A mistake on your credit report can tank your score and cost you thousands in higher interest rates. The good news: you can fix credit report errors quickly if you know the right steps.

We at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia, and Charleston, fight back against inaccurate credit information. This guide walks you through the fastest way to dispute errors and get your file corrected.

What Errors Show Up Most on Credit Reports

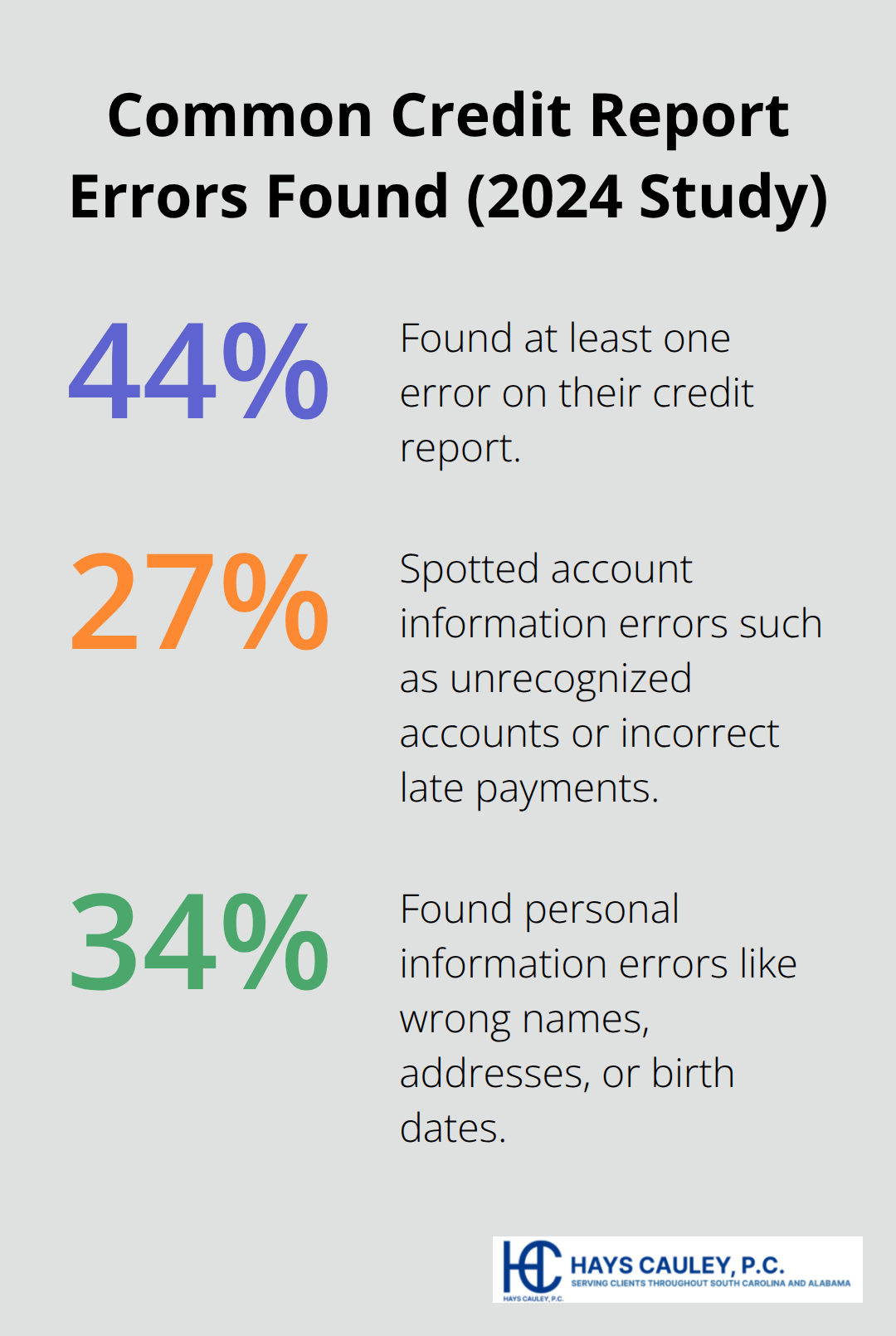

Credit report mistakes plague millions of Americans. According to a 2024 Credit Checkup study by Consumer Reports and WorkMoney involving over 4,000 participants, 44% of people who reviewed their credit reports found at least one error. That’s nearly one in two people. The study revealed that 27% spotted account information errors such as unrecognized accounts, late payments incorrectly reported, or debts that don’t belong to them.

Another 34% found personal information errors including wrong names, addresses, or birth dates. These aren’t rare edge cases-they’re widespread problems that directly impact your ability to borrow money and secure favorable interest rates.

Identity Mix-ups and Wrong Account Information

One of the most damaging errors occurs when someone else’s information gets mixed into your file. Mixed files happen when another person with a similar name or Social Security number has their accounts incorrectly linked to your report. You might see accounts you never opened, late payments you never made, or collection accounts that belong to someone else entirely. The FTC found that 1 in 5 consumers had an error on at least one of their three major credit reports, and many of these stem from identity confusion rather than fraud. If you spot an account you don’t recognize or a payment history that isn’t yours, that’s a red flag pointing to a mixed file. This requires immediate action because these errors can lower your credit score by 25 points or more, directly raising your borrowing costs.

Paid Accounts Still Showing as Delinquent

A surprisingly common error involves accounts you’ve already paid off appearing as open or delinquent on your report. The credit bureaus-Equifax, Experian, and TransUnion-sometimes fail to update account status after you’ve settled the debt. You paid the loan or credit card in full, but your report still shows it as active or with late payments. This happens because the furnisher (the lender or creditor reporting the information) may not have properly communicated the payoff to the credit bureaus, or the bureaus failed to process the update. The impact is real: lenders see an active debt or a history of missed payments and treat you as a higher-risk borrower. If you’ve paid something off within the last seven years and it still appears delinquent, dispute it immediately. The 2013 FTC study found that 4 in 5 consumers who filed disputes experienced some modification to their credit report, meaning most errors get corrected once you challenge them.

Why These Errors Matter Right Now

The stakes are high when inaccurate information sits on your file. A single error can cost you thousands in higher interest rates on mortgages, auto loans, or credit cards. Lenders rely on your credit report to determine whether you qualify for credit and what rate they’ll charge you. Employers and insurance companies also access credit reports (with your permission) to make hiring and coverage decisions. The longer an error remains uncorrected, the more damage it inflicts on your financial life. This is why the next step-knowing exactly how to dispute these errors-matters so much.

Getting Your Credit Reports and Starting the Dispute Process

Pull Your Reports from All Three Bureaus

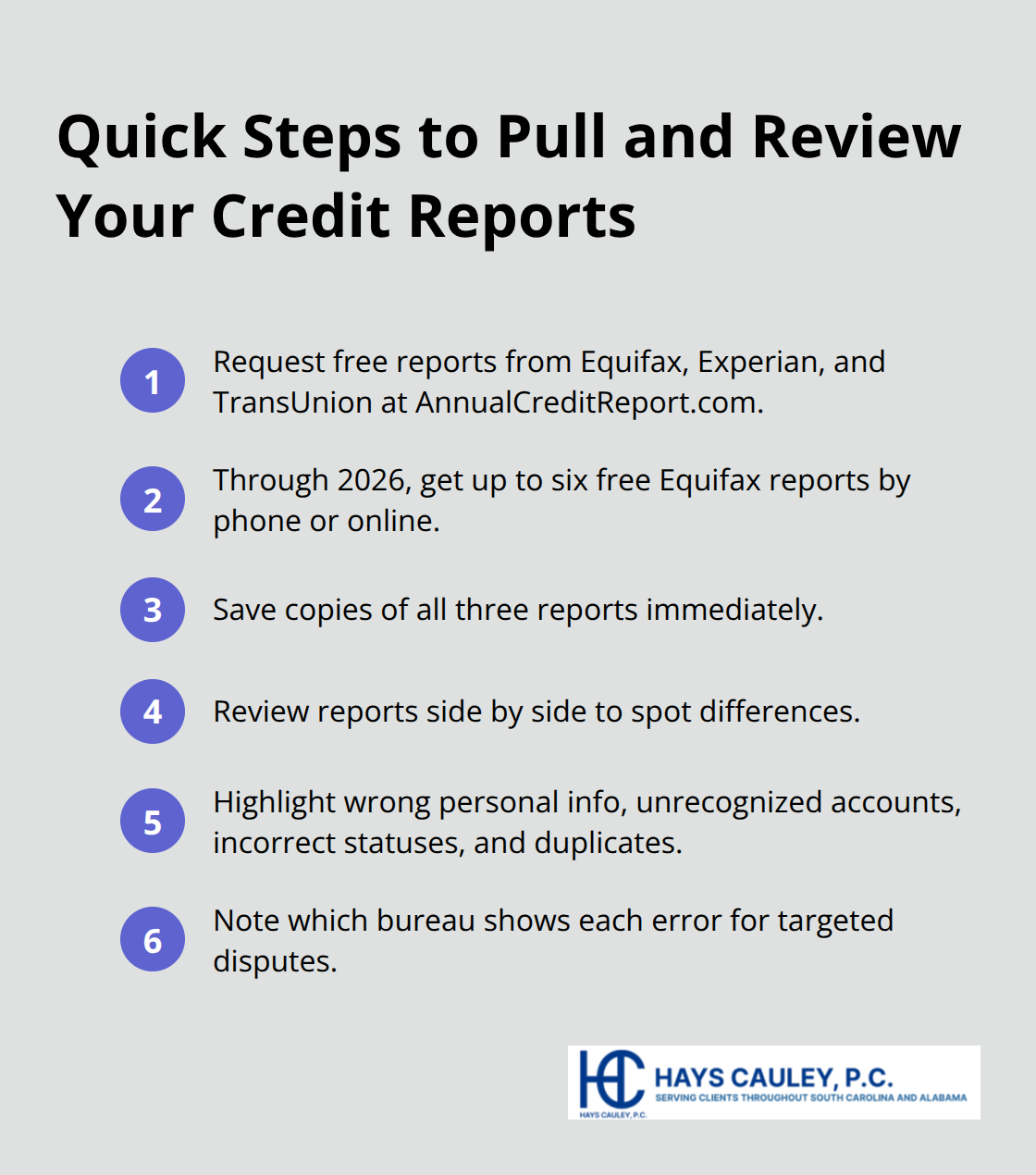

Start by obtaining your actual credit reports from all three bureaus before you file a single dispute. Visit AnnualCreditReport.com, the federally authorized portal, and request your free reports from Equifax, Experian, and TransUnion. Through 2026, Equifax offers six free reports per year if you call 1-866-349-5191 or visit their site directly, which gives you a significant advantage over the standard annual access. Print or save digital copies of all three reports immediately.

Review each one side by side because errors often appear on one bureau’s report but not the others. Circle or highlight every error you find, including wrong personal information, accounts you don’t recognize, incorrect payment statuses, and duplicate listings. This comparison step catches mixed files and identity theft issues that might otherwise slip through.

Contact Each Credit Reporting Company Separately

Once you’ve identified the errors, contact each credit reporting company that shows the mistake on their report. Do not assume one dispute covers all three bureaus; you must dispute with each bureau separately. Equifax’s dispute line is 1-866-349-5191, Experian is 1-888-397-3742, and TransUnion is 1-800-916-8800. You can dispute online, by phone, or by mail, but mail provides the strongest documentation trail. If you mail your dispute, send it certified with return receipt requested and include your full name, current address, the account number showing the error, a clear explanation of why the information is wrong, copies of supporting documents that prove your case, and a copy of your report with the errors circled. The credit reporting company has up to 30 days to investigate and must forward all relevant information to the furnisher (the business that originally reported the data). Keep copies of everything you send and receive.

Contact the Furnisher Directly

Also contact the furnisher directly using the address listed on your credit report or their designated dispute address. Furnishers must investigate within 30 days and either correct the information or explain why they believe it’s accurate. If they cannot verify the information, they must remove it and notify all three bureaus. Your documentation becomes critical here because the furnisher will request proof that the information is inaccurate, and your supporting documents must clearly demonstrate the error. The FTC study from 2013 tracked over 1,000 consumers who filed disputes and found that 4 in 5 experienced some modification to their credit report, proving that disputes work when properly documented. This dual approach-disputing with both the credit reporting company and the furnisher-maximizes your chances of a quick resolution and prevents the same error from reappearing on your file months later.

What Happens After You File a Dispute

The 30-Day Investigation Window

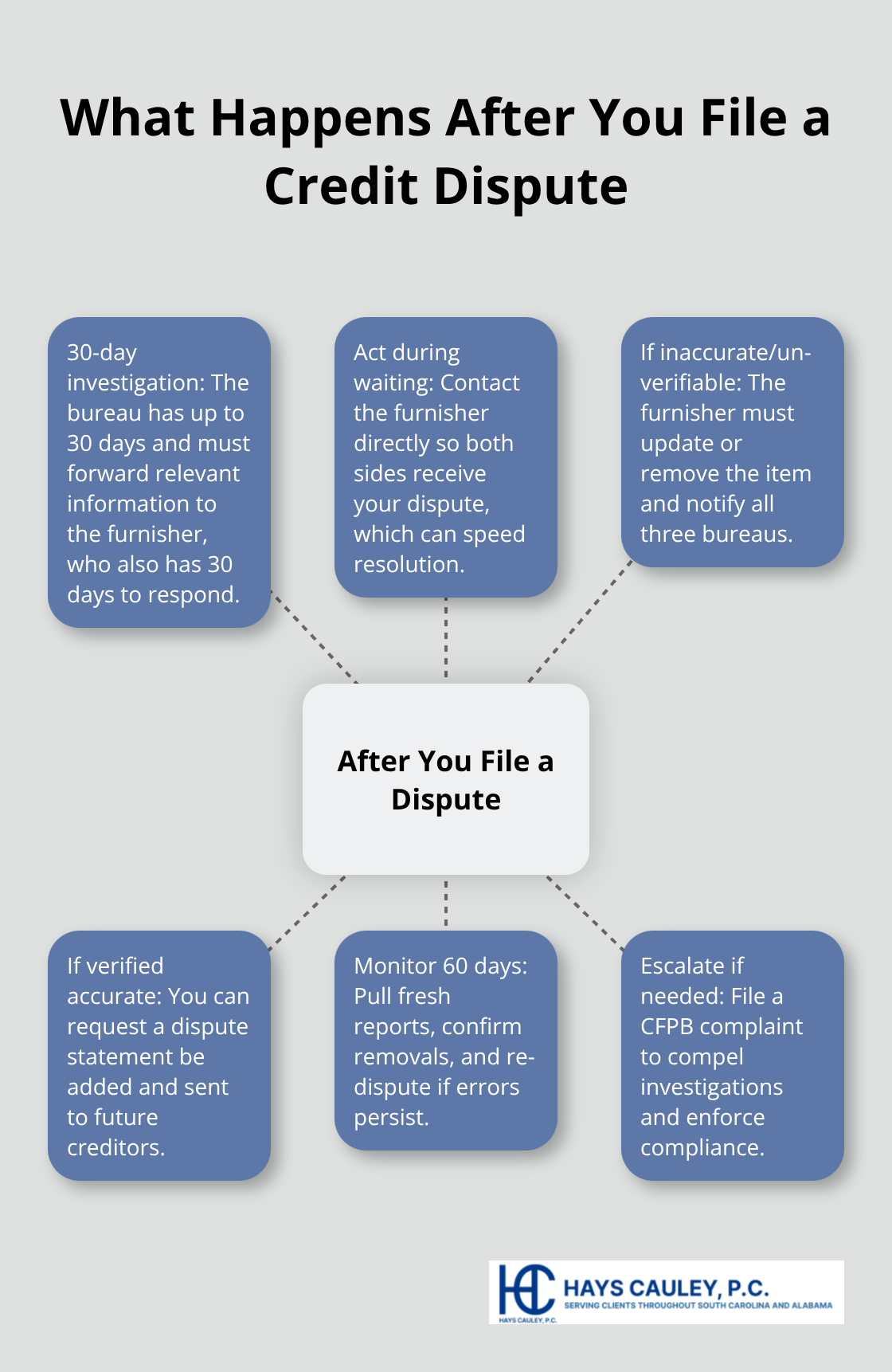

After you submit your dispute to a credit reporting bureau, that bureau has up to 30 days to investigate your claim and forward all relevant information to the furnisher. The furnisher then has their own 30-day window to respond. In practice, most investigations conclude within this timeframe, though some stretch closer to the deadline. The FTC tracked over 1,000 consumers through the dispute process and found that 4 in 5 experienced some modification to their credit report, meaning the system works when you follow through properly.

Taking Action During the Waiting Period

Do not sit idle while the investigation proceeds. Contact the furnisher directly if you haven’t already, because the credit bureau’s investigation moves faster when the furnisher receives your dispute from both directions simultaneously. According to the FTC study, slightly more than 1 in 10 consumers saw a change in their credit score after corrections were made, with about 1 in 20 experiencing maximum score changes of more than 25 points. Even modest score improvements translate into lower interest rates on future loans.

What the Furnisher’s Response Means

What happens next depends on the furnisher’s findings. If the furnisher determines the information is inaccurate or cannot verify it, they must update or remove it and notify all three bureaus so your file gets corrected across the board.

If the furnisher claims the information is accurate and refuses to change it, you have the right to request that a dispute statement be included in your file and sent to future creditors. This dispute notation protects you by signaling to lenders that you contested the information.

Monitoring Your Reports After Investigation

After the bureaus’ investigation concludes, monitor your three credit reports closely for the next 60 days. Pull fresh copies from AnnualCreditReport.com and compare them to your original reports. Verify that errors were actually removed, not just marked as disputed. If an error persists after the investigation concludes, file a second dispute immediately and contact the furnisher again. The credit reporting system rewards persistence-most errors disappear on the first try, but stubborn ones require follow-up action.

Escalating Disputes That Don’t Resolve

Keep all dispute letters, investigation responses, and supporting documents for at least three years. If you encounter resistance from a bureau or furnisher, you can file a complaint with the Consumer Financial Protection Bureau, which has authority to compel investigations and enforce compliance. The CFPB tracks complaints and identifies patterns of non-compliance across the credit reporting industry.

Final Thoughts

Credit report errors don’t fix themselves, and the longer inaccurate information sits on your file, the more it costs you in higher interest rates and rejected loan applications. You now have the tools to fix credit report quickly: pull your reports from all three bureaus, file disputes with both the credit reporting companies and furnishers, document everything, and monitor your file for changes. The FTC data proves this works-4 in 5 consumers who filed disputes experienced modifications to their credit reports.

Most errors disappear within 30 to 60 days once you take action, though some stubborn cases require follow-up disputes and persistence. Start today by visiting AnnualCreditReport.com and reviewing all three of your reports side by side. Circle every error you find and begin your disputes immediately.

If disputes stall or furnishers refuse to correct clear errors, we at Hays Cauley, P.C. can help you resolve credit reporting disputes that don’t respond to standard procedures. Contact us if you encounter resistance from credit bureaus or furnishers, or if you suspect identity theft is behind your errors-we serve South Carolina residents, including those in Greenville, Columbia, and Charleston.