Financial identity theft affects millions of Americans each year, and the consequences can be devastating. Your personal financial information is a target for criminals who want to open accounts, make purchases, or drain your savings in your name.

At Hays Cauley, P.C., we’ve helped clients navigate the aftermath of identity theft, and we know how stressful it can be. This guide walks you through prevention strategies, warning signs to watch for, and exactly what to do if you become a victim.

How Criminals Steal Your Financial Identity – Serving South Carolina, including Greenville, Columbia and Charleston

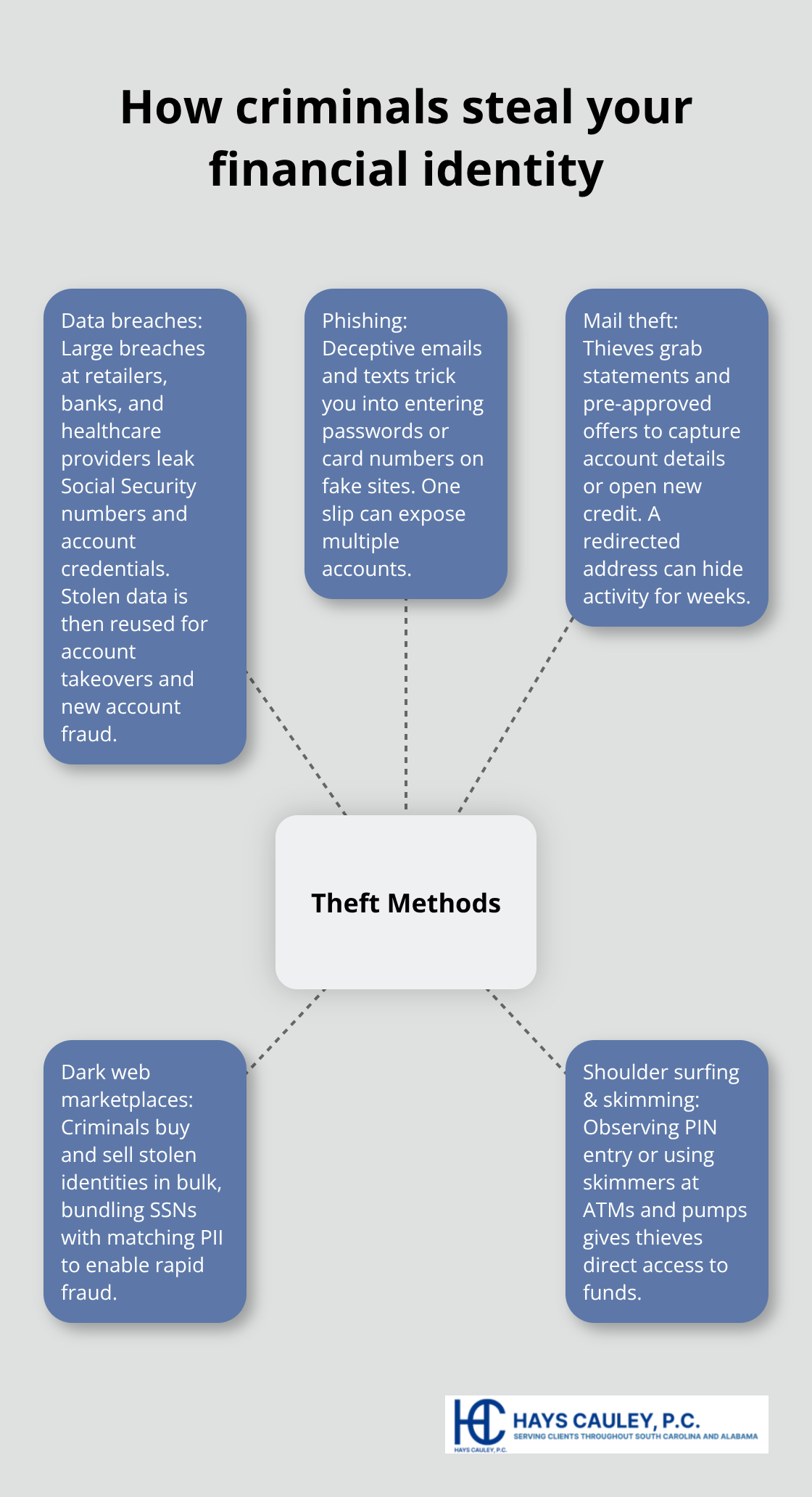

Financial identity theft occurs when someone uses your personal information to commit fraud in your name. The Federal Trade Commission identifies this as the unauthorized use of your Social Security number, bank account numbers, credit card information, or tax refunds to open accounts, make purchases, or drain your savings. Criminals obtain this information through data breaches at retailers, banks, and healthcare providers, which remain the primary source of stolen personal information used for financial fraud according to the FBI. Other common methods include phishing emails that trick you into sharing credentials, stealing physical mail to access account statements or pre-approved credit offers, purchasing stolen data from dark web marketplaces, or simply observing you enter a PIN at a store. Your information holds significant value, and thieves persist in finding ways to access it.

Red Flags That Signal Identity Theft

The signs of identity theft often appear in your financial statements before you realize something is wrong. Unfamiliar charges on your credit card or bank account, missing bills that should have arrived, redirected mail due to an address change you didn’t authorize, and new credit accounts you never opened are the most obvious warnings. The FTC recommends regularly reviewing your statements and credit reports to catch fraud early, which is why checking your free annual credit reports from Equifax, Experian, and TransUnion matters so much.

If your tax refund is delayed or you receive an IRS notice about income you didn’t earn, tax-related identity theft may have occurred. One particularly deceptive trend is synthetic identity theft, where criminals combine your real Social Security number with fabricated information to create entirely new fraudulent accounts, making detection significantly harder than traditional theft.

Respond Immediately to Suspicious Activity

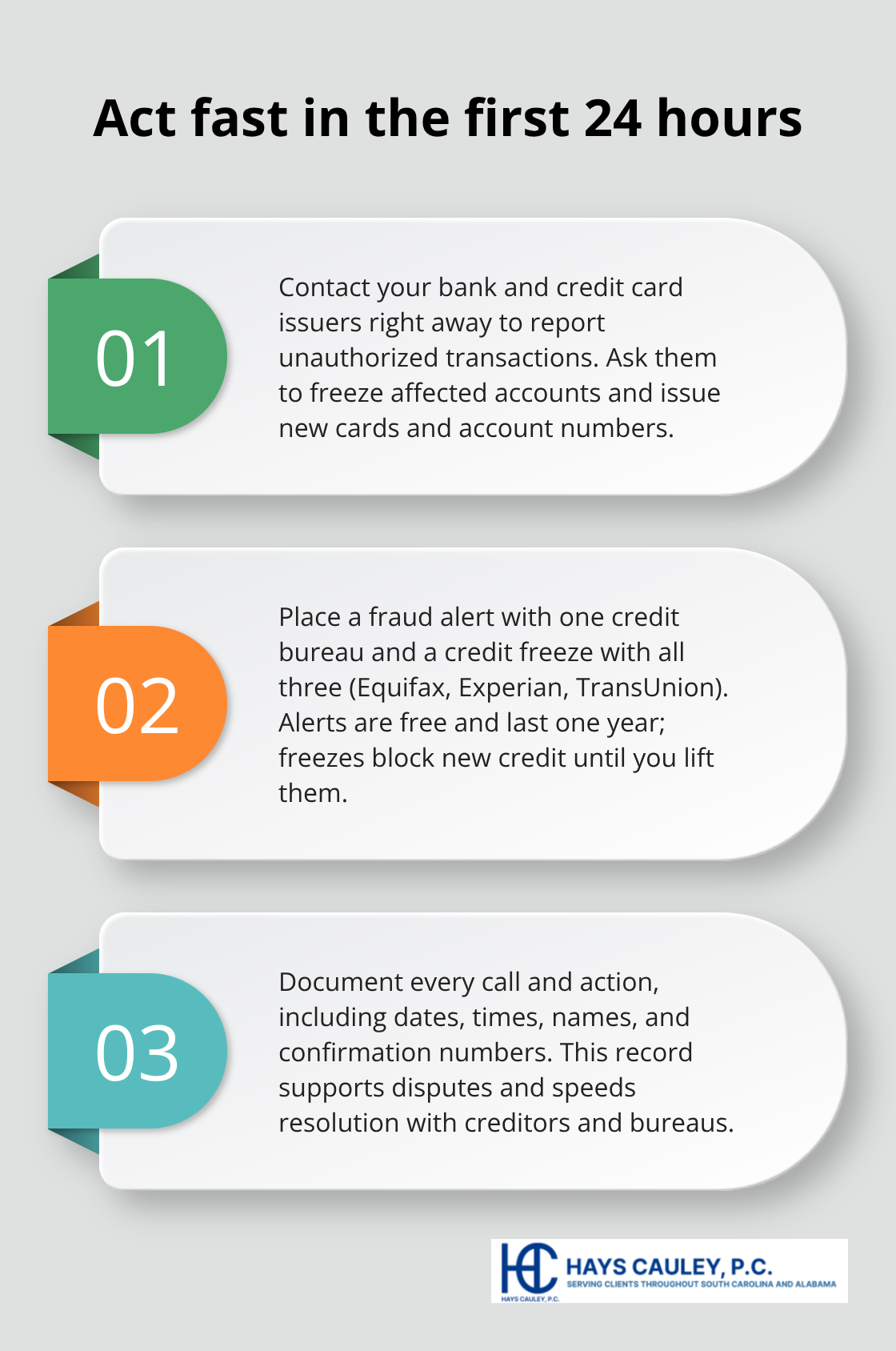

The first 24 hours after discovering suspicious activity are critical. Contact your bank and credit card companies immediately to report unauthorized transactions and request account freezes or new cards. Place a fraud alert with at least one of the three credit bureaus, which requires creditors to verify your identity before opening new accounts and is valid for one year at no cost. Then place a credit freeze with all three bureaus to prevent new lines of credit from being opened in your name without your explicit permission. These freezes and fraud alerts are free, and you can manage them by contacting Equifax, Experian, and TransUnion directly. Document everything you do (including dates, times, and names of people you speak with) because this record becomes essential if disputes arise later.

Understanding Your Next Steps

Once you’ve taken immediate action, the path forward involves filing an official report and working with your creditors to resolve fraudulent accounts. The Federal Trade Commission provides a personalized recovery plan through its Identity Theft Report system, which guides you through 30+ types of identity theft scenarios with pre-filled letters and forms. This structured approach helps you contact creditors, dispute fraudulent charges, and track your progress as you reclaim your identity. Your financial institutions and credit bureaus play a role in this recovery, and understanding how to work with them effectively accelerates the resolution process.

How to Stop Identity Theft Before It Starts – Serving South Carolina, including Greenville, Columbia and Charleston

Your credit reports form the frontline defense against financial identity theft, yet most Americans never check them. The FTC data shows you’re entitled to one free credit report annually from each of the three major bureaus-Equifax, Experian, and TransUnion-through AnnualCreditReport.com or by calling 1-877-322-8228. Space these requests strategically (one every four months) to gain ongoing monitoring at zero cost without paying $44 to over $100 per year for commercial monitoring services. When you review these reports, look specifically for unfamiliar accounts, unauthorized inquiries, address changes you didn’t authorize, and suspicious personal information. This matters because synthetic identity theft-where criminals blend your real Social Security number with fabricated details-creates accounts that traditional monitoring might miss. Simultaneously, review your bank and credit card statements the moment they arrive. Criminals don’t always target your existing accounts; they often open new ones in your name, so spotting unfamiliar charges immediately stops fraud in its tracks. If your physical mail stops arriving on schedule, contact your bank and postal carrier immediately because address changes are a common tactic thieves use to hide fraudulent activity.

Stop Pre-Approved Credit Offers at the Source

Thieves still steal mail containing pre-approved credit offers and account statements, which is why you should call 1-888-567-8688 or visit OptOutPrescreen.com to stop receiving these offers entirely. This single action removes your name from marketing lists and reduces the mail theft risk significantly. Store documents containing Social Security numbers, bank account information, and tax records in a locked location, and shred sensitive documents before disposal rather than tossing them whole into the trash. When businesses request your Social Security number, ask why they need it, how they’ll protect it, and whether an alternative identifier works instead-many companies will accommodate this request.

Strengthen Your Digital Defenses

For your digital life, use unique passwords for every financial account and make each one at least eight characters long with a mix of letters, numbers, and symbols. Never reuse passwords across accounts because a breach at one retailer can give thieves access to your bank account if you’ve used the same credentials. Enable two-factor or multi-factor authentication on every financial account you maintain, which requires something you know (a password), something you have (your phone), or something you are (your fingerprint). Authenticator apps like Google Authenticator or Microsoft Authenticator provide stronger protection than SMS text codes, which criminals can intercept through SIM-swap fraud.

Choose the Right Payment Method

For online shopping, use credit cards rather than debit cards because credit card fraud protections under the Fair Credit Billing Act are stronger than debit card protections, making disputes and chargebacks significantly easier to resolve. This distinction matters when thieves gain access to your payment information. The next step involves taking action if you suspect your information has already been compromised, which requires understanding the specific tools available to lock down your credit and prevent new fraudulent accounts.

What to Do Right Now If You’re a Victim – Serving South Carolina, including Greenville, Columbia and Charleston

The moment you suspect identity theft, speed matters more than perfection. Contact your bank and credit card companies within hours, not days, to report unauthorized transactions and freeze accounts. Most major banks have fraud departments available 24/7, and many halt suspicious activity within minutes. Request new account numbers and cards immediately. Simultaneously, place a fraud alert with one of the three credit bureaus-Equifax, Experian, or TransUnion-by phone or online.

This alert is free, lasts one year, and forces creditors to verify your identity before approving new credit in your name.

Lock Down Your Credit File

Place a credit freeze with all three bureaus to block access to your credit file entirely, preventing thieves from opening new accounts without your consent. Freezes are permanent until you lift them and cost nothing. Document everything during these calls: dates, times, names of representatives, confirmation numbers, and what was discussed. This documentation becomes your evidence trail if disputes arise later. Gather copies of fraudulent statements, unauthorized account letters, and any correspondence from creditors about accounts you didn’t open. Store these documents securely because you’ll reference them repeatedly during recovery.

File Your Identity Theft Report

File an Identity Theft Report through the Federal Trade Commission at IdentityTheft.gov, which generates a personalized recovery plan tailored to your specific situation. This report covers over 30 types of identity theft scenarios and includes pre-filled letters you can send to creditors, banks, and bureaus to dispute fraudulent accounts and demand removal of false information. The FTC provides step-by-step guidance, and you can track your progress as you work through each action item.

Address Tax and Social Security Fraud

For tax-related identity theft specifically, file Form 14039 Identity Theft Affidavit with the IRS and contact their Identity Theft Central hotline. If your Social Security number was compromised, contact the Social Security Administration to review your earnings record for fraudulent income. These steps protect your tax refunds and prevent criminals from claiming benefits in your name.

Dispute Fraudulent Accounts

Contact each financial institution where fraudulent accounts were opened to dispute charges and demand account closure. Most banks have specific fraud dispute procedures, and federal law requires them to investigate within 30 days. Provide them with your FTC Identity Theft Report as evidence. Throughout this process, obtain free copies of your credit reports from all three bureaus through AnnualCreditReport.com to verify that fraudulent accounts are being removed and to spot any remaining unauthorized activity you missed initially.

Final Thoughts

Financial identity theft recovery takes time, but the steps outlined in this guide provide a clear path forward. Prevention remains your strongest defense: monitor your credit reports quarterly using free annual access, secure your documents and devices, use unique passwords with two-factor authentication, and freeze your credit proactively even before a breach occurs. If theft happens, act within 24 hours by contacting your bank, placing fraud alerts, and filing an FTC Identity Theft Report that generates a personalized recovery plan covering your specific situation.

The resources available to you are substantial and free. AnnualCreditReport.com gives you access to all three credit reports annually, IdentityTheft.gov provides step-by-step recovery guidance, and the FTC’s hotline offers support throughout your recovery. Contact Equifax, Experian, and TransUnion directly to place freezes and fraud alerts at no cost. For tax-related theft, the IRS Identity Theft Central and Form 14039 protect your refunds and earnings record.

Recovery from financial identity theft is achievable, but the process involves multiple steps and persistent follow-up with creditors and bureaus. Many victims find the experience overwhelming, which is why professional guidance matters-at Hays Cauley, P.C., we help consumers navigate credit reporting, identity theft, and related issues when the recovery process becomes complex or creditors resist your legitimate disputes. Contact us if you’re struggling with fraudulent accounts, unresponsive creditors, or unclear next steps.