A mistake on your credit report can tank your score for years, even if the error isn’t your fault. At Hays Cauley, P.C., we’ve helped South Carolina residents fight back against inaccurate information that damages their financial standing.

SC credit score repair starts with understanding what went wrong and taking action to fix it. This guide walks you through disputing errors, rebuilding your rating, and getting your finances back on track.

What Errors Actually Appear on Credit Reports and How They Hurt You

Common Types of Errors on Credit Reports

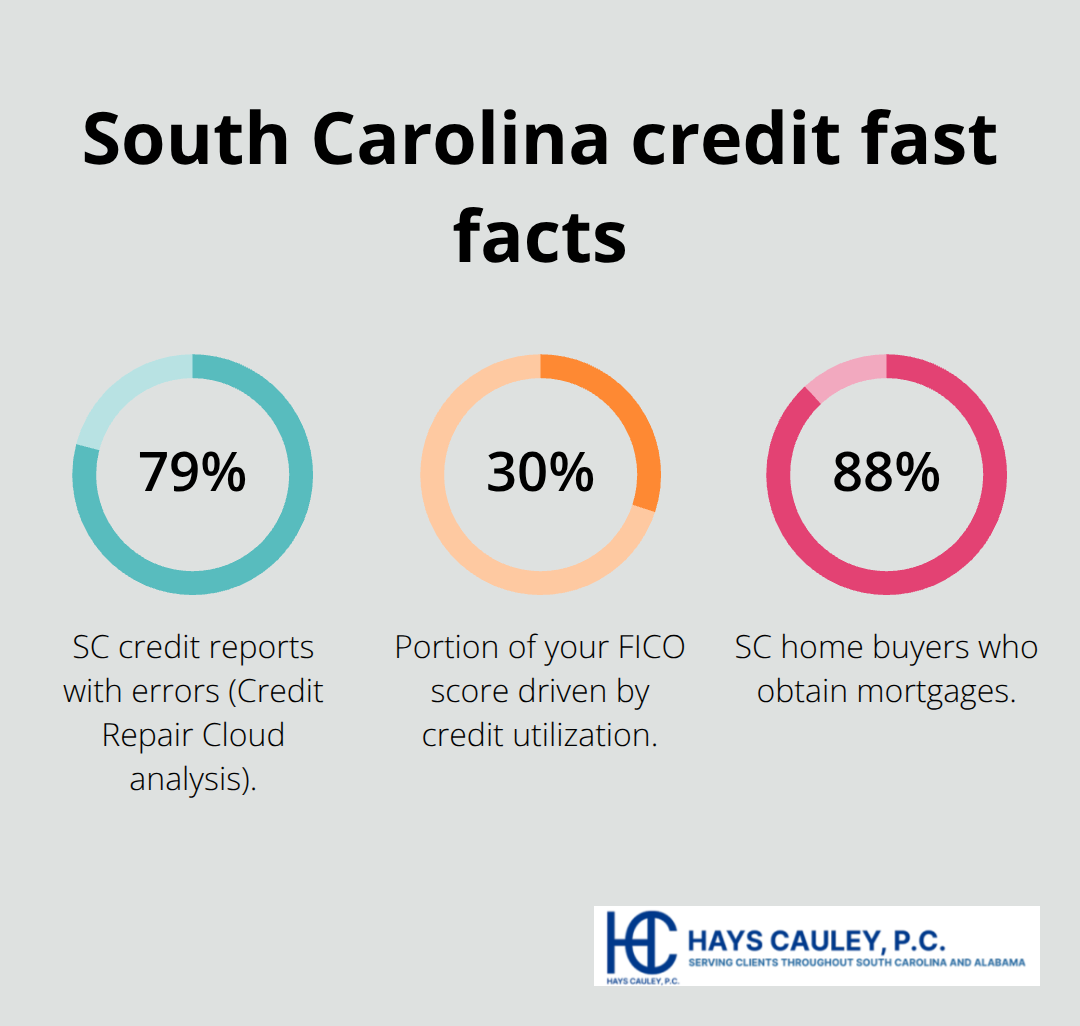

Credit report errors fall into distinct categories, and each one damages your score differently. According to Credit Repair Cloud’s analysis of South Carolina data, 79% of SC credit reports contain errors-a staggering number that shows how widespread this problem is. The most common mistakes include late payments that weren’t actually late, accounts listed twice, accounts belonging to someone else entirely, incorrect balances or credit limits, and closed accounts still appearing as open.

Accounts with wrong balances hit hardest because lenders see inflated debt levels when they check your report, making you appear riskier than you actually are. A single inaccuracy can drop your score by 50 to 100 points depending on the error type and your overall credit profile. If a creditor reports a missed payment that you made on time, that false late mark stays visible and damages your creditworthiness for years, affecting whether you qualify for mortgages, car loans, credit cards, or even apartment rentals.

How Inaccurate Information Damages Your Financial Standing

SC law specifically recognizes that consumer reporting agencies maintain files containing payment history, defaults, judgments, liens, and collections that directly influence lending decisions. The average debt on an SC credit report sits around $5,700, and when errors inflate that number, you lose negotiating power and access to better interest rates. Approximately 44.3% of SC residents have credit scores below 700, meaning most of these individuals have room to improve-but only if errors get fixed first.

The Timeline for Error Removal and Your Rights

Negative information generally stays on your credit report for seven years, while bankruptcy information remains for ten years-but inaccurate information doesn’t deserve that lifespan at all. Under the Fair Credit Reporting Act, when you dispute with Equifax, Experian, or TransUnion, the bureau must reinvestigate within 30 days and provide written results at no cost. If the investigation confirms an error, the agency must correct it in its records and notify lenders who received your report in the last six months.

South Carolina law goes further: if inaccurate information harms your creditworthiness and isn’t corrected within 10 days after a judgment, you can accumulate damages up to $1,000 per day until the error is removed. Speed matters here-the sooner you dispute an error, the sooner it stops dragging down your rating and the sooner you can rebuild. Understanding these timelines and your rights under state and federal law positions you to take action immediately rather than wait for errors to age off your report on their own.

How to Get Your Credit Report and File Disputes

Obtain Your Credit Reports from All Three Bureaus

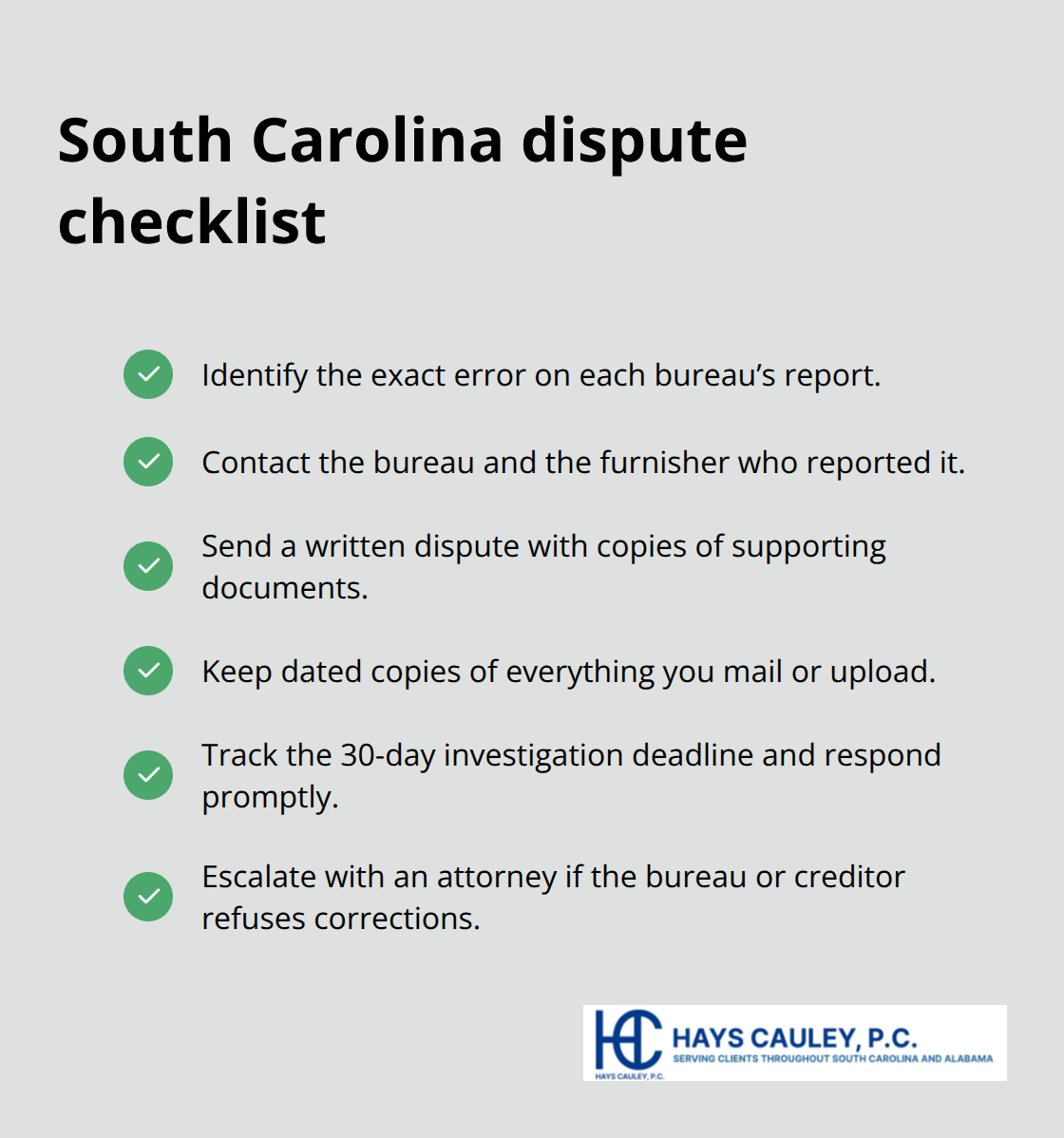

Your first move costs nothing. Visit AnnualCreditReport.com and request reports from Equifax, Experian, and TransUnion at the same time, or space your requests throughout the year to monitor accuracy across all three. Through 2026, you can pull six free credit reports annually from Equifax by calling 1-866-349-5191, which gives you multiple opportunities to catch errors early. Each bureau maintains different information, so checking all three ensures you see the complete picture of what lenders actually see about you. Print or save these reports immediately and review them line by line, comparing account names, balances, payment histories, and account statuses against your own records.

File Your Dispute in Writing with Documentation

Once you identify an error, contact both the credit reporting agency and the business that reported the inaccurate information. The FTC provides sample dispute letters to guide your communication, and you do not need a lawyer to file a dispute.

Send your dispute in writing to the bureau, clearly stating which item is wrong and why, then include a copy of supporting documentation like bank statements or payment receipts. The bureau must investigate within 30 days and provide written results at no cost. South Carolina law strengthens your position further: if the error harms your creditworthiness and remains uncorrected beyond 10 days after a judgment, you can accumulate damages of up to $1,000 daily until removal. This aggressive penalty structure means bureaus take SC disputes seriously, and your documentation should reflect this urgency by being thorough and dated.

Consider Legal Action When Disputes Stall

If a bureau ignores your dispute, refuses to correct a confirmed error, or you face pushback from creditors, a consumer protection attorney can send formal demand letters that carry legal weight and file litigation if necessary. Many consumers find that a single letter from legal counsel resolves disputes that months of personal effort could not. South Carolina allows you to file a civil action to enjoin and restrain future violations, and if you prevail, you can recover actual damages plus attorney fees, making legal representation financially viable rather than just an expense. Hays Cauley, P.C. specializes in consumer protection law and can help you navigate these disputes when the process becomes complicated or when creditors resist correction.

With your disputes filed and documentation submitted, the investigation period begins-and during those 30 days, you can take steps to strengthen your overall credit profile while waiting for results.

Fixing Your Credit After Errors Get Removed

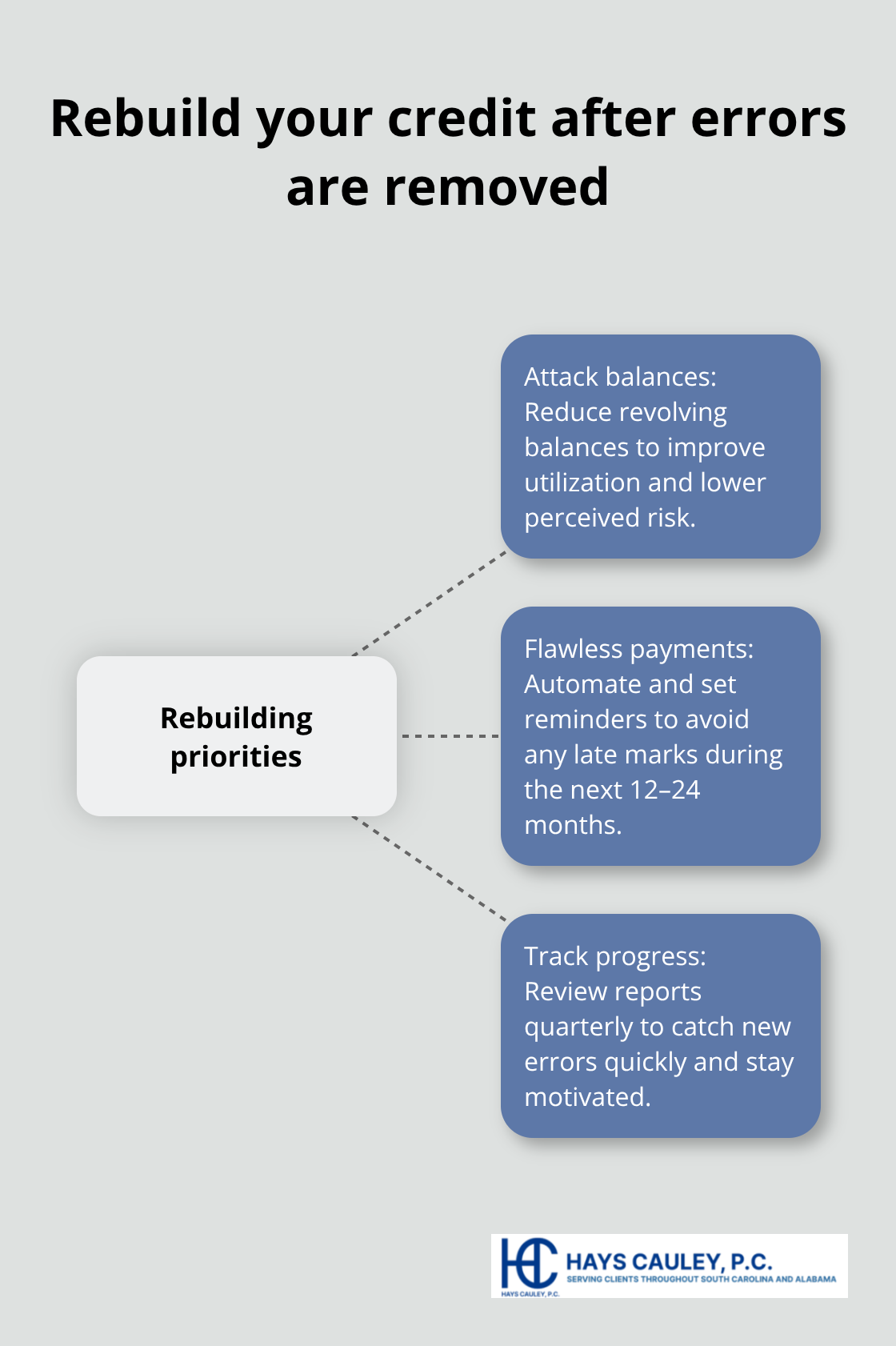

Once the credit bureaus confirm an error and remove it from your report, your score does not instantly jump back to where it should be. The removal stops the damage, but rebuilding requires deliberate action over months. South Carolina residents with errors cleared should focus on three concrete moves that produce measurable results: attacking existing debt balances, establishing a flawless payment record going forward, and tracking progress to stay motivated.

Pay Down Your Debt Strategically

The average SC resident carries around $5,700 in debt, and reducing that number directly improves your credit utilization ratio, which makes up 30% of your credit score calculation. If you have multiple accounts, prioritize paying down high-balance cards first because lenders care most about how much you owe relative to your credit limits. A card with a $5,000 limit and a $4,500 balance looks far riskier than one with a $5,000 limit and a $500 balance, even though the total debt is identical.

Start paying more than the minimum on every account, even if it’s an extra $25 per month on each card. This approach accelerates paydown and demonstrates to creditors that you’re serious about financial responsibility.

Build a Flawless Payment Record

Once you clear an error, your next 12 to 24 months matter enormously because lenders weight recent payment history more heavily than older mistakes. Set up automatic payments to ensure zero missed payments during this critical window, and consider setting payment reminders a week before due dates to catch any issues early.

About 88% of SC home buyers obtain mortgages, meaning your score directly affects whether you qualify and what interest rate you receive. Every point gained during this rebuilding phase translates to real money saved on major loans.

Monitor Your Progress Regularly

Check your credit reports every three months using your six free annual pulls through Equifax to catch any new errors immediately rather than letting them compound for months. This consistent monitoring protects your creditworthiness and alerts you to problems before they damage your score further. If debt feels overwhelming or if new errors appear on your report after removal, Hays Cauley, P.C. can help you navigate disputes and develop a strategy to protect your financial standing moving forward.

Final Thoughts

Credit report errors will not fix themselves, and waiting for negative information to age off your report wastes years you could spend rebuilding your financial standing. SC credit score repair requires action on two fronts: removing inaccurate information through disputes and then deliberately strengthening your credit profile afterward. The process works, but it demands follow-through and attention to detail across multiple steps.

Handling disputes alone is possible, but many South Carolina residents find that errors persist despite their best efforts-creditors resist corrections, bureaus drag out investigations, or new errors appear just as old ones get removed. This is where professional guidance makes a measurable difference. At Hays Cauley, P.C., we understand South Carolina’s consumer protection laws and how to apply them aggressively on your behalf, handling communication with credit bureaus and pushing back against creditor resistance when necessary.

Your financial future depends on accurate credit information and a solid payment record going forward. If disputes have stalled or you face resistance from creditors and bureaus, contact Hays Cauley, P.C. for professional guidance navigating SC credit score repair. We serve South Carolina, including Greenville, Columbia, and Charleston, and we’re ready to fight for your financial rights.