A mistake on your credit report can damage your financial future. Inaccurate information might lower your credit score, making it harder to get loans or favorable interest rates.

South Carolina residents have strong legal protections when errors appear on their credit files. We at Hays Cauley, P.C. help people understand and exercise their SC reporting rights to fix these problems quickly.

Start Here: Getting Your Credit Reports and Spotting Errors

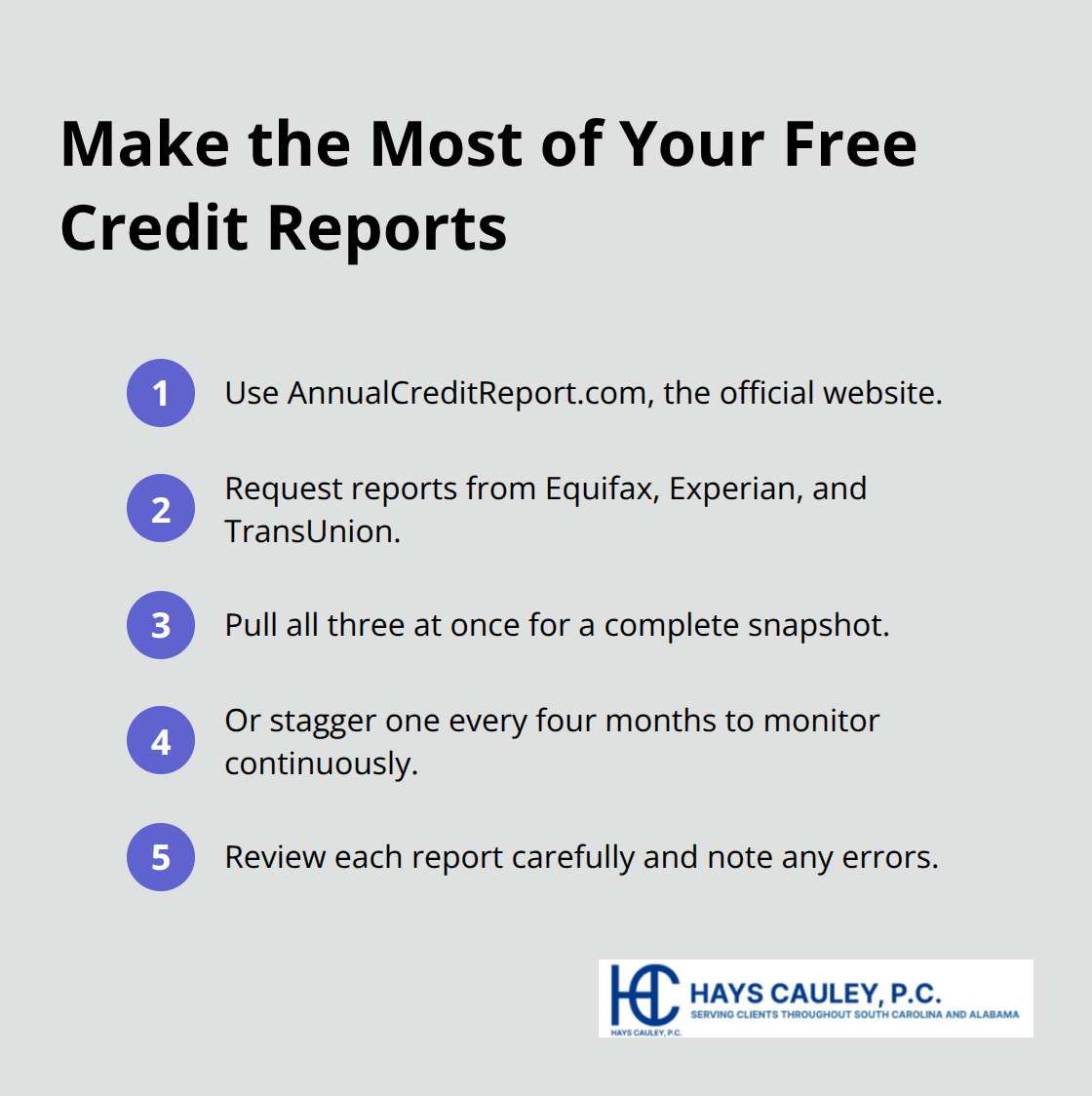

Request Your Free Annual Credit Reports

The Federal Trade Commission found that about one in five consumers have errors on their credit reports, yet most people never check. You can request your free annual credit reports from Equifax, Experian, and TransUnion through AnnualCreditReport.com, the official government website. Avoid other sites that claim to be free but actually charge fees or sign you up for paid services. You receive one free report per bureau each year, which means you can request all three at once or stagger them every four months to monitor your file continuously.

Identify the Three Most Common Errors

When your reports arrive, review them carefully for three common errors: late payments reported despite on-time payments, unauthorized accounts opened in your name, and incorrect balances or credit limits. Look for unfamiliar creditors, accounts you never opened, or personal information that doesn’t match your records. If you spot fraudulent accounts, that signals identity theft and requires immediate action beyond a standard dispute.

Document Everything You Find

Document everything you find by printing or saving copies of the error, noting the exact account name, account number, reported balance, and the inaccuracy. Gather supporting documentation before you file any dispute: bank statements showing on-time payments, account statements proving a balance discrepancy, or an identity theft report from the FTC if unauthorized accounts exist. Strong documentation dramatically improves your chances of success. The Consumer Financial Protection Bureau notes that disputes backed by specific documentation significantly improve investigation quality and outcomes, so don’t skip this step.

Build Your Paper Trail

Create a separate file for each error with copies of your evidence, your credit report pages showing the problem, and notes about when you discovered it. Keep originals for yourself and only send copies to the credit bureau or creditor. This paper trail protects you and proves you took the dispute seriously. With your documentation organized and ready, you can now move forward with filing your dispute directly with the credit bureau.

How to Dispute Errors on Your Credit Report: Serving South Carolina, including Greenville, Columbia and Charleston

Send Your Dispute in Writing to the Credit Bureau

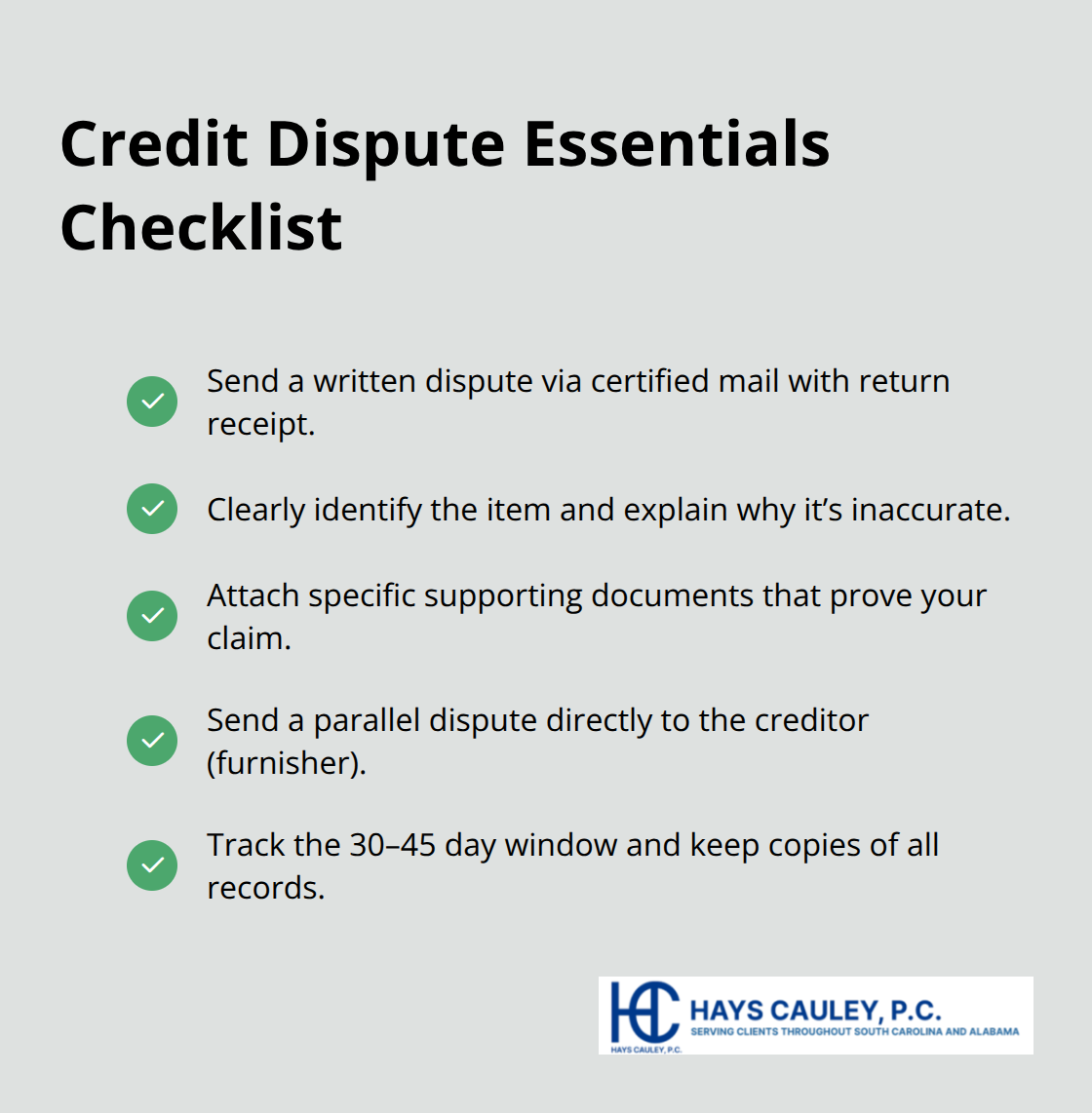

Filing a dispute directly with the credit bureau is your first move, and how you do it matters enormously. The FCRA requires bureaus to investigate within 30 days of receiving your dispute, but a weak dispute yields a weak investigation. Send your dispute in writing via certified mail with return receipt requested-this creates the paper trail that proves the bureau received it and activates your legal protections.

Phone disputes and online submissions lack this verification, leaving you vulnerable if the bureau claims they never received your request. Address your letter to the bureau’s dispute department, not general customer service, and include your name, address, account number, and the specific date you’re sending it.

Structure Your Dispute Letter for Maximum Impact

Identify the exact item you’re disputing, explain precisely why it’s inaccurate, reference your attached evidence, and request removal if the information remains unverified after investigation. Attach copies of your supporting documents-bank statements showing on-time payments, account statements proving balance errors, or FTC identity theft reports for fraudulent accounts. The Consumer Financial Protection Bureau emphasizes that disputes backed by specific documentation significantly improve investigation quality and outcomes, so the stronger your evidence package, the harder the bureau must work to verify the incorrect information.

Contact the Creditor Directly

Don’t stop after filing with the bureau. Send a separate dispute letter directly to the creditor or company reporting the inaccurate information, because they also have a duty to investigate under the FCRA. This dual approach forces both parties to examine the error independently. Include the same supporting documentation with your creditor letter to strengthen your position.

Track Your Timeline and Monitor Results

After mailing both disputes, track your timeline carefully: mark your calendar for 30 days from the certified mail receipt date, then check your credit report approximately 35 days later to confirm whether the item was removed or marked as disputed. Credit report corrections take 30 to 45 days from the moment you file your dispute, though identity theft cases or multiple errors can stretch longer. If the bureau insists the information is accurate despite your documented evidence, that may indicate an incomplete or improper investigation-a potential FCRA violation that justifies escalation or legal review. Keep copies of everything: your dispute letters, certified mail receipts, evidence packets, and all responses from the bureaus and creditors. Monitor your credit report every 30 days during this process using AnnualCreditReport.com, your free resource.

Know When to Seek Legal Assistance

If errors persist or the investigation appears inadequate, the violations you’ve documented may entitle you to remedies under federal law. A consumer protection law firm can review whether the bureau or creditor violated your FCRA rights and what options exist to hold them accountable. Understanding your legal standing under South Carolina and federal law strengthens your position significantly.

What Federal and South Carolina Law Guarantee You

The Fair Credit Reporting Act Protects Your Right to Challenge Errors

The Fair Credit Reporting Act forms your foundation for holding credit bureaus accountable. Under this federal law, you have the explicit right to dispute any information on your credit file, and the bureau must investigate your claim within 30 days of receiving it. If the bureau cannot verify the disputed item within that window, they must remove it entirely from your report. This is not a suggestion or a courtesy-it is a legal obligation. The FCRA also mandates that when a creditor or bureau takes adverse action against you based on your credit report, they must notify you in writing and provide you with a copy of the report they used. This notification requirement gives you the chance to identify errors before they cause real damage.

Furnishers Have Their Own Investigation Duties

Companies reporting data to bureaus (called furnishers) must investigate disputes you send them directly. Many people overlook this furnisher dispute route, but sending a detailed letter with supporting documentation directly to the creditor reporting the error often produces faster results than waiting for the bureau’s 30-day investigation. This dual-track approach forces both the bureau and the furnisher to examine the error independently, strengthening your position significantly.

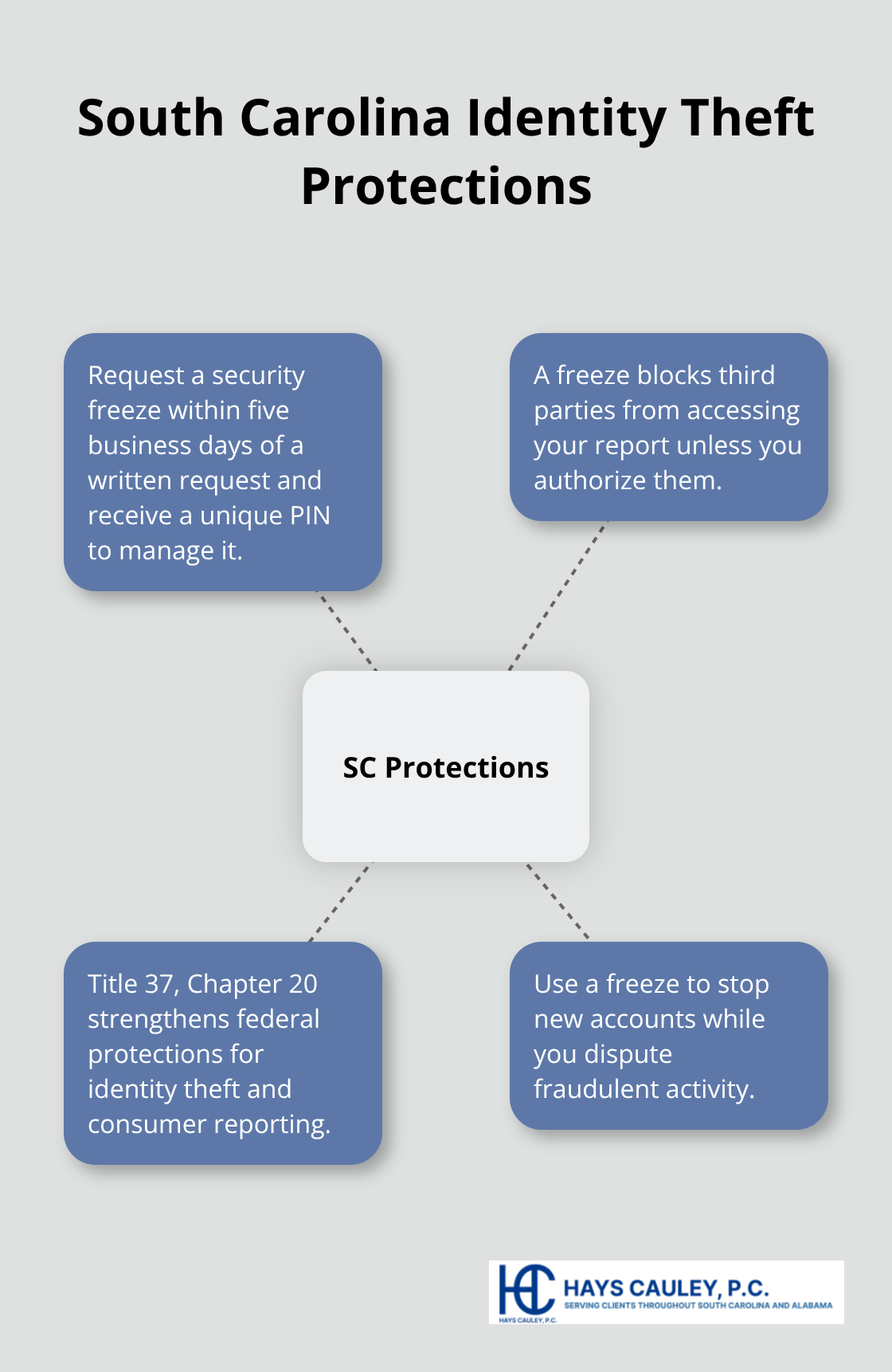

South Carolina Law Adds Powerful Protections for Identity Theft

South Carolina law strengthens federal protections further with Title 37, Chapter 20, which addresses identity theft and consumer reporting. If you discover fraudulent accounts or unauthorized activity, South Carolina law gives you the right to place a security freeze on your credit file within five business days of your written request, and you receive a unique PIN to manage it. This freeze blocks third parties from accessing your report entirely unless you authorize them, making it far harder for identity thieves to open new accounts in your name.

State Law Requires Notice Before Credit Reporting and Debt Collection

South Carolina also requires that creditors provide you with 20 days’ written notice before reporting a debt to a credit bureau or filing a lien, giving you time to cure the default. If a creditor violates disclosure requirements under federal Truth in Lending Act standards, you can recover actual damages plus up to twice the finance charge in penalties, plus attorney’s fees-a powerful incentive for lenders to get things right. Willful violations by lenders can even result in criminal penalties up to $5,000 in fines or one year in jail.

Courts Can Reject Unfair Debt Collection Practices

South Carolina courts have the authority to refuse enforcement of unconscionable debt collection practices or limit unfair terms, and they can award actual damages plus penalties when collectors engage in harassment or deception. These state-level remedies work alongside your federal FCRA rights, meaning you can pursue multiple avenues simultaneously if violations occur (and a consumer protection law firm like Hays Cauley, P.C. can help you understand which remedies apply to your situation).

Final Thoughts

Your SC reporting rights give you concrete tools to fix errors and protect your financial future. Willful FCRA violations result in three times your actual damages or at least $1,000 per incident plus attorney’s fees, while negligent violations yield actual damages or at least $1,000 per incident. South Carolina law adds its own penalties for disclosure violations and unconscionable debt collection practices, meaning multiple avenues exist to hold violators accountable.

If errors persist after you file disputes with both the bureau and the creditor, that signals a potential violation worth investigating. An incomplete investigation, a refusal to remove unverified information despite your documentation, or continued reporting of fraudulent accounts all suggest the bureau or creditor may have broken the law. Identity theft cases demand immediate action: file a police report, place a fraud alert or security freeze, and document everything the thief did in your name.

We at Hays Cauley, P.C. help South Carolina residents understand and enforce their credit reporting and identity theft rights. If your disputes stall, if you suspect violations, or if identity theft has damaged your file, contact us to discuss what remedies may apply to your situation.