How to Protect Yourself from Identity Theft

Identity theft affects millions of Americans annually, and South Carolina residents are no exception. We at Hays Cauley, P.C. understand how devastating it can be when criminals misuse your personal information.

Understanding identity theft laws and knowing how to respond quickly makes all the difference. This guide walks you through warning signs, prevention strategies, and the exact steps to take if theft occurs.

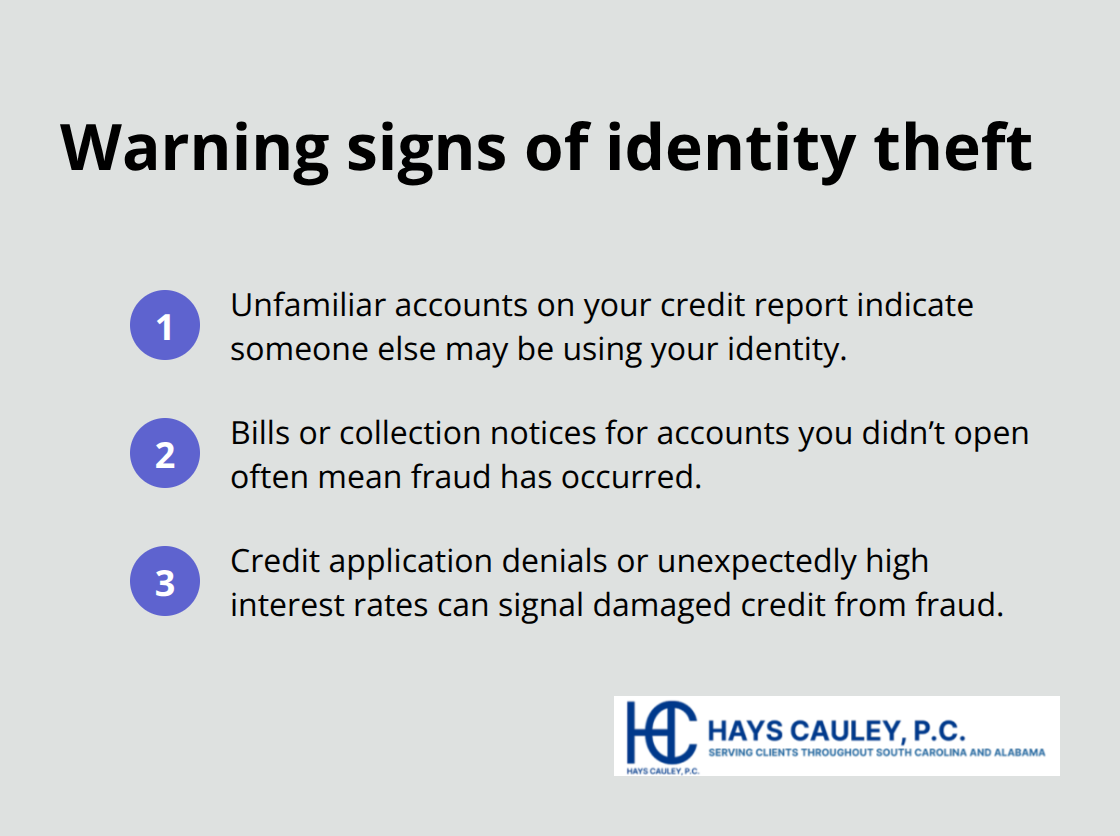

Warning Signs That Indicate Identity Theft

The Federal Trade Commission reported that identity theft and related fraud losses exceeded $10 billion in 2023, making this crime impossible to ignore. Most victims don’t realize they’ve been targeted until weeks or months after the theft occurs, which is why knowing what to watch for matters significantly.

Unfamiliar Accounts on Your Credit Report

Unfamiliar accounts appearing on your credit report represent one of the clearest red flags. When you pull your credit report from annualcreditreport.com, look closely at every account listed. If you see credit cards, loans, or lines of credit you never opened, identity theft is in progress.

Credit inquiries from companies you didn’t contact also signal trouble because thieves often shop around for new credit using your name. Don’t dismiss these as errors. Contact the creditor immediately and ask them to verify that you authorized the account.

Bills and Collection Notices From Unknown Sources

Unexpected bills arriving in your mailbox for accounts you never created are serious warning signs. Collection agencies may contact you about debts you didn’t incur, which happens frequently when criminals open accounts in your name and stop paying. These notices often arrive months after the fraudulent account opens, meaning the thief has already done significant damage. If you receive a bill for a utility account, credit card, or loan you don’t recognize, call the company’s fraud department immediately rather than ignoring it. Don’t pay anything. Document the date you received the notice and keep it for your records (this documentation becomes essential if you need to file a dispute later).

Credit Application Denials and Rate Surprises

When lenders deny your credit application or offer you significantly higher interest rates than you expected, your credit profile has likely suffered damage. Thieves who open accounts in your name and default on them tank your credit score, sometimes by 100 points or more. If you apply for a mortgage or car loan and get rejected, request your credit report immediately. You’re entitled to one free report annually from each of the three major bureaus. Compare what you see against your own financial history. Discrepancies mean someone else has been using your identity. Higher interest rates on new credit applications signal to lenders that you’re a higher-risk borrower, which happens when fraud has damaged your credit history. Act quickly when this occurs because each month of inaction allows more fraudulent accounts to accumulate.

These warning signs demand immediate action. The next section covers the practical steps you can take right now to prevent identity theft from happening in the first place.

How to Stop Identity Theft Before It Starts: Serving South Carolina, including Greenville, Columbia and Charleston

Taking action today prevents months of headaches tomorrow. The Federal Trade Commission recommends checking your credit reports at least annually, but you should pull them every four months instead. This three-times-yearly approach catches fraud faster than annual checks alone.

Get your free reports from annualcreditreport.com and examine every account, inquiry, and address listed. When you spot something unfamiliar, place a fraud alert immediately by contacting any of the three major bureaus-Equifax, Experian, or TransUnion. That single call triggers all three to flag your account, requiring lenders to verify your identity before opening new credit. The alert lasts one year and costs nothing. If you’ve already been victimized, request an extended seven-year fraud alert instead. Consider going further with a credit freeze, which blocks access to your entire credit file unless you temporarily lift it. Freezes are free nationwide and remain in place until you remove them, making it nearly impossible for criminals to open accounts in your name.

Create Passwords That Thieves Cannot Crack

Weak passwords invite account takeover fraud, where criminals hijack your email, banking, or credit accounts after stealing credentials. Stop using the same password across multiple sites-this is non-negotiable. Instead, create unique passwords for each account using a mix of uppercase letters, numbers, and symbols. A password manager like Bitwarden or 1Password securely stores these complex combinations so you only need to remember one master password. Change passwords every 90 days for high-risk accounts like banking and email, though quarterly updates aren’t as critical for less sensitive accounts once two-factor authentication is active.

Activate Two-Factor Authentication on All Accounts

Two-factor authentication requires something you know (your password) plus something you have (a code from an authenticator app or text message). Enable this feature on every account that offers it, especially email and banking platforms. The National Institute of Standards and Technology confirms this dual-layer approach stops most account takeovers. This protection matters most for accounts that control access to your other accounts-your email address serves as the master key to password resets across your digital life.

Protect Your Social Security Number and Financial Details

Your Social Security number, date of birth, and financial account details have real market value to identity thieves. Never carry your Social Security card in your wallet-leave it at home in a secure location. When businesses request your full Social Security number, ask why they need it and whether an alternative identifier will work. Many companies accept the last four digits instead. Shred documents containing personal information using a cross-cut shredder before throwing them away, since standard shredders leave documents readable.

Secure Your Mail and Limit Online Exposure

Mail theft remains a serious vector for identity theft, so retrieve your mail promptly and consider using a locked mailbox. Opt out of prescreened credit offers by calling 1-888-567-8688 or visiting optoutprescreen.com, which eliminates one way thieves can open accounts in your name. Online, limit what you share on social media and tighten privacy settings so your information isn’t publicly visible. Use secure Wi-Fi connections for sensitive transactions and avoid conducting banking or shopping on public networks.

These prevention steps significantly reduce your risk, but they don’t guarantee complete protection. Even the most cautious individuals sometimes fall victim to sophisticated fraud schemes. The next section covers what happens when prevention fails and how to respond when you discover that your identity has been stolen.

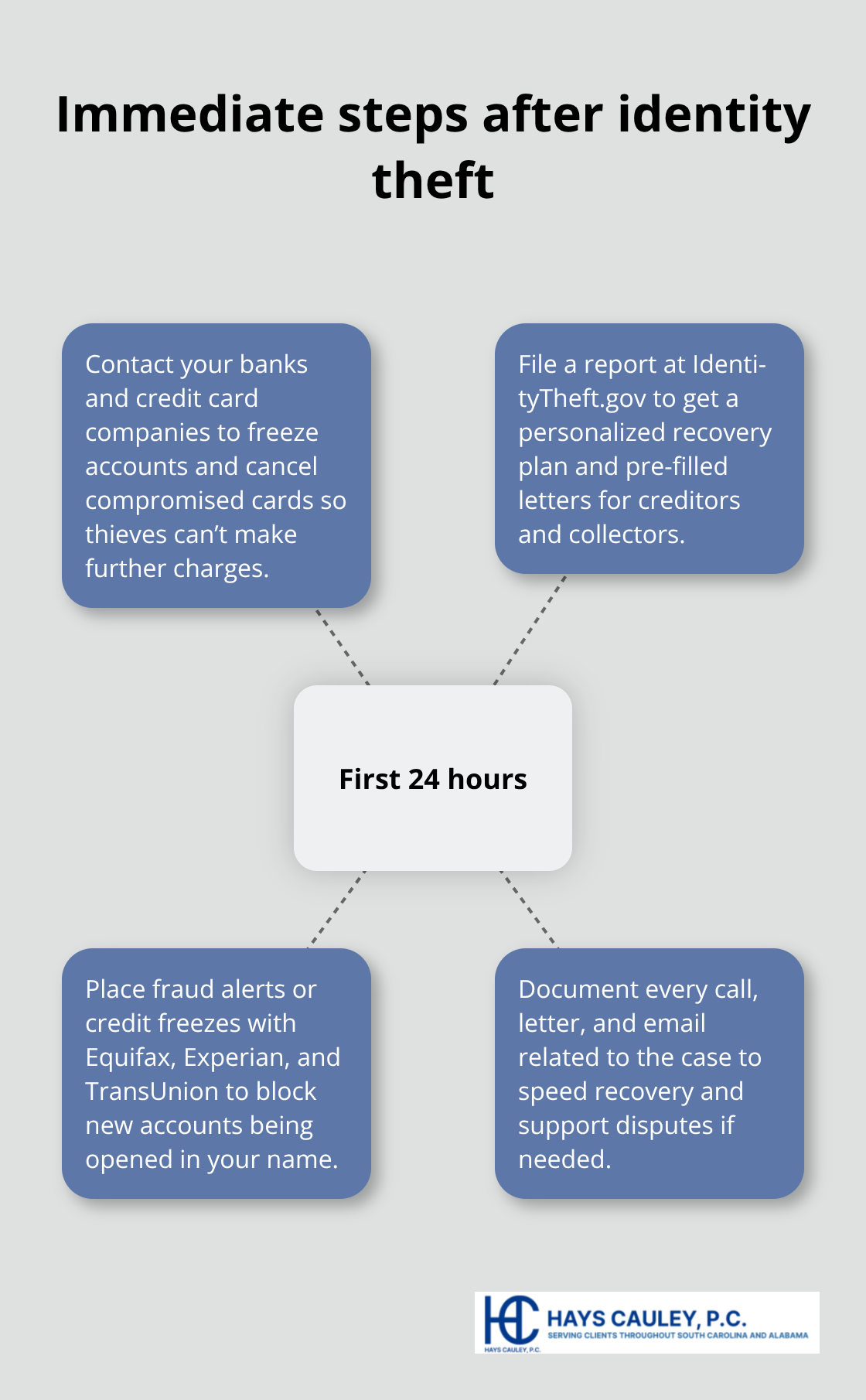

Act Immediately When Identity Theft Strikes: Serving South Carolina, including Greenville, Columbia and Charleston

Contact Your Financial Institutions First

The first 24 hours after discovering identity theft are critical. Contact your banks and credit card companies right away, even if you’re unsure whether the fraud is real. Tell them you suspect identity theft and ask them to freeze your accounts and review recent transactions.

Request that they cancel compromised cards and issue new ones with different account numbers. Document the name of every person you speak with, the date, time, and what they told you. Many banks reverse fraudulent charges within 60 days if you report them promptly, but delays cost you money and make recovery harder.

File a Report with the Federal Trade Commission

Next, file a report with the Federal Trade Commission at IdentityTheft.gov. This step matters because the FTC generates a personalized recovery plan you can print and track as you work through the restoration process. The plan includes pre-filled letters to send to creditors and debt collectors, saving you hours of writing. The FTC also provides guidance for more than 30 different types of identity theft scenarios, from tax fraud to medical identity theft, so you receive tailored advice rather than generic suggestions. Filing takes about 10 minutes and costs nothing.

Place Fraud Alerts and Credit Freezes

Simultaneously, place a fraud alert or credit freeze with all three major credit bureaus: Equifax, Experian, and TransUnion. A fraud alert requires lenders to verify your identity before opening new accounts, lasting one year at no cost. If identity theft is confirmed, request an extended seven-year fraud alert instead. A credit freeze blocks access to your entire credit file unless you temporarily lift it, making it nearly impossible for thieves to open new accounts in your name. Freezes remain in place indefinitely until you remove them and cost nothing. Many victims choose both: a fraud alert immediately while they investigate, then a credit freeze for long-term protection.

Organize Your Documentation

Keep detailed records of every letter, email, and phone call related to your case. Maintain copies of police reports, credit bureau correspondence, and communications with creditors. This documentation speeds recovery and protects you if disputes arise later. Recovery typically takes weeks or months depending on the theft type, so patience and organization separate victims who restore their identity quickly from those who struggle for years. We at Hays Cauley, P.C. understand how overwhelming this process feels, and we’re here to help consumers navigate identity theft and credit-related issues.

Final Thoughts

Identity theft prevention and rapid response form your strongest defenses against this growing threat. The steps outlined in this guide-monitoring your credit reports every four months, using unique passwords with two-factor authentication, and limiting personal information exposure-stop most criminals before they cause damage. When prevention fails, knowing exactly what to do matters enormously, and South Carolina’s identity theft laws protect you as a victim with specific rights and remedies available through the legal system.

Contact your banks immediately after discovering fraud, file a report with the Federal Trade Commission at IdentityTheft.gov, and place fraud alerts or credit freezes with all three major bureaus within the first 24 hours. These actions dramatically reduce the financial and emotional toll of identity theft, and the FTC provides free recovery plans tailored to your specific situation while credit freezes cost nothing. Staying vigilant means checking your credit reports regularly, reviewing bank and credit card statements monthly, and monitoring for warning signs like unfamiliar accounts or unexpected bills.

Resources abound to support your recovery efforts through annualcreditreport.com, the FTC’s IdentityTheft.gov portal, and assistance from the Social Security Administration and IRS for tax-related fraud. If you face overwhelming circumstances or complex credit disputes, Hays Cauley, P.C. helps consumers navigate identity theft and credit-related issues with dedicated support from a consumer protection law firm serving South Carolina, including Greenville, Columbia and Charleston.