Your credit report affects everything from loan approvals to job opportunities. Yet many South Carolina residents don’t know what protections the law gives them.

The Fair Credit Reporting Act (FCRA) is a federal law that shields you from inaccurate reporting and unauthorized access to your credit information. At Hays Cauley, P.C., we help residents understand and enforce these rights when they’re violated.

What the FCRA Actually Protects

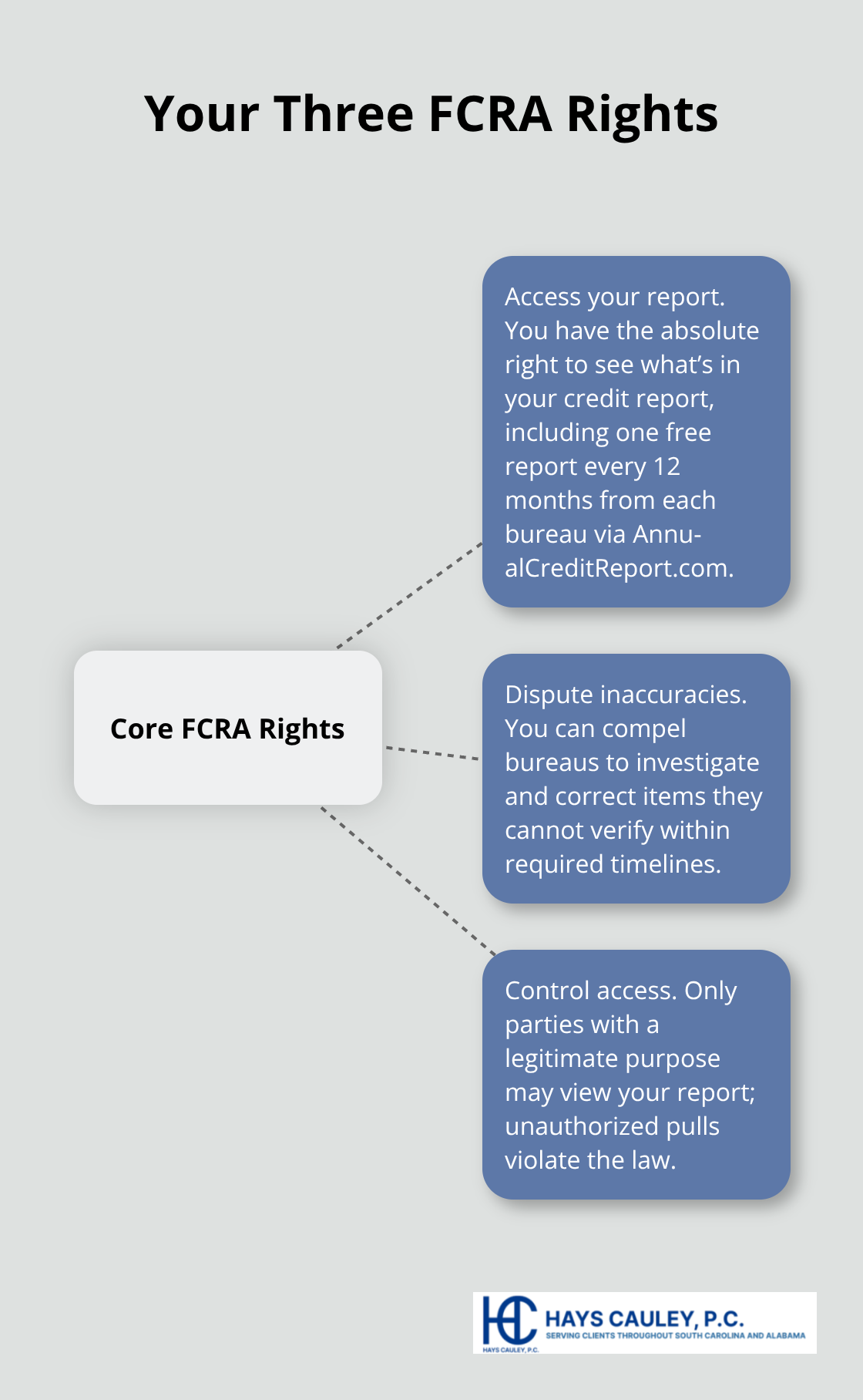

Three Core Rights You Control

The FCRA gives you three concrete powers over your credit information, and most South Carolina residents never use them. First, you have the absolute right to see what’s in your credit report. The three major bureaus-Equifax, Experian, and TransUnion-must give you one free report every 12 months through AnnualCreditReport.com. Space them out across the year rather than checking all three at once to catch errors earlier. When you pull your report, look for accounts you didn’t open, wrong payment histories, incorrect balances, and duplicate entries. These errors directly tank your credit score and cost you money on loans and insurance.

Second, you can force the bureaus to fix verified inaccurate information. If you find an error, send a written dispute letter to the bureau identifying the problem with supporting documents like payment statements or identity verification. The bureau must investigate within 30 days and correct anything they cannot verify. This isn’t optional for them-it’s the law. Third, you control who sees your report. Only people with a legitimate reason can access it. If someone pulls your report without permission for a loan decision or employment screening, that’s a violation.

What Happens When Violations Occur

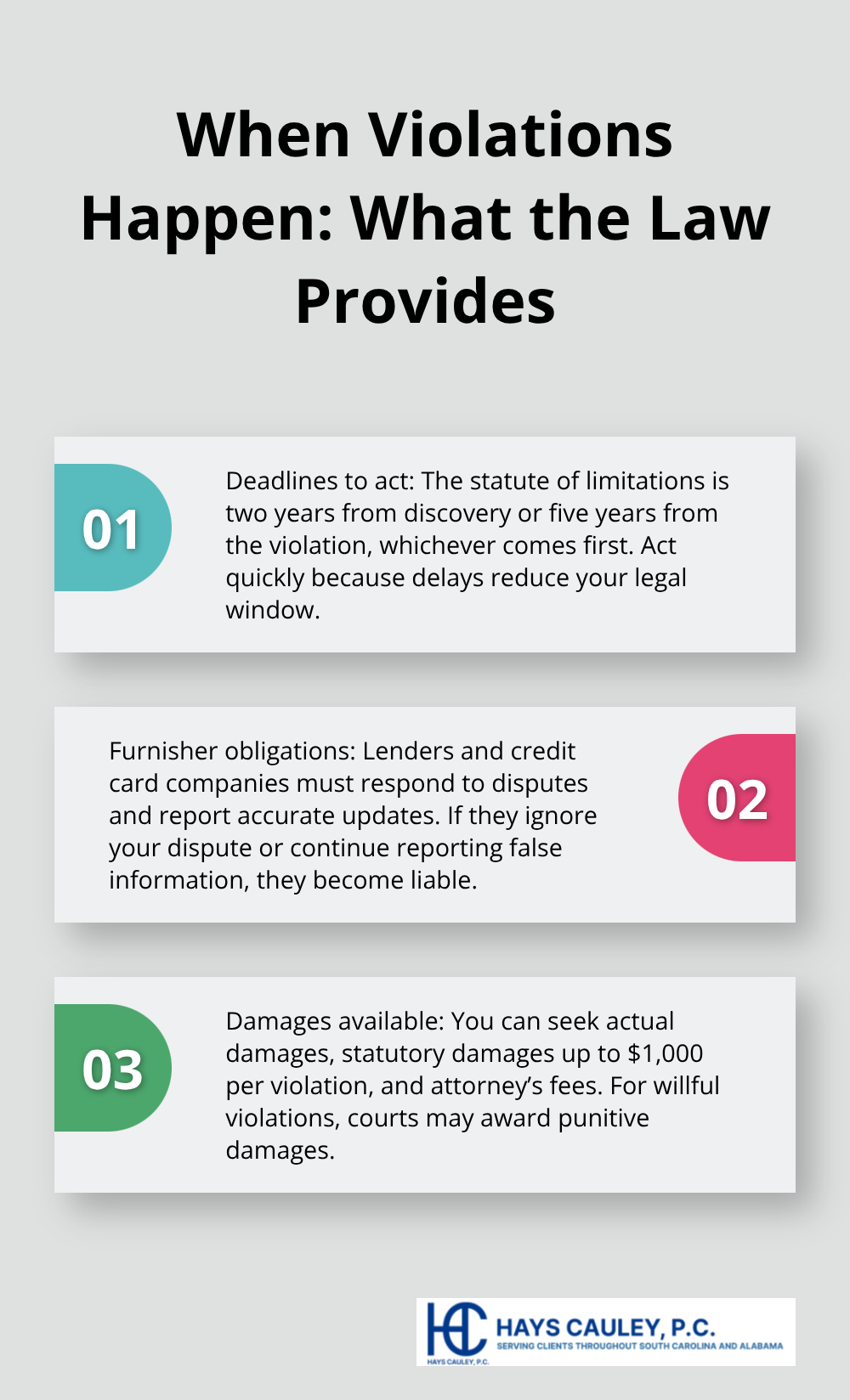

The teeth in the FCRA matter most when violations happen. If a bureau ignores your dispute or a lender reports false information about you, you can sue. South Carolina law allows you to recover actual damages, statutory damages up to $1,000 per violation, and attorney’s fees. For willful violations, you can claim punitive damages. If a bureau fails to remove inaccurate information after you win a judgment, damages can reach $1,000 per day until they correct it.

The statute of limitations gives you two years from discovery or five years from the violation, whichever comes first. This means acting quickly matters-delays eat into your legal window. The FCRA also requires furnishers like lenders and credit card companies to respond to disputes and report accurate updates. When they ignore your dispute or continue reporting false information, they become liable too.

Taking Action Against Violations

Violations of your FCRA rights don’t correct themselves. You must take action to hold bureaus and furnishers accountable. Many South Carolina residents face situations where credit bureaus refuse to investigate disputes properly or furnishers continue reporting inaccurate information despite clear evidence of errors. These violations carry real financial consequences-higher interest rates, loan denials, and damaged credit scores that take years to rebuild. Understanding your right to sue for violations transforms the FCRA from a passive protection into an active tool you can wield.

How to Get Your Free Credit Report and Spot Errors

Access Your Reports Through the Official Government Source

Start with AnnualCreditReport.com, the only official source for your free credit reports from Equifax, Experian, and TransUnion. South Carolina residents often waste time searching Google for free reports and land on scam sites that charge fees or steal personal information. The FTC runs AnnualCreditReport.com directly, so you access a government resource, not a third party. Request one report every four months rather than all three at once. This spacing strategy catches errors faster because you see fresh data from different bureaus across the year instead of a snapshot from one moment. When you pull each report, print it immediately and review it offline.

Identify the Four Most Common Credit Report Errors

Credit bureaus process hundreds of millions of transactions daily, which means errors slip through constantly. Look for accounts you never opened, payment histories that don’t match your records, incorrect balances, and duplicate entries where the same debt appears twice. These mistakes directly lower your credit score and cost you real money through higher interest rates on mortgages and auto loans.

Take your time reviewing each section of your report. Many South Carolina residents rush through this step and miss errors that damage their creditworthiness for years.

Send a Certified Dispute Letter to the Bureau

Once you identify an error, write a dispute letter to the specific bureau and send it certified mail with return receipt. Include your name, address, account number if applicable, and a clear description of what’s wrong with supporting documents like bank statements or payment confirmations. The bureau must investigate within 30 days and notify you of the results. If they cannot verify the information, they must delete it. Many South Carolina residents make the mistake of disputing online through the bureau’s website instead of sending certified mail, which creates no legal record if the bureau ignores the request.

Hold Furnishers Accountable for False Reporting

Furnishers like lenders and credit card companies must also respond to disputes and report accurate information going forward. If a bureau fails to investigate properly or a furnisher continues reporting false information after your dispute, that violation opens the door to legal action. The timeline matters because the FCRA gives you only two years from discovery to file suit, so document everything and act within weeks, not months. When furnishers ignore your dispute or continue reporting inaccurate data despite clear evidence of errors, they become liable for violations that carry real financial consequences.

Common FCRA Violations and Your Remedies

Unauthorized Access to Your Credit Report

Unauthorized access to your credit report happens more often than most South Carolina residents realize. Lenders, employers, and third parties pull reports without legitimate reasons every day, and many people never know it happened. The FCRA requires anyone accessing your report to have a permissible purpose-a legitimate business reason tied to credit, employment, insurance, or tenant screening. When someone pulls your report for marketing purposes, curiosity, or without your knowledge, that violates federal law. You won’t see unauthorized pulls on your report because they don’t appear there, but you can catch them by monitoring who accessed your file. If you notice inquiries you didn’t authorize, send a written dispute to the bureau immediately and request removal of the unauthorized inquiry. Document the date you discovered it and the inquiry that shouldn’t be there. The two-year statute of limitations starts from the moment you discover the violation, so act fast.

Failure to Correct Disputed Information

Failure to correct disputed information after you submit evidence represents the most common FCRA violation South Carolina residents encounter. You send a certified dispute letter with supporting documents, the bureau investigates, and then reports back that the information is verified and remains on your report-even when the information is clearly inaccurate. When a bureau cannot verify information during investigation, the FCRA requires them to delete it within 30 days. If they verify false information and leave it on your report, or if they fail to investigate your dispute properly, you have grounds to sue. Furnishers like credit card companies and lenders also violate the FCRA when they continue reporting inaccurate information after receiving notice of your dispute.

Your Right to Sue for Violations

Many South Carolina residents give up after one failed dispute, but the FCRA gives you the right to pursue legal action when bureaus and furnishers ignore their obligations. You can recover actual damages, statutory damages up to $1,000 per violation, and attorney’s fees. For willful violations, courts award punitive damages. If a bureau fails to remove inaccurate information after judgment, damages can accumulate at $1,000 per day until correction occurs. The financial stakes justify pursuing violations through litigation rather than accepting inaccurate reporting as permanent. We at Hays Cauley, P.C. help South Carolina residents enforce these rights when bureaus and furnishers refuse to comply with the law.

Final Thoughts

Your FCRA rights guide starts with three fundamental protections: the right to see your credit report, the right to dispute inaccurate information, and the right to control who accesses your data. These aren’t theoretical protections-they’re enforceable federal rights that South Carolina residents can use to fix errors and hold bureaus and furnishers accountable. The FCRA gives you concrete tools to challenge inaccurate reporting that damages your creditworthiness and costs you money through higher interest rates and loan denials.

If your rights are violated, act immediately by requesting your free credit reports from Equifax, Experian, and TransUnion through AnnualCreditReport.com and reviewing them carefully for unauthorized accounts, incorrect payment histories, wrong balances, and duplicate entries. Send certified dispute letters to any bureau reporting inaccurate information and document everything you submit. If a bureau fails to investigate properly or a furnisher continues reporting false data after your dispute, you have grounds to sue for actual damages, statutory damages up to $1,000 per violation, and attorney’s fees-the two-year statute of limitations from discovery means delays cost you.

Many South Carolina residents face situations where credit bureaus refuse to correct verified errors or furnishers ignore disputes entirely, and these violations carry real consequences that extend far beyond your credit score. We at Hays Cauley, P.C. help consumers with credit reporting issues by enforcing FCRA rights when bureaus and furnishers refuse to comply with the law. If you’ve disputed errors without success or discovered unauthorized access to your report, contact us to discuss your options and protect your financial future.