A local credit reporting attorney can be the difference between a damaged credit score and financial recovery. Inaccurate information on your credit report costs you money through higher interest rates and denied loans.

We at Hays Cauley, P.C. help South Carolina residents challenge reporting errors and reclaim their financial standing. This guide shows you what to look for in legal representation and how the right attorney fights for your rights.

Why Local Credit Reporting Attorneys Matter

Credit Reporting Errors Cost You Real Money

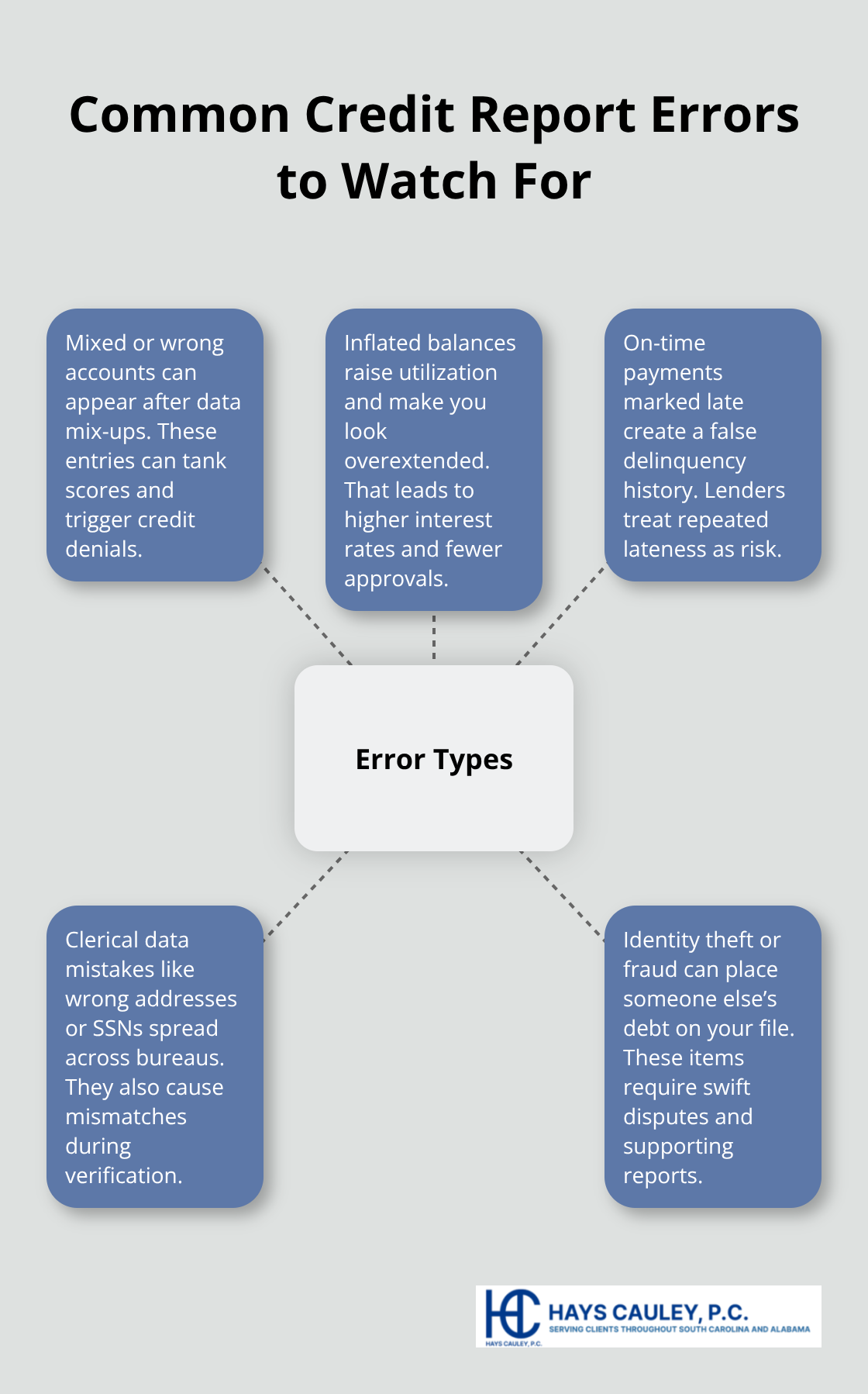

Credit reporting errors are far more common than most people realize. The Federal Trade Commission found that roughly one in five consumers identified errors on their credit reports, and one in twenty consumers discovered errors serious enough to affect credit decisions. These aren’t minor mistakes-they directly impact your wallet. An inaccurate negative item can cost you thousands in higher interest rates on mortgages, auto loans, and credit cards. A single late payment mark stays on your report for seven years, even if you’ve since paid the debt in full.

The major credit bureaus process hundreds of millions of transactions daily, and that volume creates genuine opportunities for mistakes to slip through. You might see accounts that don’t belong to you, inflated balances, or payment histories marked as delinquent when you paid on time. Some errors are simple clerical mistakes-a wrong address or Social Security number. Others are more damaging fraud where someone else’s debt appears on your report.

Why DIY Disputes Fall Short

The Fair Credit Reporting Act gives you the right to dispute these errors and have them corrected, but the bureaus often move slowly or deny legitimate disputes outright. DIY disputes typically take thirty to forty-five days for bureaus to investigate, and complex errors frequently get denied on the first attempt. You send your dispute letter, wait weeks for a response, and then receive a letter stating the bureau found no error-even though the information is clearly wrong.

This pattern repeats itself. You dispute again. The bureau investigates again. Nothing changes. That’s where a local attorney becomes invaluable. An attorney knows how to force the bureaus to actually verify their claims rather than simply rubber-stamp the information they already have on file.

Federal Law Creates Strategic Advantages

Federal credit law is genuinely complex, and most people underestimate this complexity. The Fair Credit Reporting Act imposes strict requirements on how bureaus must handle disputes, what information they must verify, and how quickly they must respond. South Carolina also has its own consumer protection laws that provide additional rights beyond the federal framework.

A local attorney familiar with South Carolina courts and judges understands how to navigate these requirements strategically. They know which procedural moves force bureaus to prove their claims, how to gather evidence that demonstrates harm to your credit score or finances, and when to file suit rather than wait for another failed dispute. The right legal representation doesn’t just correct your report-it holds the bureaus accountable and creates leverage in negotiations that you simply don’t have on your own.

This is where understanding what to look for in an attorney becomes your next critical step.

What to Look for in a Credit Reporting Lawyer

Track Record Matters Most

Start with track record. When you call a potential attorney, ask directly how many credit reporting cases they’ve handled and what percentage resulted in corrected items on credit reports. Most attorneys won’t volunteer this information, so you must ask. Look for someone who has handled at least fifty to one hundred Fair Credit Reporting Act cases. This volume matters because credit reporting litigation follows predictable patterns, and attorneys with real experience know exactly which arguments work with local judges and which ones fall flat.

Check federal court records through PACER to verify their case history yourself. Search for their name alongside FCRA to see actual lawsuits they’ve filed. Your state bar website also maintains disciplinary records that reveal whether an attorney has faced complaints or sanctions. Verify their license is in good standing before scheduling a consultation.

Beyond case numbers, ask about their success rate on disputes that the bureaus initially denied. Many consumers exhaust their own dispute attempts before hiring an attorney, which means you’re asking the lawyer to overturn a bureau’s previous decision. This is harder than winning on the first try, and only experienced attorneys consistently succeed at this level.

Federal Requirements and State Law Knowledge

Knowledge of federal requirements separates competent attorneys from those who simply file documents. The Fair Credit Reporting Act contains specific timelines and verification standards that bureaus routinely ignore, and your attorney must know how to exploit these violations strategically. Ask whether they’ve won cases where bureaus failed to properly verify disputed information or violated the thirty-day investigation deadline.

Ask about their experience with South Carolina’s consumer protection laws, which provide additional remedies beyond federal law. These state protections strengthen your position considerably, and an attorney who understands both frameworks can build a more powerful case than one who relies solely on federal claims.

Direct Communication and Fee Transparency

Availability for real communication is non-negotiable. Many attorneys advertise free consultations but then route you to a paralegal or answering service. Demand to speak with the actual attorney during your initial consultation, not just staff. Confirm they’ll handle your case personally rather than delegating it to junior associates unfamiliar with credit reporting litigation.

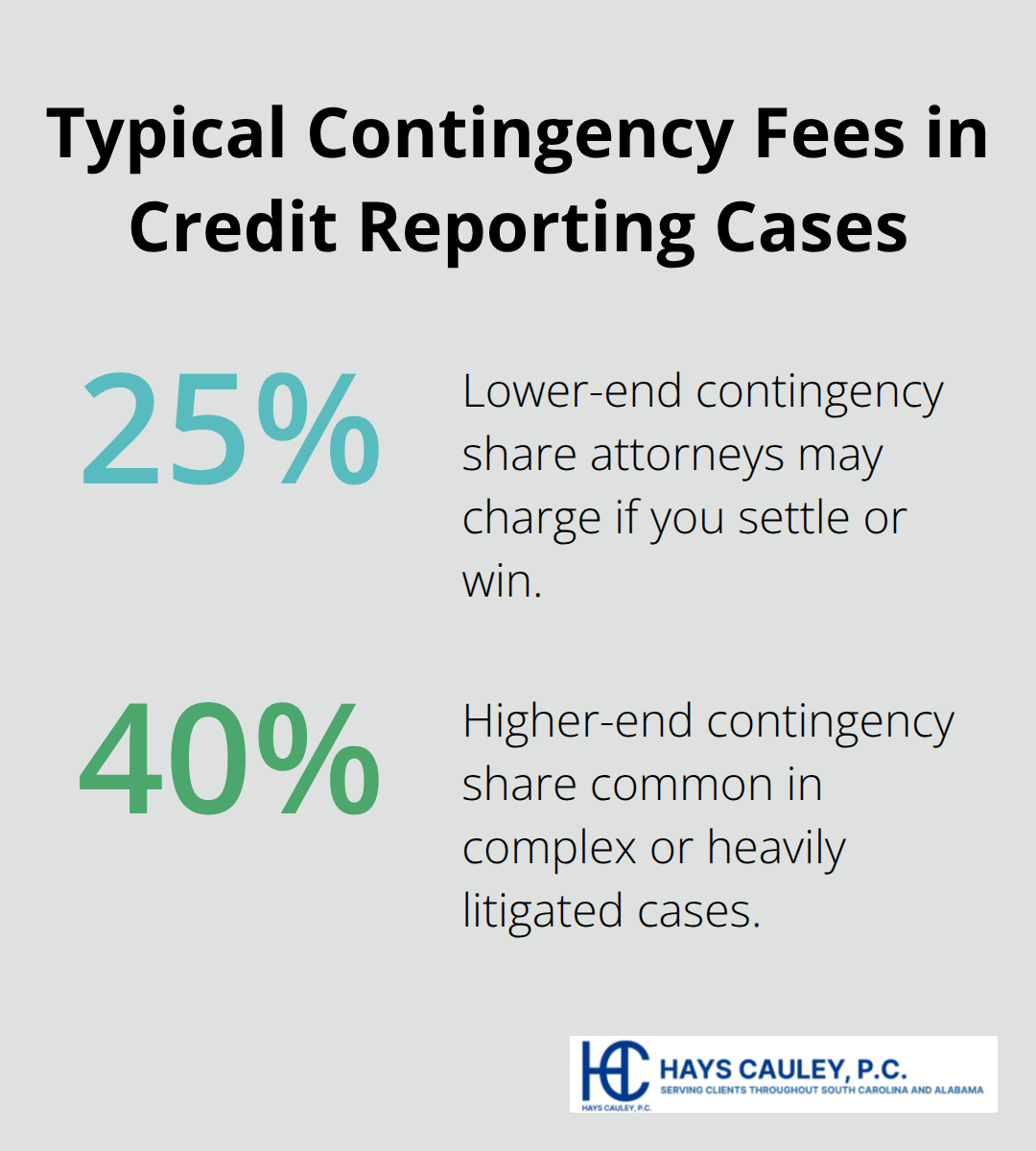

Hourly rates for credit reporting attorneys typically range from two hundred to five hundred dollars per hour, though many work on contingency where they collect twenty-five to forty percent of any settlement or judgment. Contingency arrangements are favorable for you because the attorney only gets paid if you win. Ask about their fee structure upfront and get everything in writing. This transparency prevents surprises later and helps you compare options fairly.

Finding the Right Fit for Your Situation

The attorney you select must align with your specific circumstances. If you’ve already disputed errors multiple times without success, you need someone with a proven track record of overturning bureau denials. If your credit damage extends beyond reporting errors to identity theft or debt collection violations, you need an attorney who handles those issues alongside credit reporting claims. South Carolina residents in Greenville, Columbia, and Charleston should prioritize local attorneys who understand regional court procedures and judge preferences.

Your next step involves identifying which errors actually appear on your report and understanding how those errors harm your financial position. An attorney can guide this analysis, but you must first gather your credit reports and document the specific inaccuracies you want corrected.

How an Attorney Wins Your Credit Dispute

Identifying Errors That Actually Cost You Money

An attorney’s first move is pulling your complete credit file and identifying which errors harm your financial position. Not every inaccuracy on your report justifies legal action. Your attorney focuses on errors that directly damage your finances, such as accounts reporting late payments you made on time, balances inflated above what you actually owed, or accounts that don’t belong to you entirely. The Federal Trade Commission data shows that roughly one in five consumers find errors, but only a fraction of those errors significantly impact credit scores or borrowing costs. Your attorney determines which errors are worth fighting and which ones require less aggressive correction strategies. They also identify patterns that suggest systemic violations by the bureaus, such as repeated failures to investigate disputes properly or verify information within the thirty-day legal window. This focused approach means you’re not wasting resources on minor issues while missing major ones that cost you thousands in higher interest rates.

Forcing Bureaus to Prove Their Claims

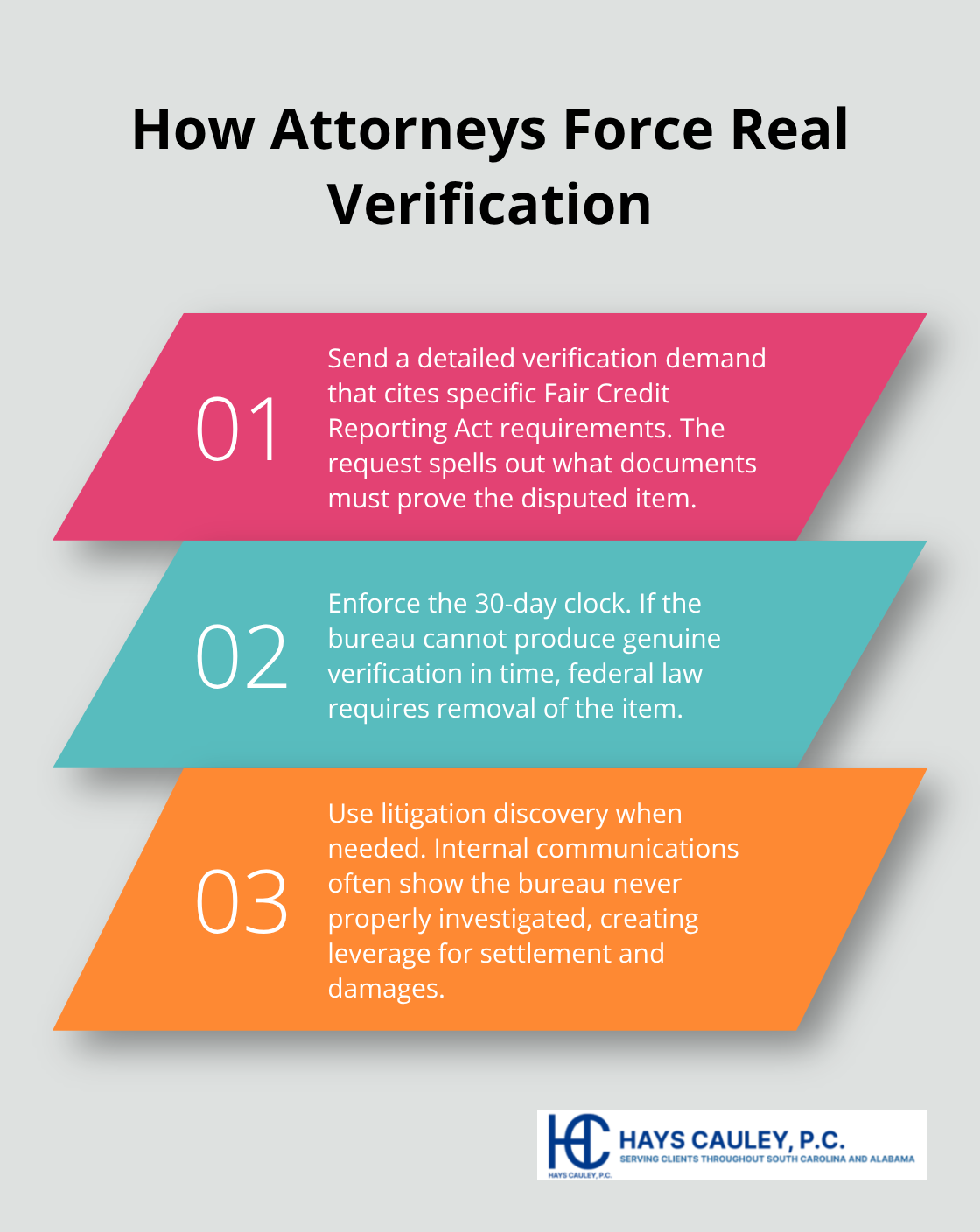

Building leverage against the bureaus requires forcing them to actually prove their claims rather than simply deny your disputes. When you dispute on your own, bureaus often respond with form letters stating they found no error without ever contacting the original creditor to verify the information. An attorney sends a detailed verification demand that cites specific Fair Credit Reporting Act requirements and explains exactly what documentation must be provided to substantiate the disputed item. If the bureau cannot produce genuine verification within thirty days, federal law requires them to remove the item from your report. Most bureaus fail this test because they lack actual documentation and rely instead on automated systems and incomplete records. Your attorney also discovers what happened behind the scenes through discovery requests if the case proceeds to litigation, revealing communications showing the bureau never bothered investigating your dispute.

Negotiating Settlements and Damages

This evidence becomes powerful leverage in settlement negotiations. When settlement discussions begin, your attorney knows the bureau’s weak points and uses that knowledge to negotiate removal of errors or damages for the harm caused to your credit score. The goal isn’t just correcting your report but also recovering compensation for denied credit, higher interest rates you paid, or emotional distress from years of inaccurate reporting. Federal law allows you to recover actual damages plus court-determined penalties when bureaus violate verification requirements or fail to investigate disputes properly. Your attorney quantifies these damages by documenting the specific financial harm you suffered (denied loans, higher interest rates on approved credit, or missed opportunities). Settlement negotiations often conclude with the bureau agreeing to remove the disputed item and pay damages rather than face litigation costs and potential judgment. This combination of corrected credit information and financial compensation protects your financial future in ways that DIY disputes simply cannot achieve.

Final Thoughts

Your credit report controls your financial opportunities, and inaccurate information costs you real money through higher interest rates and denied loans. Start by gathering your credit reports from TransUnion, Equifax, and Experian, then document every error you find with specific details about how each inaccuracy harmed your finances. This documentation becomes essential when you consult with a local credit reporting attorney because it demonstrates the scope of the problem and the financial damage you’ve suffered.

Contact a local credit reporting attorney in your area who has handled at least fifty to one hundred Fair Credit Reporting Act cases and ask about their track record with disputes that bureaus initially denied. Demand transparency about costs and direct communication with the attorney handling your case, not just staff members, and use free initial consultations to assess whether they understand your situation and can articulate a clear strategy for winning. Most attorneys work on contingency (collecting twenty-five to forty percent of any settlement), which means you pay nothing unless you win.

We at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia, and Charleston, challenge credit reporting errors and recover damages from bureaus that violate federal law. Contact Hays Cauley, P.C. at 843-665-1717 in Florence, SC for a free consultation and learn how legal representation can correct your report and hold the bureaus accountable.