Credit Report Error Investigation What To Expect

A credit report error investigation can feel overwhelming when you discover inaccuracies on your credit file. These mistakes-whether from data entry errors, identity theft, or outdated information-can damage your credit score and affect your ability to borrow money.

The good news is that you have legal rights and clear steps to challenge these errors. We at Hays Cauley, P.C. help South Carolina residents fight inaccurate credit reports and protect their financial futures.

How Credit Report Errors Happen: Serving South Carolina, including Greenville, Columbia and Charleston

Data Entry Mistakes Create Widespread Problems

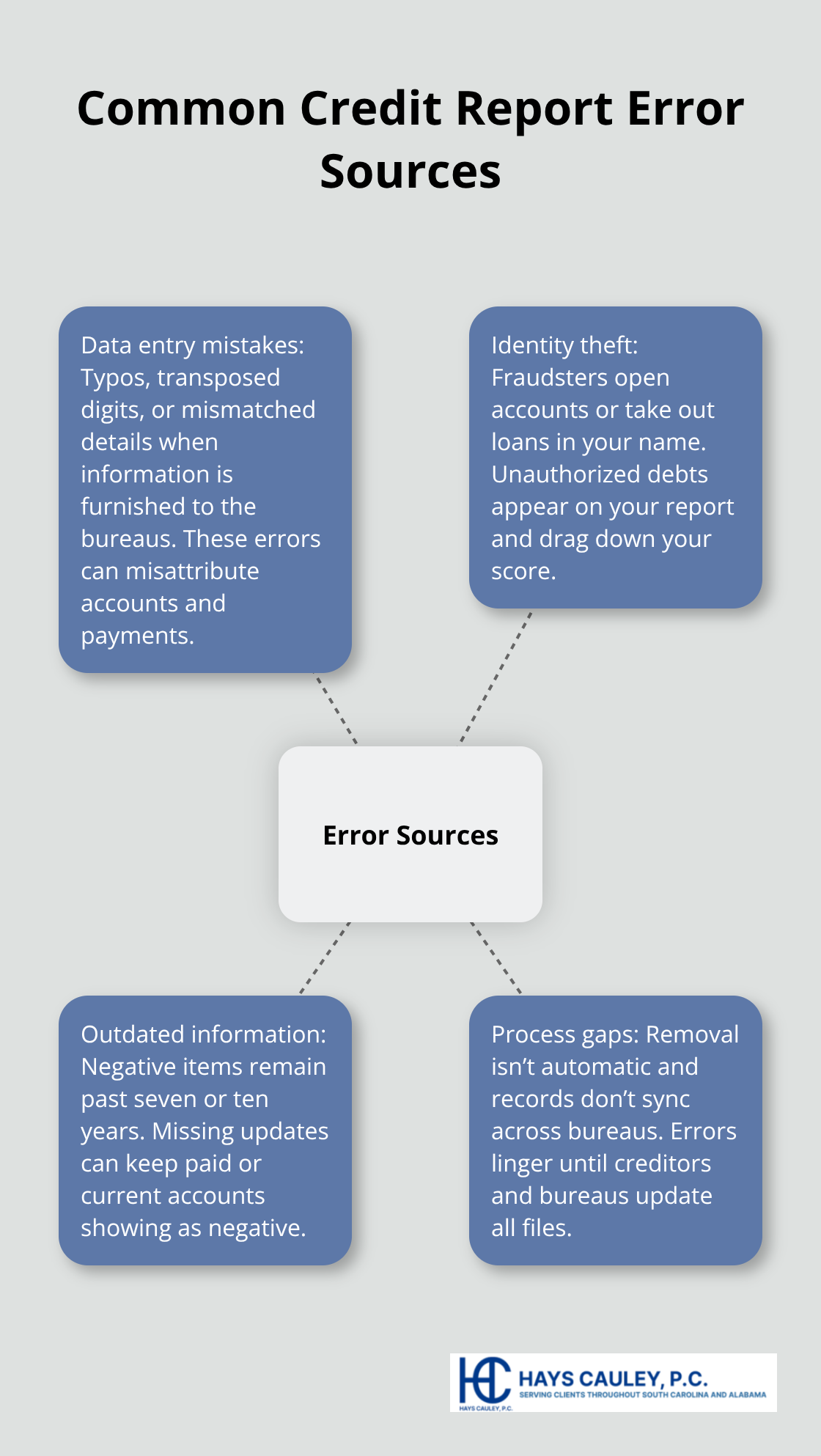

Data entry mistakes remain the most common reason errors land on your credit report. When a creditor reports your account information to Experian, Equifax, or TransUnion, a single typo-a wrong account number, transposed digits, or mismatched personal details-can create serious problems. These errors occur thousands of times each year because the reporting process involves manual data entry across multiple systems. A creditor might list your account under a similar name variation, or a payment intended for one account gets credited to another. The Federal Trade Commission found that roughly one in five Americans discovered errors on their credit reports, and many of these stemmed from simple data handling mistakes that took weeks or months to surface. The real problem is that these errors stay active while you fight them, potentially damaging your credit score during the investigation period.

Identity Theft Opens Accounts in Your Name

Identity theft represents a more serious source of credit report errors because fraudsters open accounts in your name without permission. This isn’t a data entry mistake-it’s deliberate criminal activity that requires immediate action. When someone steals your Social Security number or personal information, they can open credit cards, take out loans, or establish utility accounts that appear on your credit report. These fraudulent accounts tank your credit score while building debt you never incurred. If you suspect identity theft caused errors on your report, report it immediately at IdentityTheft.gov, which provides a personalized recovery plan and helps you document the fraud for credit bureaus and creditors. The Federal Trade Commission reports that identity theft complaints have increased significantly in recent years, making this a real threat you cannot ignore.

Outdated Information Lingers Past Legal Limits

Creditors and credit bureaus sometimes fail to remove information that legally should disappear from your report. Negative but accurate information like late payments should fall off after seven years, while bankruptcy information can stay for ten years according to federal law. Many credit reporting errors involve information that exceeded these timeframes but remained listed anyway. This happens because the removal process isn’t automatic-creditors must actively update their records and notify all three bureaus when an item should be deleted. When they don’t, outdated accounts continue damaging your score long after they should have been removed. Additionally, incomplete information gets reported when creditors fail to note that you’ve brought an account current or paid off a debt entirely.

Why These Errors Persist Without Action

Checking your credit reports from all three bureaus through annualcreditreport.com at least once yearly helps catch these persistent errors before they cause further damage to your financial standing. The three major bureaus-Experian, Equifax, and TransUnion-maintain separate files, and errors on one bureau don’t necessarily appear on the others. This means you must monitor all three reports to catch inaccuracies. Many consumers wait until they apply for a loan or mortgage to check their reports, by which time errors have already damaged their scores. The sooner you identify these mistakes, the sooner you can take action to correct them and protect your financial future.

Your Rights When Disputing Credit Report Errors: Serving South Carolina, including Greenville, Columbia and Charleston

Federal law gives you concrete power to force credit bureaus and creditors to investigate errors on your report. The Fair Credit Reporting Act requires that both the credit reporting agencies and the companies that furnish information to them investigate disputes within 30 days of receiving them. If you provide additional information during that initial investigation, the timeline extends to 45 days maximum according to the Consumer Financial Protection Bureau. This isn’t a suggestion-it’s a legal requirement with teeth. The CFPB enforces these rules, and violating them can result in penalties against the bureaus and furnishers.

How the Investigation Process Works

When you file a dispute in writing, the credit bureau must forward your dispute and all supporting documents to the company that reported the information, and that company must investigate and report back. If the furnisher finds the information is inaccurate, they must notify all three bureaus immediately so they update your file. You also have the right to add a brief dispute statement to your file if the investigation doesn’t resolve your concern, and that statement will appear on future reports sent to potential lenders and employers. The key advantage here is that the burden shifts to them-they must prove the information is accurate, not the other way around.

Craft Your Dispute Letter With Specific Details

Your dispute letter must contain precise information or the bureaus will reject it. Include your full name and current address, your confirmation number from the credit report if available, the account number of each disputed item, and a clear explanation of why the information is wrong. The Consumer Financial Protection Bureau provides a sample dispute letter template you should use as your foundation. Attach copies of supporting documents-never originals-such as bank statements, payment receipts, identity documents, or correspondence with creditors that prove your position.

Make a photocopy of your credit report and circle the errors you’re disputing so there’s no confusion about which items you’re challenging.

Mail your dispute using certified mail with return receipt requested; this proves the bureau received it and starts the 30-day clock. You can also file disputes online through Equifax, Experian, and TransUnion’s websites or call them directly at 866-349-5191 for Equifax, 888-397-3742 for Experian, and 800-916-8800 for TransUnion. Keep copies of everything-your letter, supporting documents, receipts, and correspondence-because you’ll need this documentation if the dispute doesn’t resolve to your satisfaction.

Track Your Investigation and Demand Updates

After filing your dispute, check your progress regularly through each bureau’s online portal. Equifax provides a 10-digit confirmation code after you file, and you can track status anytime in your account. The furnisher has five business days after the investigation closes to notify you of results, and the bureau must send you written notice of the investigation outcome along with an updated copy of your credit report. If the information is corrected, verify that all three bureaus reflect the change-corrections don’t automatically sync across all three.

If the investigation doesn’t resolve your dispute, contact the bureaus again to request they add a dispute statement to your file; this statement will appear on future reports sent to creditors and employers. Some bureaus charge a small fee to add dispute statements if the investigation found the information accurate, but you can request they notify creditors who received your report in the past six months at no cost. If a creditor continues reporting inaccurate information after your dispute, that’s a violation they must address with the bureau.

What Happens When Disputes Stall

Creditors and bureaus sometimes ignore legal timelines or fail to investigate properly. When this occurs, you need someone who understands consumer protection law to hold them accountable. We at Hays Cauley, P.C. help South Carolina residents navigate disputes when creditors and bureaus refuse to correct errors or when investigations drag on beyond legal requirements. The next section walks you through the specific steps to file your dispute and protect your rights throughout the process.

Taking Action: Your Step-by-Step Dispute Strategy

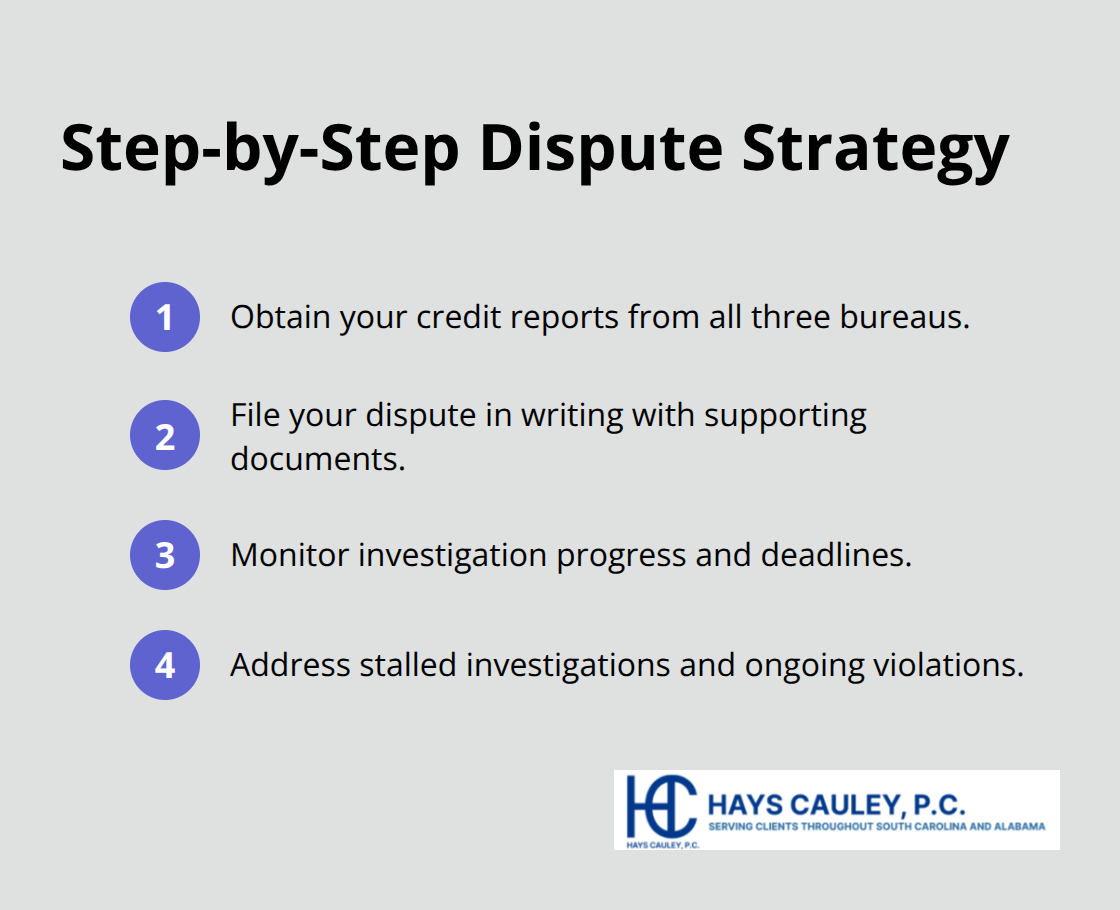

Obtain Your Credit Reports From All Three Bureaus

Your credit reports are the foundation of any successful dispute, and you need all three reports because errors don’t always appear consistently across Experian, Equifax, and TransUnion. Visit annualcreditreport.com to pull your free reports from all three bureaus at once, or space them out over the year to monitor changes quarterly. When you review each report, check your personal information for accuracy, verify that all accounts listed are actually yours, and flag any negative items that either contain errors or exceed their legal timeframes. The Consumer Financial Protection Bureau reports that roughly one in five Americans found errors on their reports, so take this review seriously. Write down the exact account numbers, creditor names, and specific inaccuracies you plan to dispute before you start the formal process.

File Your Dispute in Writing With Supporting Documents

File your dispute in writing with each bureau that has the error, using certified mail with return receipt so you have proof they received it. Your letter must include your full name and address, each account number you’re disputing, a clear explanation of why the information is wrong, and copies of supporting documents like bank statements, payment receipts, or correspondence with creditors. Mail to the appropriate address: Equifax Disclosure Department, P.O. Box 740241, Atlanta, GA 30374; Experian, P.O. Box 4500, Allen, TX 75013; TransUnion, P.O. Box 2000, Chester, PA 19022. You can also file disputes online through each bureau’s website or call them directly at 866-349-5191 for Equifax, 888-397-3742 for Experian, and 800-916-8800 for TransUnion.

Monitor Your Dispute Progress Throughout Investigation

Track your dispute immediately after filing. Equifax provides a 10-digit confirmation code you can use to monitor progress anytime in your myEquifax account. The investigation clock starts the moment the bureau receives your dispute, and they have 30 days to investigate, or 45 days if you submit additional information during the initial investigation period. Once the investigation closes, the furnisher has five business days to notify you of results.

When you receive the written notice and updated credit report, verify that corrections appear across all three bureaus and that any dispute statements were added to your file as requested.

Address Stalled Investigations and Continued Violations

If the investigation stalls or the bureau ignores legal timelines, that’s when you need professional help. We at Hays Cauley, P.C. hold creditors and bureaus accountable when they fail to investigate properly or continue reporting inaccurate information in violation of federal law. Creditors and bureaus sometimes ignore legal requirements or fail to investigate properly, and you deserve representation that understands consumer protection law and knows how to force compliance with federal regulations.

Final Thoughts

Credit report errors stem from data entry mistakes, identity theft, and outdated information that creditors fail to remove. Each type damages your financial standing differently, but all require immediate action to correct. A credit report error investigation takes time and persistence, yet the payoff protects your ability to borrow at favorable rates, qualify for housing, and maintain employment opportunities that depend on your credit history.

Inaccurate information costs you real money through higher interest rates and missed opportunities. The Federal Trade Commission found that roughly one in five Americans discovered errors on their reports, yet most never dispute them. Those who do dispute typically see corrections within 30 to 45 days, depending on complexity. The sooner you file your dispute with supporting documentation, the sooner you reclaim your financial reputation.

We at Hays Cauley, P.C. help South Carolina consumers navigate disputes when creditors and bureaus ignore legal timelines or refuse to correct inaccurate information. Our team holds furnishers and credit reporting agencies accountable when they violate federal law, and we know how to force compliance with the Fair Credit Reporting Act. Contact Hays Cauley, P.C. to protect your financial future and win your dispute.