Identity theft prevention in SC requires action now, not after fraud strikes. South Carolina residents lose millions annually to identity theft, with the average victim spending over 200 hours resolving the damage.

We at Hays Cauley, P.C. help residents understand the real threats and take concrete steps to protect themselves. This guide covers what identity theft costs you, how to stop it before it happens, and where to turn if you become a victim.

What Identity Theft Actually Costs You

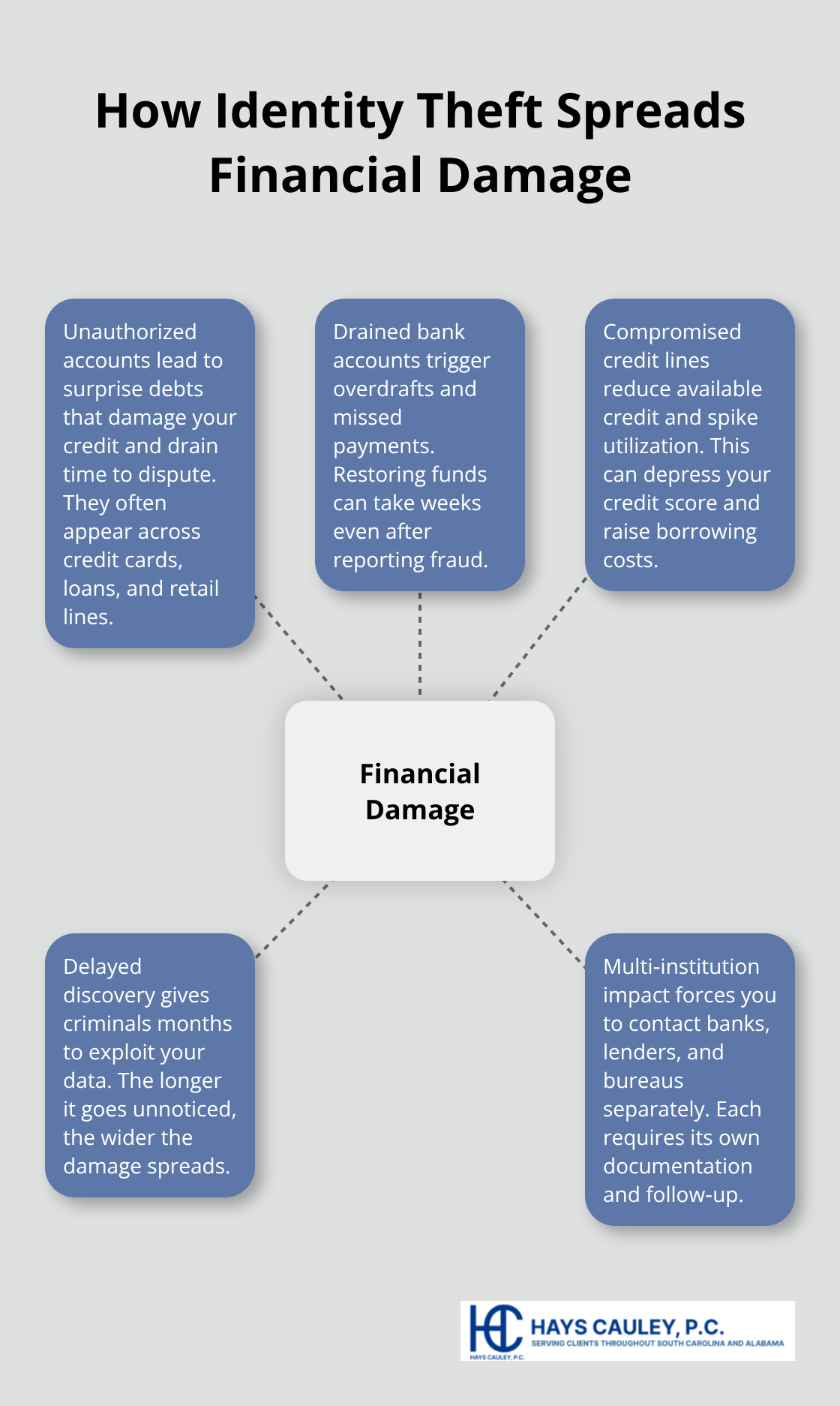

Financial Damage Spreads Across Multiple Accounts

The financial damage from identity theft in South Carolina extends far beyond the initial fraudulent charges. Victims face unauthorized accounts opened in their names, drained bank accounts, and compromised credit lines that take years to resolve. When someone uses your Social Security number, driver’s license number, or checking account information to commit fraud, the costs multiply quickly across multiple financial institutions. South Carolina Code § 16-13-510 recognizes identity fraud as a serious felony because the financial and personal consequences are severe. Many victims discover the theft months or even years after it occurs, meaning fraudsters have already caused substantial damage before any action takes place.

Credit Score Collapse and Long-Term Financial Consequences

The credit damage compounds the financial loss significantly. A fraudulent account can lower your credit score by 100 points or more, directly affecting your ability to secure loans, mortgages, or favorable interest rates. Lenders and creditors view the fraudulent accounts as legitimate debt, holding you responsible for charges you never made. The Federal Trade Commission reports that the average identity theft victim spends considerably more than 200 hours resolving the damage, which translates to lost wages, time away from family, and stress-filled interactions with creditors and credit bureaus.

The Dispute Process Demands Time and Persistence

South Carolina residents must file disputes with each credit bureau separately, provide documentation of the fraud, and wait 30 days for reinvestigation results. Even after disputes are filed, inaccurate information sometimes reappears on your credit report, forcing you to file again. This cycle of disputing, waiting, and refiling consumes months or years of your life.

Psychological Impact and Lasting Stress

The emotional toll of watching your financial reputation crumble while fighting to prove the fraud wasn’t your fault creates lasting psychological stress. Many victims report anxiety about opening mail, checking their credit, or making purchases because the experience leaves them hypervigilant about their finances. Some South Carolina residents turn to legal support to navigate credit bureau disputes and hold fraudsters accountable, rather than fighting the system alone. Understanding these costs-financial, emotional, and temporal-makes prevention strategies not just advisable but necessary before theft strikes your accounts.

How to Stop Identity Theft Before It Happens: Serving South Carolina, including Greenville, Columbia and Charleston

Monitor Your Credit Reports Constantly, Not Just Once a Year

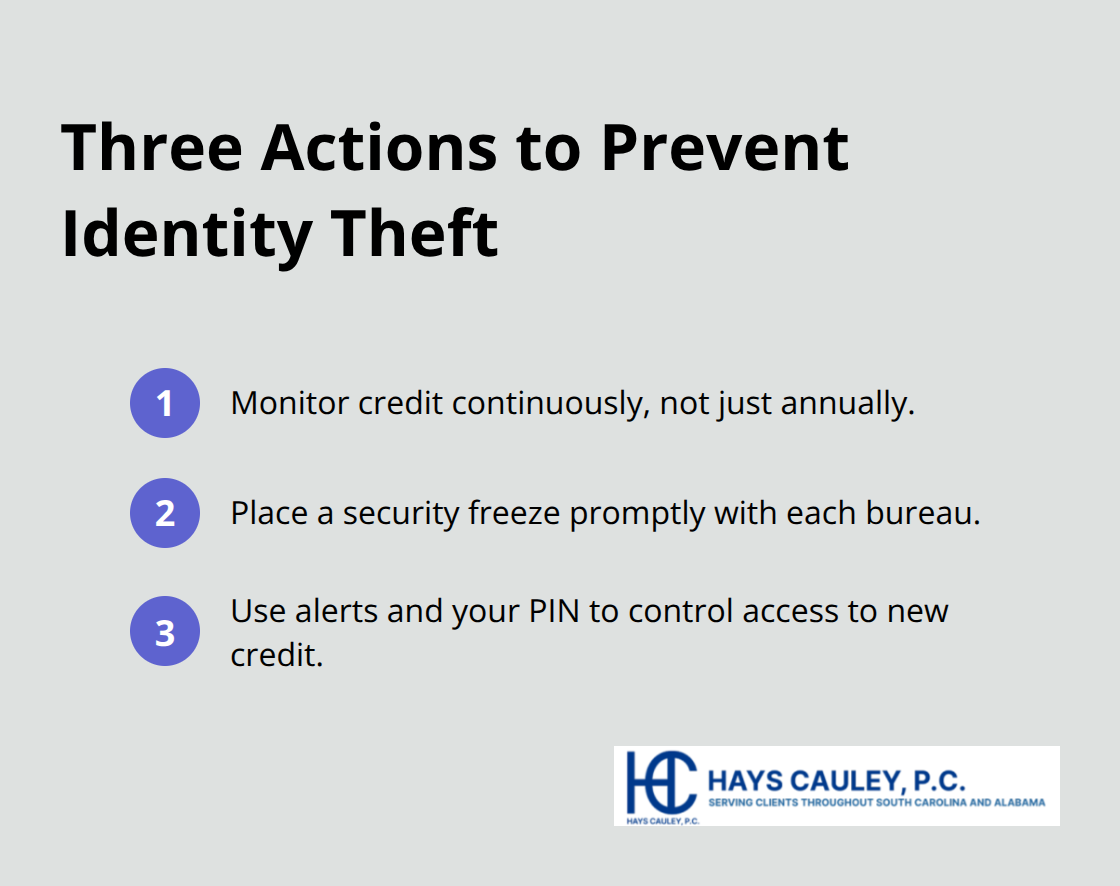

Three simultaneous actions stop identity theft before it damages your finances. First, you must monitor your credit reports constantly rather than waiting for annual checkups. The Federal Trade Commission allows you to access your credit report free once yearly from each of the three major bureaus through annualcreditreport.com, but this annual approach leaves you exposed for 365 days. South Carolina law permits you to place a security freeze on your credit file within five business days of requesting one, which blocks fraudsters from opening accounts in your name even if they possess your Social Security number, driver’s license number, or other identifying information.

The credit-reporting agency must send written confirmation and provide a unique PIN within ten business days. This freeze stops the most common identity theft vector cold.

Secure Your Social Security Number and Financial Documents

Second, you must actively secure the specific documents and numbers that criminals target most aggressively. Your Social Security number appears on tax returns, bank statements, and insurance documents that sit in your home unprotected. South Carolina Code § 37-20-10 prohibits public posting or display of Social Security numbers, and companies cannot print them on cards or require them over insecure internet connections. You should shred any document containing your Social Security number, checking account number, savings account number, credit card number, debit card number, or PIN before disposal. Many South Carolina residents store these documents in accessible locations where household members, contractors, or visitors can photograph them with smartphones. Use a locked file cabinet or safe deposit box instead.

Create Barriers That Make Credential Theft Substantially Harder

Third, you must create barriers that make stealing your credentials substantially harder than targeting someone else. You should enable two-factor authentication on every financial account, email address, and password manager you use. This single step stops 99.9 percent of account takeovers because fraudsters rarely possess both your password and your phone. Use a password manager like Bitwarden or 1Password to generate unique passwords containing 16 characters with mixed uppercase, lowercase, numbers, and symbols for each account rather than reusing passwords across sites. South Carolina victims who enable two-factor authentication report zero fraudulent account access, while those relying on passwords alone experience repeated unauthorized logins months after initial detection.

What Happens When Prevention Fails

These three defenses work together to create multiple obstacles that stop most fraudsters before they cause damage. However, prevention sometimes fails despite your best efforts. When criminals breach your information through data breaches at retailers, healthcare providers, or financial institutions, you need to know exactly what steps to take next and where to find support.

What to Do Immediately After Identity Theft Strikes

Act Fast to Place Fraud Alerts

The moment you suspect identity theft, speed matters more than perfection. Contact the three major credit bureaus-Equifax at 888-836-6351, Experian at 888-397-3742, and TransUnion through transunion.com-and place a fraud alert on your file. Once one bureau confirms the alert, the others receive notification automatically, and the entire process takes less than an hour. South Carolina law requires credit-reporting agencies to respond to your fraud alert within one business day and send written confirmation with a unique PIN within ten business days.

This alert forces creditors to verify your identity before opening new accounts, blocking the primary vector criminals use to multiply damage.

File a Police Report and Report to the FTC

After placing the alert, file a police report with your local South Carolina law enforcement agency and request a copy for your records. This report becomes your proof of victimhood when disputing fraudulent accounts with creditors and credit bureaus. Next, contact the Federal Trade Commission through their ID Theft Complaint Form at reportidentitytheft.ftc.gov or call 877-438-4338. The FTC maintains a database of identity theft complaints that helps law enforcement identify patterns and prosecute criminals operating across multiple states.

Close Compromised Accounts Immediately

Close any compromised financial accounts immediately and contact your banks, credit card issuers, and other financial institutions to report the fraud. Many institutions can reverse fraudulent charges within 60 days if you report them quickly, but waiting weeks allows criminals to drain accounts completely. South Carolina’s Department of Consumer Affairs Identity Theft Unit provides free, personalized guidance through their intake form and one-on-one assistance at idthefthelp@scconsumer.gov, 800-922-1594, or 293 Greystone Boulevard Suite 400 in Columbia.

Use Official Resources and Dispute Fraudulent Accounts

The unit offers step-by-step checklists for specific fraud types-tax fraud, benefits fraud, medical identity theft, government-issued identification theft-and provides tools to determine whether your data was stolen in a breach. Resources include guidance on credit and debit card fraud response, protected consumer freezes for minors, and child identity theft prevention. When disputing fraudulent accounts with credit bureaus, provide documentation proving you did not authorize the accounts, and the bureaus must reinvestigate at no cost and respond within 30 days with findings and a corrected file. South Carolina law allows you to recover three times your actual damages or up to 1,000 dollars per incident from credit-reporting agencies for willful violations, plus attorney fees. If disputes stall or inaccurate information reappears after correction, a consumer protection law firm can help South Carolina residents hold credit bureaus accountable and navigate the recovery process when fighting alone fails.

Final Thoughts

Identity theft prevention in SC requires three concrete actions that stop most fraudsters before they cause damage: monitor your credit reports through security freezes, protect your Social Security number and financial documents, and enable two-factor authentication on every account. The cost of inaction far exceeds the time required for prevention, as South Carolina residents who ignore these steps face months of disputes with credit bureaus, damaged credit scores that affect loan approvals for years, and the emotional stress of watching fraudsters drain accounts. The financial damage spreads across multiple institutions, and the recovery process demands persistence that many victims cannot sustain alone.

We at Hays Cauley, P.C. understand the frustration of fighting identity theft without professional guidance. If your prevention efforts fail or you discover fraudulent accounts already opened in your name, contact us to discuss your situation and explore your legal options. Taking action now prevents the costly recovery process later.