A mistake on your credit report can cost you thousands in higher interest rates and rejected loan applications. SC credit report errors are more common than you’d think, affecting your ability to buy a home, refinance debt, or even get approved for a credit card.

The good news is that you have legal rights to challenge inaccuracies. We at Hays Cauley, P.C. help South Carolina residents identify and fix these errors so your credit report reflects the truth about your financial history.

What Credit Report Errors Actually Look Like in South Carolina

Personal Information Errors Create Mixed-File Problems

Personal information errors are far more dangerous than most people realize. When your name is misspelled, your address is wrong, or your Social Security number is transposed, creditors may attach accounts to your file that don’t belong to you. South Carolina ranks 13th in the nation for identity theft per 100,000 residents, which means these errors happen frequently here. A single mismatched digit can trigger a mixed-file error, where your credit history gets tangled with someone else’s entirely. The Federal Trade Commission reports that roughly one in five credit reports contains inaccuracies, and personal data mistakes are often the culprit.

If you spot a wrong address on your report, that’s a red flag-it may signal that someone opened an account in your name. Check every letter of your name, verify your current and previous addresses, and confirm your Social Security number matches your official documents. These steps take minutes but prevent years of credit damage.

Incorrect Payment History Destroys Your Score

Incorrect account details and payment histories are the most damaging errors you’ll encounter. A single missed payment can stay on your credit report for seven years and raise your borrowing costs significantly. South Carolina consumers face this problem regularly-roughly one in five has incorrect payment histories on their reports.

A late mark that never happened, an account showing as unpaid when you paid it, or a wrong credit limit can tank your score and cost you thousands in higher mortgage rates. An account marked 30 days late when it was actually current, combined with a duplicate debt listing inflating your balance, can drop your score by 50 points or more. A 50-point score drop can increase mortgage interest rates by roughly 0.5%, costing tens of thousands over a 30-year loan.

When you review your credit report, pull your actual bank statements and canceled checks to prove you paid on time. Then dispute with both the credit bureau and the furnisher simultaneously via certified mail. This dual approach forces both parties to investigate and coordinate corrections.

Fraudulent Accounts Signal Identity Theft

Fraudulent accounts and unauthorized inquiries signal that someone may be using your identity. An unfamiliar account on your report is the most damaging error type and can stay for seven years if not corrected. The FTC reported over 175,000 credit-reporting complaints in 2020 related to unfamiliar accounts alone.

In 2024, South Carolina experienced over 15,000 identity theft cases, with financial identity theft making up 68 percent and an average loss of about $9,800 per incident. Hard inquiries from creditors you never contacted are another warning sign-too many can lower your score by five points or more. Unexpected collection accounts, accounts you never opened, or inquiries from unfamiliar lenders demand immediate action.

The number 0% seems to be not appropriate for this chart. Please use a different chart type.

If you see these errors, file a police report and contact the South Carolina Department of Consumer Affairs Identity Theft Unit at 800-922-1594. Place a fraud alert with the three major bureaus within 24 hours. A fraud alert lasts one year and forces lenders to verify your identity before opening new accounts. For stronger protection, place a credit freeze with Equifax, Experian, and TransUnion-freezes are free in South Carolina and take effect within one business day.

Now that you understand what errors look like, the next step is pulling your actual credit reports and learning how to read them for these red flags.

Pulling Your Credit Reports and Reading Them for Errors

You need to see what’s actually on your credit file before you can fix anything. The Federal Trade Commission estimates that inaccuracies appear on roughly one in five credit reports, so the odds are decent that you have at least one error waiting to be found. Start at AnnualCreditReport.com, the official source managed by the FTC. This site lets you pull free reports from all three major bureaus-Equifax, Experian, and TransUnion-without entering a credit card. South Carolina residents get an extra advantage: you can request six additional free Equifax reports per year through 2026, giving you more frequent snapshots to catch new fraud early.

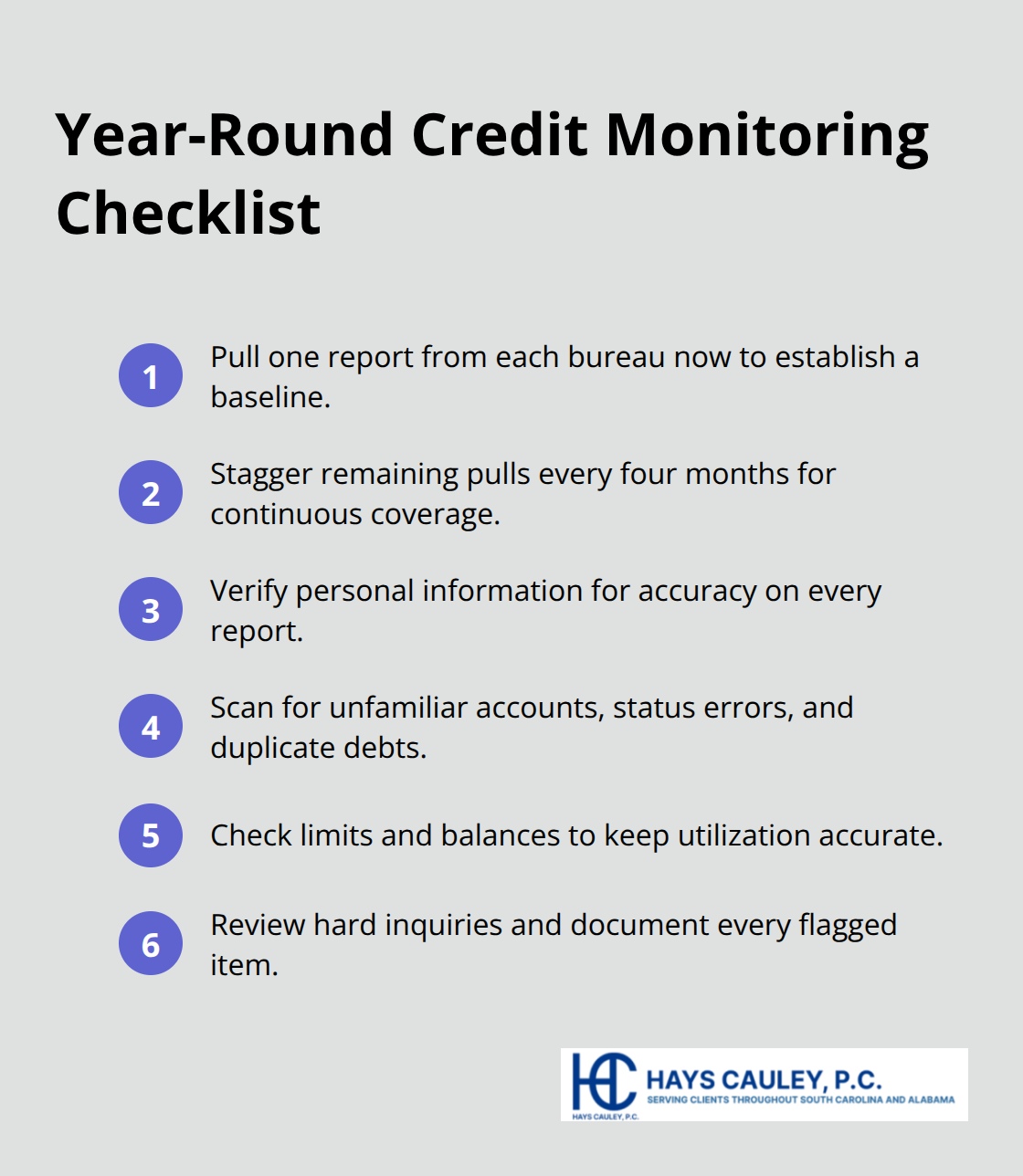

Create a Monitoring Schedule That Works

Pull one report from each bureau now, then stagger the remaining requests every four months so you monitor continuously throughout the year. This rotating approach catches errors faster than waiting until your next annual pull. You’ll spot fraudulent accounts before they damage your score and catch reporting mistakes before they compound into bigger problems.

Start With Personal Information at the Top

Check that your name is spelled correctly, your Social Security number matches your official documents, and your addresses are accurate. A single transposed digit or old address you haven’t lived at in years can signal a mixed-file error where someone else’s debt got attached to your account. These details take seconds to verify but prevent years of credit damage.

Scan Accounts for Unfamiliar Creditors and Red Flags

Scan the accounts section for unfamiliar creditors, unknown credit cards, or collection agencies you never dealt with. These are your red flags for fraud or reporting errors. For each account you recognize, verify the account status matches reality-an account showing as active when you closed it years ago is a problem. Check payment history dates against your own records; if the bureau shows a 30-day late mark in March but you have a bank statement proving you paid on time, that’s a documented error worth disputing.

Look at credit limits and balances too. A balance listed as higher than what you owe inflates your credit utilization ratio and tanks your score unnecessarily. A credit limit listed as lower than it actually is won’t hurt your score much, but accuracy still matters for your overall file.

Review Inquiries and Document Everything

Finally, review the inquiries section at the bottom. Hard inquiries from lenders you never contacted can signal identity theft or a furnisher pulling your file without permission. Too many hard inquiries in a short period will lower your score by a few points, so flag anything suspicious.

Create a simple spreadsheet as you review, noting the account number, the specific error, why it’s wrong based on your records, and which bureau reported it. This document becomes your roadmap for the disputes you’ll file next. Once you’ve identified the errors on your report, you’re ready to take action and challenge them directly with the credit bureaus and furnishers.

Challenge Credit Bureau Errors in Writing

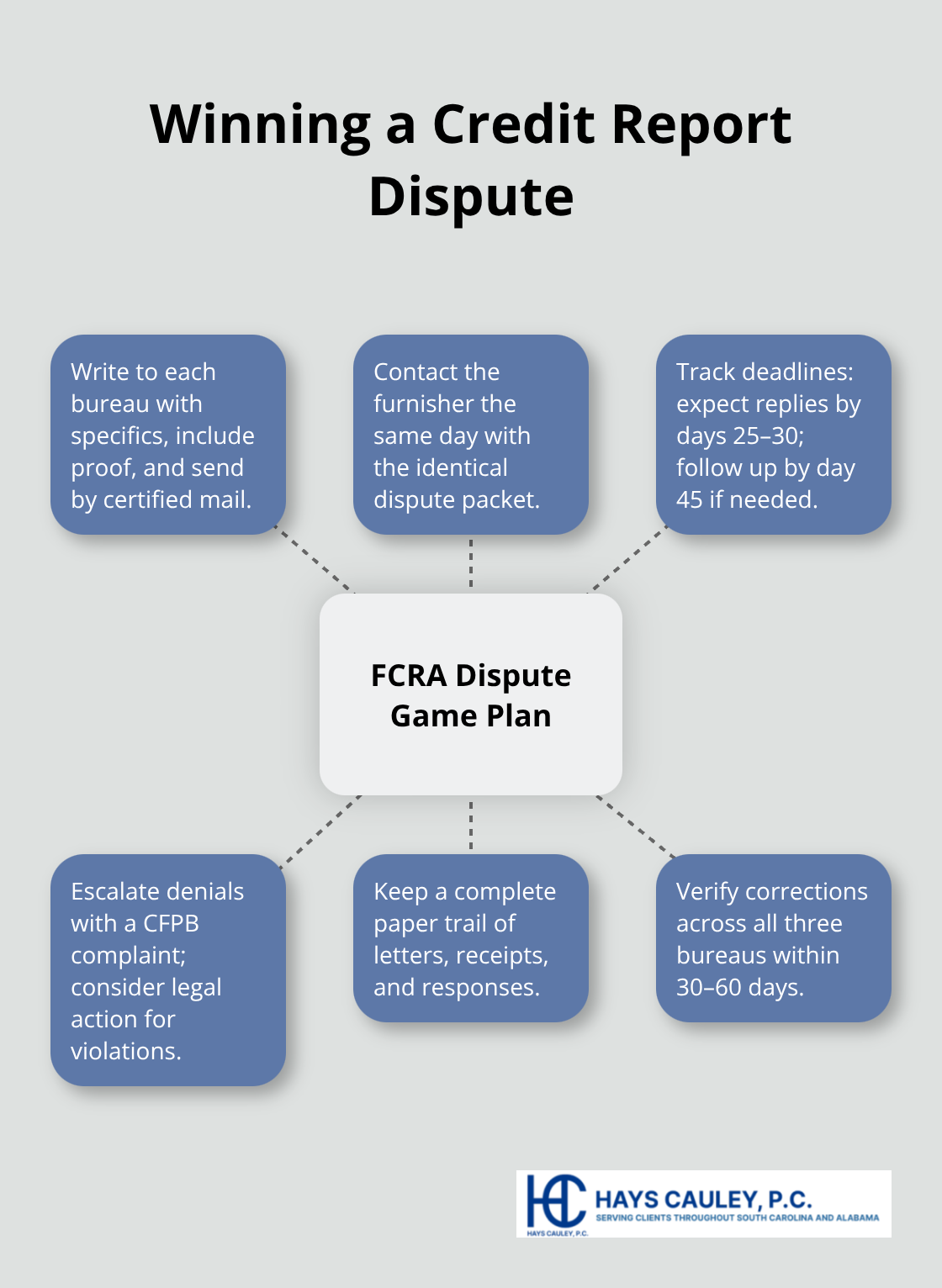

Send Your Dispute Letter to the Right Place

File your dispute with the credit bureaus in writing, not through an online form or phone call. The Fair Credit Reporting Act requires bureaus to investigate within 30 days, but only if you provide specific information. Include the account number, the exact error you’re disputing, why it’s wrong based on your documentation, and attach copies of your supporting evidence like bank statements or payment receipts. Never send originals; always send copies via certified mail with return receipt requested so you have proof the bureau received your dispute. Address your letter to the disputes department at each bureau, not a general mailing address, and reference your certified mail tracking number in the letter itself.

Contact the Furnisher on the Same Day

On the same day you mail the bureau, send an identical dispute letter to the furnisher-the creditor or data provider who reported the error to the bureau in the first place. This dual approach forces both parties to investigate and coordinate corrections. You can dispute with the furnisher directly in writing, preferably by certified mail, using the same documentation you sent to the bureau. Most disputes that include solid documentation get resolved within the 30-day window. The CFPB reports that about 70 percent of disputes lead to some modification on the credit report, which means persistence and proper documentation actually work.

Track Your Dispute Progress by Calendar

Expect responses by day 25 to 30; if you hear nothing by day 45, follow up with the bureau using your certified mail receipts as proof you already filed. Keep every piece of correspondence in a folder, including your original dispute letters, the certified mail receipts, and any responses from the bureaus or furnishers. Create a simple tracking system (a spreadsheet or document) that notes the date you mailed each dispute, the tracking number, and the expected response date for each bureau and furnisher.

Handle Denials and Escalate When Necessary

If the bureau denies your dispute, request a dispute statement to be included in your file and on all future reports you pull. You can then escalate to the Consumer Financial Protection Bureau with a formal complaint, which typically gets agency responses within 15 business days. If you believe the bureau willfully violated the Fair Credit Reporting Act, you may have grounds for legal action. Willful violations can result in damages up to $3,000 per incident plus attorney fees, and negligent violations carry at least $1,000 per incident. If disputes stall or you face escalated disputes and identity theft issues in South Carolina, Hays Cauley, P.C. serves Greenville, Columbia, and Charleston and can guide you through the process.

Verify Corrections Across All Three Bureaus

After any correction is made, pull fresh reports from all three bureaus within 30 to 60 days to confirm the changes stuck and weren’t just removed from one bureau while remaining on the others. Corrections sent to lenders that pulled your report take time to propagate, and your score can improve over time, but the timeline varies and can take several months.

Final Thoughts

A single error on your credit report can cost you tens of thousands in higher mortgage rates and rejected loan applications. When you correct inaccurate payment histories, remove fraudulent accounts, and fix personal information mistakes, your credit score improves and lenders see you as a lower-risk borrower. That translates directly into better loan terms, lower interest rates, and real money saved over time.

The process works-the CFPB reports that about 70 percent of disputes lead to some modification on your credit report. You have legal rights under the Fair Credit Reporting Act, and credit bureaus must investigate your disputes within 30 days at no cost. When you follow the steps outlined in this guide (pulling your free reports, documenting errors, filing written disputes via certified mail, and tracking responses), you use the same approach that works for thousands of consumers every year.

Sometimes disputes stall, furnishers ignore your letters, or bureaus deny your claims despite solid documentation. If SC credit report errors persist or you face identity theft complications, contact Hays Cauley, P.C. to discuss your options-we serve Greenville, Columbia, and Charleston.