Identity Theft Protection SC Essentials For Peace of Mind

Identity theft protection SC isn’t optional anymore. Criminals in South Carolina steal personal information through data breaches, phishing scams, and stolen mail every single day.

We at Hays Cauley, P.C. created this guide to show you exactly how theft happens, what steps stop it, and what to do if you become a victim.

How Identity Theft Happens in South Carolina

Data Breaches Expose Millions of Records

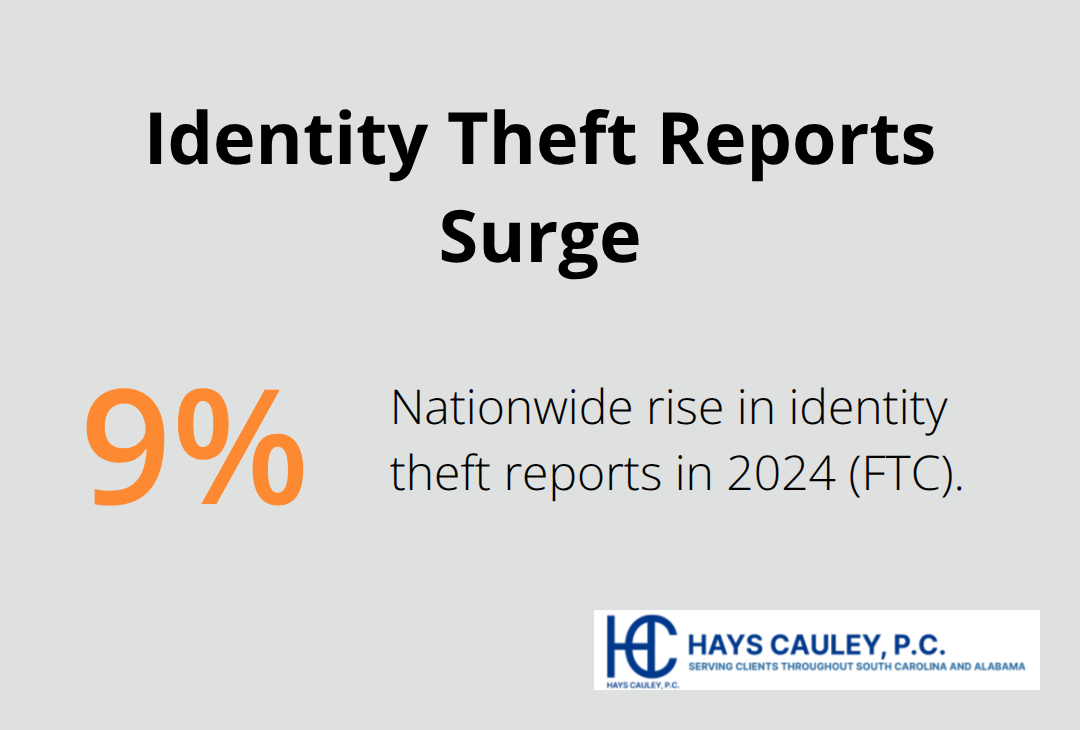

Data breaches expose millions of records annually, and South Carolina residents face real threats from multiple angles. The Federal Trade Commission reported a 9% nationwide rise in identity theft reports in 2024, with early 2025 showing even higher numbers. Nearly 3 billion records were exposed in major breaches including DISA Global Solutions and PowerSchool, affecting countless South Carolina families and students. Criminals exploit these breaches to build profiles on victims, then use stolen information to open accounts or drain existing ones.

Criminals Use Multiple Methods to Steal Your Information

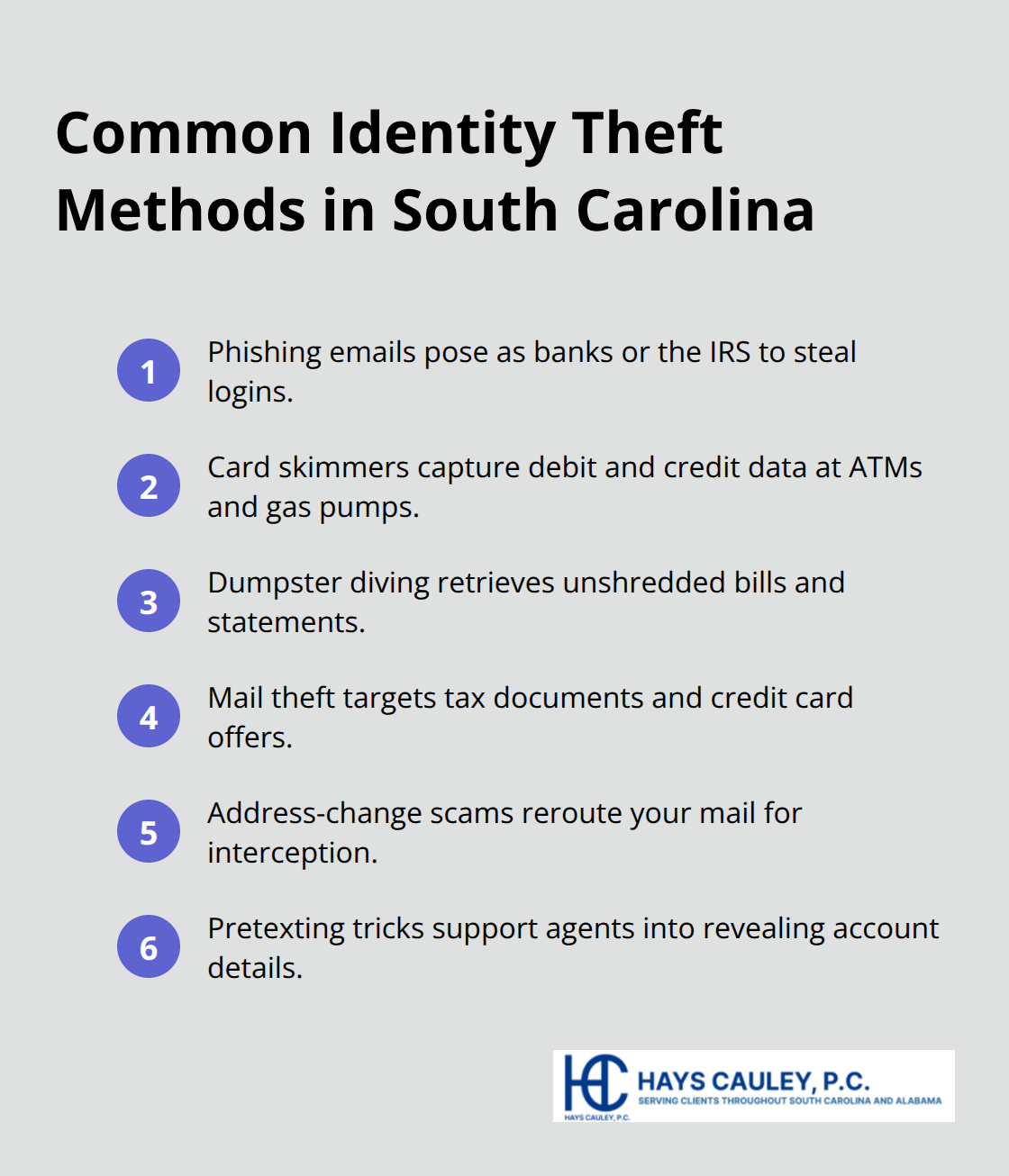

Phishing scams arrive in your email inbox with messages pretending to be from your bank or the IRS, asking you to click a link and verify account information. Card skimming happens at ATMs and gas pumps where criminals install hidden readers to capture your debit or credit card number when you swipe. Dumpster diving sounds outdated, but criminals still find unshredded bills and bank statements in residential trash that contain your name, address, and account numbers. Mail theft targets specific pieces that arrive at your home, including tax documents, credit card offers, and bank statements. Address-change scams redirect your mail to a different location so criminals intercept bills and statements before you notice anything wrong.

Pretexting involves someone calling your bank or credit card company posing as you, using personal details to convince representatives to reveal account information or authorize changes.

Warning Signs Appear Before Major Damage Occurs

Missing mail that normally arrives signals an address-change fraud before criminals open accounts in your name. Unexpected credit card offers or bills arriving for accounts you never opened indicate someone already used your information successfully. Calls from creditors about debts you don’t recognize mean fraudsters filed applications using your Social Security number. Checking your credit reports with Equifax, Experian, and TransUnion reveals unauthorized accounts, hard inquiries, or negative marks you didn’t create. The South Carolina Department of Consumer Affairs Identity Theft Unit recommends checking reports at least annually, though quarterly monitoring catches fraud faster. Child identity theft represents a specific threat because parents often don’t monitor minors’ credit until years later when damage accumulates. If you spot unfamiliar accounts or inquiries, act immediately by contacting the credit bureaus and filing reports with the Federal Trade Commission.

These warning signs tell you when theft has already started, but the real protection comes from stopping criminals before they strike. The next section shows you exactly which steps prevent identity theft from happening in the first place.

How to Stop Identity Theft Before It Starts

Monitor Your Credit Reports Quarterly

Quarterly credit report checks catch fraud faster than annual reviews, and the South Carolina Department of Consumer Affairs Identity Theft Unit recommends this approach for serious protection. Pull your reports from Equifax, Experian, and TransUnion at no cost through annualcreditreport.com, then scan each one for unfamiliar accounts, hard inquiries from companies you never contacted, or negative marks that aren’t yours. Look specifically for accounts opened recently that you don’t recognize, inquiries from creditors you didn’t apply to, and address changes you didn’t authorize.

Most people wait until they suspect theft to check their reports, but quarterly monitoring catches criminals within weeks rather than months or years. Set phone reminders every three months so checking becomes routine, not an afterthought. When you spot something wrong, contact the credit bureau immediately by phone using their dedicated fraud lines: Equifax at 888-378-4329, Experian at 888-397-3742, and TransUnion at 800-680-7289. These bureaus must investigate within 30 days and correct verified errors.

Destroy Physical Documents Before Trash Day

Shredding sensitive documents eliminates the easiest theft method available to criminals in your neighborhood. Dumpster diving remains effective because most households throw away unshredded bills, bank statements, tax returns, and credit card offers that contain names, addresses, account numbers, and Social Security numbers. Purchase a cross-cut shredder and destroy anything with personal information before trash day, including old credit card statements, medical bills, insurance documents, and pre-approved credit offers.

Secure Your Digital Accounts with Strong Passwords

Use unique passwords for every account and never reuse passwords across websites or apps because one breach exposes all your accounts. Password managers like Dashlane or 1Password generate complex passwords and store them securely so you only remember one master password. Enable two-factor authentication on every account that offers it, especially email, banking, and credit card accounts, because stolen passwords alone cannot access these accounts without the second verification step.

Two-factor authentication via authenticator apps like Google Authenticator or Authy provides stronger protection than text messages, which criminals can intercept. This dual-layer defense makes your accounts significantly harder to breach, even when criminals possess your password.

Freeze Your Credit When You’re Not Applying for New Accounts

Place a credit freeze with all three bureaus when you’re not actively applying for credit, which prevents criminals from opening new accounts in your name even with your Social Security number. The freeze is free and takes minutes through each bureau’s website, then you temporarily lift it when you actually apply for credit yourself. This single step stops most identity theft attempts cold because criminals cannot open accounts without accessing your credit file.

These protective steps work best when you combine them into a routine that runs automatically throughout the year. However, even the strongest prevention measures cannot stop every criminal, which is why knowing what to do if theft occurs matters just as much as stopping it beforehand.

Immediate Actions When Identity Theft Strikes

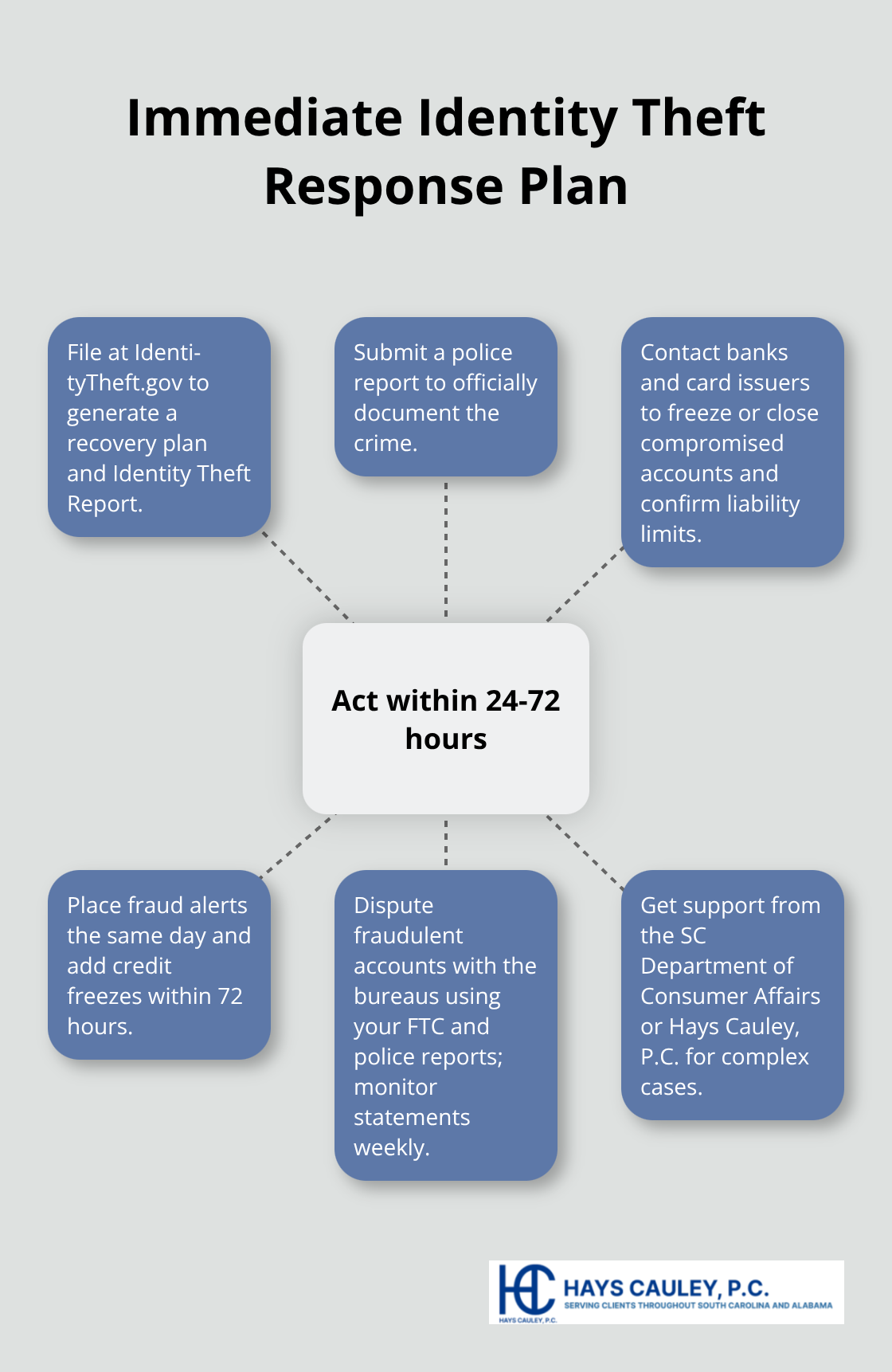

The moment you suspect identity theft, speed matters more than perfection. Contact the Federal Trade Commission at IdentityTheft.gov and file a theft complaint immediately because the FTC provides a personalized recovery plan and Identity Theft Report that guides your next steps. This report becomes official documentation you can share with creditors, banks, and credit bureaus to prove the theft occurred. The FTC received over 2.6 million identity theft reports in 2024, so their system handles high volume efficiently. File a police report labeled Identity Theft at the same time because law enforcement creates an official record that strengthens your credibility with financial institutions.

Contact Your Financial Institutions Immediately

Call your banks and credit card companies directly using the numbers on your statements, not numbers from search results, because criminals intercept calls to fake customer service lines. Tell each institution which accounts show fraudulent activity, request they freeze or close compromised accounts, and ask about liability limits. Most credit card companies limit fraud liability to $50 under federal law, and many waive it entirely if you report quickly. For bank accounts, federal protections vary, but reporting within 60 days limits your losses significantly.

Place Fraud Alerts and Credit Freezes

Place a fraud alert with all three credit bureaus by calling Equifax at 888-378-4329, Experian at 888-397-3742, and TransUnion at 800-680-7289 on the same day you discover theft. Fraud alerts are free and remain active for one year, slowing new account openings because creditors must verify your identity before issuing credit. After placing an alert, each bureau sends confirmation letters to your address, providing written proof for your records. Within 72 hours, implement a credit freeze with all three bureaus if you want maximum protection, because freezes prevent anyone from accessing your credit file without your explicit permission. Freezes remain permanent until you lift them, making them stronger than fraud alerts, though you must temporarily unfreeze when applying for legitimate credit yourself.

Dispute Fraudulent Accounts and Monitor Activity

Request copies of your credit reports and dispute any fraudulent accounts or inquiries directly with each bureau, submitting documentation from your police report and FTC report. The bureaus must investigate within 30 days and remove verified fraudulent items from your file. Monitor your bank and credit card statements weekly for 12 months after discovering theft because criminals sometimes use stolen information months later.

Seek Additional Support for Complex Cases

The South Carolina Department of Consumer Affairs Identity Theft Unit offers one-on-one support via phone or email if you need personalized assistance navigating recovery. If your case involves tax fraud or government benefits abuse, file additional complaints with the IRS or relevant agencies using your FTC Identity Theft Report as supporting documentation. Hays Cauley, P.C., a consumer protection law firm dedicated to helping consumers with credit reporting, identity theft, and debt-related issues, can assist South Carolina residents who face creditor disputes, wrongful debt collection, or credit reporting errors that occur after theft.

Final Thoughts

Identity theft protection SC requires action on three fronts: prevention before theft occurs, quick detection when it happens, and aggressive recovery afterward. Quarterly credit monitoring catches fraud within weeks rather than years, strong passwords and two-factor authentication stop account takeovers, and credit freezes prevent new accounts from opening in your name. When theft strikes, filing with the Federal Trade Commission, contacting your banks immediately, and placing fraud alerts with all three credit bureaus creates an official record that protects you legally and financially.

South Carolina offers specific resources through the Department of Consumer Affairs Identity Theft Unit, which provides one-on-one support and step-by-step checklists for different theft scenarios. The FTC’s IdentityTheft.gov website generates personalized recovery plans based on your situation, while the three major credit bureaus provide free fraud monitoring and dispute resolution. These resources exist because identity theft affects millions annually, and recovery requires coordination across multiple agencies and institutions.

We at Hays Cauley, P.C. understand that identity theft creates stress beyond the financial damage-our consumer protection law firm helps South Carolina residents navigate credit reporting disputes, identity theft recovery, and debt-related issues that arise after theft occurs. If creditors pursue fraudulent debts in your name or credit bureaus refuse to remove false information from your reports, contact us for guidance on protecting your rights and rebuilding your financial life. Professional support makes the recovery process faster and more effective.