Your credit report shapes your financial future. Errors on it can cost you thousands in higher interest rates and denied loans.

We at Hays Cauley, P.C. help people across South Carolina fight back against inaccurate credit reports. A local credit report attorney can dispute errors, hold bureaus accountable, and protect your rights under federal law.

When You Need a Local Credit Report Attorney

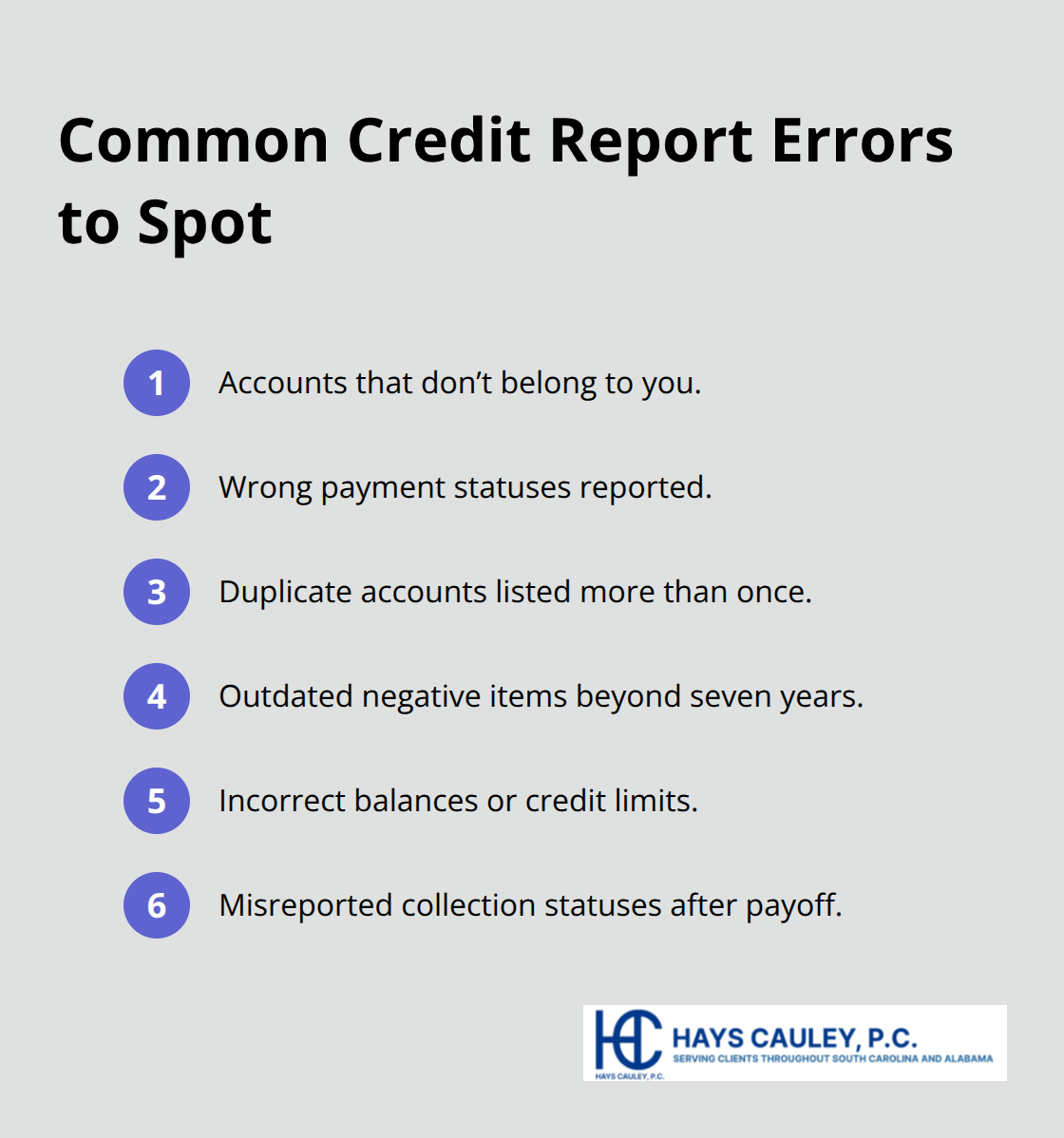

Spotting errors on your credit report requires knowing what to look for. The three major bureaus-Equifax, Experian, and TransUnion-report accounts, payment history, collections, and public records like judgments or liens. Inaccuracies fall into predictable categories: accounts that don’t belong to you, wrong payment statuses, duplicate entries, or outdated information that should have been removed. The CFPB’s Consumer Complaint Database shows that credit reporting complaints remain consistently high, with many stemming from accounts appearing on files years after they were closed or paid off. You can pull your credit reports from annualcreditreport.com to see the clearest picture of what lenders see. Once you spot an error-a missed payment showing as current, a collection account listed twice, or an account balance that doesn’t match your records-you face a decision: dispute it yourself or hire a local attorney.

The Real Cost of Staying Silent

Inaccurate credit reports hit your wallet hard and immediately. A single error can tank your score by 100 points or more, pushing you from approval-range credit into subprime territory where interest rates climb. The difference between a 750 credit score and a 650 score on a 30-year mortgage costs you over $150,000 in additional interest. Beyond mortgages, inaccuracies affect auto loans, credit cards, rental approvals, and even employment background checks in certain industries. The CFPB data shows that consumers often fail to catch errors because they don’t monitor reports regularly or don’t understand what they’re reading. Waiting six months or a year to address an error means six months or a year of damage to your creditworthiness. Clients who delay action watch their scores plummet while false accounts age on their files. The longer an error sits, the harder it becomes to remove because credit bureaus sometimes resist reinvestigation after initial disputes fail.

Why Geography Matters for Your Case

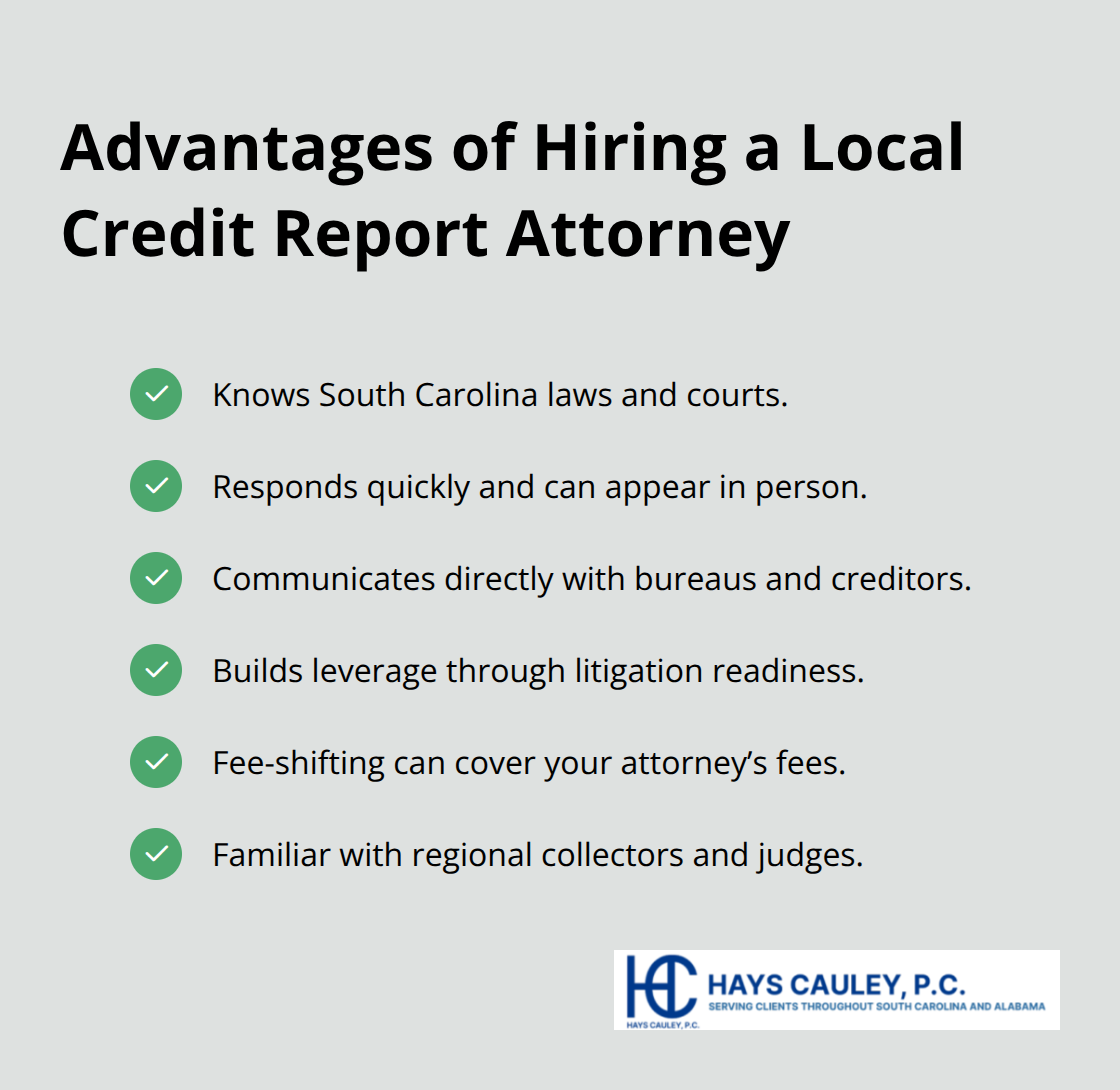

Local representation gives you advantages that online credit repair services cannot match. A local attorney knows the specific practices of regional debt collectors, understands how South Carolina courts interpret credit reporting law, and can physically appear in court if litigation becomes necessary. An attorney licensed in South Carolina also knows state-specific rules about security freezes, identity theft remedies, and damage calculations under the Fair Credit Reporting Act. Out-of-state firms charge similar fees but lack familiarity with local creditors and judges. When a bureau ignores your dispute or a collector refuses to validate a debt, a local attorney can file suit quickly and leverage relationships with local court systems. The Federal Fair Credit Reporting Act allows you to recover actual damages, statutory damages of up to $1,000 per violation, and attorney’s fees if you win. That means your legal fees often come from the violating party, not from your pocket.

What Errors Look Like in Practice

Credit report errors take many forms, and you need to recognize them to act. A collection account that you already paid off may still appear as active (damaging your score even though you resolved it). An account opened in someone else’s name signals identity theft and requires immediate attention. Duplicate accounts-the same debt listed multiple times-artificially inflate your total debt load and lower your score. Accounts with incorrect payment histories (showing late payments when you paid on time) undermine your creditworthiness without cause. Outdated negative items that exceed the seven-year reporting period should have been removed but sometimes remain. These errors compound over time, making your credit profile look worse than reality. A local attorney can identify which errors violate the Fair Credit Reporting Act and which ones qualify for removal or correction under federal law.

Choosing the Right Credit Report Attorney

Track Record Matters More Than Marketing

Finding an attorney who actually wins cases matters more than finding one with flashy marketing. Start by checking whether they’ve handled Fair Credit Reporting Act violations before-this is non-negotiable. The FCRA allows you to recover actual damages, statutory damages up to $1,000 per violation, and attorney’s fees, so an attorney who knows this law inside and out can calculate your case value accurately and pressure violators into settlement. Ask directly about their track record: How many FCRA cases have they settled or won in the past two years? What was the average recovery? An attorney who hesitates or gives vague answers is not the one you want.

Request references from past clients or ask to review settlement agreements (with names redacted). Real cases produce real numbers. When you call, listen for specificity. An attorney who talks about fighting credit bureaus in general terms hasn’t done the work. One who mentions recent cases involving duplicate accounts, outdated collections, or identity theft on credit files demonstrates hands-on experience. South Carolina courts have specific standards for what constitutes a willful violation under the FCRA, and a local attorney knows these standards cold.

Speed and Direct Communication Win Cases

Availability and communication style separate adequate representation from strong representation. Credit reporting cases move fast-the Fair Credit Reporting Act requires credit bureaus to complete reinvestigations within 30 days of your dispute, and delays cost you money every day. An attorney who takes weeks to return calls or communicates only by email will slow your case unnecessarily.

Call during business hours and time how quickly they pick up or return your message. Ask whether they handle your case personally or hand it off to paralegals. Confirm that the attorney will communicate directly with credit bureaus and creditors on your behalf-you should not manage back-and-forth exchanges yourself. This direct contact accelerates resolution and prevents miscommunication that damages your position.

Fee Structure and Written Agreements Protect You

Discuss their fee structure upfront. Contingency fees (where you pay nothing unless you win and the violating party covers costs) align the attorney’s interests with yours. Flat fees for dispute work typically range from $500 to $2,500 depending on complexity. Hourly rates vary widely by location and attorney experience.

Get everything in writing before you hire anyone. An attorney who pressures you to decide immediately or refuses to provide a written fee agreement is a red flag. A clear written agreement protects both you and the attorney by establishing expectations upfront. This document should specify what services the attorney will perform, when you owe payment, and what happens if your case settles or goes to trial.

With the right attorney selected and terms agreed upon, you’re ready to understand exactly what that attorney will do on your behalf.

What Your Attorney Does to Fix Your Credit Report

An attorney transforms your credit dispute from a frustrating back-and-forth into a legal action with teeth. When you hire representation, the attorney stops you from making costly mistakes that credit bureaus exploit. Many consumers dispute errors directly with bureaus and accept vague reinvestigation responses that don’t actually fix anything. The Fair Credit Reporting Act requires bureaus to complete reinvestigations within 30 days, but they often send form letters claiming they found no error without explaining what they checked or why they disagreed with your evidence. A local attorney drafts formal dispute letters that cite specific FCRA violations and demand detailed responses. These letters carry legal weight because they signal that litigation follows if the bureau ignores the dispute. When a bureau receives a letter from an attorney instead of a consumer, reinvestigation becomes thorough rather than cursory.

Formal Disputes That Demand Results

Your attorney files a lawsuit naming the bureau and any creditor who furnished false information if reinvestigation fails. Under the FCRA, you can recover actual damages (the money you lost due to the error), statutory damages of up to $1,000 per violation, and attorney’s fees. This fee-shifting provision means bureaus and creditors take attorney threats seriously because they know they’ll pay your legal costs if they lose. Your attorney also handles negotiations directly with creditors who furnished false data to the bureaus. Many collection accounts and late payments on your report come from creditors or debt buyers, not the bureaus themselves. A creditor who knows an attorney is investigating their reporting practices often agrees to remove the account from your file or pay a settlement to make the case disappear. This direct negotiation saves months of waiting for reinvestigation results that may never come.

Complaints That Trigger Regulatory Action

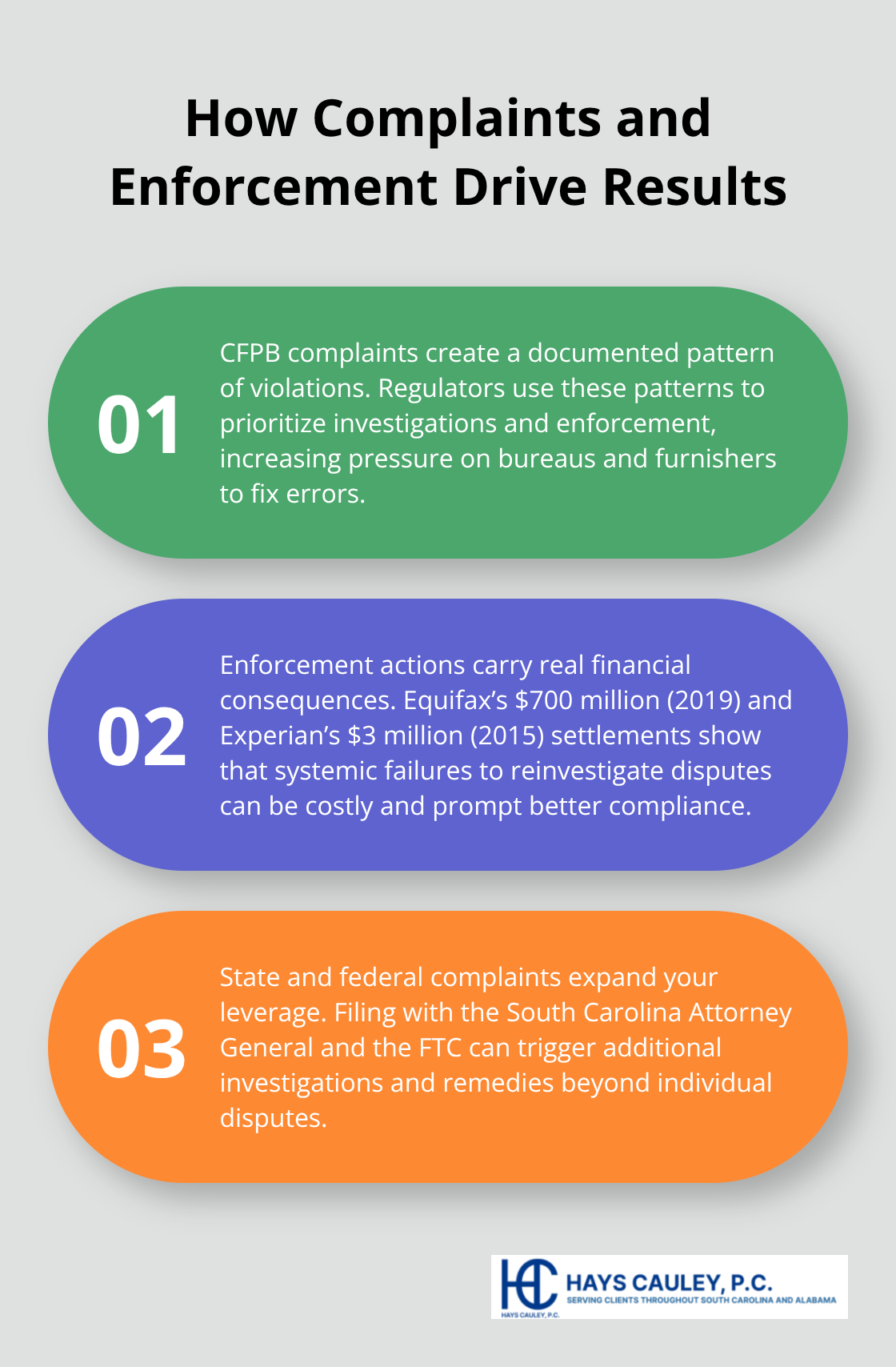

Filing a complaint against violators gives you leverage beyond what individual disputes provide. The Consumer Financial Protection Bureau maintains a complaint database where consumers report credit reporting problems, and patterns in those complaints influence CFPB enforcement actions. When your attorney files a complaint on your behalf, it becomes part of the public record and signals to regulators that the violator has crossed the line. The CFPB has issued enforcement actions against major bureaus including Equifax, Experian, and TransUnion for systematic failures to reinvestigate disputes properly. Equifax paid $700 million in a 2019 settlement, and Experian paid $3 million in 2015 for similar violations. These settlements prove that complaints and lawsuits work.

Your attorney also files complaints with the South Carolina Attorney General’s office and the Federal Trade Commission if the violation rises to the level of deceptive or unfair practice. State attorneys general have authority to pursue violators under state consumer protection laws, and your complaint can trigger an investigation that helps not just you but other consumers harmed by the same practice.

Documentation That Wins Cases

An attorney who handles your case gathers documentation that supports every claim. This means obtaining your original credit reports, the dispute letters you sent, the reinvestigation responses from bureaus, communications with creditors, and evidence of the damage the error caused (loan denials, higher interest rates, employment rejections). This documentation becomes the foundation of your case, and bureaus know that an attorney with a paper trail will win in court far more often than they will. The strength of your evidence determines whether a bureau settles quickly or fights the case through trial.

Final Thoughts

Your credit report controls access to loans, housing, and financial stability. Inaccurate information steals money from your future through higher interest rates and denied applications, but the Fair Credit Reporting Act gives you the right to dispute errors and recover damages when bureaus or creditors violate your rights. A local credit report attorney cuts through the confusion and forces action where credit bureaus have ignored your complaints, transforming your dispute from frustration into results.

Pull your credit reports from annualcreditreport.com and identify specific errors by writing down account names, balances, payment statuses, and dates that don’t match your records. Document any loan denials, higher interest rates, or employment rejections that resulted from inaccurate reporting, as this documentation proves the damage the error caused and becomes the foundation of your case. The FCRA’s fee-shifting provision means you recover attorney’s fees from the party that violated your rights, making legal representation affordable even when your case is complex.

Contact Hays Cauley, P.C. for a free consultation and bring your credit reports and documentation. Ask about their track record with Fair Credit Reporting Act cases, their fee structure, and their timeline for resolution. A strong local credit report attorney will answer directly and provide references or settlement examples that demonstrate hands-on experience. Serving South Carolina, including Greenville, Columbia and Charleston.