Your credit reporting rights in South Carolina are protected by state and federal law, but many people don’t know what those protections actually cover.

Inaccurate information on your credit report can damage your ability to get loans, rent an apartment, or even land a job. At Hays Cauley, P.C., we help South Carolina residents understand and enforce their credit reporting rights when agencies violate the law.

What Credit Reporting Agencies Must Do Under South Carolina Law

Credit reporting agencies in South Carolina operate under strict rules, and most people have no idea what those rules require. Under South Carolina Code 37-20 and the federal Fair Credit Reporting Act, these agencies must verify information before they report it, correct errors within 30 days of your dispute, and remove inaccurate data from your file. The FTC reports that about 1 in 5 consumers have errors on their credit reports, which means the accuracy problem is widespread and serious. When you dispute information, the agency cannot simply ignore you-they must investigate your claim, contact the business that reported the information, and send you written results of their investigation within 30 days. If they find the information is inaccurate, they must correct it and notify any party that received a report containing the mistake in the past six months.

How Long Negative Information Actually Stays

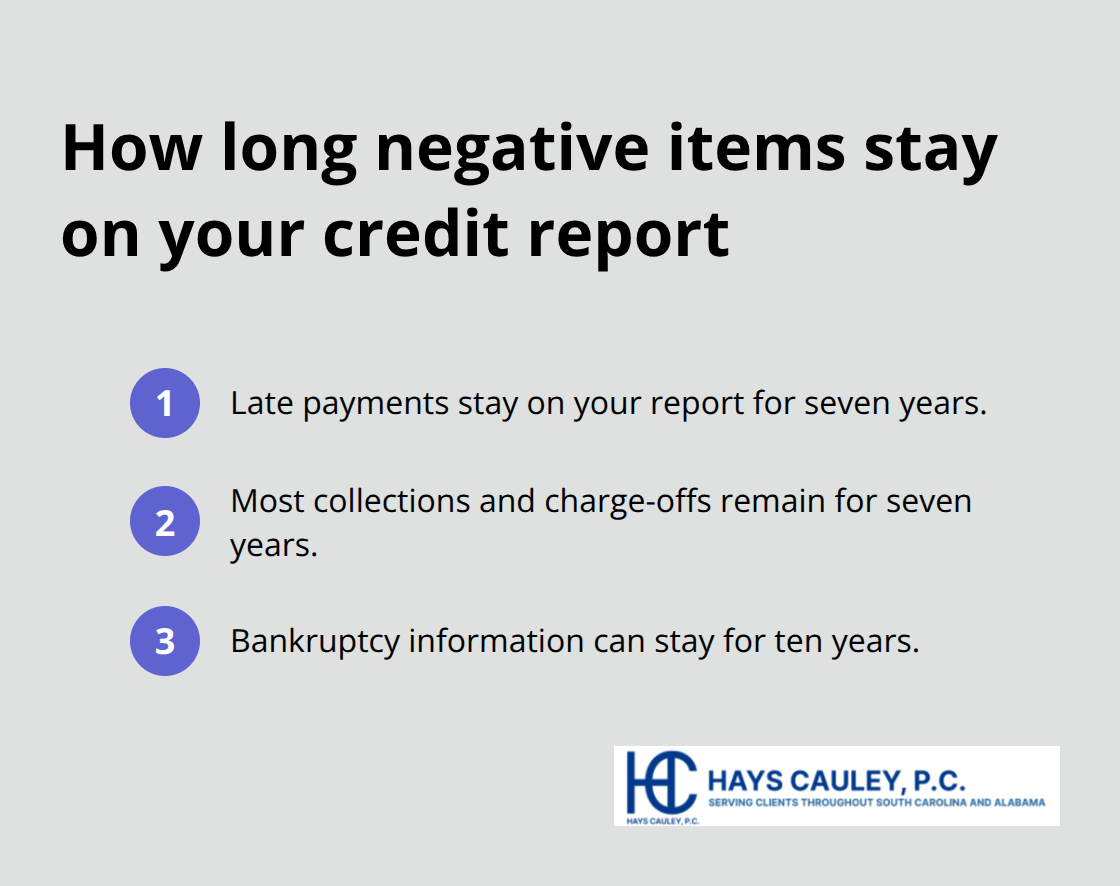

The reporting timeline matters because inaccurate information that lingers costs you money through higher interest rates or denied credit. South Carolina law aligns with federal standards: late payments stay on your report for seven years, most collections and charge-offs remain for seven years, and bankruptcy information can stay for ten years. However, this timeline only applies if the information is accurate.

If a late payment is reported as late when you actually paid on time, or if an account balance is wrong, you have the right to dispute it immediately. The three major bureaus-Equifax, Experian, and TransUnion-must respect your dispute and investigate it. If the investigation shows the information is inaccurate or the business that reported it fails to verify it within 30 days, the agency must remove it, regardless of how recent the item is.

Getting Your Free Credit Reports and Monitoring

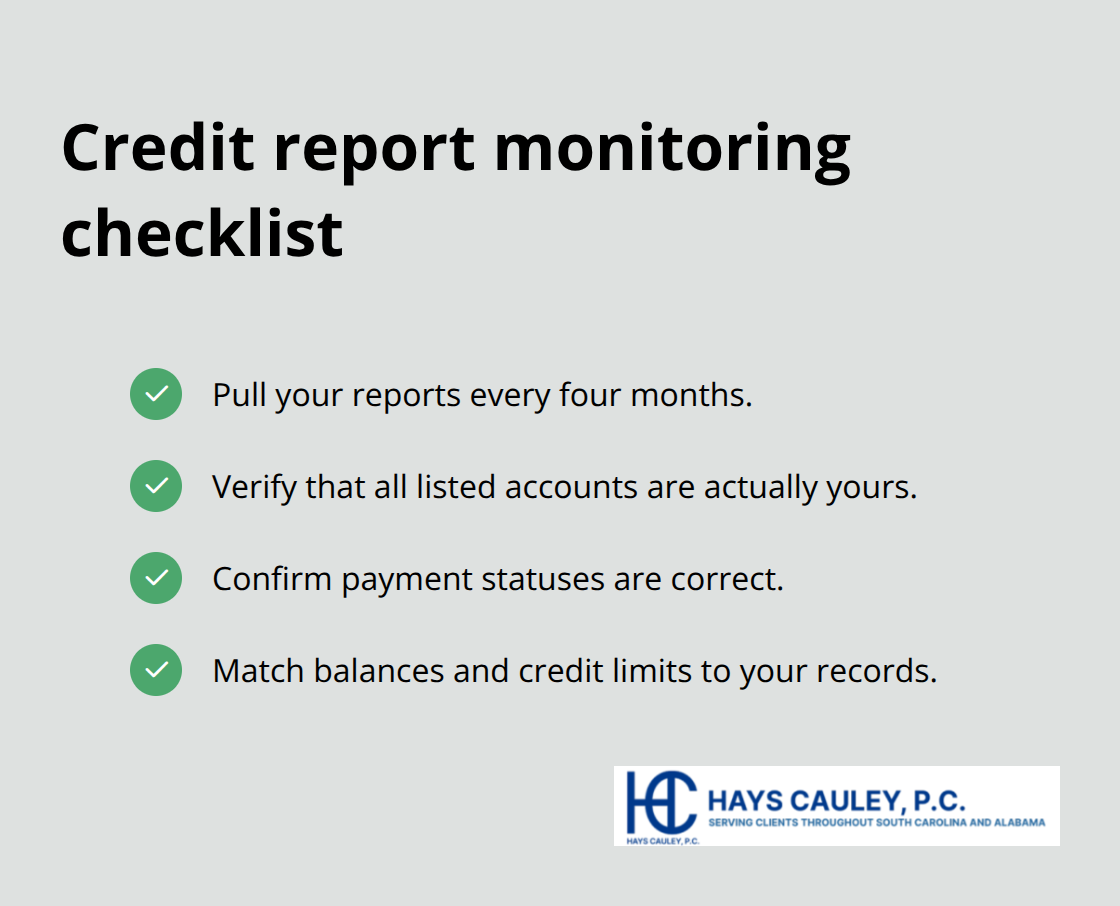

You can pull your credit reports for free once every 12 months from each of the three bureaus through AnnualCreditReport.com, and Equifax currently offers six additional free reports per year through 2026 when you call 1-866-349-5191. Many people check their reports only once or twice a year, but errors can appear at any time. Pulling your reports every four months gives you better visibility into what furnishers are reporting about you. When you review your report, check three specific areas: whether accounts listed are actually yours, whether payment statuses are correct, and whether balances and credit limits match your records.

How to Document and File Your Dispute

If you spot an error, document it with the exact account number, the specific information that is wrong, and any supporting documents like payment confirmations or account statements. Send your dispute in writing to the bureau by certified mail with return receipt, and also send the same dispute directly to the business that reported the information. This dual approach speeds resolution because the business often corrects errors faster than the bureau’s formal investigation process. The business that reported the information must investigate independently and report back to the bureau within 30 days (sometimes up to 45 days). Once the business confirms an error, it notifies all three bureaus so they can correct your file. You should receive written results and a free copy of your updated report if changes occur. The entire process typically takes 30 to 45 days from the time you mail your dispute, though some corrections happen faster when the furnisher acts quickly.

What Happens When Agencies Violate These Rules

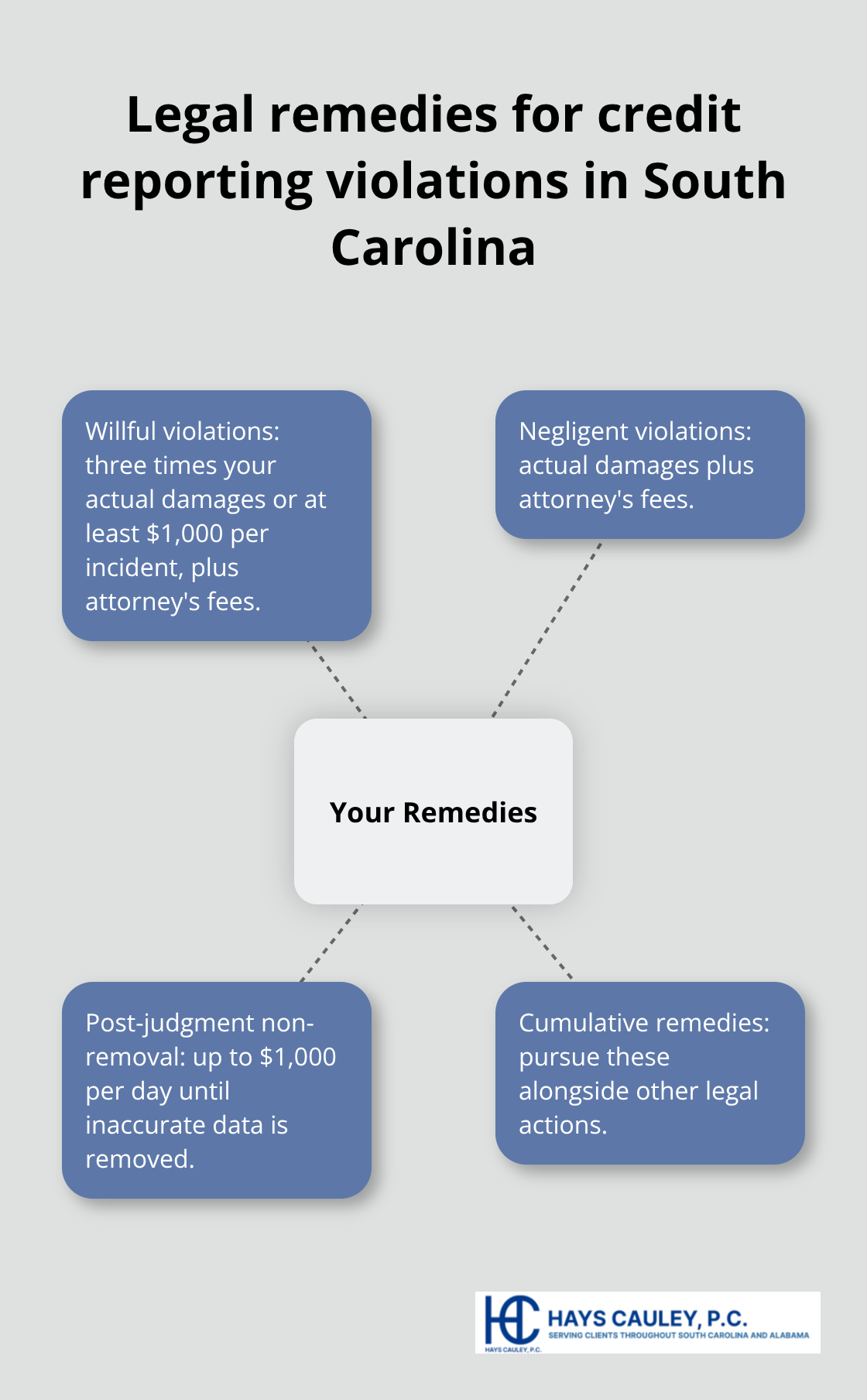

Violations of South Carolina’s credit reporting laws carry real consequences. Willful violations can result in three times your actual damages or at least $1,000 per incident, plus attorney’s fees. Negligent violations result in actual damages plus attorney’s fees. If an agency fails to remove inaccurate information after you obtain a judgment against them, damages can increase by up to $1,000 per day until removal occurs. These remedies are cumulative, meaning you can pursue them alongside other legal actions.

Understanding these protections matters because many agencies count on consumers not knowing their rights or not taking action. When you know what violations look like, you can identify them in your own situation and take steps to hold agencies accountable.

How to Dispute Errors on Your Credit Report

File Your Dispute in Writing

You must send a written dispute via certified mail with return receipt to the specific bureau that has the error. Include your full name, address, the account number in question, and a clear explanation of what is wrong. For example, if a payment shows as late when you paid on time, state the exact payment date and amount. The FTC provides sample dispute letters you can use as templates. Send identical disputes simultaneously to both the bureau and the business that reported the information, because the business often corrects errors faster than the formal bureau investigation. Written disputes create a paper trail that protects you legally, whereas phone disputes (Equifax at 866-349-5191, Experian at 888-397-3742, and TransUnion at 800-916-8800) lack documentation. Keep copies of everything you send and receive, including the certified mail receipts, because this documentation matters if you later pursue legal action against a bureau for violations.

What Information to Include

Your dispute letter must contain specific details about the error. State the exact account number, the specific information that is wrong, and any supporting documents like payment confirmations or account statements. Include the date you discovered the error and the date you paid (if applicable). The more precise your dispute, the faster the investigation moves. Vague complaints slow down the process because the bureau and furnisher must request clarification. Attach copies (not originals) of your supporting documents to both the bureau and the furnisher. This dual approach ensures both parties have the same evidence and cannot claim they lacked information to investigate properly.

Timeline for Resolution

The timeline for resolution typically runs 30 to 45 days from when you mail your dispute. The bureaus have 30 days to investigate, and furnishers can take up to 45 days to respond. After the investigation, corrected information usually appears on your report 30 to 45 days later, meaning the full process can stretch beyond two months. Check your status around day 35 after mailing to see if the investigation has started. Once the business corrects an error, it must notify all three bureaus, so the correction should eventually appear across your entire file. You should receive written results and a free copy of your updated report if changes occur.

What Happens If the Dispute Fails

If the investigation doesn’t resolve the dispute, you can add a brief statement to your file explaining your position and request that this statement appear in future reports sent to employers and creditors. If the disputed information remains and the bureau fails to investigate properly or the business refuses to verify accuracy, you have grounds to file a complaint with the Consumer Financial Protection Bureau or pursue legal action. Pull fresh reports every four months to confirm corrections were made and to catch new errors early. When bureaus or furnishers fail to investigate disputes properly, violations of South Carolina law occur, and consumers have legal remedies available to hold them accountable.

When Credit Bureaus Break the Rules

Violations happen more often than most consumers realize. The FTC receives thousands of complaints annually about credit reporting agencies failing to investigate disputes properly, continuing to report information after the legal deadline, or refusing to remove inaccurate data. When a bureau or furnisher violates South Carolina law, you have concrete remedies available.

Penalties for Willful and Negligent Violations

Willful violations carry penalties of three times your actual damages or at least $1,000 per incident, plus attorney’s fees. Negligent violations result in actual damages plus attorney’s fees. If an agency fails to remove inaccurate information after you win a judgment against them, damages increase by up to $1,000 per day until removal occurs. These penalties exist because violations cause real financial harm-denied credit, higher interest rates, or rejected rental applications all stem from inaccurate reporting.

The Most Common Violations

The most common violation we see is bureaus continuing to report accounts as delinquent without ever investigating your dispute or verifying the information with the business that reported it. A furnisher must contact you to verify accuracy before reporting negative information, yet many skip this step entirely. Another frequent violation occurs when a bureau receives your dispute and marks it as frivolous without conducting any investigation. Under federal law, the bureau can only dismiss a dispute as frivolous if it is clearly irrelevant or duplicative, not because the dispute is inconvenient.

Timing Violations and Deadline Failures

A furnisher has 30 days from receiving your dispute to investigate and report back to the bureau. Many furnishers ignore this deadline or respond after 45 or 60 days, which violates the law. If corrected information arrives late, you have grounds for legal action. The third violation occurs when bureaus continue reporting items beyond the legal time limits. Late payments must be removed after seven years, yet some bureaus leave items on file for eight or nine years. Bankruptcy information must be removed after ten years, not eleven.

How to Document and Report Violations

If you discover that a bureau or furnisher violated the law, document the violation with dates, account numbers, and copies of all correspondence. Contact the Consumer Financial Protection Bureau to file a complaint, which creates an official record. Then consult a consumer protection law firm in South Carolina. Your remedies are cumulative, meaning you can file complaints, pursue disputes, and pursue legal action simultaneously. Hays Cauley, P.C. helps consumers pursue violations aggressively and serves South Carolina, including Greenville, Columbia, and Charleston.

Final Thoughts

Pull your credit reports every four months from AnnualCreditReport.com and review each section for accounts you don’t recognize, incorrect payment statuses, or wrong balances. When you spot an inaccuracy, document it with account numbers and supporting evidence, then file written disputes with both the bureau and the furnisher at the same time. This dual approach speeds resolution and creates the paper trail you need if violations occur.

Your credit reporting rights in South Carolina are backed by real legal remedies-willful violations result in three times your actual damages or at least $1,000 per incident, plus attorney’s fees, while negligent violations carry actual damages plus attorney’s fees. If an agency fails to remove inaccurate information after a judgment, damages increase by $1,000 per day until removal. These penalties exist because credit reporting violations cause measurable financial harm through denied credit, higher interest rates, and rejected applications.

Contact a consumer protection law firm when a bureau or furnisher ignores your dispute, continues reporting information beyond legal time limits, or refuses to investigate your claim. We at Hays Cauley, P.C. help consumers pursue credit reporting violations and serve South Carolina, including Greenville, Columbia, and Charleston. If you’ve documented repeated violations or obtained a judgment that an agency still hasn’t honored, contact us to discuss your situation and learn whether you have grounds for legal action.