Errors on your credit report can damage your financial standing and limit your access to loans, housing, and employment opportunities. A well-written Fair Credit Reporting Act dispute letter gives you the power to challenge these inaccuracies directly with credit bureaus.

We at Hays Cauley, P.C. have seen how proper dispute letters can restore credit scores and open doors for South Carolina residents. This guide walks you through creating an effective dispute letter that gets results.

What Rights Does the Fair Credit Reporting Act Give You

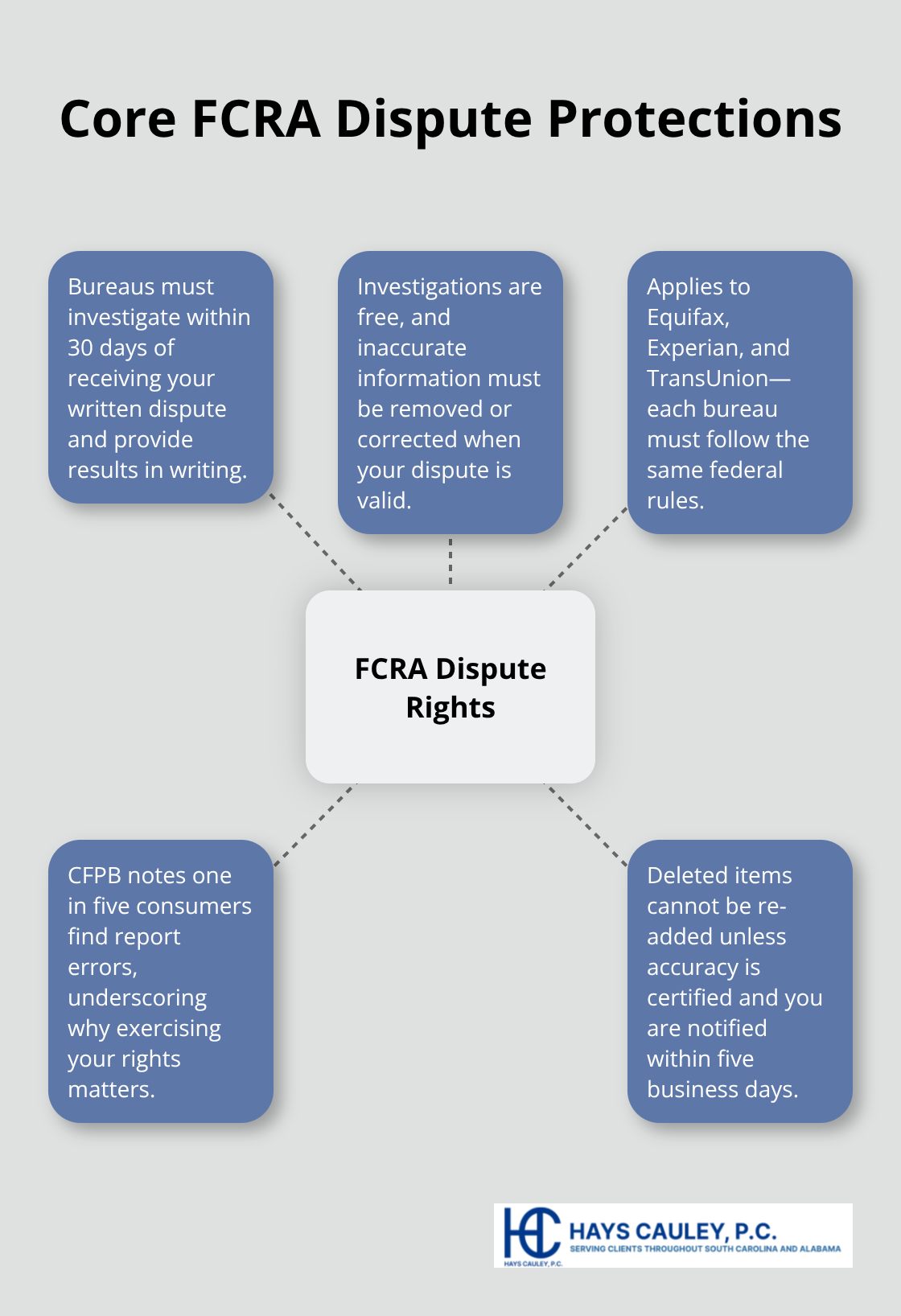

The Fair Credit Reporting Act provides South Carolina consumers with powerful tools to fight credit report errors. This federal law requires credit bureaus (Equifax, Experian, and TransUnion) to investigate disputes within 30 days after they receive your written request. The Consumer Financial Protection Bureau reports that one in five consumers find errors on their credit reports, which makes your dispute rights more valuable than ever. The FCRA mandates that credit bureaus provide free investigations and must remove or correct inaccurate information when your dispute proves valid.

Your Dispute Rights Cover More Than You Realize

Credit bureaus must accept disputes about any information you believe is inaccurate, incomplete, or unverifiable. This includes incorrect payment histories, accounts that don’t belong to you, wrong balances, and outdated negative information. The Federal Trade Commission confirms that you can dispute the same item multiple times if you have new evidence. Credit bureaus cannot charge fees for dispute investigations, and they must notify the data furnisher within five business days after they receive your dispute.

The 30-Day Investigation Timeline Protects You

Once credit bureaus receive your dispute letter, they have exactly 30 days to complete their investigation and respond to you. If they fail to meet this deadline, the disputed information must disappear from your report immediately. The FCRA requires credit bureaus to provide you with written results of their investigation, plus a free copy of your updated credit report if changes were made. This strict timeline forces credit bureaus to act quickly on legitimate disputes.

When Credit Bureaus Must Delete Information Permanently

Credit bureaus must permanently remove disputed information if the data furnisher cannot verify its accuracy within the investigation period. The FCRA prohibits credit bureaus from re-adding previously deleted information unless the data furnisher certifies its accuracy and notifies you within five business days. This protection stops credit bureaus from manipulating your credit report after successful disputes.

Now that you understand your rights under the FCRA, you need to know exactly what information to include in your dispute letter to maximize your chances of success.

What Must Your Dispute Letter Include

Your dispute letter needs five critical components to trigger a proper FCRA investigation. Start with your complete personal information: full legal name, current address, Social Security number, and date of birth. Credit bureaus receive thousands of disputes daily, and incomplete identification information gives them an excuse to reject your letter immediately. The Federal Trade Commission emphasizes that proper identification prevents delays and strengthens your dispute rights. Include your phone number and email address so credit bureaus can contact you if they need clarification during their investigation.

Your Letter Must Identify Each Disputed Item Precisely

List each disputed item with specific account numbers, creditor names, and the exact information you challenge. Vague complaints like “this account is wrong” fail to meet FCRA requirements and lead to generic responses that don’t fix your credit report. The Consumer Financial Protection Bureau found that disputes with specific details get resolved 40% faster than general complaints. Clearly identify each error, explain the inaccuracy, and request its removal or correction. Attach copies of your credit report with disputed items circled or highlighted to eliminate any confusion about which information you challenge.

Documentation Transforms Weak Disputes Into Strong Cases

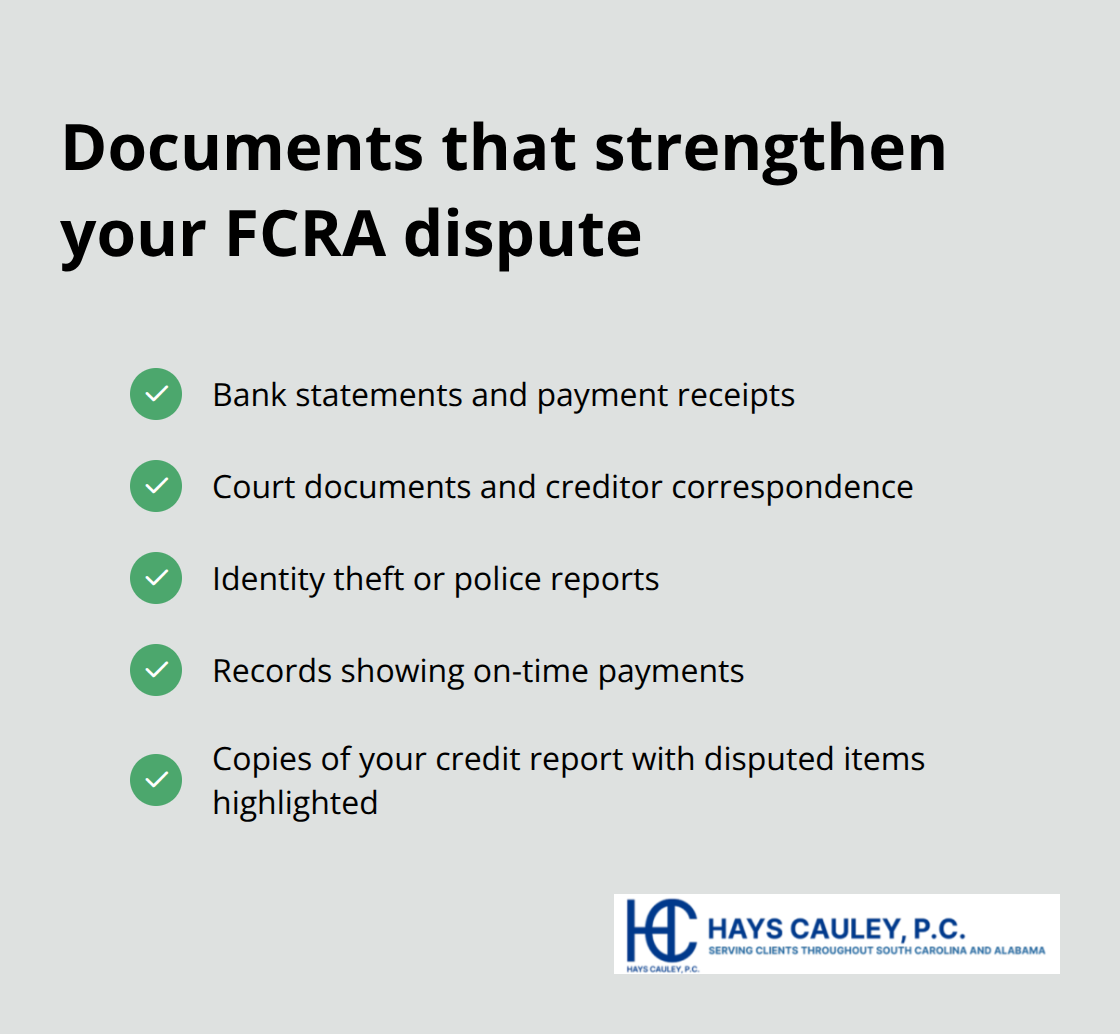

Send copies of bank statements, payment receipts, court documents, or correspondence with creditors that prove your position. Original documents stay with you while copies go to the credit bureau with your dispute letter. The FCRA requires credit bureaus to consider all relevant information you provide during their investigation.

Payment records that show on-time payments can eliminate late payment marks, while identity theft reports can remove accounts that don’t belong to you.

Proper Delivery Methods Protect Your Rights

Use certified mail with return receipt requested to create an official record of when credit bureaus received your dispute and evidence. This delivery method provides legal proof that you submitted your dispute within required timeframes (particularly important for identity theft cases). The postal receipt becomes valuable evidence if credit bureaus claim they never received your dispute letter.

Now that you know what information to include in your dispute letter, the next step involves the actual submission process and how to track your dispute through completion.

How Do You Submit Your Dispute Letter Effectively

Send your dispute letter through certified mail with return receipt requested to create an unbreakable paper trail that protects your legal rights. The United States Postal Service charges $3.75 for certified mail plus $3.05 for return receipt, but this $6.80 investment provides legal proof that credit bureaus received your dispute on a specific date. Online dispute portals offered by Equifax, Experian, and TransUnion seem convenient but strip away your documentation rights and limit your ability to attach evidence. The Federal Trade Commission warns that online disputes often receive automated responses rather than thorough human review.

Build a Dispute Tracking System That Works

Start a dedicated file folder for each credit bureau dispute and assign a unique number to every letter you send. Record the date you mailed your dispute, the certified mail number, and the date credit bureaus must respond (30 days from receipt). The Consumer Financial Protection Bureau reports that consumers who maintain detailed records win disputes 60% more often than those who rely on memory. Take photos of all documents before you mail them, and keep your certified mail receipts attached to copies of your dispute letters.

Take Action When Credit Bureaus Ignore You

Contact credit bureaus immediately when they miss the 30-day response deadline because the Fair Credit Reporting Act requires automatic removal of disputed information after this period expires. Send a follow-up letter via certified mail that demands removal of the disputed items and references the missed deadline. File complaints with the Consumer Financial Protection Bureau and your state attorney general if credit bureaus continue to ignore your legitimate disputes. South Carolina residents can also contact the South Carolina Department of Consumer Affairs for additional assistance with unresponsive credit bureaus.

Document Every Communication Step

Keep copies of all correspondence you receive from credit bureaus and note the dates when you receive their responses. Credit bureaus must provide written results of their investigation within the 30-day timeframe, and you need these documents to verify they completed proper investigations. Save all postal receipts, tracking confirmations, and delivery confirmations in your dispute file. This documentation becomes vital evidence if you need to escalate your dispute to regulatory agencies or pursue legal action for FCRA violations.

Final Thoughts

An effective Fair Credit Reporting Act dispute letter demands attention to detail and proper documentation. You must include your complete personal information, identify each disputed item with specific account details, and attach supporting evidence that proves your position. Send your letter through certified mail to create legal proof of delivery and maintain detailed records of all communications with credit bureaus.

The 30-day investigation timeline gives you powerful leverage, but credit bureaus sometimes ignore legitimate disputes or provide inadequate responses. When credit reporting errors persist despite your best efforts, legal intervention becomes necessary. Complex cases that involve identity theft, mixed credit files, or repeated FCRA violations often require professional assistance to achieve resolution.

We at Hays Cauley, P.C. help South Carolina residents navigate challenging credit reporting disputes that individual consumers struggle to resolve alone (particularly when credit bureaus fail to respond appropriately). Our consumer protection law firm focuses on credit reporting, identity theft, and debt-related issues that affect your financial future. Contact us at Hays Cauley, P.C. when you need guidance on complex credit reporting violations or when your Fair Credit Reporting Act dispute letter fails to produce results.