Verify Credit Bureau Data How To Ensure Your Credit Reports Are Accurate

Your credit report affects your ability to borrow money, rent an apartment, and sometimes even get hired for a job. Errors on these reports happen more often than you’d think, and they can cost you thousands of dollars in higher interest rates or denied applications.

To verify credit bureau data, you need to know where to look and what mistakes to watch for. We at Hays Cauley, P.C. help people challenge inaccuracies and protect their financial futures.

Where Your Credit Report Data Comes From

Three major credit bureaus-Equifax, Experian, and TransUnion-build your credit report from data supplied by lenders, creditors, debt collectors, and the court system. Banks report your payment history, credit card companies submit balance information, and collection agencies add accounts they’ve purchased. This constant flow of data means your report changes frequently, and mistakes slip through regularly. The 2013 FTC study found that 1 in 5 consumers had errors on at least one of their three credit reports, and roughly 1 in 4 consumers identified errors that could affect their credit scores. These aren’t rare edge cases-they’re common problems that impact millions of people’s borrowing costs and financial opportunities.

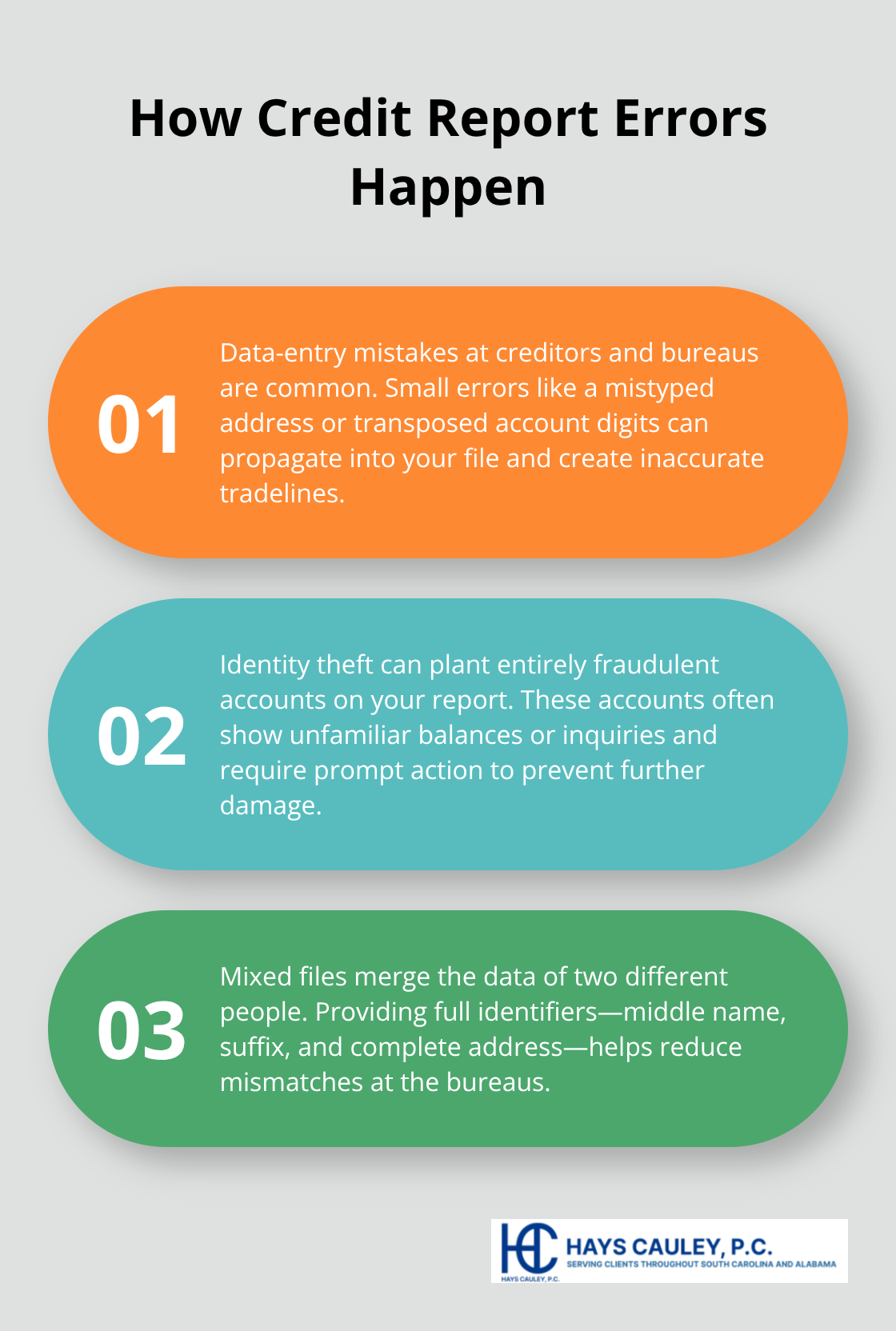

How errors enter your file

Creditors make data-entry mistakes when they submit information to the bureaus. A typo in your address, a transposed digit in your account number, or confusion between you and someone with a similar name can all create inaccuracies. Identity theft creates more serious errors, with fraudulent accounts appearing under your name.

Mixed files occur when two people’s credit data get merged in a bureau’s database, which happens more often when people share similar names, Social Security numbers, birthdates, or addresses. When you apply for credit, provide complete identification information including middle name, suffix, and full address to reduce the chance of mismatches. Examine your bills carefully each month to spot charges that don’t belong to you before they reach the bureaus.

What errors look like on your report

Common errors include misspelled names, wrong phone numbers, incorrect addresses, closed accounts still listed as open, accounts marked as yours when you’re only an authorized user, and late payments on accounts that were paid on time. Dates matter too-check that the last payment date, date opened, and date of first delinquency are correct. Some people find the same debt listed multiple times under different creditor names. Data management errors like incorrect current balances or credit limits appear frequently. The FTC study showed that when consumers actually disputed errors, four in five experienced some modification to their credit report, and slightly more than one in ten saw their credit score change. This means errors are fixable, but you have to find them first.

Taking action on what you find

Once you spot an error, you have two paths forward. You can contact the credit reporting company directly to dispute the inaccuracy, or you can reach out to the creditor (the furnisher of the information) who reported it. Most effective disputes involve both-the credit reporting company must investigate and forward relevant information to the furnisher, while the furnisher must verify or correct the data within 30 days. If the furnisher confirms the information is accurate and won’t update it, you can ask the bureaus to include a dispute statement on your file. This statement travels with your report and appears to future lenders and others who request it. Understanding these options puts you in control of your financial record and sets the stage for the formal dispute process.

How to Get and Review Your Credit Reports

Access Your Free Credit Reports the Right Way

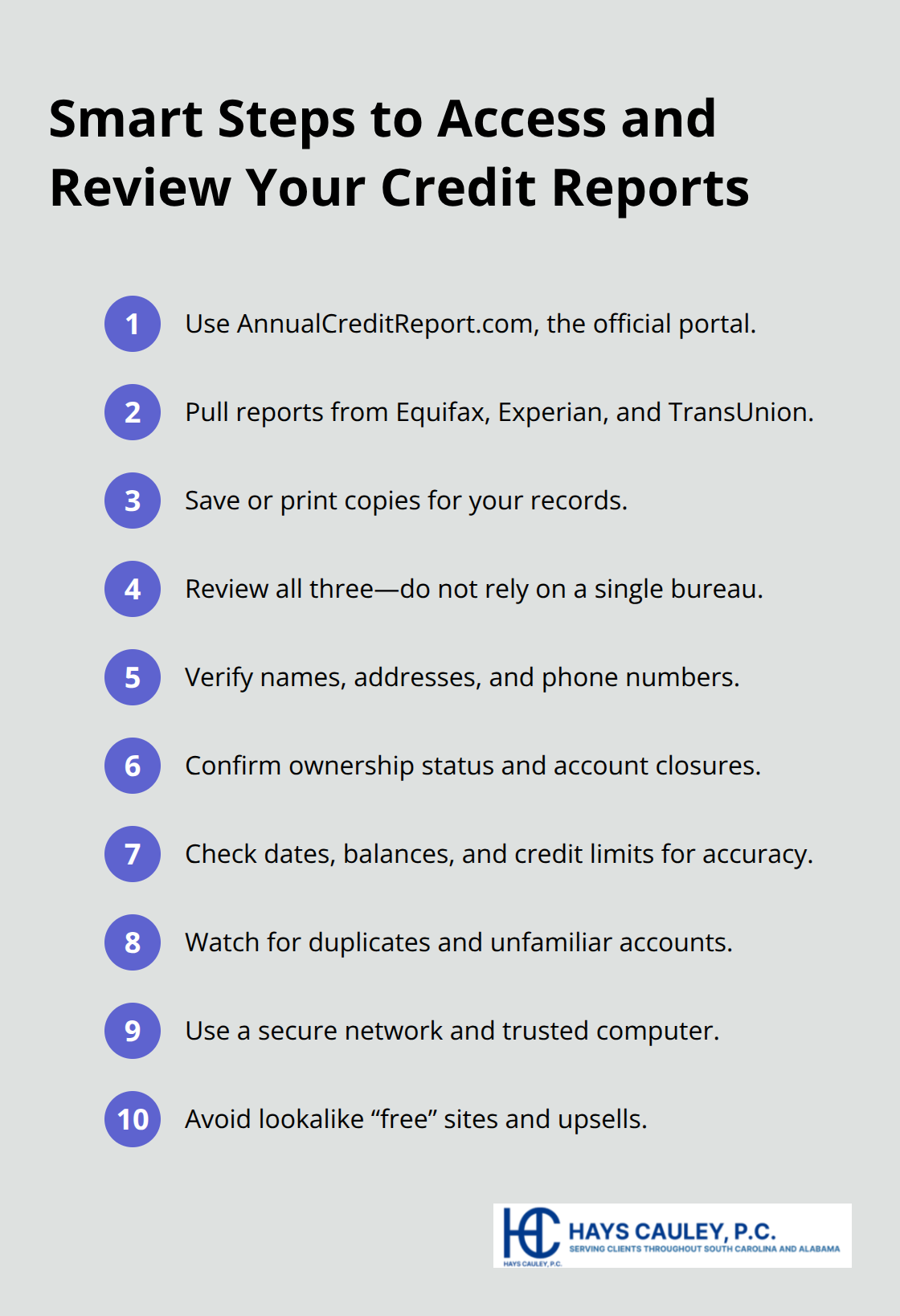

Getting your hands on your actual credit reports is the only way to spot errors before they damage your finances. Head to annualcreditreport.com, the official site mandated by federal law to provide free reports from Equifax, Experian, and TransUnion. You receive one free report from each bureau every 12 months, though you can also request free weekly reports year-round from all three. Don’t trust lookalike websites promising free credit reports-they exist to harvest your personal information or sell you unnecessary services. Use a regular computer on a secure network when accessing annualcreditreport.com since mobile devices and unsecured networks put your data at risk. The site offers access in Braille, Large Print, and Audio Format if you need those accommodations.

Once you pull your reports, print them out or save them as PDFs so you have a record to reference while reviewing. Many people check only one bureau’s report, but the 2013 FTC study found that 1 in 5 consumers had errors on at least one of their three reports-meaning you could miss problems if you skip any of them.

Hunt for Common Mistakes in Your File

Now comes the hard part: actually reading through your reports and hunting for mistakes. Look for misspelled names, wrong phone numbers, or incorrect addresses listed under your information. Check whether closed accounts still show as open, and verify that you appear as the account owner rather than just an authorized user on accounts that aren’t yours. Scan for duplicate listings of the same debt under different creditor names, and examine dates carefully-verify the last payment date, date opened, and date of first delinquency match your actual payment history. Watch for accounts marked as late or delinquent when you paid on time, and verify that current balances and credit limits are correct.

Document Everything for Your Dispute

Create a document listing each error you find, including the account number, the specific inaccuracy, and what the correct information should be. Gather supporting documents like bank statements, payment confirmations, or account statements that prove the error. The FTC study showed that four in five consumers who disputed errors experienced some modification to their credit report, which means your documentation matters-it’s what makes the difference between a dispute that gets dismissed and one that gets fixed. This preparation work takes time, but it separates people who complain about errors from people who actually get them removed.

With your errors documented and your evidence collected, you now have everything you need to move forward with the formal dispute process. The next section walks you through exactly how to file disputes with the credit bureaus and creditors who reported the inaccurate information.

How to File and Win Credit Disputes

Send Your Dispute Letter to the Credit Bureau

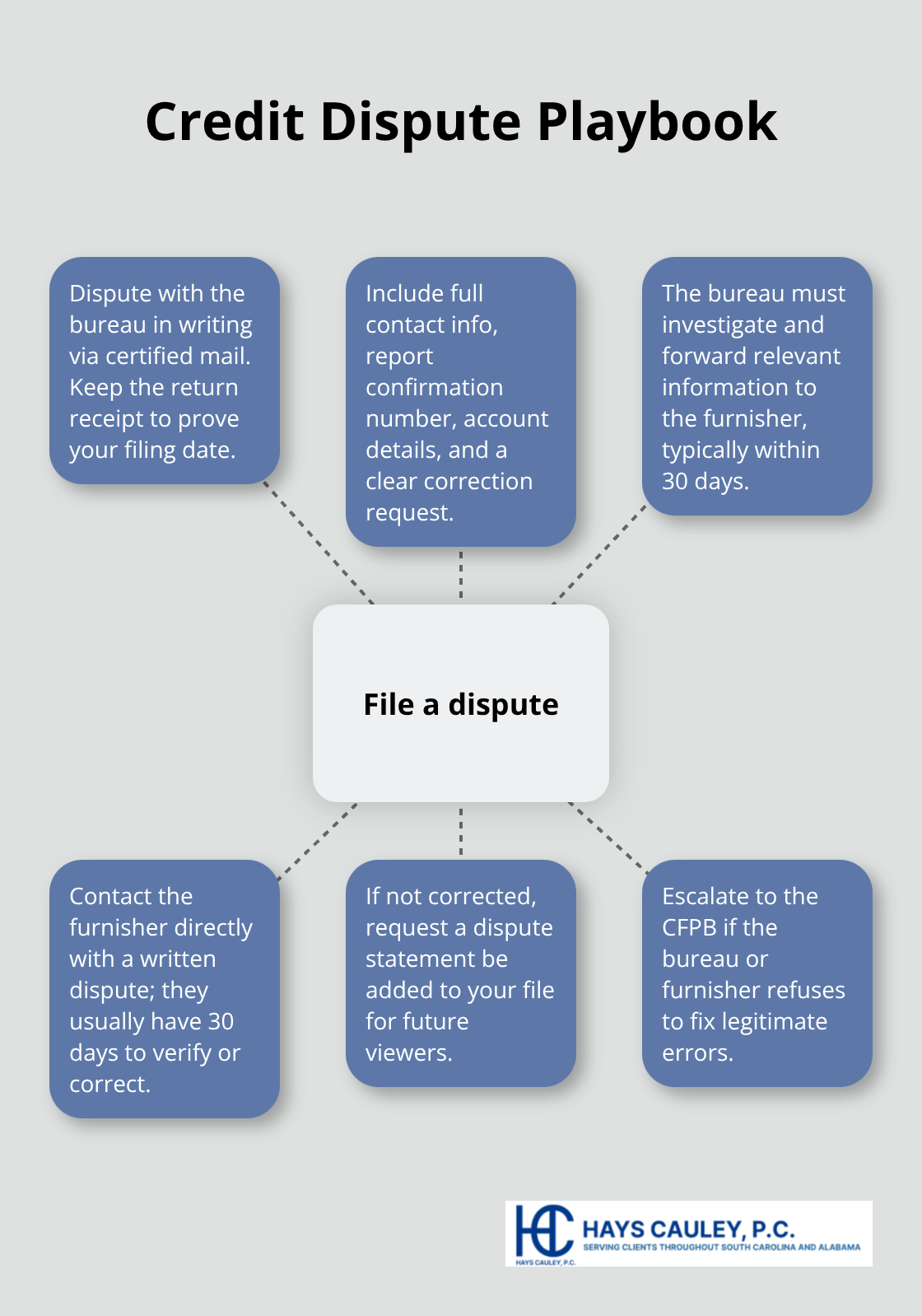

A written dispute letter to a credit bureau must clearly identify the error and explain why it’s wrong. Contact Equifax at 866-349-5191, Experian at 888-397-3742, or TransUnion at 800-916-8800 to obtain current mailing addresses, then send your dispute via certified mail with return receipt requested. This creates a verifiable record that proves you filed the dispute on a specific date.

Your letter should include your full contact information, your credit report confirmation number, each disputed item’s account number, a clear explanation of what’s wrong, and what correction or removal you’re requesting. Attach a circled or highlighted copy of the disputed portion from your report along with copies of supporting documents like bank statements or payment confirmations. The credit reporting company must investigate your dispute and forward relevant information to the furnisher within 30 days, then report the results back to you.

Contact the Furnisher Directly

Don’t assume one dispute with the bureau is enough-you must also contact the furnisher (the creditor who reported the inaccurate information) directly. Send a written letter explaining the error and requesting correction. The furnisher typically has 30 days to investigate and must update or remove information if it’s wrong or unverifiable. If the furnisher confirms the information is accurate and refuses to change it, you can request the credit bureaus add a dispute statement to your file, which appears on your report whenever future lenders or employers request it.

Understand Your Timeline and Results

The 2013 FTC study found that four in five consumers who filed disputes experienced some modification to their credit report. Slightly more than one in ten saw their credit score change after errors were corrected, with about one in 250 experiencing a change of more than 100 points. If the bureaus or furnisher dismiss your dispute as frivolous, you’ll receive notification within five business days of that decision.

Escalate to the CFPB if Needed

If problems persist after disputing with both the bureau and furnisher, file a complaint with the Consumer Financial Protection Bureau. The CFPB will forward your issue to the company, provide you a tracking number, and keep you updated on status. This escalation path exists specifically for situations where credit bureaus or furnishers refuse to correct legitimate errors, and it gives your complaint official weight within the regulatory system.

Final Thoughts

Your credit report directly impacts your financial life, and a single error can cost you thousands in higher interest rates or block you from renting an apartment. The 2013 FTC study showed that one in five consumers had errors on at least one of their three credit reports, yet four in five who actually disputed those errors saw modifications to their files. This means inaccuracies are fixable, but only if you take action to verify credit bureau data and challenge what you find.

Start by pulling your free reports from all three bureaus at annualcreditreport.com and carefully review them for mistakes like misspelled names, wrong addresses, accounts that aren’t yours, or incorrect payment statuses. Document every error you find with supporting evidence such as bank statements or payment confirmations, then file written disputes with both the credit bureaus and the furnishers who reported the inaccurate information. Send everything via certified mail so you have proof of when you filed.

Verifying your credit reports at least annually catches new errors before they damage your credit score or borrowing costs. If you’re facing persistent errors or need help navigating the dispute process, contact us at Hays Cauley, P.C. to discuss your credit reporting issues and learn how we can fight for accurate information on your behalf.