Identity theft protection cost varies wildly depending on what you actually need. Some plans run just a few dollars monthly, while others charge significantly more for premium features.

At Hays Cauley, P.C., we’ve seen firsthand how confusing these pricing structures can be. This guide breaks down what you’ll really pay and helps you figure out which plan makes sense for your situation.

Average Costs of Identity Theft Protection Services

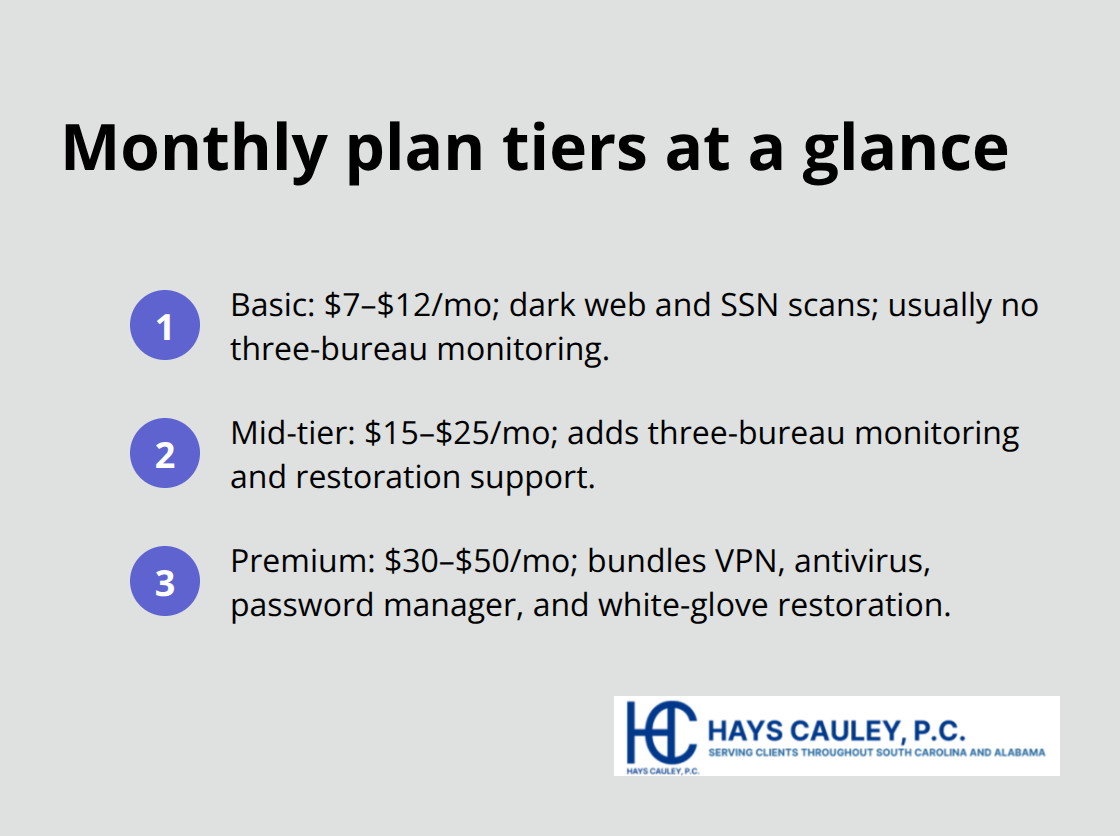

What You’ll Actually Pay Monthly

Basic identity theft protection plans start around $7 to $12 per month, with Surfshark Alert sitting at the budget end around $2.19 monthly and Zander offering Essential plans near $7 per month. These stripped-down options typically include dark web monitoring and SSN scanning, but they often lack the three-bureau credit monitoring that catches fraud across Equifax, TransUnion, and Experian simultaneously. Mid-tier plans from providers like IdentityForce, IdentityGuard, and Identity Guard range from $15 to $25 monthly and add three-bureau coverage plus restoration support. Premium plans push toward $30 to $50 monthly and bundle in extras like VPNs, antivirus software, password managers, and white-glove restoration services where a dedicated fraud specialist handles your recovery. Aura’s individual plan costs around $15 monthly with three-bureau monitoring included, while their family plan covering up to five adults and unlimited children runs $50 monthly-a practical option if you’re protecting multiple household members.

LifeLock pairs its protection with Norton 360 cybersecurity, pricing individual plans from about $12 monthly upward, though bundling requirements can inflate costs if you want full antivirus and VPN access.

Annual Plans Beat Monthly Pricing

Switching to annual billing typically saves 20 to 40 percent compared to month-to-month commitments. IdentityForce individual annual plans run around $200 to $350 yearly versus $20 to $35 monthly, while family plans drop to $250 to $400 annually. The average identity theft victim lost $9,800 in 2024, with out-of-pocket expenses averaging $3,500 per person-making annual prepayment a calculated investment rather than an expense. Aura offers first-year discounts that drop individual pricing significantly below standard rates, making the initial commitment more attractive. Most providers publish annual rates clearly on their websites, so comparing the total yearly cost rather than just monthly fees prevents surprises and reveals genuine value.

What Happens When You Add Extra Features

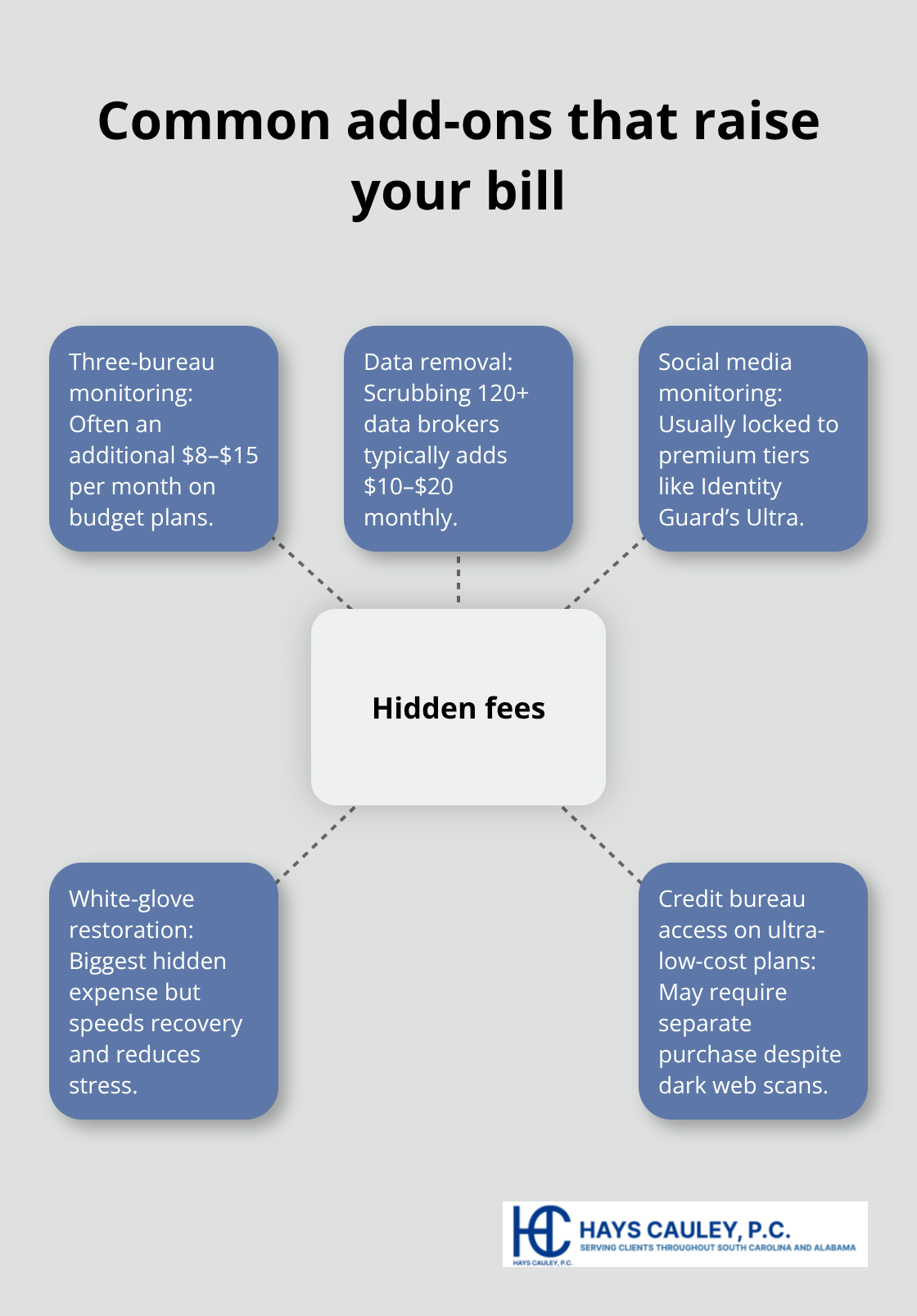

Many providers charge additional fees for features that sound included but actually require upgrades. Data removal services (removing your information from 120+ data brokers) add value but often cost extra on base plans. Social media monitoring, available on Identity Guard’s Ultra tier, monitors your accounts for unauthorized access and suspicious activity. White-glove restoration services-where a dedicated specialist guides you through recovery after fraud occurs-typically appear only on premium tiers and justify higher monthly costs through faster resolution and reduced stress during an incident.

Family Plans Change the Equation

Protecting multiple household members shifts your cost calculation significantly. Aura’s family plan covers five adults and unlimited children for $50 monthly, while IdentityGuard’s family option extends to five adults and unlimited children at comparable pricing. These plans often include parental controls and cyberbullying protection for minors, adding layers of protection that individual plans cannot match. When you calculate cost per person across a family of four or five, monthly fees drop substantially compared to purchasing separate individual subscriptions.

Understanding the Real Price You Pay

The lowest-cost options (under $10 monthly) typically omit three-bureau credit monitoring, meaning fraud on one bureau might slip past your alerts. Mid-range plans ($15–$25 monthly) deliver the monitoring most people actually need plus restoration support. Premium tiers ($30–$50 monthly) add cybersecurity tools and white-glove service that reduce your burden if theft occurs. Your actual cost depends on whether you need family coverage, how many data brokers concern you, and whether you want bundled cybersecurity tools-not just the advertised monthly price.

What Hidden Fees Actually Cost You

The True Price Behind Advertised Monthly Rates

The advertised monthly price tells only part of the story. Many identity theft protection services charge separate fees for features that sound bundled but require paid upgrades. Three-bureau credit monitoring, which tracks your accounts across Equifax, TransUnion, and Experian simultaneously, costs extra on budget plans under $10 monthly. Surfshark Alert at $2.19 monthly provides dark web monitoring and basic scanning but requires you to pay separately for actual credit bureau access. When you add three-bureau monitoring to a basic plan, you’re often looking at an additional $8 to $15 monthly, effectively doubling your initial cost.

Add-Ons That Inflate Your Bill

Data removal services that scrub your information from 120 or more data brokers typically run $10 to $20 extra monthly on most platforms. Social media monitoring, which alerts you to unauthorized access on your accounts, appears only on premium tiers like Identity Guard’s Ultra plan and costs substantially more than base coverage. White-glove restoration services, where a dedicated fraud specialist handles your recovery after identity theft occurs, represent the biggest hidden expense but also deliver measurable value through faster resolution and reduced personal stress during an incident.

Calculating Your Actual Annual Spending

The real expense emerges when you calculate total annual cost including all necessary add-ons. A plan advertised at $15 monthly becomes $240 yearly, but adding three-bureau monitoring ($12 extra), data removal ($15 extra), and restoration support ($10 extra) pushes actual annual spending to $612 before taxes. IdentityForce charges $20 to $35 monthly for individual plans, but their pricing includes up to $2 million in identity theft insurance and restoration support from the start, eliminating surprise fees later. This approach costs more upfront but prevents the sticker-shock experience of discovering essential features require additional payments.

Family Coverage and Per-Member Restrictions

Family plans create different hidden cost dynamics because adding coverage for spouses and children sometimes triggers per-person insurance limits or reduces total coverage. Aura’s family plan covers five adults and unlimited children for $50 monthly without per-member restrictions, while other providers cap dependents or require higher tiers for full family protection. The average identity theft victim spends roughly $3,500 out-of-pocket on recovery, making comprehensive plans with included restoration services a smarter financial decision than budget options that nickel-and-dime you during crises.

Making an Informed Comparison

Before committing to any plan, calculate your true monthly cost by adding all necessary features, then compare that total against competitors offering those same features included in their base price. Experian IdentityWorks splits its offering into free and paid tiers, with the free version supported by ads and lacking online security tools-a pattern that repeats across the industry. The providers that bundle restoration support, three-bureau monitoring, and insurance coverage into their base price often deliver better value than those that charge separately for each component, even if the initial monthly rate appears higher. Understanding what each provider includes versus what they charge extra for transforms your decision from sticker-price shopping into genuine cost comparison.

How to Choose the Right Identity Theft Protection Plan

Match Your Specific Threats to Provider Coverage

Choosing an identity theft protection plan requires matching your specific threats against what providers actually deliver, not comparing advertised prices or feature lists that sound identical across competitors. Start by identifying which type of fraud poses the greatest risk to you personally. Credit card fraud accounts for the majority of identity theft cases, with the FTC recording roughly 2.8 million credit card fraud incidents in 2021, making three-bureau credit monitoring non-negotiable if you carry multiple cards or shop online frequently. Tax-related identity theft and bank fraud represent smaller but more devastating threats, particularly around tax season when criminals file returns using stolen SSNs. Medical identity theft and loan fraud affect fewer people but carry higher average losses per victim. Once you know your primary risk, filter providers by whether they actually cover that specific threat adequately rather than assuming all plans protect against everything equally.

Evaluate What You Actually Need Versus Marketing Claims

Calculate what you genuinely need versus what marketing departments want you to purchase. IdentityForce includes up to $2 million in identity theft insurance and restoration support in their base plans starting at $20 to $35 monthly, while Aura covers five adults and unlimited children for $50 monthly with three-bureau monitoring and VPN included from day one. Compare these against providers that advertise lower monthly rates but require separate payments for three-bureau monitoring, data removal, or restoration services. A provider offering exceptional white-glove restoration means little if their credit monitoring only tracks one bureau instead of all three, leaving gaps where fraud slips through undetected. The Federal Trade Commission emphasizes that permanent access to free weekly credit reports provides ongoing value, which means any plan should complement your own credit monitoring habits rather than replace personal vigilance entirely.

Verify Coverage for Your Household Members

If you have children at home, verify whether your provider covers minors without per-child insurance caps or coverage restrictions, since child identity theft grows annually and requires different monitoring than adult accounts. Families with five or more members find per-person pricing cheaper through Aura’s unlimited children model than purchasing individual subscriptions separately. Family plans create different cost dynamics because adding coverage for spouses and children sometimes triggers per-person insurance limits or reduces total coverage. Aura’s family plan covers five adults and unlimited children for $50 monthly without per-member restrictions, while other providers cap dependents or require higher tiers for full family protection.

Test Provider Responsiveness Before Committing

Test a provider’s actual responsiveness before committing to annual billing by examining whether they offer a money-back guarantee or trial period, since 24/7 support quality varies dramatically between companies and matters intensely when fraud actually occurs in your accounts. Many providers publish annual rates clearly on their websites, so comparing the total yearly cost rather than just monthly fees prevents surprises and reveals genuine value.

The average identity theft victim spends roughly $3,500 out-of-pocket on recovery, making comprehensive plans with included restoration services a smarter financial decision than budget options that nickel-and-dime you during crises. Before committing to any plan, contact your bank and credit card companies and place a fraud alert on your credit reports to protect yourself during the selection process, then calculate your true monthly cost by adding all necessary features and compare that total against competitors offering those same features included in their base price.

Final Thoughts

Identity theft protection cost ultimately depends on matching what you actually need against what providers charge. Budget plans under $10 monthly save money upfront but leave gaps in coverage that expose you to fraud, while mid-range plans between $15 and $25 monthly deliver three-bureau credit monitoring and restoration support that most people genuinely need. The average identity theft victim loses roughly $3,500 out-of-pocket on recovery expenses, making comprehensive plans with included restoration services far cheaper than budget options that charge separately for essential features when fraud actually happens.

Annual billing typically saves 20 to 40 percent compared to month-to-month commitments, and family coverage changes your cost equation significantly since protecting multiple household members through plans covering five adults and unlimited children costs less per person than purchasing individual subscriptions separately. Parents with children at home should verify whether their provider covers minors without per-child insurance caps, since child identity theft requires different monitoring than adult accounts. Before committing to any plan, calculate your true monthly cost by adding all necessary features, then compare that total against competitors offering those same features included in their base price.

Test a provider’s responsiveness through their money-back guarantee or trial period, since 24/7 support quality varies dramatically and matters intensely when fraud actually occurs in your accounts. If you’re dealing with identity theft or credit reporting issues, we at Hays Cauley, P.C. help consumers navigate credit reporting, identity theft, and debt-related problems. The right protection plan paired with professional guidance gives you the strongest defense against fraud.