Your credit reporting rights in South Carolina are stronger than many residents realize. Errors on your credit report can damage your financial future, yet most people don’t know how to challenge them.

We at Hays Cauley, P.C. have helped countless South Carolina residents protect their credit reporting rights SC and hold creditors accountable. This guide walks you through your protections under state and federal law, how to spot inaccuracies, and what legal options you have when violations occur.

What South Carolina and Federal Law Actually Protect

Federal Protections Under the Fair Credit Reporting Act

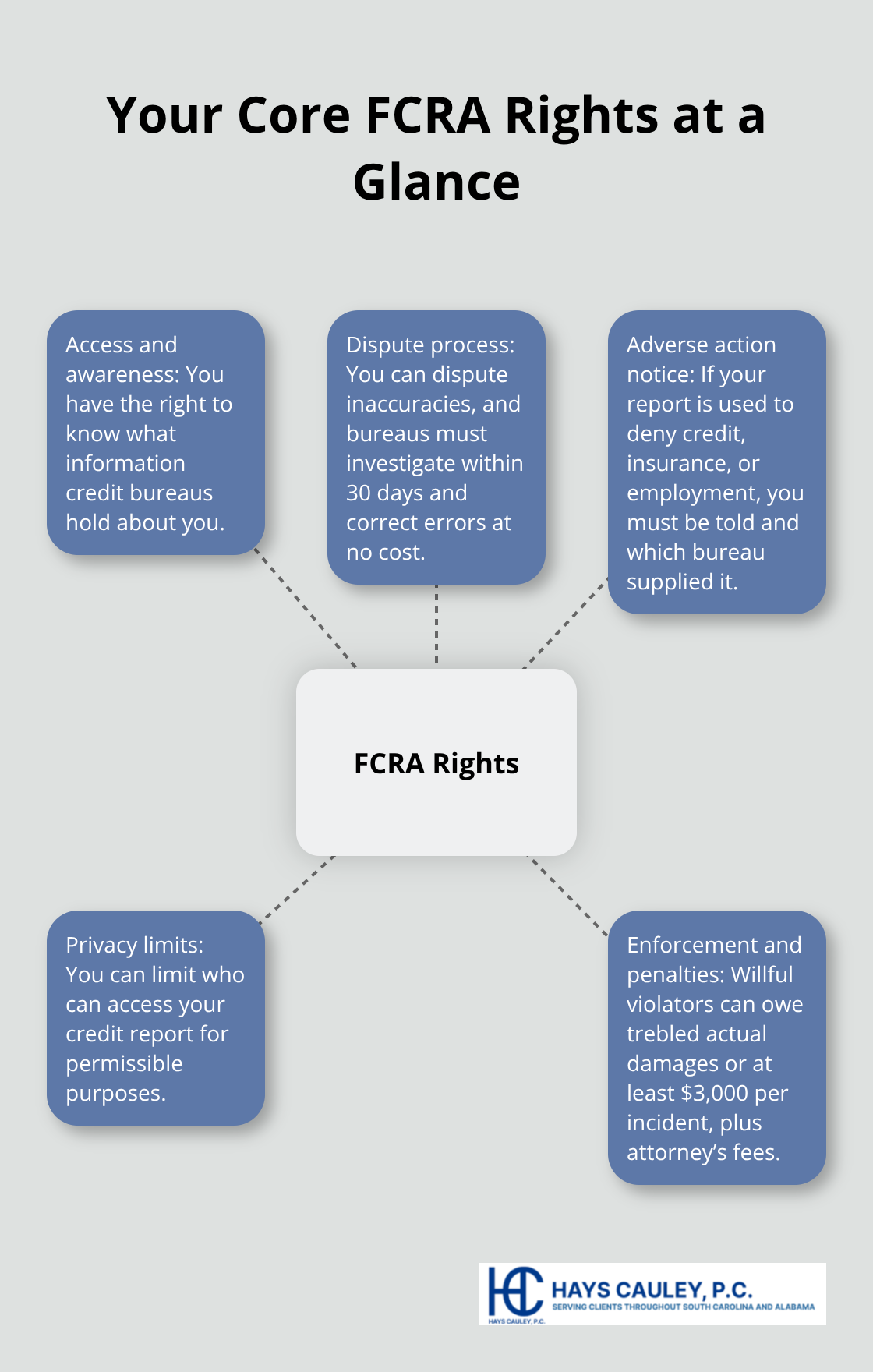

The Fair Credit Reporting Act, passed in 1970 and revised most recently in March 2026, forms your foundation for credit reporting protection. This federal law applies across all states and grants you the right to know what information credit bureaus hold about you, to dispute inaccuracies, and to limit who can access your report. The FTC enforces FCRA violations, and violators face serious penalties-willful violations result in trebled actual damages or at least $3,000 per incident, plus attorney’s fees. The FCRA requires that consumer reporting agencies investigate disputes within 30 days and correct errors at no cost to you. If a credit bureau uses your report to make an adverse decision about credit, insurance, or employment, they must notify you and tell you which bureau provided the report.

South Carolina’s Additional Layer of Protection

South Carolina strengthens these federal protections with its own Consumer Identity Theft Protection Law under Title 37, Chapter 20. This state law covers any SC resident engaged in personal, family, or household transactions and adds significant teeth to identity theft prevention. Willful violations carry trebled actual damages or at least $1,000 per incident, and negligent violations carry actual damages or at least $1,000 per incident. South Carolina law also grants you the right to place a security freeze on your consumer file within five business days at no charge. Any temporary lift of that freeze activates within about 15 minutes when you need credit. If you dispute information in your file, both the credit bureau and the business that reported the information must reinvestigate for free and respond within 30 days.

Accessing Your Credit Report for Free

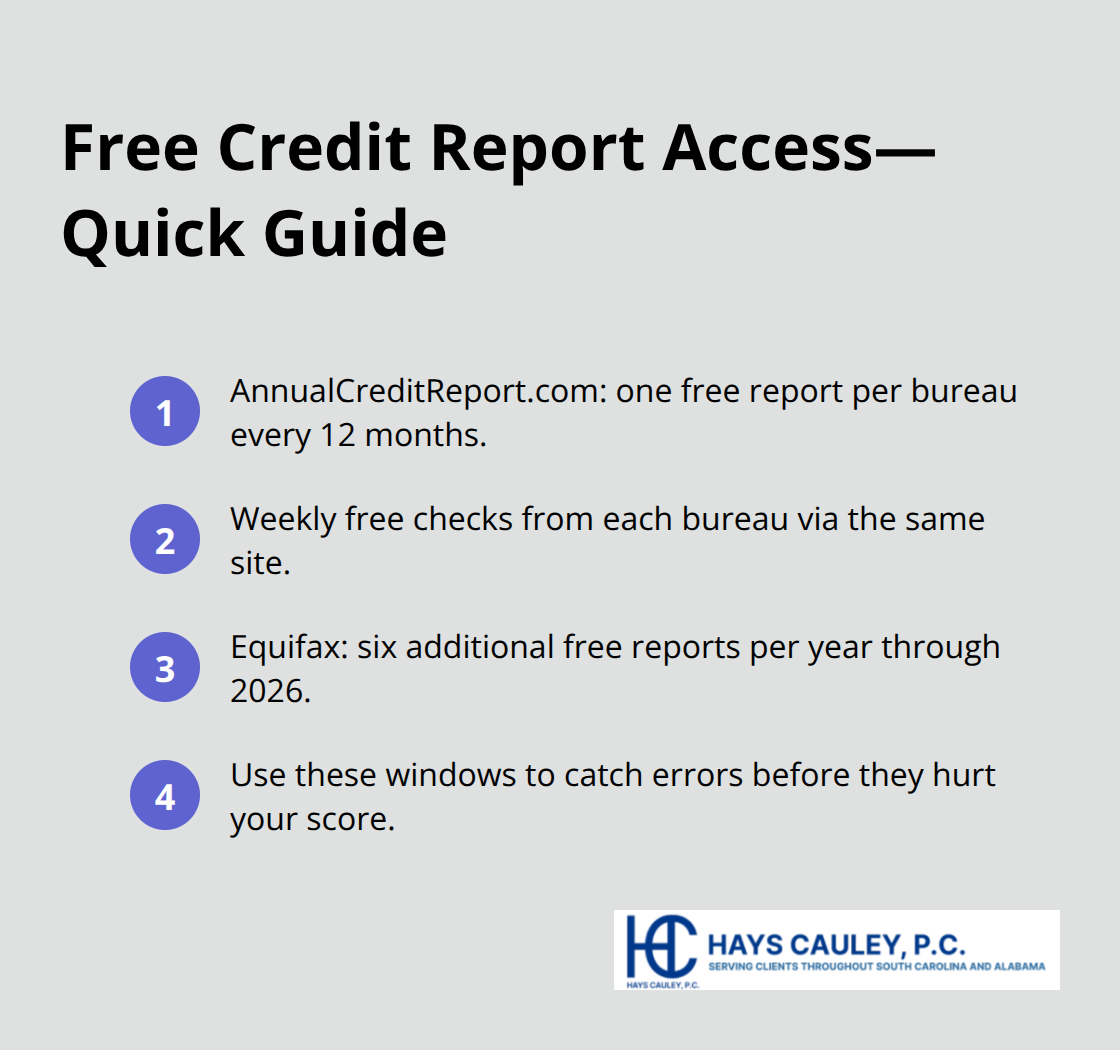

Your right to access your credit report is absolute and free. You can obtain a free copy from each of the three major bureaus-Equifax, Experian, and TransUnion-once every 12 months through AnnualCreditReport.com, the official site authorized by federal law. All three bureaus have permanently extended a program that lets you check each bureau’s report once a week at no cost through the same site. Equifax offers six free reports per year through 2026 by visiting their site or calling 1-866-349-5191. This means you have multiple opportunities annually to catch errors before they damage your score.

Spotting Inaccuracies That Cost You Money

A single 30-day late payment can drop your score by 100 points or more depending on your starting score. Negative items like charge-offs, collections, and tax liens stay on your report for seven years. When you pull your reports, compare them side by side across all three bureaus and look for unfamiliar accounts, wrong addresses, duplicate entries, incorrect balances, and misdated late payments. Industry data estimates around 13 million people per year encounter inaccuracies on their credit reports. These errors are far more common than most residents realize, which makes regular monitoring essential.

Taking Control Through Disputes

If you spot errors, you have the power to challenge them directly with the bureau or the creditor that reported the information. Both are required to investigate at no charge and correct the record if the information proves inaccurate. The dispute process itself is straightforward, but understanding what happens next-and how to respond if the bureau denies your claim-determines whether you actually get the correction you need. This is where many South Carolina residents stumble, not because they lack rights, but because they don’t know how to exercise them effectively.

How to Get Your Free Credit Reports and Challenge Errors

Access Your Reports Without Spending Money

Visit AnnualCreditReport.com and request reports from all three bureaus-Equifax, Experian, and TransUnion. You receive one free report from each bureau every 12 months, but the program now offers permanent weekly free access at the same site. Equifax provides six free reports annually through 2026 by visiting their site directly or calling 1-866-349-5191. This eliminates any barrier to monitoring your credit.

Pull your reports immediately, then set a schedule to check them every four to six weeks. When you receive each report, print or save it and compare all three side by side. Look specifically for unfamiliar accounts you never opened, addresses where you never lived, duplicate entries with slightly different names, incorrect account balances, and late payments dated wrong or appearing after you paid them.

Recognize What Errors Look Like

Industry data shows approximately 13 million people annually find errors on their reports. These aren’t rare mistakes-they’re common enough that you should expect to find something. A single 30-day late payment can drop your score by 100 points or more depending on your starting score. Negative items like charge-offs, collections, and tax liens stay on your report for seven years, making accuracy critical to your financial health.

File Your Dispute the Right Way

When you find an inaccuracy, act fast. Write a dispute letter to each bureau reporting the error, explain exactly what’s wrong, and attach copies of supporting documents like bank statements or payment receipts. Include a copy of your report with the errors circled. Send it by certified mail with return receipt requested so you have proof of delivery. The FTC provides a sample dispute letter on their website.

You can also dispute online or by phone directly with Equifax, Experian, and TransUnion, though written disputes create better documentation. The bureau must investigate within 30 days and correct the information if it’s inaccurate, then notify the business that reported it so they update their records too.

Push Back When Disputes Get Denied

If the bureau denies your dispute, you can add a statement of dispute to your file that appears on future reports. Don’t stop there-contact the creditor or business that reported the error directly using the same written approach. Creditors often respond faster than bureaus when they see documentation proving the information is wrong. If corrections don’t happen within 45 days after your initial dispute, violations may have occurred that warrant legal action from a consumer protection law firm like Hays Cauley, P.C., serving South Carolina, including Greenville, Columbia and Charleston.

When disputes stall and corrections fail to materialize, understanding your legal options becomes the next critical step in protecting your financial future.

When Credit Bureaus Refuse to Fix Errors

Recognizing When Violations Occur

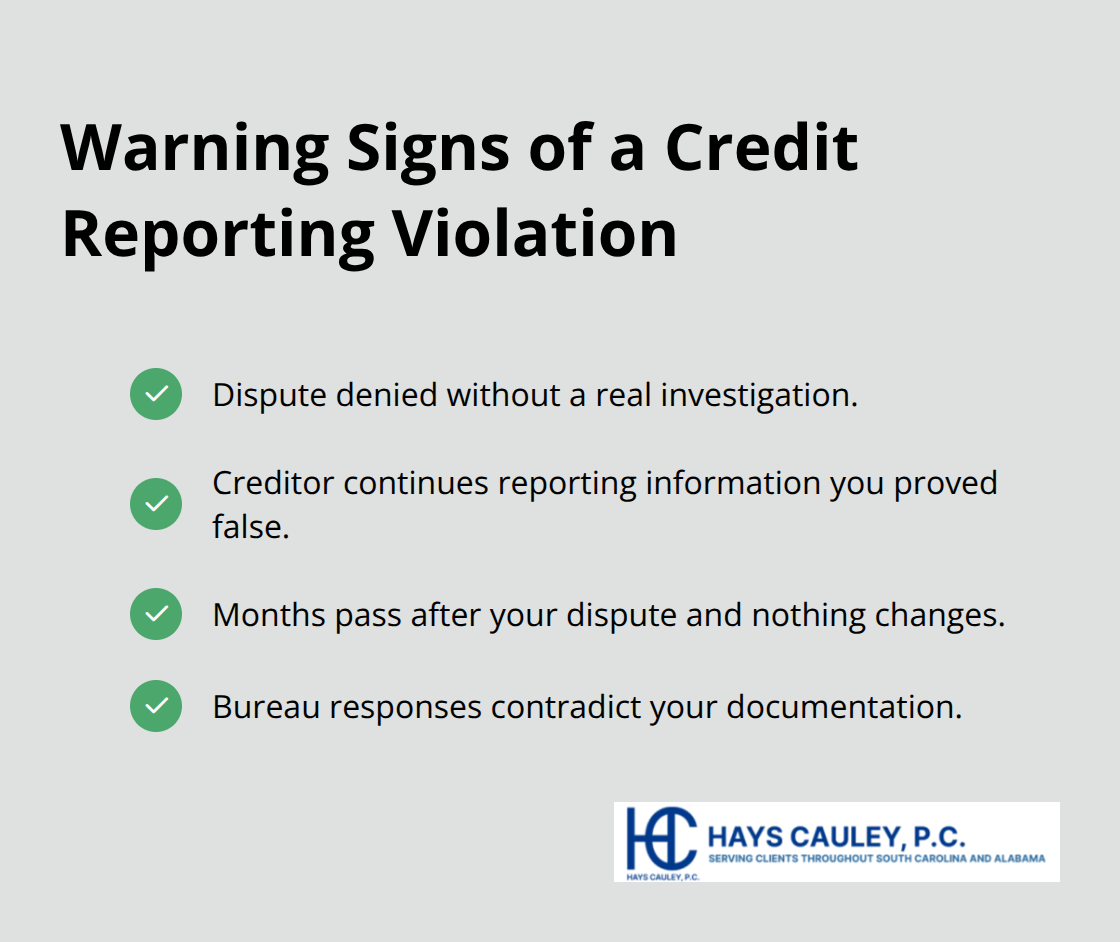

Credit reporting violations rarely announce themselves loudly. A bureau denies your dispute without adequate investigation. A creditor ignores your correction request and continues reporting the same false information. Months pass after you filed your dispute and nothing changes.

The FTC receives thousands of complaints annually from consumers whose disputes vanish into bureaucratic black holes. South Carolina law requires reinvestigation within 30 days, but many bureaus and creditors simply ignore this requirement or conduct investigations so cursory they amount to rubber-stamping the original error. When a bureau receives your dispute and the furnishing creditor fails to investigate or reports back without actually verifying the information, that’s a willful violation under federal law. Negligent violations occur when the bureau or creditor should have investigated but didn’t follow proper procedures. The difference matters because willful violations under the Fair Credit Reporting Act allow you to recover trebled actual damages or at least $3,000 per incident, plus your attorney’s fees.

Building Your Documentation Case

Start building your case immediately by organizing every piece of communication. Save your original dispute letter with proof of delivery, the bureau’s response letter, any correspondence with the creditor, bank statements showing you paid the account, and your credit reports showing the error persists. Take screenshots of online disputes and note dates, times, and names of anyone you spoke with by phone. If the bureau claims they investigated but the error remains unchanged, request a copy of their investigation file under the Fair Credit Reporting Act, which they must provide. Many violations become obvious when you see what the bureau actually did-which is often nothing.

Calculating Your Financial Harm

Document how the error affected you financially (increased interest rates you paid, higher insurance premiums, or denied credit). A single 30-day late payment can reduce your score by 100 points or more, and that score difference translates to thousands in additional borrowing costs over your lifetime. This documentation strengthens your case significantly when violations persist.

When Legal Action Becomes Necessary

When corrections don’t happen after 45 days of your initial dispute, South Carolina law and federal law both provide grounds for legal action. Violations that persist after judgment can accrue up to $1,000 per day in additional damages. If you can document that a bureau stalled for more than 30 days, failed to contact the creditor, or ignored evidence you provided, you have a strong case. A consumer protection law firm can review your documentation and determine whether your case qualifies for litigation.

Final Thoughts

Your credit reporting rights in South Carolina are real and enforceable under both federal and state law. The Fair Credit Reporting Act and South Carolina’s Consumer Identity Theft Protection Law give you concrete power to challenge inaccuracies, freeze your file, and hold bureaus accountable when they ignore your disputes. Start this week by pulling your free credit reports from all three bureaus through AnnualCreditReport.com, compare them side by side, and mark any unfamiliar accounts or incorrect balances.

If a bureau denies your dispute without proper investigation or continues reporting false information after 30 days, violations have likely occurred. Document everything, request copies of the bureau’s investigation file, and calculate how the error affected your borrowing costs. When corrections don’t happen within 45 days of your initial dispute, legal action may be your most effective option to protect your credit reporting rights SC.

We at Hays Cauley, P.C. help South Carolina residents protect their credit reporting rights and hold creditors and bureaus accountable when violations occur, serving South Carolina, including Greenville, Columbia and Charleston. If you’ve disputed errors that remain uncorrected or suspect a bureau violated federal law, contact us for a free consultation to discuss your situation.