![Verify Debt Before You Pay [Guide]](https://hayscauley.net/wp-content/uploads/emplibot/debt-collector-verification-hero-1771718914-1024x585.jpeg)

Debt collectors contact millions of Americans each year, and many people pay debts without confirming they’re actually responsible for them. At Hays Cauley, P.C., we’ve seen how debt collector verification can protect you from paying obligations that may be invalid, outdated, or even fraudulent.

This guide walks you through the steps to verify any debt before handing over money, the mistakes that cost people thousands of dollars, and the legal rights you have when disputing accounts.

Steps to Verify Your Debt Right Now

Act Within Your 30-Day Window

The moment a debt collector contacts you, you have 30 days to act. This window is your protection under the Fair Debt Collection Practices Act, and wasting it costs you leverage. Send a written verification request to the debt collector within those 30 days. This request must ask for the creditor’s name, the original account number, the exact amount owed, and proof that the collector has the legal right to collect from you. The collector must stop collection activities on the disputed portion of the debt until they respond with verification or a judgment.

Request Complete Documentation

Many collectors fail to provide adequate documentation because they purchased the debt for pennies on the dollar and never received complete files from the original creditor. Request an itemized breakdown showing principal, interest, fees, and any payments or credits applied since a specific date. Ask for the date the debt became delinquent and the statute of limitations expiration date for your state. Without these details in writing, you cannot confirm whether the amount is accurate or if the debt is even collectible.

Check Your Credit Report for Discrepancies

Your credit report is your second verification tool, and you should pull it immediately from AnnualCreditReport.com, which provides free annual reports from all three bureaus. Compare the account number, balance, and delinquency date to what the collector claims. If the reported balance differs significantly from the collector’s demand, that’s a red flag worth investigating. Many debts on credit reports carry errors in interest calculations or duplicate listings. File a dispute directly with the credit bureau if you spot inaccuracies.

Verify With the Original Creditor

Contact the original creditor independently to verify charges, especially for medical or utility debts where billing errors are common. Ask them for a complete payment history and itemized statement. This step protects you from paying inflated amounts that collectors added without authorization.

Determine If the Debt Is Time-Barred

Determine whether the debt is time-barred under your state’s statute of limitations. In South Carolina, most debts have a three-year window for collection, though some accounts may be older. A time-barred debt doesn’t disappear from your credit report, but collectors cannot sue you over it. Avoid admitting the debt or making a payment if it’s time-barred, as that action can restart the clock. Once you complete verification, you’ll know exactly what you owe and whether you have valid defenses against collection.

Mistakes That Destroy Your Debt Defense

Pay After Verification, Not Before

The biggest mistake people make is paying a debt collector before verification is complete. Once you send money, you admit the debt exists and may restart the statute of limitations clock, even if the debt was time-barred. The Federal Trade Commission notes that consumers who pay before verification lose their strongest legal position. If the collector cannot produce valid documentation, you have no obligation to pay anything.

Many people panic when contacted and hand over money within days, thinking it will end the harassment. This action weakens your negotiating power and eliminates your right to dispute. The 30-day window exists specifically to protect you from making this mistake. Send your verification request in writing within that timeframe, and do not make any payment until the collector responds with complete documentation proving the debt is yours and that they have the legal authority to collect it.

Challenge Unrecognized Debts on Your Credit Report

A second critical error is ignoring debts on your credit report that you don’t recognize. Many consumers assume that if a debt appears on their credit report, it must be legitimate. This assumption costs them thousands in unnecessary payments. The CFPB reports that errors appear on approximately 20 percent of credit reports, and duplicate listings occur frequently when a debt has been sold multiple times between collectors.

When you spot an unrecognized account, do not ignore it hoping it will disappear. Instead, file a dispute with the credit bureau immediately using their official dispute process. Simultaneously, request validation from the collector claiming to own the debt. Taking action on unrecognized accounts protects you far more than silence ever will.

Document Everything in Writing

A third mistake that destroys your defense is failing to document everything in writing. Collectors count on verbal conversations disappearing into thin air, leaving no evidence of what was promised or claimed. Every communication with a debt collector must appear in writing: send verification requests via certified mail or email with read receipts, keep copies of all letters you receive, and maintain a detailed log with dates, times, and names of anyone you spoke with.

This documentation becomes your evidence if the collector violates the Fair Debt Collection Practices Act or if the dispute ends up in court. Written records also prevent collectors from misrepresenting what they told you or what you agreed to pay. Your next step involves understanding the specific legal protections that apply to your situation-protections that give you real power when you know how to use them.

Legal Protections That Stop Collectors Cold: Serving South Carolina, including Greenville, Columbia and Charleston

The Fair Debt Collection Practices Act Gives You Real Power

The Fair Debt Collection Practices Act provides specific weapons against collectors who cannot prove what they claim. Under this federal law, collectors must provide a written validation notice within five days of first contact, and that notice must include the creditor’s name, the exact debt amount, and your right to dispute within 30 days. If you send a written verification request within that 30-day window, the collector must stop all collection activity on the disputed amount until they mail you verification or a court judgment proving the debt is yours. This pause is not optional-it’s the law.

The Federal Trade Commission enforces these rules, and violations carry real consequences. You can recover actual damages plus up to $1,000 in additional damages per violation, plus attorney fees and court costs if you win. This means a collector who ignores your dispute request or continues calling after you’ve requested verification in writing has just exposed themselves to a lawsuit.

How to Send a Verification Request That Works

Send your verification request via certified mail with return receipt or email with read confirmation so you have proof of delivery. Include a specific request for the original creditor’s name and address, the account number, the date the debt became delinquent, the current balance itemized by principal and fees, and documentation showing the collector purchased the right to collect from you.

Many collectors cannot produce this documentation because they bought the debt in bulk from third parties without receiving complete files. When they fail to respond adequately within 30 days, you have grounds to dispute the entire debt. The written record you create protects you far more than any phone call ever could.

File a Dispute With the Credit Bureaus

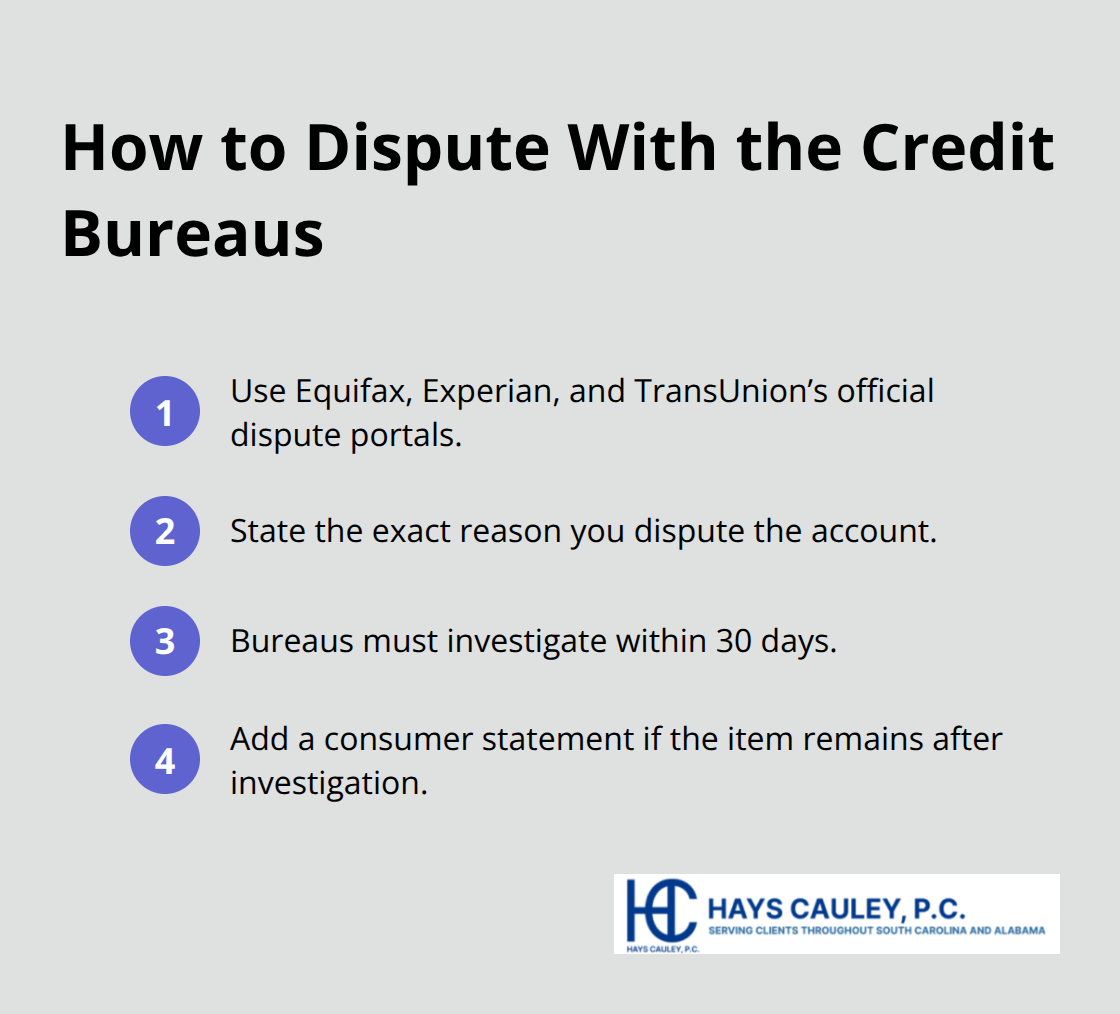

File a dispute with the credit bureaus to create a second layer of protection that works independently from your collector dispute. Contact Equifax, Experian, and TransUnion directly through their official dispute portals at their websites-not through third-party dispute services that charge fees for work you can do yourself. Explain exactly why you dispute the account: state that you don’t recognize it, that the amount is incorrect, that it’s a duplicate listing, or that the collector failed to validate it.

The credit bureau must investigate within 30 days and remove the account if the collector cannot verify it. If the account remains after investigation, request that a consumer statement be added to your credit file explaining your dispute. This statement appears whenever someone reviews your credit report. The CFPB notes that approximately 20 percent of credit reports contain errors, so disputing unrecognized accounts is not unusual or suspicious-it’s how the system corrects mistakes.

Protect Yourself From Continued Violations

Keep copies of everything you send to the credit bureaus and save their responses. If a collector continues collection efforts after you’ve filed a credit bureau dispute and sent a written verification request, that’s a violation you can report to the CFPB or pursue in court with an attorney. Your documentation becomes the evidence that proves the collector violated federal law and ignored your rights.

Final Thoughts

Debt collector verification protects you from paying debts you don’t owe, and the steps in this guide-requesting validation, checking your credit report, and verifying with the original creditor-shift the burden back to collectors to prove their claims. You have legal rights under the Fair Debt Collection Practices Act, and using them costs you nothing except the effort to send written requests and maintain records. Start today by pulling your credit report from AnnualCreditReport.com and reviewing every account listed.

If you spot debts you don’t recognize or amounts that seem wrong, send a written verification request to the collector within your 30-day window and file disputes with the credit bureaus simultaneously. Keep copies of everything you send and receive, as this documentation becomes your evidence if the collector violates federal law or if you need to defend yourself in court. Many collectors count on consumers ignoring their rights and paying without verification.

When you request validation in writing and document every step, you shift the burden back to them to prove what they claim. If you’re facing aggressive collection activity or believe a collector has violated your rights, contact Hays Cauley, P.C. to discuss your situation and learn what options are available to you.