Freeze Credit Report SC: Why South Carolinians Do It and How

Identity theft affects thousands of South Carolinians every year, and one of the most effective ways to protect yourself is to freeze your credit report. A credit freeze SC prevents criminals from opening accounts in your name, even if they have your personal information.

We at Hays Cauley, P.C. understand how stressful identity theft can be, which is why we’ve created this guide to walk you through the process. Whether you’re concerned about a data breach or simply want to be proactive, this article covers everything you need to know about protecting your financial identity.

Why South Carolinians Need to Freeze Their Credit

South Carolina residents face a real and growing threat from identity theft. Between July and October 2019 alone, security breaches affected 595,344 South Carolinians-a 316% spike compared to the first half of that year, according to the South Carolina Department of Consumer Affairs. In 2024, the Identity Theft Resource Center reported 2,850 data breaches affecting over a billion victims globally, making a credit freeze one of the most practical defenses available. A credit freeze blocks lenders from accessing your credit report without your explicit permission, which means criminals cannot open new credit accounts in your name even if they possess your Social Security number, date of birth, and address. This layer of protection matters especially for South Carolinians because once your information appears in a breach notification, you become a target. Scammers move quickly, and the Global Anti-Scam Alliance found that global scammers stole over $1 trillion in 2024.

A frozen credit report stops the most common form of identity theft before it starts, making it far more difficult for thieves to open credit cards, take out loans, or establish phone accounts under your name.

When breaches hit close to home

Many South Carolinians receive a breach notification from a company they do business with and then realize they need a credit freeze. The moment you receive notice that your data has been compromised, action becomes urgent. Waiting weeks or months gives criminals a window to act, so you should freeze your credit within days of a breach notification. You should also freeze your credit if you notice suspicious activity on your existing accounts, receive unexpected bills or collection notices, or simply want to prevent future fraud before it happens. There is no requirement to wait for a breach to occur; you can freeze proactively at any time.

What a freeze actually stops and what it doesn’t

A credit freeze prevents new credit applications from being approved in your name because lenders cannot access your frozen credit report to make lending decisions. However, a freeze does not protect existing accounts from fraud, so you must continue monitoring your current credit cards, bank accounts, and loan statements for unauthorized charges. Current creditors can still access your report, as can debt collectors, government agencies, and employers conducting background checks. Marketing companies cannot access your frozen report to send you credit offers (a welcome side benefit). The freeze remains in effect indefinitely until you request it be lifted, giving you complete control over when your credit report becomes accessible again.

Taking action after a breach

If you’ve received a breach notification, the next step is straightforward: contact all three major credit bureaus to initiate your freeze. The process takes minimal time, costs nothing, and provides substantial protection against the criminals who now have your information. Understanding how to freeze your credit with Equifax, Experian, and TransUnion will help you act quickly and effectively.

Getting Your Credit Frozen in South Carolina

Contact all three bureaus to activate your freeze

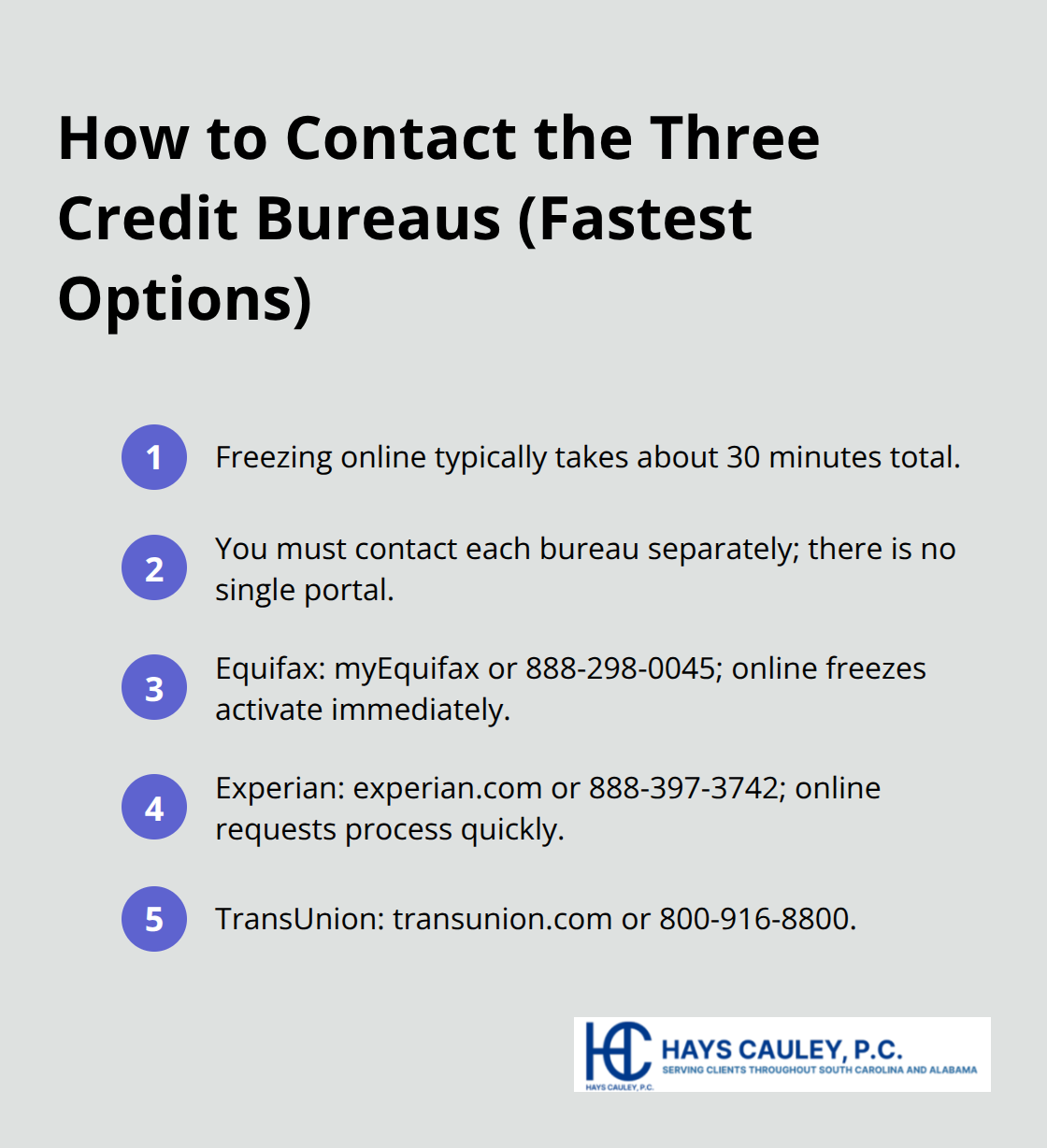

Freezing your credit with all three bureaus takes roughly 30 minutes if you act online, which is the fastest method available. Equifax, Experian, and TransUnion each maintain separate freeze systems, so you cannot freeze all three from a single portal-you must contact each bureau individually.

Start with Equifax at myEquifax or 888-298-0045; online freezes activate immediately. Experian processes online requests just as quickly through experian.com or 888-397-3742. TransUnion handles freezes at transunion.com or 800-916-8800.

If you prefer mailing a written request, expect three to five business days for processing, though South Carolina law requires bureaus to implement freezes within five business days of receiving your request. The online and phone routes are superior because they eliminate mail delays entirely-you receive confirmation within hours rather than days. When you freeze online, each bureau provides a unique PIN or password within 10 business days, which you’ll need later if you want to temporarily lift the freeze for a specific credit application. Save these PINs in a secure location separate from your other passwords.

Prepare your documents before you start

For online freezes, have your Social Security number, date of birth, and current address ready; the bureaus verify your identity through these details and may ask additional security questions. If you freeze by phone, the same information applies. Mailing a freeze request requires more documentation: include copies of one form of proof showing your Social Security number (such as a tax return or W-2) and two forms of address verification from the past two years (utility bills, bank statements, or lease agreements work well). Never mail original documents-always send copies.

South Carolina residents should mail Equifax requests to P.O. Box 105788, Atlanta, GA 30348-5788; Experian to P.O. Box 9554, Allen, TX 75013; and TransUnion to P.O. Box 160, Woodlyn, PA 19094. Use certified mail for paper requests to obtain proof of delivery and track processing.

Verify your freeze is working

After the freeze activates, test it by attempting to apply for a small credit product like a store card-if the application is denied or delayed due to your frozen report, your security freeze is working correctly. Serving South Carolina, including Greenville, Columbia and Charleston, residents should act on freezes immediately after receiving breach notifications rather than waiting weeks, since criminals typically strike within days of obtaining stolen data. Once you confirm your freeze is active, you’ll want to understand how to manage it when you need to apply for new credit, which requires a temporary lift of your freeze.

What Does a Credit Freeze Actually Cost in South Carolina

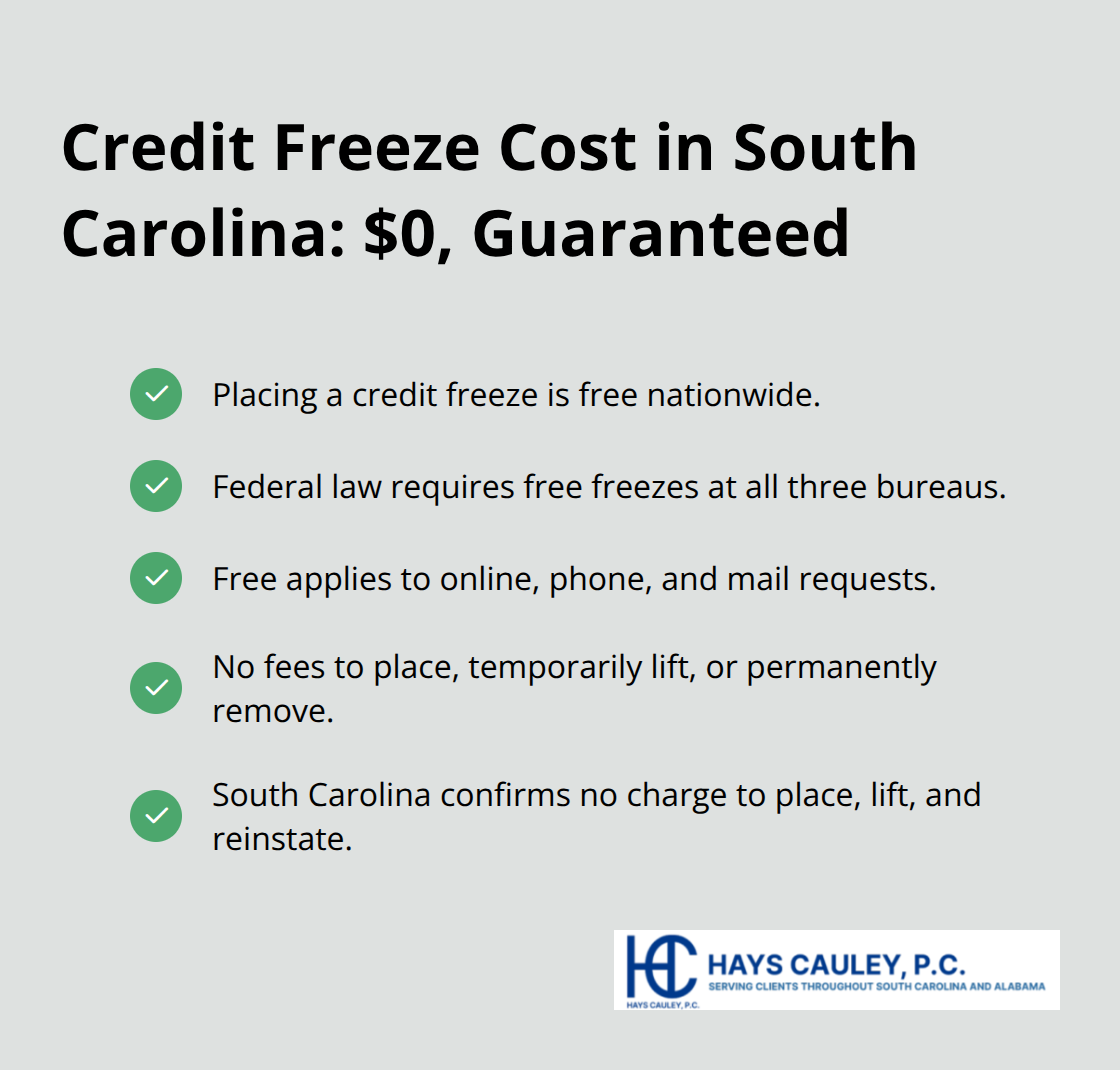

Freezing your credit costs nothing in South Carolina and across the United States, which removes the biggest barrier to taking this protective action immediately. Federal law guarantees that all three major bureaus must offer free freezes, and this applies whether you freeze online, by phone, or by mail. No hidden fees exist for placing a freeze, lifting it temporarily, or removing it permanently.

This zero-cost protection is one reason why South Carolinians should act without hesitation after receiving a breach notification. The South Carolina Department of Consumer Affairs confirms that placing, lifting, and reinstating a security freeze carries no charge under state law, reinforcing your right to this protection at no expense.

Thaw your freeze when you need new credit

The moment you apply for a mortgage, auto loan, credit card, or even a cell phone plan, lenders attempt to access your frozen credit report and get denied. You can thaw your freeze at one specific bureau if you know which lender will pull your report, or thaw all three if you’re unsure. Electronic thaw requests process within 15 minutes to one hour according to South Carolina law and FTC guidance, so you can submit a thaw request on the morning of your application and have access restored long before your appointment. Each bureau provides you with a unique PIN or password when your freeze activates, and you use this PIN to request temporary or permanent thaws online, by phone, or by mail. After your credit application completes, simply refreeze with that bureau or all three bureaus within minutes. The entire cycle of thaw-and-refreeze takes less than 30 minutes if you act online.

Plan ahead for credit applications

When you know credit applications are coming, thaw at the right time to avoid application delays or denials that frustrate lenders and slow down your approval process. You control the timing entirely, which means you can thaw your report hours before an appointment and refreeze it immediately afterward. This flexibility makes a frozen credit report compatible with normal credit activity-you simply need to plan a few hours ahead. South Carolina law allows you to schedule automatic refreezes for convenience, so you don’t have to remember to refreeze manually after each application.

Monitor your existing accounts actively

A frozen credit report does not stop fraud on accounts you already own, which means you must monitor your existing credit cards, bank accounts, and loan statements actively after a freeze activates. The Federal Trade Commission recommends checking your credit reports from all three bureaus at least once per year through annualcreditreport.com, which provides free copies without affecting your credit score. Many South Carolinians also sign up for free credit monitoring services offered by the bureaus themselves or review their statements monthly for unauthorized charges. If you discover fraudulent activity on an existing account, contact your bank or credit card issuer immediately to report it and request a chargeback or account closure. A credit freeze is a strong first line of defense, but it works best alongside active monitoring of your financial accounts and regular review of your credit reports for inaccuracies or unfamiliar accounts that signal identity theft.

Final Thoughts

A freeze credit report SC strategy protects you from identity theft at no cost and takes roughly 30 minutes online. Criminals strike within days of obtaining stolen data, so you must act quickly after receiving a breach notification rather than waiting weeks or months. Contact Equifax, Experian, and TransUnion online to freeze all three bureaus, save your PINs securely, and verify your freeze works by attempting a small credit application.

Continue monitoring your existing accounts actively because a freeze does not protect current credit cards or bank accounts from fraud. Review your credit reports annually through annualcreditreport.com and watch for unfamiliar accounts or suspicious charges that signal unauthorized activity. You maintain complete control over when your credit report becomes accessible, which means you can thaw temporarily for legitimate credit applications and refreeze immediately afterward.

If you’ve experienced identity theft or received a breach notification and need guidance on your rights and recovery options, we at Hays Cauley, P.C. are here to help. Our team focuses on consumer protection issues including identity theft and credit reporting matters. Serving South Carolina, including Greenville, Columbia and Charleston, we work with residents who face fraud, inaccurate credit reports, or debt-related concerns.