A mistake on your credit report can cost you thousands of dollars in higher interest rates and denied loans. The Fair Credit Reporting Act gives you specific FCRA rights in South Carolina to fight back against inaccurate information.

At Hays Cauley, P.C., we help people remove errors and hold credit bureaus accountable. This guide shows you exactly what steps to take.

FCRA Rights in South Carolina: What the Fair Credit Reporting Act Actually Gives You, Serving South Carolina, Including Greenville, Columbia and Charleston

Access Your Credit Report for Free

The Fair Credit Reporting Act is federal law that applies to you in South Carolina with three hard-edged rights. First, you can access your credit report from Equifax, Experian, and TransUnion once every 12 months for free through AnnualCreditReport.com. The CFPB data from the second half of 2025 shows roughly 1.4 million complaints involved incorrect information on credit reports, which means errors are widespread and worth hunting for.

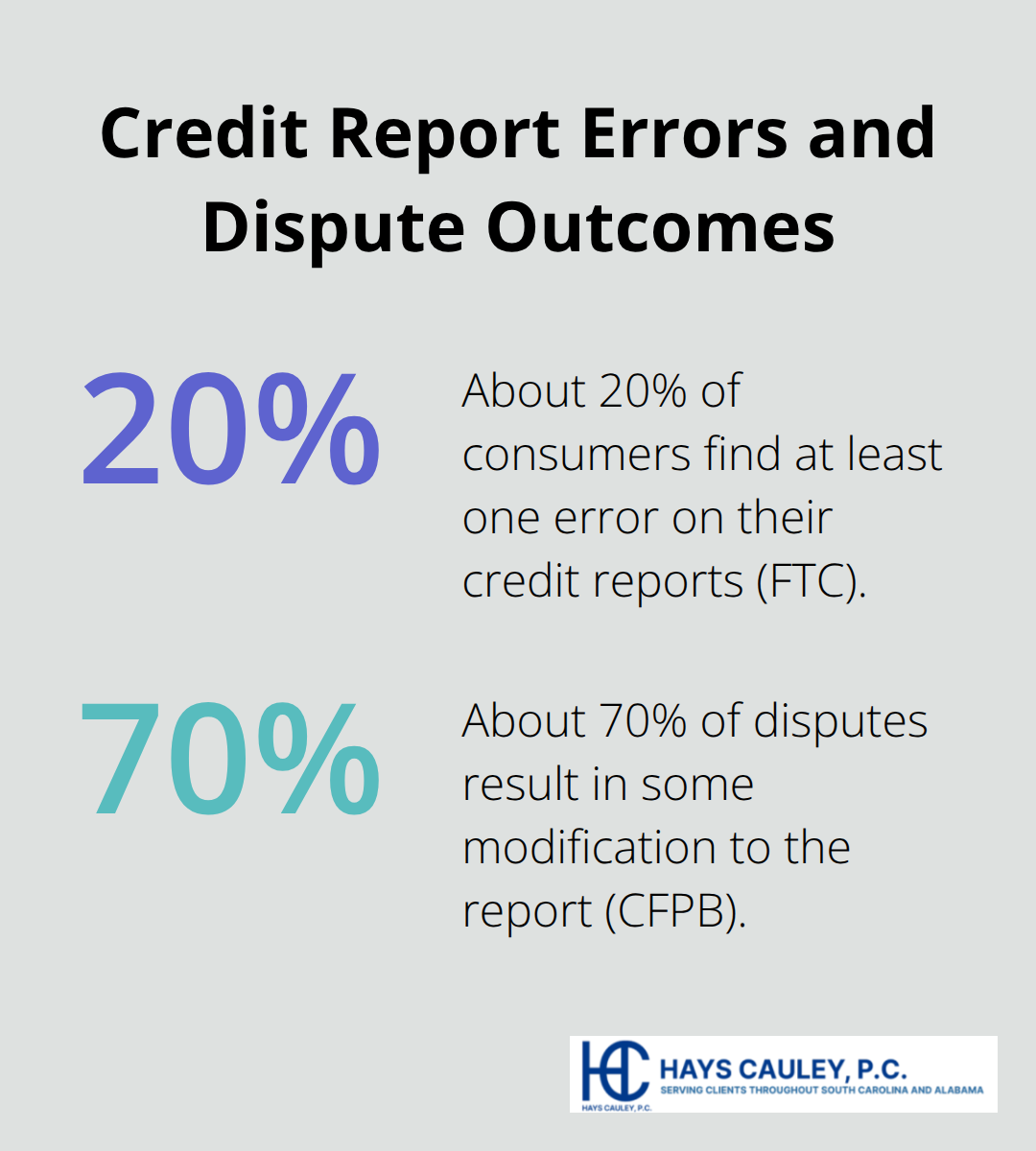

Pull one report every four months instead of all three at once so you catch problems earlier in the year rather than waiting until December. When you review your report, look specifically for accounts you never opened, payment dates that don’t match your records, balances that are wrong, and duplicate entries. About 20 percent of consumers find at least one error on their reports according to the FTC, so the odds are solid you’ll spot something.

Challenge Inaccurate Information in Writing

Your second right lets you challenge any inaccurate information directly with the credit bureau in writing. Send your dispute letter by certified mail with return receipt to create a legal record, not just online. Include your full name, address, the specific account number, exactly what is wrong, and attach copies of supporting documents like bank statements or payment confirmations.

The bureau must investigate within 30 days and remove information they cannot verify. Your third right guarantees you receive accurate information from the start. If the bureau finds an error during investigation, they must notify all three bureaus to correct the data.

Apply Pressure from Multiple Directions

The FCRA also lets you dispute information directly with the company that reported it to the bureau, which applies pressure from both angles and speeds corrections. If a company continues reporting false data after you dispute it, they must notify the bureau that you are disputing the information. These rights are not suggestions or guidelines-they are legal protections you can enforce in South Carolina, and understanding how to use them positions you to take action against inaccurate reporting.

How to Build a Strong Dispute That Works

Obtain and Review All Three Reports Carefully

Start by obtaining all three credit reports from AnnualCreditReport.com and print them out to review offline. The FTC reports that about 20 percent of consumers find errors on at least one report, but you won’t catch them by skimming online. Mark every discrepancy directly on the printed pages: wrong account balances, payment dates that don’t match your records, accounts you never opened, or negative marks that should have aged off.

Identify Exactly What Is Wrong

Be specific about which field contains the error. Vague disputes get rejected regularly, so instead of writing “this account is wrong,” identify exactly what is incorrect, such as “the balance shows $5,432 but my last statement shows $2,100” or “the last payment date listed is March 2023, but I paid in full on January 15, 2023.” Precision matters because credit bureaus dismiss unclear claims without investigation.

Gather Your Supporting Documents

Collect supporting documents before filing anything: bank statements, payment confirmations from your creditor, account statements, or letters from the company. If identity theft is involved, obtain your identity theft report from IdentityTheft.gov immediately. Strong documentation (statements, confirmations, creditor letters) transforms a weak dispute into one that produces results.

Write and Send Your Dispute Letter

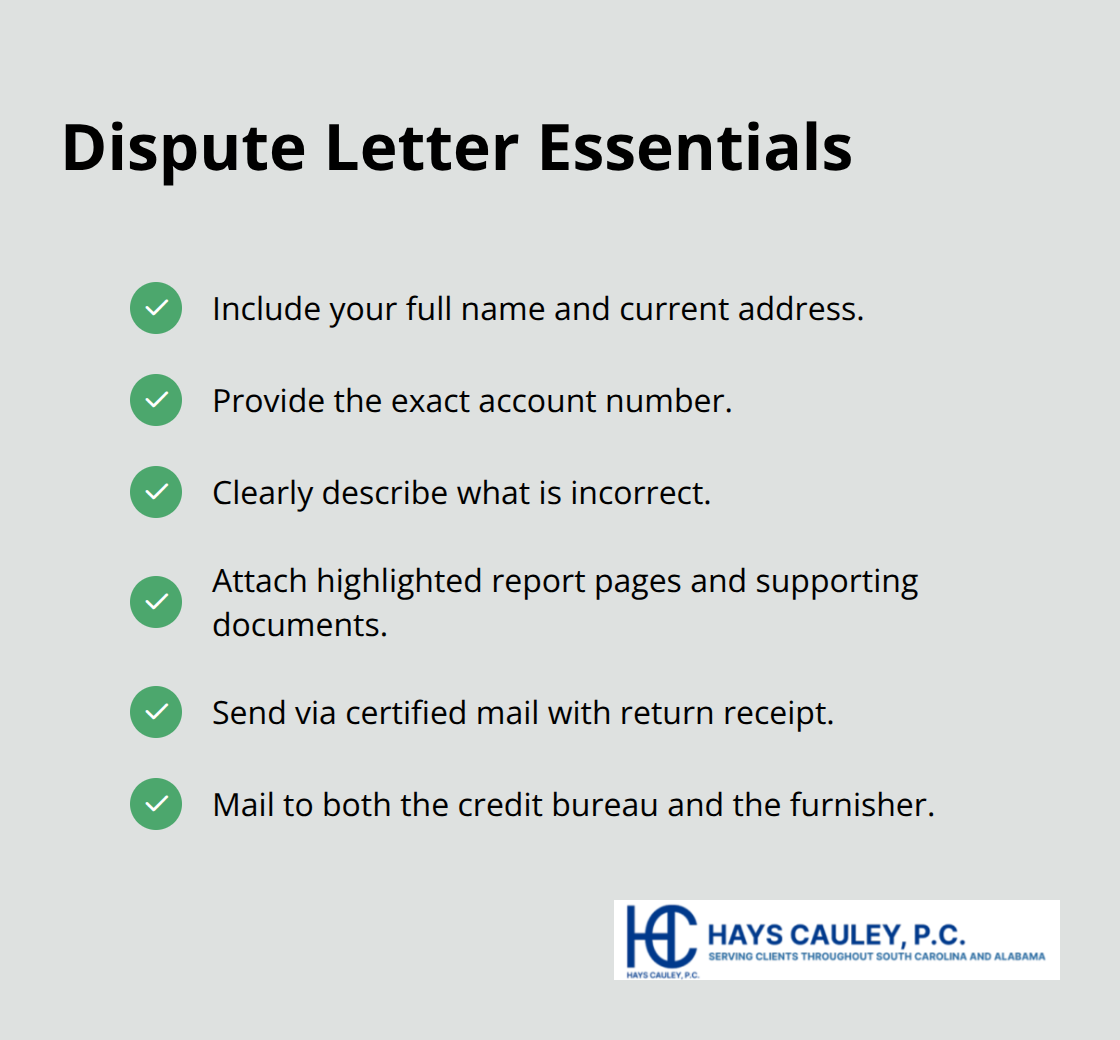

Write your dispute letter in plain language and keep it to one paragraph. Include your full name, current address, the exact account number, a clear description of what is wrong, and attach highlighted pages from your report with supporting documents. Send this package via certified mail with return receipt to both the credit bureau and the furnisher at their direct-dispute addresses.

For Equifax disputes, mail to P.O. Box 740256, Atlanta, GA 30348; for Experian, P.O. Box 4500, Allen, TX 75013; for TransUnion, P.O. Box 2000, Chester, PA 19016.

Track Your Dispute and Verify Results

Keep copies of everything you send and record the submission date and tracking number. The CFPB data shows about 70 percent of disputes result in some modification to the report, but that outcome depends on documentation quality and precision. Check your reports again about 45 days after filing to confirm corrections appeared. If the bureau did nothing, escalate immediately with the furnisher and provide more detailed documentation to push the correction forward.

What Happens During the Investigation Period

The credit bureau has exactly 30 days from the date they receive your dispute to investigate and respond. This is not a guideline-it is a legal requirement under the FCRA. The CFPB’s supervisory findings show that some bureaus delay investigations or fail to contact the furnisher properly, which violates your rights and can expose them to liability. During those 30 days, the bureau must forward all evidence you provided to the company that reported the information and request verification. If the furnisher cannot verify the accuracy of the information within that window, the bureau must delete it from your report. This is the critical point: inaccurate information that cannot be verified gets removed, period.

The Bureau’s Written Response

The bureau will send you written results of the investigation, and you should receive a free updated copy of your credit report showing the corrections. If the information was inaccurate, the furnisher must notify all three bureaus so the error does not reappear on reports from Equifax, Experian, or TransUnion. The furnisher also must notify the bureau that you are disputing the information if they continue reporting it after your challenge.

What to Do If the Investigation Fails

If the bureau concludes the information is accurate and refuses to remove it, you have additional options. The FTC reports that about 70 percent of disputes result in some modification, which means 30 percent do not-and those cases require escalation. You can add a statement of dispute directly to your credit file, which will appear on future reports and explains your position to lenders and employers who review your report.

File a Complaint and Create Official Records

You can also file a complaint with the CFPB through their Consumer Complaint Database, which creates an official record and often prompts bureaus to reconsider their position. If the bureau continues reporting information you have disputed, they must include a notation on your report that you are disputing it. This notation signals to creditors that the account status remains contested.

Pursue Legal Action for Continued Violations

If the information truly is inaccurate and the bureau refuses to correct it, or if the furnisher continues reporting false data after being notified of the dispute, you have grounds to pursue legal action under the FCRA. We at Hays Cauley, P.C. are a consumer protection law firm dedicated to helping consumers with credit reporting and related issues when the standard dispute process fails to produce results.

When the Dispute Process Isn’t Enough

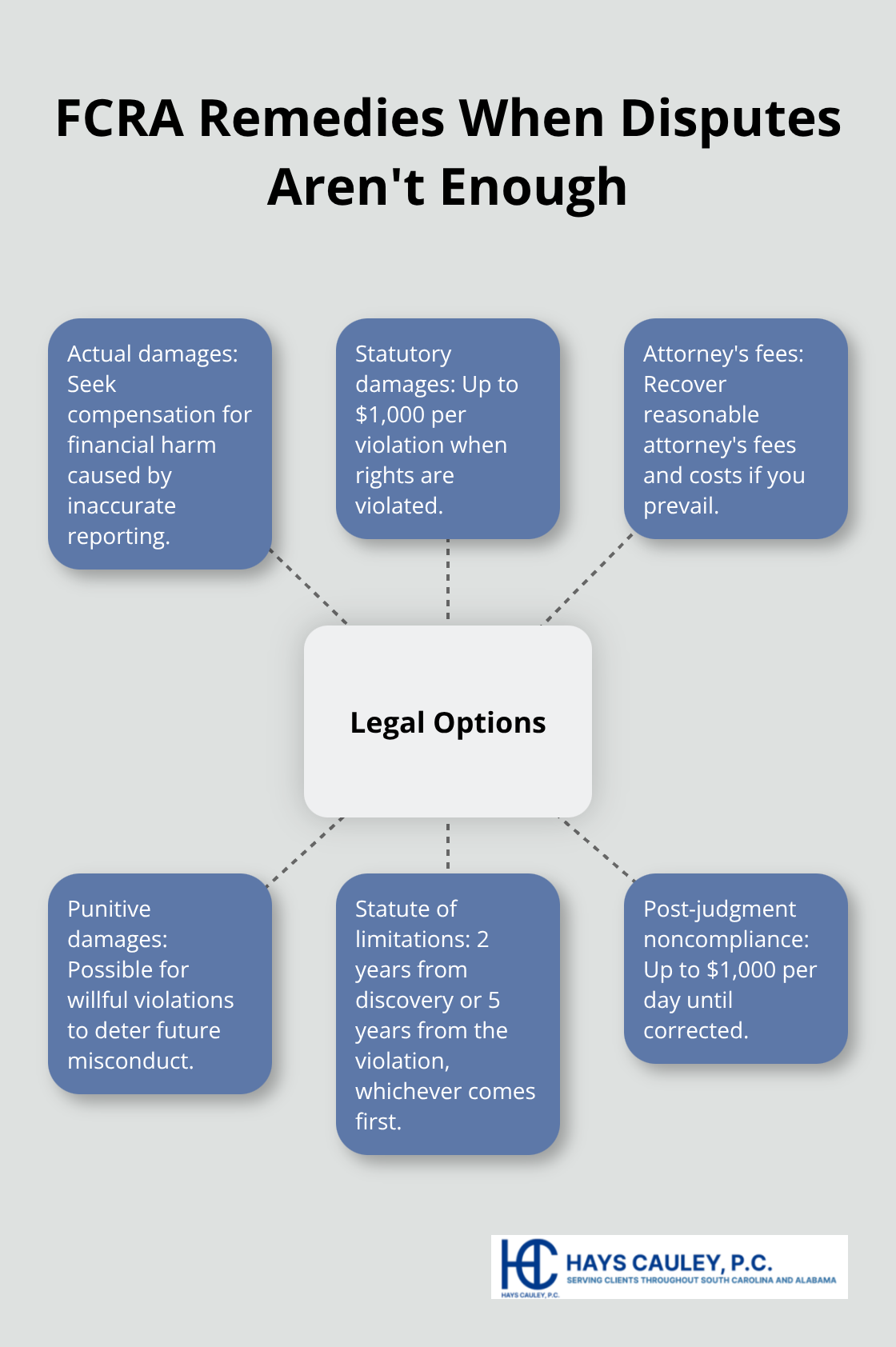

The standard dispute process works for many people, but not everyone. If you filed disputes, documented everything correctly, and the credit bureau still refuses to remove inaccurate information after 30 days, you need legal action. FCRA rights in South Carolina become actionable in court when bureaus ignore your disputes or furnishers continue reporting false information despite your challenges, and you can recover actual damages for financial harm, statutory damages up to $1,000 per violation, and attorney’s fees (willful violations may result in punitive damages as well).

The statute of limitations for FCRA claims runs two years from discovery or five years from the violation, whichever comes first, so timing matters. If a bureau fails to remove inaccurate information even after a judgment, damages accrue up to $1,000 per day until corrected. We at Hays Cauley, P.C. handle cases where bureaus and creditors break the law and work to restore your credit and financial future by holding them accountable.

Contact Hays Cauley, P.C. to discuss your situation and learn whether you have grounds for legal action under the FCRA.