Your credit report shapes your financial life. Errors on that report can cost you thousands in higher interest rates and denied loans. We at Hays Cauley, P.C. help South Carolina residents fix these problems through legal action.

A credit report attorney SC can challenge inaccurate information and hold creditors accountable for violations.

Why Your Credit Report Matters

Your credit report determines whether you qualify for loans, what interest rates you’ll pay, and sometimes whether you get hired. Lenders pull your report before approving mortgages or auto loans. Employers check it before offering jobs. Insurance companies use it to set premiums. A single error on your report triggers a chain reaction: a missed loan approval, higher monthly payments, or a job offer rescinded. The FTC reported over 175,000 complaints about credit reporting in 2020, and about 1 in 5 consumers find an error on at least one of their three credit reports from Equifax, Experian, or TransUnion. These aren’t rare problems. They’re widespread enough that you should assume your report contains mistakes until you verify otherwise.

Errors That Actually Harm You

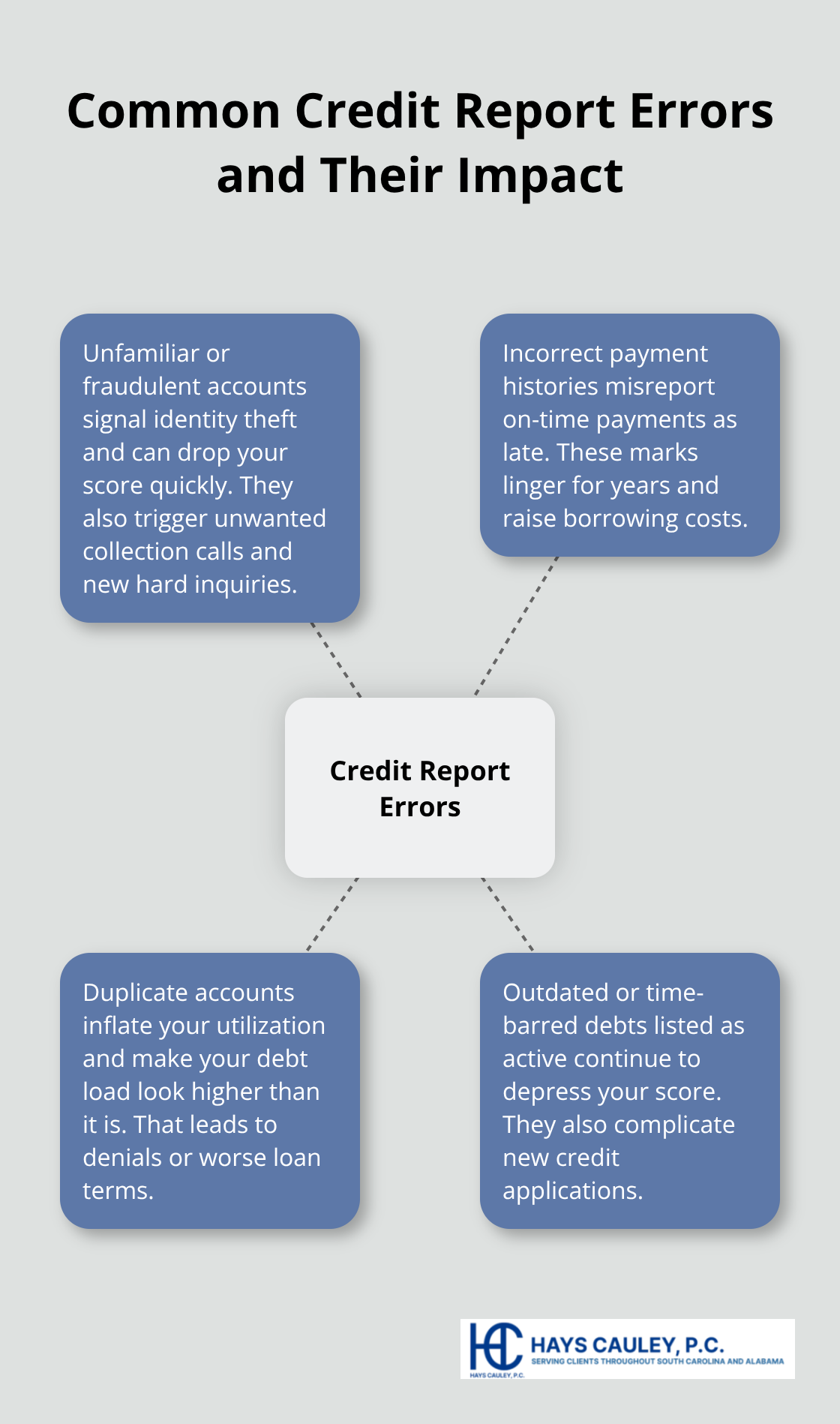

Unfamiliar accounts appearing on your report suggest fraud or identity theft. An account you never opened tanks your credit score and triggers collection calls from creditors you’ve never heard of.

Incorrect payment histories cause equal damage-a lender reporting you paid late when you actually paid on time stays on your record for years and costs you thousands in higher interest rates. Duplicate accounts of the same debt inflate your credit utilization ratio and make your financial situation look worse than it is.

These problems carry real costs. If a lender sees a late payment mark from three years ago, they’ll deny your mortgage application or charge you 0.5 to 1 percent more in interest. On a $300,000 home loan, that amounts to $1,500 to $3,000 per year in extra costs. Outdated debts listed as active when they should be removed also harm your score and your ability to borrow.

The Legal Window Closes Fast

Time pressure matters. Under the Fair Credit Reporting Act, you generally have two years from discovery or five years from the error’s occurrence to file a lawsuit against credit bureaus or creditors. That window closes. Every month you wait with an error on your report means a month of higher interest rates, rejected applications, or missed opportunities.

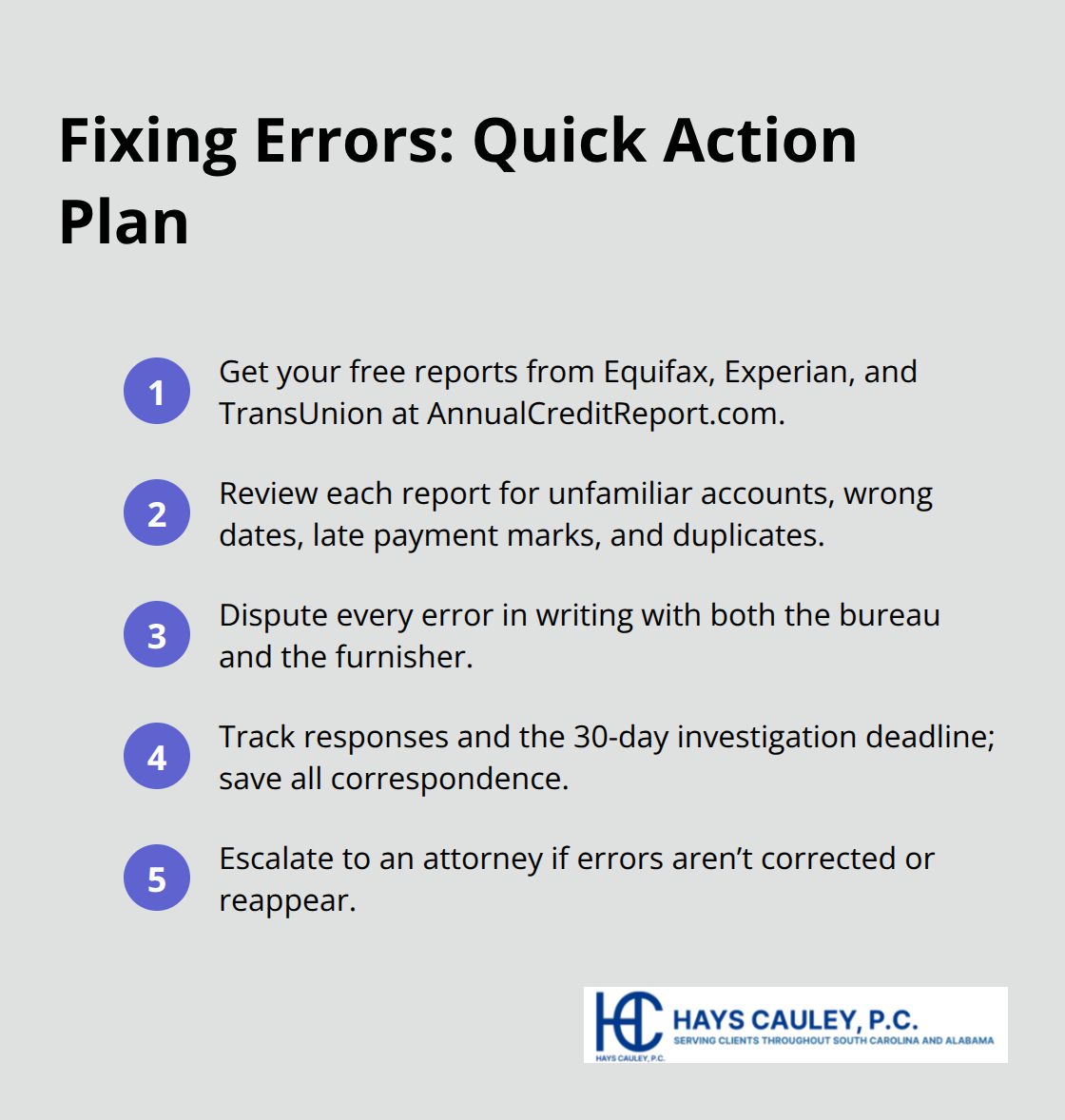

South Carolina residents can obtain one free credit report per bureau each year through AnnualCreditReport.com. Pull them now. Look for unfamiliar accounts, incorrect dates, payment marks that don’t match your records, and duplicate entries.

If you find errors, dispute them immediately with both the credit bureau and the furnisher (the creditor or lender reporting the information). The bureaus must investigate within 30 days and correct verified errors. If they don’t, you have grounds for legal action.

What Happens When Bureaus Ignore You

The credit bureaus don’t always correct errors on their own. Some furnishers ignore dispute requests. Some bureaus conduct incomplete investigations and reinstate false information. When that happens, you need someone who understands your rights under federal and state law. A credit report attorney can review your dispute history, identify violations, and pursue damages that the bureaus won’t voluntarily pay. Whether you’ve already disputed errors or you’re starting from scratch, legal action can force corrections that protect your financial future.

When to Hire a Credit Report Attorney

Signs You Need Legal Help

You need a credit report attorney when the credit bureaus refuse to correct errors after you’ve disputed them directly. The Fair Credit Reporting Act requires bureaus to investigate disputes within 30 days and correct any information they cannot verify. If that doesn’t happen, you’ve hit a wall that only legal action can break through. You also need an attorney if you’ve already filed disputes with the bureaus and furnishers but the false information remains on your report months later. At that point, waiting longer costs you real money in denied loans and higher interest rates.

Additionally, if you discover that a credit bureau or creditor violated the FCRA through incomplete investigations, failure to notify you of adverse actions, or unauthorized access to your report, an attorney can identify those violations and pursue damages. Some violations carry statutory penalties up to $1,000 per incident under federal law, plus actual damages and attorney fees. South Carolina law may provide additional claims beyond federal protections, which a local attorney can evaluate for your situation.

How Attorneys Force Corrections

An attorney accelerates corrections that the bureaus won’t make voluntarily. A credit report attorney reviews your complete dispute history to identify where the bureaus or furnishers failed their legal obligations. The attorney then drafts demand letters tailored to federal and state requirements, which increases pressure for corrections without requiring immediate court filing. If the bureaus still refuse, the attorney compiles evidence of harm-such as denied loan applications, higher interest costs, or missed job opportunities-and files suit to pursue actual damages, statutory penalties, and legal fees.

Timeline and Deadlines

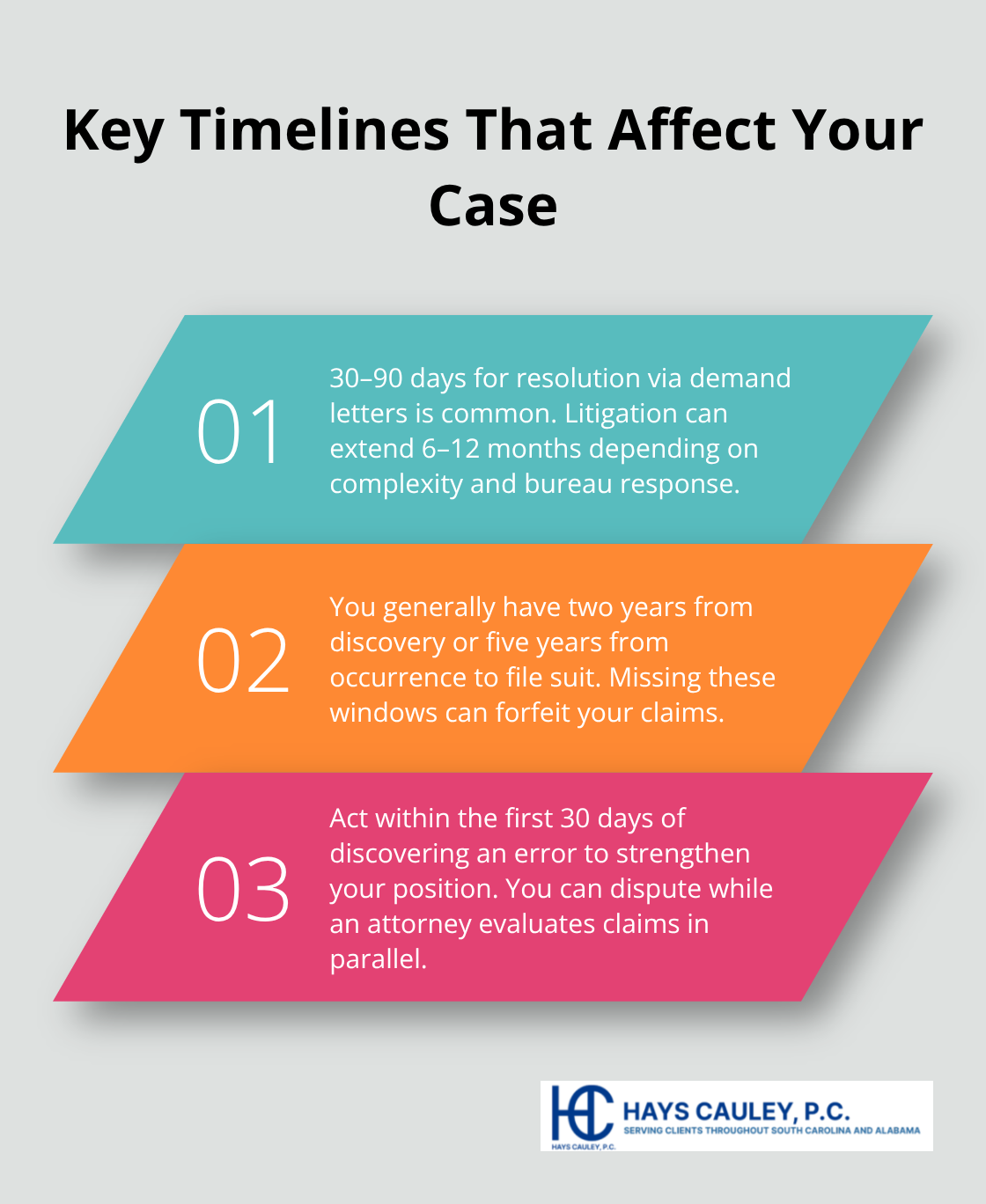

The timeline from initial dispute to resolution typically takes 30 to 90 days if handled through demand letters alone, but litigation can extend 6 to 12 months depending on the complexity and the bureau’s response. You have up to two years from discovery of a violation or five years from when the error occurred to file a lawsuit, so waiting beyond that deadline forfeits your right to sue. Acting within the first 30 days after discovering an error gives you the strongest position, since you can still pursue the dispute process while an attorney evaluates your legal claims simultaneously.

The window for legal action closes fast. Every month you delay with an error on your report means another month of financial damage. South Carolina residents who have exhausted the dispute process on their own should contact a local attorney to discuss whether violations occurred and what damages they can recover. The next section covers what to look for when selecting an attorney who understands your state’s regulations and can navigate both federal and state law effectively.

Finding a Credit Report Attorney Serving South Carolina, Including Greenville, Columbia and Charleston

When you search for a credit report attorney in South Carolina, you’ll encounter firms that handle credit disputes alongside bankruptcy, debt collection defense, and general consumer law. This matters because credit reporting law requires focused knowledge of both the Fair Credit Reporting Act and South Carolina’s Consumer Identity Theft Protection Code. A firm that treats credit disputes as one service among many won’t have the depth of experience needed to identify all violations in your case or to maximize your recovery.

The attorney you hire should have handled cases under both federal law and South Carolina law, since violations of either can support your claim for damages. The Fair Credit Reporting Act allows you to recover actual damages, statutory damages up to $1,000 per violation, and attorney fees if a bureau or furnisher violates your rights. South Carolina law may provide additional claims for negligent or willful noncompliance that go beyond federal protections, and a local attorney familiar with state court decisions will know which violations carry the highest recovery potential in your jurisdiction.

What to Look for in Your Initial Consultation

Ask the attorney whether they’ve filed suits in South Carolina courts and whether they’ve recovered damages under both federal and state theories. An attorney who hesitates or gives vague answers hasn’t done this work regularly. During your initial consultation (which should be free), ask the attorney to explain the specific violations they see in your case based on your dispute history. If they can’t point to concrete violations and explain the legal basis for each one, they won’t effectively represent you in court or in settlement negotiations.

The attorney should ask detailed questions about your dispute timeline, the responses you received from bureaus, and any adverse actions you suffered as a result of the errors. That thoroughness signals they understand how to build a damages case.

Questions That Separate Strong Candidates from Weak Ones

Ask whether the attorney has handled cases involving the specific type of error on your report. If you have unfamiliar accounts from identity theft, ask about their experience with identity theft claims under South Carolina law. If you have duplicate accounts or outdated debts listed as active, ask how many cases they’ve won based on those errors.

Ask how they calculate damages and what range of recovery they typically see in cases similar to yours. An experienced attorney will give you a realistic range based on factors like the age of the error, the number of violations, and the extent of your financial harm. Ask whether they work on contingency or require upfront fees. Some attorneys charge upfront fees for demand letter work and shift to contingency if litigation becomes necessary. Others work entirely on contingency, meaning you pay nothing unless they recover damages. Understand the fee structure before hiring, since it affects your net recovery.

Ask how long they expect your case to take from initial consultation to resolution. Most credit report disputes settle within 6 to 12 months if violations are clear, but complex cases involving multiple bureaus or furnishers can extend longer. Realistic timelines matter because every month your case remains open is a month you live with the error’s financial impact.

Why Local Representation Matters

A South Carolina attorney who practices in your region understands how local courts handle credit reporting cases and which judges have a track record of awarding substantial damages in FCRA violations. They know the specific courthouses in Greenville, Columbia, and Charleston and have relationships with court staff that can accelerate scheduling and filings. They also understand South Carolina-specific issues like how the state’s exemption laws affect asset seizure if a creditor obtains a judgment against you, which intersects with credit reporting disputes when errors lead to collection lawsuits.

A national firm based in another state lacks this local knowledge and may miss opportunities unique to your jurisdiction. Additionally, a local attorney can meet with you in person to review your documents and discuss strategy face-to-face, which builds trust and allows for more thorough case preparation than phone consultations alone. When you call, ask whether the attorney maintains an office in your area and whether they handle cases in your county’s courts regularly. If they work remotely and rarely appear in local courtrooms, they’ll struggle to navigate the procedural nuances that affect your case’s outcome.

Final Thoughts

Your credit report error won’t fix itself, and the credit bureaus won’t voluntarily correct information they’ve already investigated, even when that information is wrong. The furnishers won’t reinvestigate without pressure, and waiting costs you real money every month in higher interest rates, denied applications, and missed opportunities. Only legal action backed by someone who understands both federal law and South Carolina regulations can force the corrections you need.

A credit report attorney SC can identify violations you might miss on your own and pursue damages that make the bureaus take your case seriously. The Fair Credit Reporting Act gives you the right to recover actual damages, statutory penalties up to $1,000 per violation, and attorney fees when bureaus or creditors violate your rights. South Carolina law may provide additional claims that increase your total recovery.

Start by pulling your free credit reports from Equifax, Experian, and TransUnion through AnnualCreditReport.com if you haven’t already. If you’ve already disputed errors and the bureaus refused to correct them, contact us for a free consultation to discuss your case and learn what damages you can recover. The two-year window from discovery of a violation closes faster than you think.