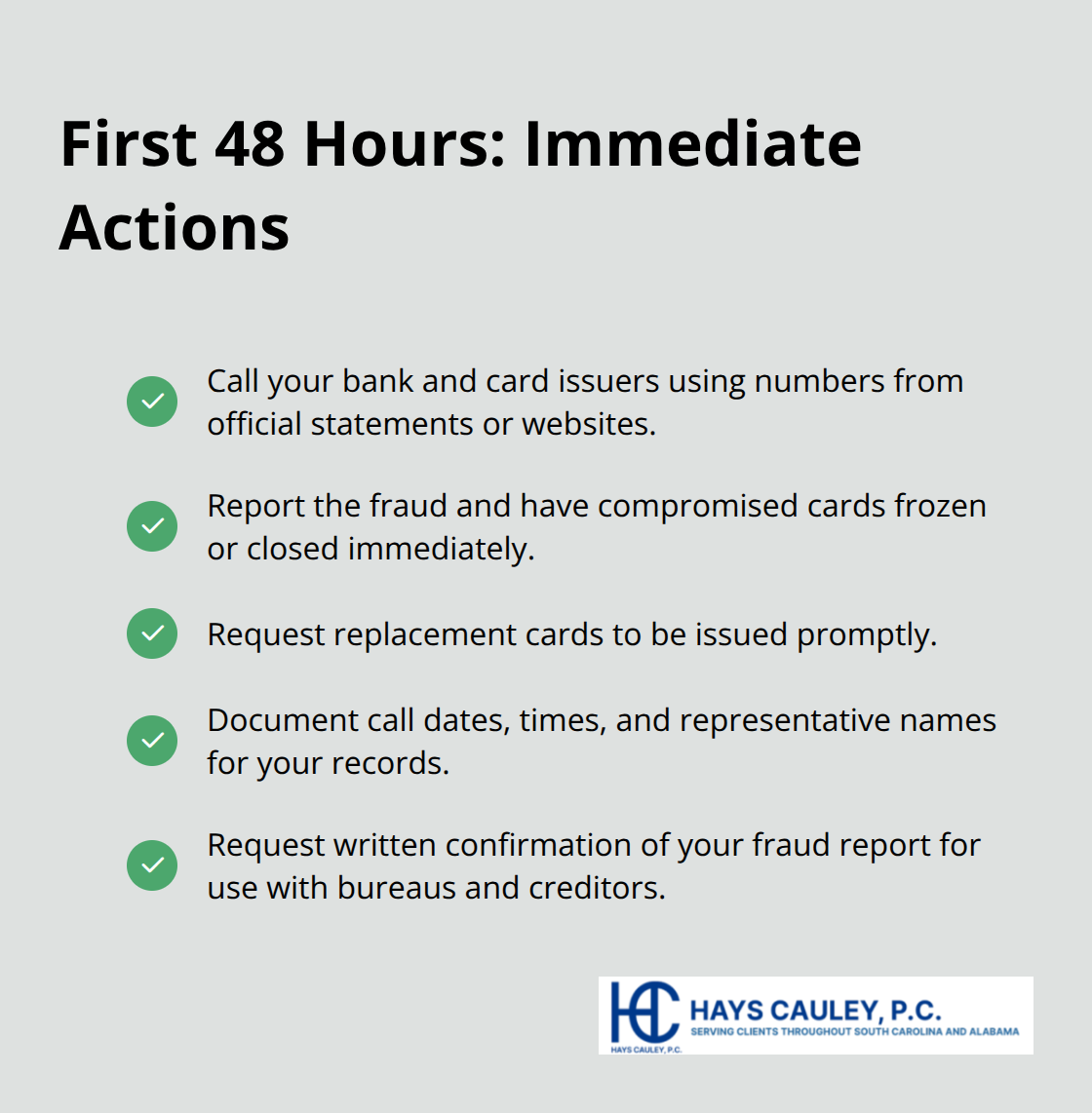

Act Within the First 48 Hours

The first hours after discovering identity theft determine how much damage criminals can inflict on your financial life. Call your bank and credit card companies directly using the phone numbers on your statements or official websites-not numbers from emails or letters you receive, since fraudsters sometimes intercept mail. Tell them fraud occurred on your account and request they freeze or close compromised cards immediately. Most banks can issue replacement cards within 3-5 business days.

Document the date and time of your call along with the representative’s name for your records. Request written confirmation of the fraud report so you have proof for credit bureaus and other creditors.

Place a Fraud Alert With Credit Bureaus

Your next critical step involves placing a fraud alert with the credit bureaus, which tells lenders to verify your identity before opening new accounts. Contact Experian, TransUnion, and Equifax to place an initial fraud alert, which lasts one year and requires only one bureau to notify the other two automatically. This alert costs nothing and tells creditors to call you before approving new credit applications in your name. After placing the alert, obtain your credit reports from all three bureaus at annualcreditreport.com and review them for unfamiliar accounts, unauthorized inquiries, or incorrect personal information.

File a Report With the Federal Trade Commission

File a detailed report with the Federal Trade Commission at IdentityTheft.gov, which generates a personalized recovery plan with pre-filled letters to send to creditors, debt collectors, and banks. This official documentation strengthens your position when disputing fraudulent accounts. The FTC provides step-by-step guidance tailored to your specific type of identity theft, whether it involves credit card fraud, tax-related theft, or other variations.

Get Legal Help if Needed

If you face significant financial losses or complexity involving multiple fraudulent accounts, a consumer protection attorney can guide you through recovery steps and help dispute inaccurate information on your credit reports. South Carolina law recognizes identity fraud as a serious crime with felony penalties up to ten years imprisonment, meaning law enforcement can pursue criminal charges against the perpetrator when evidence exists. An attorney familiar with identity theft cases can help you navigate both the civil recovery process and coordinate with law enforcement if criminal prosecution is appropriate.

Moving Forward After Identity Theft

Recovery from identity theft extends far beyond the initial crisis response, requiring consistent monitoring for months and years after the fraud occurs since criminals sometimes use stolen information gradually to avoid detection. Check your credit reports every three months during the first year following identity theft, then return to annual reviews once you confirm no new fraudulent accounts appear. When reviewing reports, look for accounts you didn’t open, inquiries from creditors you never contacted, and personal information changes like address modifications. Dispute any inaccuracies immediately by contacting the credit bureau in writing and providing documentation of the error.

Preventing future identity theft requires maintaining the protective habits you established during recovery (strong passwords, two-factor authentication, weekly statement reviews, document shredding, and prompt mail retrieval). These ongoing practices significantly reduce your risk of becoming a victim again and help you avoid becoming the subject of identity theft articles yourself. Continue monitoring your bank and credit card statements weekly rather than waiting for monthly statements to arrive.

If you face complexity in disputing fraudulent accounts or recovering from substantial financial losses, Hays Cauley, P.C. can help guide you through the process. We work with consumers dealing with credit reporting and identity theft issues to protect your rights and restore your financial standing. Taking action now prevents your situation from becoming a cautionary tale.