Fair Credit Reporting Act Damages You Can Claim

A credit report error can cost you thousands in denied loans, higher interest rates, and missed opportunities. The Fair Credit Reporting Act gives you the right to recover damages when agencies or creditors violate your rights.

We at Hays Cauley, P.C. help South Carolina residents-in Greenville, Columbia, and Charleston-understand what Fair Credit Reporting Act damages you can claim and how to recover them.

What Damages Can You Actually Recover Under the FCRA

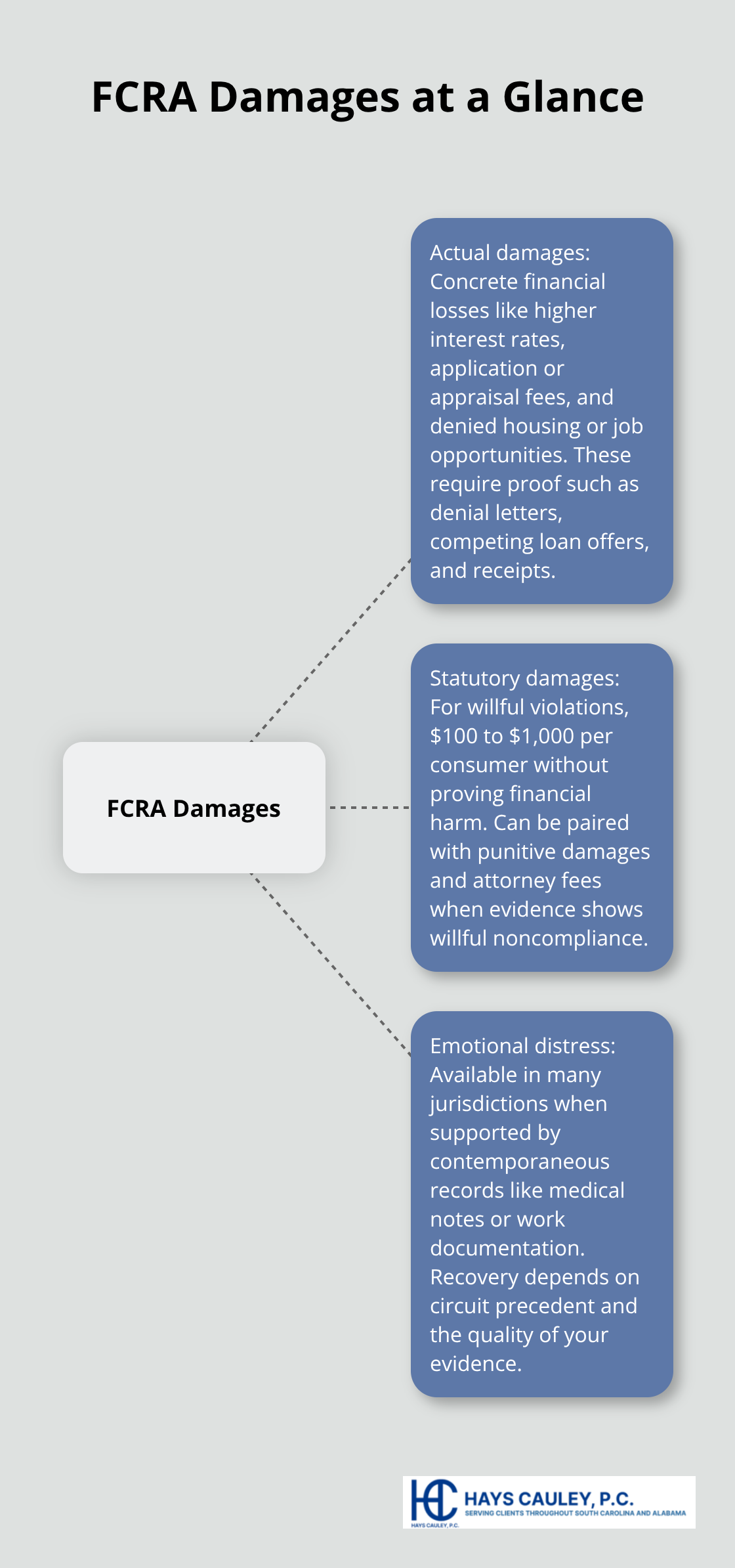

Actual Damages from Credit Report Errors

The Fair Credit Reporting Act authorizes three distinct categories of damages, and understanding the differences matters because they determine your recovery strategy. Actual damages cover concrete financial losses you suffered because of inaccurate reporting. If a credit report error caused a lender to deny your mortgage application, you can claim damages for the difference between the loan rate you were denied and the rate you eventually obtained elsewhere, plus any application fees and appraisal costs.

Housing denials represent the most common actual damages claim. In Nelson v. Experian Information Solutions Inc., courts recognized that a deceased flag incorrectly placed on a credit report and left uncorrected for over three months caused measurable economic harm through denied housing opportunities. You must document these losses with loan denial letters, competing loan offers showing rate differences, and receipts for application fees.

Employment-related damages also qualify if you can show the credit report error directly caused a job loss or prevented a job offer. The burden falls on you to prove the specific financial impact with supporting documentation.

Statutory Damages Without Proving Financial Harm

Statutory damages offer a fundamentally different path forward-and this matters because you do not need to prove actual financial harm. Under 15 U.S.C. 1681n(a)(1)(A), willful violations of the FCRA permit statutory damages of not less than $100 and not more than $1,000 per consumer. The Eleventh Circuit’s decision in Santos v. Healthcare Revenue Recovery Group confirmed that you can pursue these statutory damages without showing any actual credit damage whatsoever.

This ruling aligns with the Seventh, Eighth, Ninth, and Tenth Circuits, all holding that statutory damages operate as a separate remedy pathway from actual damages. The distinction matters because willful conduct warrants different proof standards than negligence. Punitive damages and attorney fees remain available alongside statutory damages, multiplying your potential recovery. Evidence showing a pattern of willful noncompliance (such as systematic incorrect reporting or ignored dispute messages) strengthens statutory damages claims.

Emotional Distress and Non-Economic Harm

Emotional distress damages present a more complicated landscape. Courts allow emotional distress recovery under the FCRA in many jurisdictions, but the Cummings v. Premier Rehab Keller decision narrowed emotional damages under certain federal statutes. However, Cummings does not foreclose emotional distress under FCRA claims; recovery depends on circuit-specific precedent and whether you can document the distress through contemporaneous evidence like medical records, therapy notes, or lost income from stress-related absences.

Understanding these three damage categories positions you to evaluate your claim’s strength and identify which recovery paths apply to your situation. The next section walks through how to gather the evidence that supports each type of damages claim.

Building Your Evidence Trail for FCRA Damages

Obtain Your Credit Reports and Dispute Records

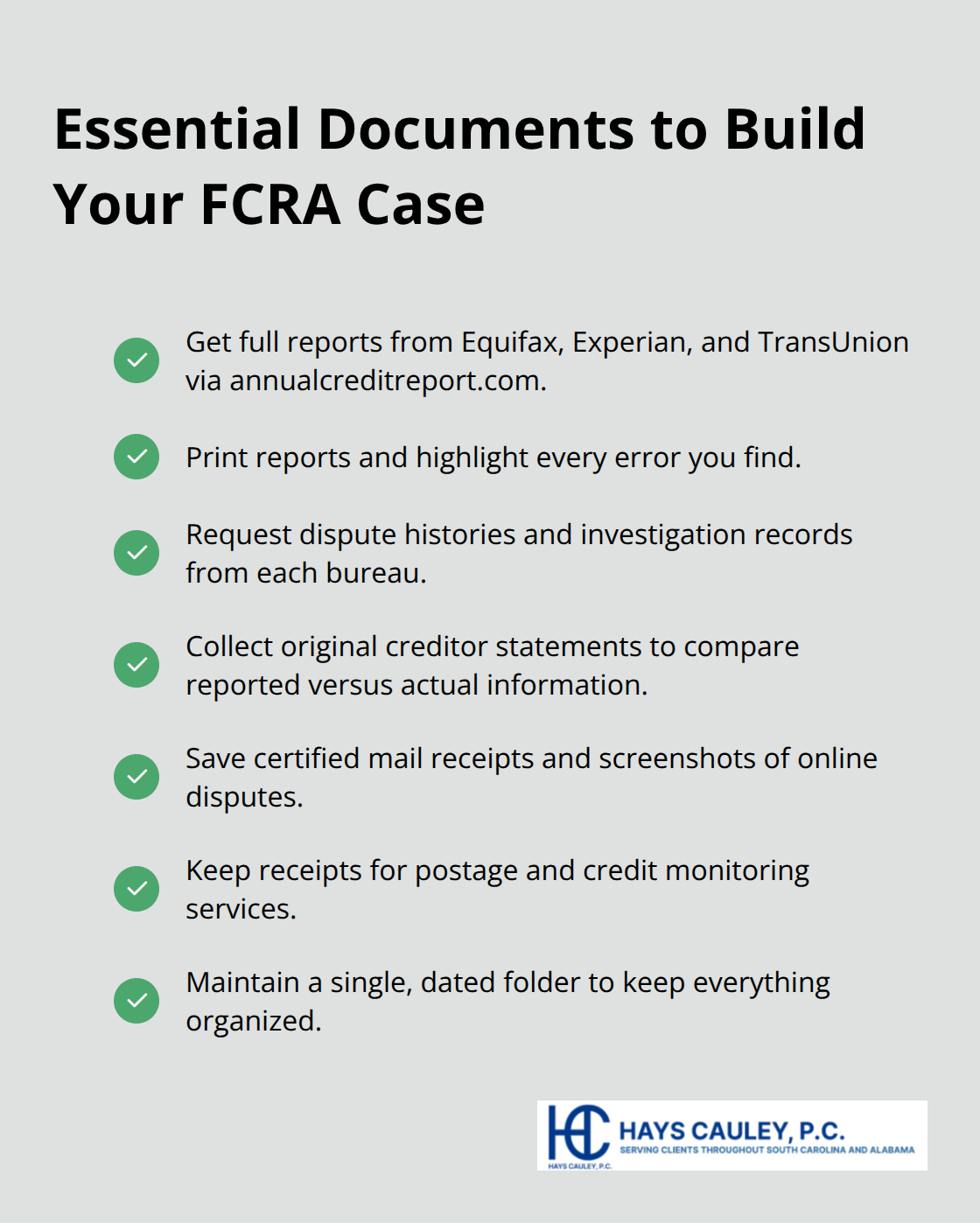

Documentation separates successful FCRA claims from dismissed ones. You must obtain your complete credit report from all three bureaus-Equifax, Experian, and TransUnion-through annualcreditreport.com, the federally mandated free source. Print these reports immediately and highlight every error. Then request your dispute history and investigation records from each bureau; the FCRA requires them to provide these upon request.

You should gather the original creditor statements showing what was actually reported versus what appears on your credit file. In Ramones v. AR Resources, Inc., the court found liability when investigators failed to review dispute messages or verify discrepancies, demonstrating how detailed dispute documentation strengthens your claim.

Create a Timeline of Your Disputes

You need to track the exact dates you submitted disputes, what specific errors you identified, and when each bureau claimed to investigate. A timeline spreadsheet works well for this purpose. Include screenshots of online disputes and print copies of certified mail receipts proving delivery. This organized record shows whether the bureaus met their legal obligations to investigate within 30 days and correct inaccurate information promptly.

Collect Proof of Financial Losses

For denied credit or higher interest rates, you must collect the loan denial letters explicitly stating the reason, your original credit score range before the error, competing loan offers showing the rate you obtained elsewhere, and any difference calculations. Document application fees, appraisal costs, and inspection fees you paid. For housing denials specifically, you should gather the lender’s written explanation and any communications where they cited your credit report. Employment-related damages require the employer’s written notice of job denial or termination and any evidence linking it to a credit report error. Remember that statutory damages can supplement actual losses, meaning even minimal financial harm may qualify for recovery.

Document Emotional Distress and Related Expenses

Medical records, therapy bills, or documented stress-related medical visits support emotional distress claims in circuits permitting such recovery. The National Consumer Law Center’s Fair Credit Reporting treatise notes that courts commonly exclude expert testimony on emotional damages unless supported by contemporaneous medical or psychological documentation, so medical records become essential. You should keep receipts for all dispute-related expenses: postage for certified letters, fees for credit monitoring services you purchased after discovering the error, and time logs calculating hours spent investigating and disputing. Courts recognize these as recoverable actual damages.

Organize Everything for Maximum Impact

You must maintain this documentation in a single folder with dates clearly labeled; organized evidence accelerates settlement negotiations and strengthens your position if litigation becomes necessary. The strength of your evidence directly determines whether you can recover actual damages, statutory damages, or both. With your documentation complete, the next step involves understanding how to present your claim to the responsible parties and what legal options you have if they refuse to settle.

How to Present Your FCRA Damages Claim

Your organized documentation now moves into action. Start with a formal dispute to each credit reporting agency that published the inaccurate information. The FCRA requires bureaus to investigate your dispute within 30 days and correct or delete inaccurate information. Send your dispute in writing via certified mail with return receipt requested-never rely on online dispute portals alone because they create no paper trail if the bureau claims non-receipt. Include copies of your supporting documentation, a clear description of each error, and a statement that you dispute the accuracy of the reported information. The bureau must acknowledge receipt of your dispute in writing.

When the Bureau Fails to Respond

If the bureau fails to respond within 30 days or refuses to correct the error after investigation, you have strengthened your claim for willful noncompliance, which supports both statutory damages and punitive damages under the FCRA. This failure to investigate properly becomes critical evidence in your case. Courts recognize that systematic failures to address disputes demonstrate willful conduct rather than negligence, triggering the higher statutory damages range of $100 to $1,000 per consumer under 15 U.S.C. 1681n.

Sending a Demand Letter

After the bureau fails to correct the error, send a demand letter to the furnisher (the original creditor or debt collector who reported the false information) and the bureau itself. Your demand letter should specify the inaccuracy, reference the dates of your disputes, cite the bureau’s failure to investigate properly or correct the error, calculate your actual damages with supporting documentation, and demand payment within 30 days. State your claim for statutory damages between $100 and $1,000 per consumer under 15 U.S.C. 1681n, plus actual damages, punitive damages, and attorney fees. Many furnishers and bureaus settle at this stage because the cost of litigation exceeds the settlement amount, particularly when evidence shows willful noncompliance.

Filing a Lawsuit

If 30 days pass without a meaningful settlement offer, file your lawsuit in state or federal court within two years of discovering the violation or five years after the violation occurred, whichever comes first. The statute of limitations favors early action because delay weakens evidence and allows the defendant to argue the claim is stale. Hays Cauley, P.C. handles these claims from demand letter through trial, managing the entire process so you focus on moving forward rather than navigating complex FCRA procedures.

Final Thoughts

The Fair Credit Reporting Act damages you can claim fall into three categories: actual damages for concrete financial losses, statutory damages of $100 to $1,000 per consumer for willful violations regardless of proof of harm, and emotional distress damages recognized in many jurisdictions. Your recovery depends entirely on the strength of your documentation and how quickly you act. A credit report error sitting uncorrected for months strengthens your claim for willful noncompliance, which multiplies your potential recovery through punitive damages and attorney fees alongside statutory damages.

Time matters more than most people realize. The FCRA gives you two years from discovery or five years from the violation to file suit, but delay weakens your evidence and allows defendants to argue staleness. Every month an inaccurate item remains on your report harms your credit score, employment prospects, and housing opportunities. The sooner you obtain your credit reports, identify errors, and document your disputes, the stronger your position becomes.

We at Hays Cauley, P.C. handle Fair Credit Reporting Act damages claims from initial dispute through settlement or trial, managing the entire process while you move forward with your life. If you have discovered inaccurate information on your credit report, contact Hays Cauley, P.C. to discuss your options for recovering damages. We serve South Carolina, including Greenville, Columbia, and Charleston, and we work on contingency, meaning you pay nothing unless we recover compensation for you.