Identity Theft Defense Attorney: Your Legal Protection

Identity theft affects millions of Americans each year, and the financial and emotional toll can be devastating. If criminals have stolen your personal information, you need immediate action and strong legal protection.

We at Hays Cauley, P.C. help victims navigate the complex process of reclaiming their identity and finances. An identity theft defense attorney can stop creditors from pursuing fraudulent debts and guide you toward full recovery.

How Criminals Steal Your Identity and What to Watch For

Criminals use surprisingly straightforward methods to access your personal information, and the Federal Trade Commission reported over 1.1 million identity theft cases in 2023 alone. Phishing emails and text messages remain the most effective attack vector because people routinely click malicious links without verifying the sender. Data breaches at retailers, financial institutions, and healthcare providers expose millions of Social Security numbers, credit card numbers, and bank account details annually. Card skimming devices installed on ATMs or gas pumps silently capture your card information during normal transactions. Public Wi-Fi networks at coffee shops and airports offer virtually no encryption, making it simple for criminals to intercept passwords and account credentials. Mail theft targets physical documents containing account numbers, tax information, and credit offers.

How Criminals Weaponize Stolen Information

Once criminals obtain your identifying information, they open fraudulent accounts, file false tax returns, or apply for employment using your name and Social Security number. South Carolina law recognizes two distinct crimes under SC Code § 16-13-510: financial identity fraud, which involves unauthorized use of your information to obtain money or property, and ordinary identity fraud, which covers using your information to secure employment or evade law enforcement. The penalties for these offenses carry serious consequences-imprisonment up to 10 years, discretionary fines, or both.

Red Flags Demand Your Immediate Attention

Unexpected charges on your bank or credit card statements represent the most obvious warning sign, but many victims miss subtler indicators. A sudden drop in your credit score without any action on your part signals fraudulent account openings or missed payments on accounts you never created. Receiving bills for services you never ordered (such as phone plans or utilities) means someone is actively using your identity. Collection calls for debts you do not recognize indicate that criminals have opened accounts in your name and defaulted on them. IRS notices of unfiled returns or duplicate returns mean someone filed a tax return using your Social Security number.

Credit denials with no clear reason often occur because fraudulent accounts have damaged your credit profile.

Take Action Within Days, Not Weeks

You should obtain your free annual credit report from each of the three major bureaus through annualcreditreport.com and scrutinize every account, address, and inquiry listed. Do not assume errors will resolve themselves; credit bureaus rely on you to dispute fraudulent entries, and South Carolina victims can contact the Identity Theft Unit at IDTheftHelp@scconsumer.gov or call 800-922-1594 for guidance. Delays allow criminals to cause additional damage and make recovery substantially more difficult. The moment you spot suspicious activity, your next step involves understanding your legal rights and how an attorney can stop creditors from pursuing fraudulent debts on your behalf.

What Laws Protect You and How an Attorney Stops the Abuse

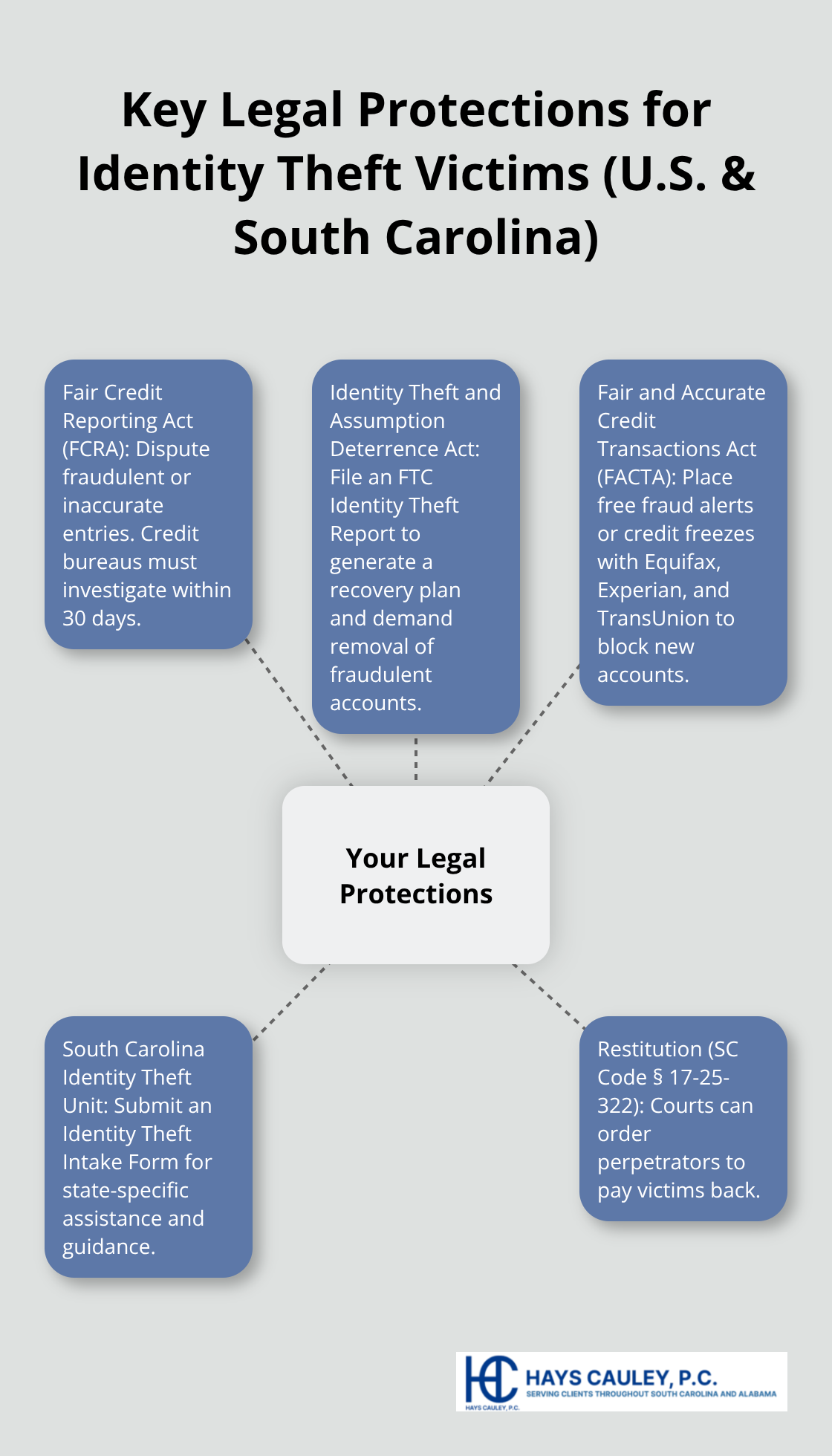

Federal law gives you powerful weapons against identity theft, and most victims never use them. The Fair Credit Reporting Act allows you to dispute any fraudulent account or inaccurate entry on your credit report, and credit bureaus must investigate your claim within 30 days under the law. The Identity Theft and Assumption Deterrence Act lets you file an Identity Theft Report with the Federal Trade Commission at identitytheft.gov, which generates a recovery plan and gives you legal standing to demand that creditors remove fraudulent accounts. The Fair and Accurate Credit Transactions Act entitles you to place a fraud alert or credit freeze with Equifax, Experian, and TransUnion at no cost, which blocks criminals from opening new accounts in your name.

South Carolina adds its own protections: victims can file an Identity Theft Intake Form with the South Carolina Department of Consumer Affairs Identity Theft Unit, and the state authorizes courts to order restitution from perpetrators under SC Code § 17-25-322.

The Real Cost of Inaction

Identity theft causes documented harm-victims in 2023 reported median losses of $500 to $1,000 per case according to the Federal Trade Commission, but many lose far more when fraudulent debts accumulate. Delays in asserting your rights allow criminals to cause additional damage and make recovery substantially more difficult. The laws exist specifically to protect you, yet most victims fail to leverage them effectively without legal guidance.

How Attorneys Stop Creditor Harassment

An identity theft attorney stops the harassment immediately by contacting creditors and collection agencies on your behalf, which forces them to cease collection efforts on fraudulent accounts under the Fair Debt Collection Practices Act. Creditors routinely pursue victims for debts opened by criminals because they assume the victim authorized the account; an attorney shifts the burden back to them and makes them prove otherwise. Disputing errors yourself often fails because creditors ignore individual complaints, but a letter from a law firm commanding compliance with federal law produces results. When creditors ignore cease-and-desist letters or continue calling after being notified of identity theft, an attorney files complaints with state regulators and pursues damages for harassment.

Coordinating Your Recovery Strategy

An attorney works directly with credit bureaus to remove fraudulent entries and demands that creditors prove the debt belongs to you-most cannot. An attorney also coordinates with the Identity Theft Unit at IDTheftHelp@scconsumer.gov or 800-922-1594 to access South Carolina-specific resources and ensures you file proper documentation to support your recovery claim. This coordination removes the burden of fighting creditors alone and holds negligent parties accountable. With your legal rights now established and creditors stopped in their tracks, the next step involves the practical work of restoring your credit and monitoring your accounts to prevent future fraud.

Restoring Your Credit After Identity Theft: Serving South Carolina, including Greenville, Columbia and Charleston

Credit bureaus will not fix fraudulent entries on their own, no matter how obvious the fraud appears. You must dispute each fraudulent account directly with Equifax, Experian, and TransUnion, and the Fair Credit Reporting Act requires these bureaus to investigate your dispute within 30 days and remove any item they cannot verify. Start by obtaining your three free credit reports from annualcreditreport.com and identify every fraudulent account, inquiry, and negative mark created by the thief.

Submit Disputes with Specific Documentation

When you submit disputes, provide specific details about why each entry is fraudulent rather than vague statements. Include copies of police reports, identity theft reports from identitytheft.gov, or correspondence from creditors acknowledging the fraud. Credit bureaus often reject disputes that lack supporting documentation, so attach everything you have.

Send your dispute letters via certified mail with return receipt requested so you have proof of delivery. The South Carolina Department of Consumer Affairs Identity Theft Unit at IDTheftHelp@scconsumer.gov or 800-922-1594 can provide sample dispute letters and guidance on which documentation carries the most weight with the major bureaus. Many victims make the mistake of disputing only with the credit bureaus and ignoring the creditors themselves; you must also contact each creditor in writing and demand they remove the fraudulent account, citing the Fair Credit Reporting Act and providing your identity theft documentation.

Monitor Your Credit Throughout the Year

Checking your credit report once per year is insufficient protection after identity theft. Instead, obtain your three free annual reports and stagger them throughout the year by pulling one report every four months from annualcreditreport.com so you monitor your credit continuously. Consider placing a fraud alert with all three bureaus, which forces creditors to verify your identity before opening new accounts, or opt for a credit freeze, which blocks all access to your credit file unless you temporarily lift it.

The Federal Trade Commission reported that fraud alerts and freezes stop approximately 90 percent of new account fraud because criminals cannot open accounts without accessing your credit file. Many victims also monitor their credit with free services like Credit Karma or Credit Sesame, which alert you to new accounts and inquiries in real time rather than waiting months to discover fraud on your annual report.

Additionally, set up account alerts with your banks and credit card issuers so you receive notifications of logins, large transfers, or password changes. Review your bank and credit card statements weekly, not monthly, because criminals often make small test charges before committing larger fraud; catching these early prevents substantial losses.

Organize Documentation Chronologically

Every communication you receive regarding fraudulent accounts should be saved permanently, including bills, collection letters, credit bureau responses, and creditor correspondence. Create a dedicated folder (either physical or digital) and organize documents chronologically so you can quickly reference them if creditors continue pursuing fraudulent debts or if you need to escalate disputes with regulators.

Document every phone call with creditors by noting the date, time, the person’s name, and exactly what was discussed; follow up with written confirmation emails stating that you discussed identity theft and the account in question. When creditors violate the Fair Debt Collection Practices Act by calling after you have notified them of identity theft, document these violations with dates and times because they create grounds for legal action. The Federal Trade Commission requires creditors to maintain records showing they investigated your dispute, so request these investigation files in writing and save them as proof that the creditor failed to conduct a proper investigation.

Create a Master Spreadsheet for Tracking

Create a spreadsheet listing each fraudulent account, the date you discovered it, the creditor’s name, the date you disputed it with the credit bureau, the date you contacted the creditor directly, and the current status of removal or resolution. This documentation protects you from creditors who falsely claim they never received your dispute letters and provides evidence if you need to file complaints with state regulators or pursue legal action against creditors who continue harassing you after being notified of the fraud (especially when they violate federal debt collection laws).

Final Thoughts

Identity theft recovery demands more than disputing credit reports and monitoring accounts-it requires an identity theft defense attorney fighting on your behalf to stop creditors, hold negligent parties accountable, and restore your financial stability. We at Hays Cauley, P.C. understand the frustration victims face when creditors ignore disputes or collection agencies continue calling despite proof of fraud. Our consumer protection law firm helps victims with credit reporting, identity theft, and debt-related issues by coordinating directly with creditors, credit bureaus, and regulators to remove fraudulent entries and stop harassment.

An identity theft defense attorney shifts the burden from you to the parties responsible for the fraud. Creditors take letters from law firms seriously because they understand the legal consequences of violating federal debt collection laws. When you contact creditors alone, they often ignore your complaints or demand proof you cannot easily provide, but an attorney demands they prove the debt belongs to you-and most cannot.

The long-term benefits of legal protection extend far beyond stopping immediate harassment. We ensure you file proper documentation with the South Carolina Department of Consumer Affairs Identity Theft Unit and coordinate with all three credit bureaus simultaneously rather than you fighting them individually. Contact Hays Cauley, P.C. today to discuss your identity theft case and learn how legal protection can restore your credit and your peace of mind.