Fair Credit Reporting Act Penalties in South Carolina What You Need to Know

The Fair Credit Reporting Act (FCRA) plays a vital role in protecting consumers’ financial information and rights. At Hays Cauley, P.C., we understand the importance of knowing your rights and the potential consequences for those who violate them.

This blog post will explore the Fair Credit Reporting Act penalties in South Carolina, empowering you to safeguard your credit information and take action when necessary.

What Does the FCRA Mean for South Carolina Residents?

The FCRA’s Core Purpose

The Fair Credit Reporting Act (FCRA) serves as a federal shield for the accuracy and privacy of consumer credit information. South Carolina residents receive critical protections and rights regarding their credit reports and financial data through this law.

Impact on South Carolina Consumers

Credit reporting agencies must adhere to FCRA regulations, which benefit South Carolina residents. These agencies have an obligation to ensure the information they collect and distribute is accurate, relevant, and current. When you apply for a loan, credit card, or job in South Carolina, the information used to make decisions about you should be reliable.

Access and Dispute Rights

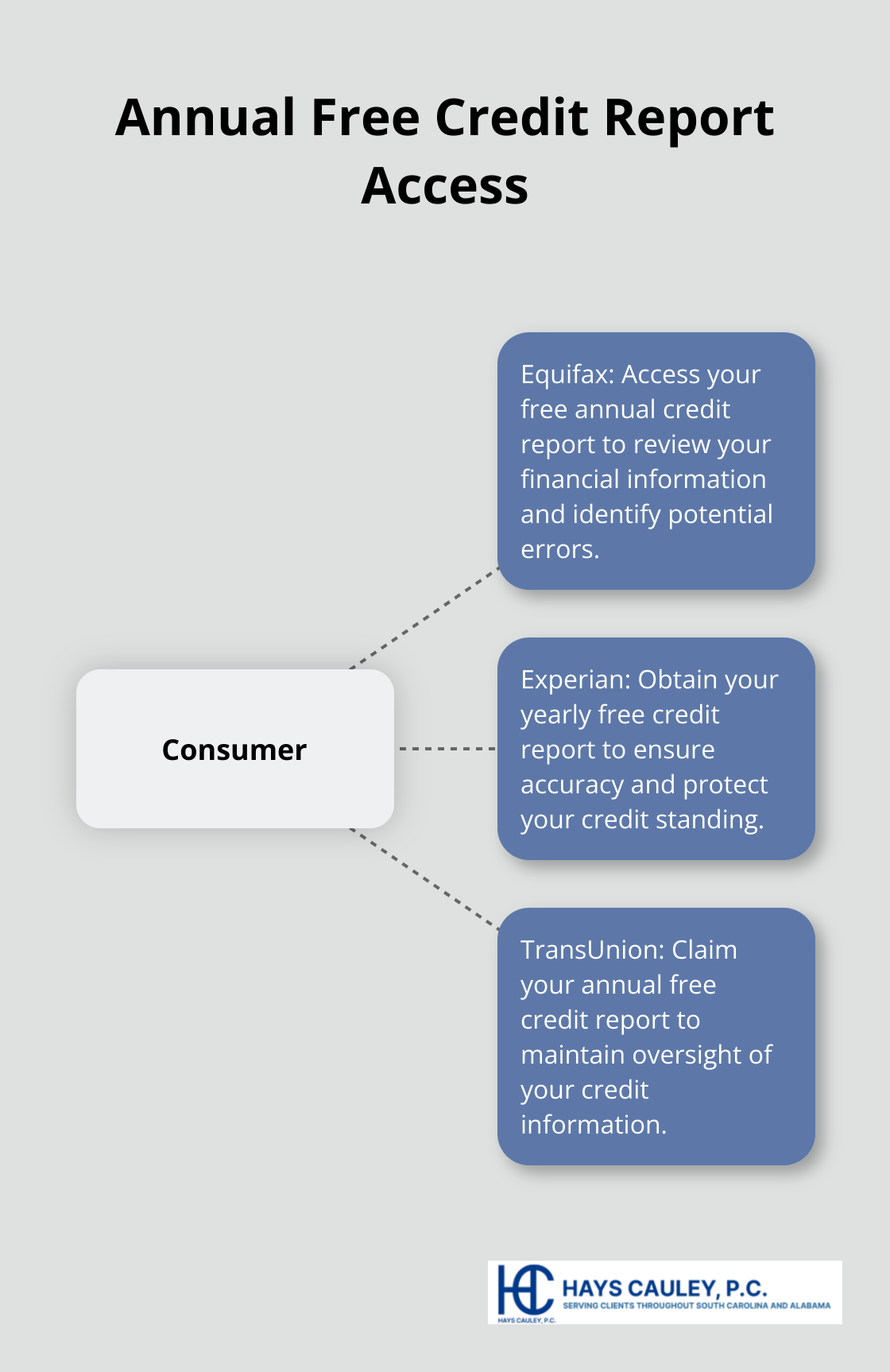

The FCRA provides South Carolina consumers with a powerful tool: the right to access their credit reports for free once a year from each of the three major credit bureaus (Equifax, Experian, and TransUnion). This access allows you to review your credit information and identify any errors that could harm your financial standing.

If you discover inaccuracies, the FCRA grants you the right to dispute this information. Credit bureaus must investigate your claims within 30 days and correct any verified errors. This process can prove crucial for maintaining a healthy credit score and ensuring fair treatment in financial matters.

Protection Against Unfair Practices

The FCRA also protects South Carolina residents from unfair practices related to their credit information. For example:

- Employers must obtain your written consent before pulling your credit report for hiring decisions.

- If a company denies you credit based on information in your report, they must provide you with an adverse action notice explaining the reasons for the denial.

These protections can make a real difference in the lives of South Carolina consumers. Understanding your rights under the FCRA is the first step to take control of your financial narrative and ensure fair treatment by credit reporting agencies.

As we move forward, it’s important to understand the specific types of FCRA violations and the penalties associated with them. This knowledge will empower you to recognize when your rights might be infringed upon and what actions you can take to protect yourself.

What Are FCRA Violations and Their Consequences?

Credit Reporting Agency Violations

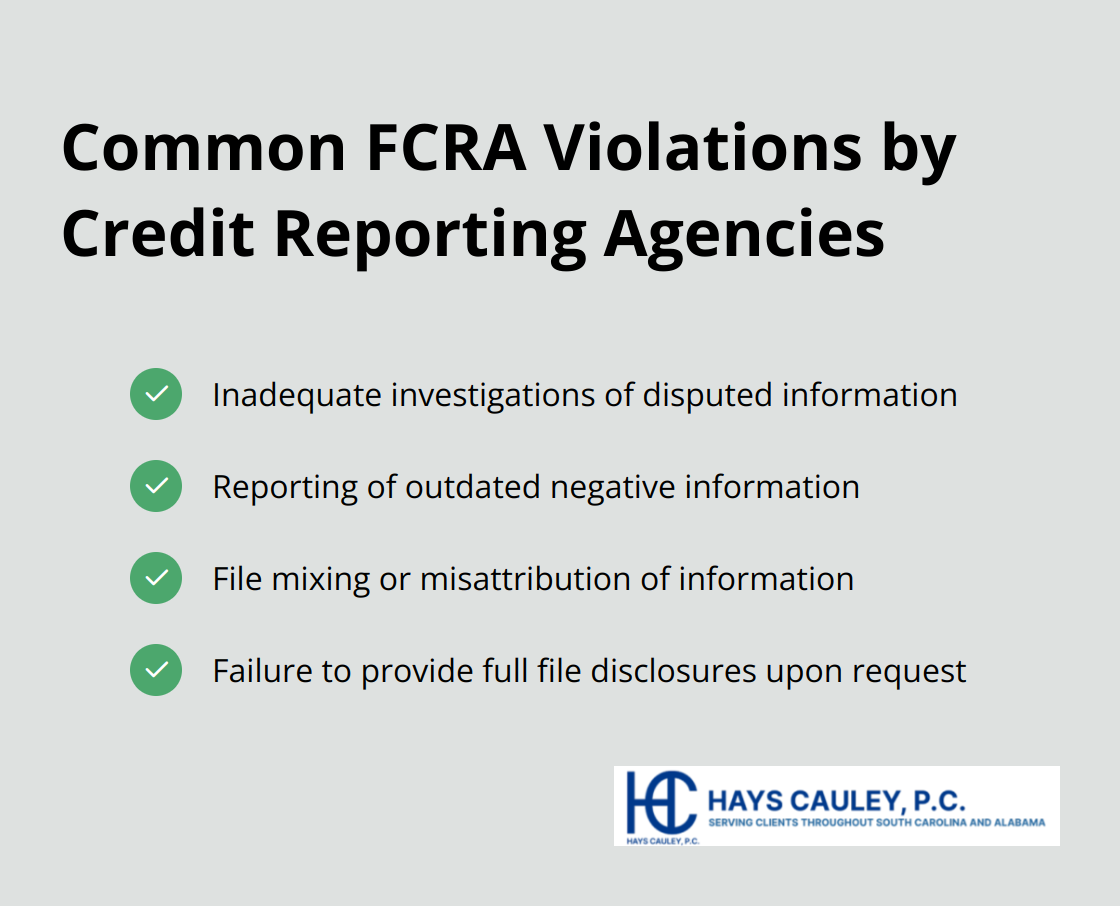

The Fair Credit Reporting Act (FCRA) establishes strict guidelines for credit reporting agencies (CRAs) like Equifax, Experian, and TransUnion. These agencies sometimes fail to meet their FCRA obligations. Common violations include:

- Inadequate investigations of disputed information

- Reporting of outdated negative information

- File mixing or misattribution of information

- Failure to provide full file disclosures upon request

These violations can severely impact the credit scores and financial opportunities of South Carolina residents.

Information Furnisher Missteps

Banks, credit card companies, and other entities that provide information to CRAs must also comply with FCRA rules. They may violate the Act by:

- Reporting inaccurate information

- Failing to update or correct errors after notification

- Inadequate investigation of consumer disputes

- Continued reporting of proven false information

Such violations perpetuate errors in credit reports, which causes ongoing harm to consumers.

Penalties for Willful Noncompliance

When a CRA or furnisher knowingly violates the FCRA, they face severe penalties for willful noncompliance. These can include:

- Actual damages suffered by the consumer

- Statutory damages between $100 and $1,000 per violation

- Punitive damages (as determined by the court)

- Attorney’s fees and court costs

In cases of widespread violations, these penalties can add up to millions of dollars. For example, in 2019, Equifax agreed to pay up to $700 million to settle federal and state investigations following a massive data breach.

Consequences of Negligent Noncompliance

Even unintentional violations carry consequences for negligent noncompliance:

- Actual damages incurred by the consumer

- Reasonable attorney’s fees (as determined by the court)

While these penalties may appear less severe, they can still result in significant financial liability for violators.

South Carolina consumers should know that the FCRA provides robust protections. If you suspect a violation, you should document the issue and seek legal advice promptly. This action will help you understand your rights and potential for compensation.

The next chapter will explore how South Carolina residents can enforce their rights under the FCRA and take action against violations.

How South Carolina Residents Can Enforce Their FCRA Rights

Document the Issue

South Carolina residents who suspect an FCRA violation should start by collecting all relevant documents. This includes copies of credit reports, correspondence with credit bureaus or creditors, and evidence of financial harm due to inaccurate reporting. A detailed log of all phone calls (including dates, times, and names of representatives) will strengthen your case.

Contact Credit Reporting Agencies

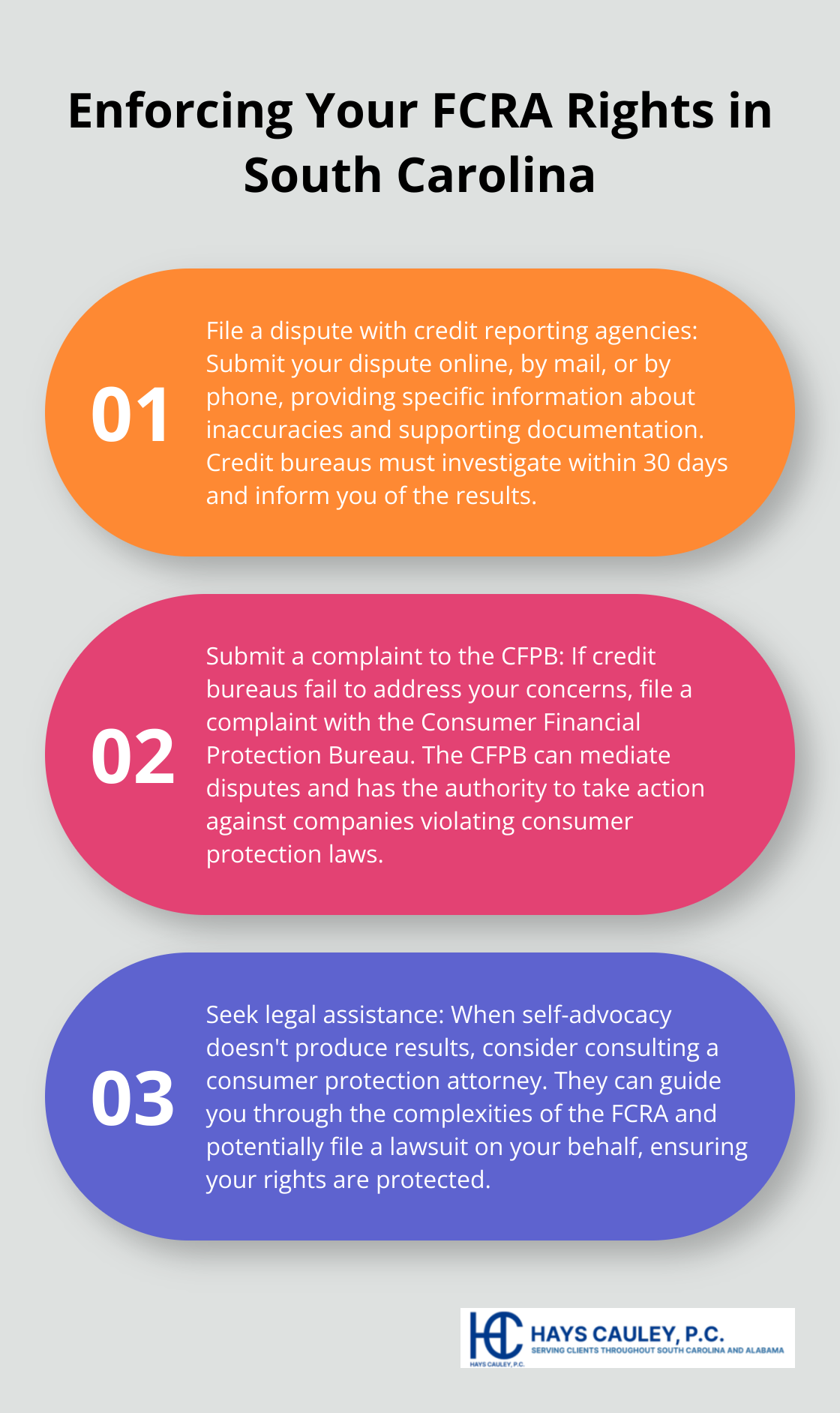

Your first action should be to file a dispute directly with the credit reporting agencies. You can submit this dispute online, by mail, or by phone. Provide specific information about what you believe is incorrect and include any supporting documentation. Credit bureaus must investigate your claim within 30 days and inform you of the results.

File a Complaint with the CFPB

If credit bureaus fail to address your concerns, submit a complaint to the Consumer Financial Protection Bureau (CFPB). The CFPB can mediate disputes and has the authority to take action against companies that violate consumer protection laws. Their website offers a straightforward complaint submission process and valuable resources on consumer rights.

Consider Legal Assistance

When self-advocacy doesn’t produce results, legal action may be necessary. A consumer protection attorney can guide you through the complexities of the FCRA and potentially file a lawsuit on your behalf. Many attorneys (including those at consumer protection law firms) offer free initial consultations to assess your case.

Understand the Statute of Limitations

In South Carolina, you have a limited time to file an FCRA lawsuit. The statute of limitations is generally two years from the date you discover a violation, or five years from the date the violation occurred (whichever comes first). This timeline makes it essential to address potential violations promptly.

The Federal Trade Commission reports that millions of Americans have errors on their credit reports that could affect their credit scores. Taking swift action to enforce your FCRA rights protects your financial health and contributes to a more accurate and fair credit reporting system for all South Carolina residents.

Final Thoughts

The Fair Credit Reporting Act (FCRA) protects South Carolina consumers and imposes penalties on violators. These penalties range from monetary damages to legal action, which deters willful and negligent noncompliance by credit reporting agencies and information furnishers. South Carolina residents must review their credit reports regularly and dispute inaccuracies promptly to protect their financial well-being.

Consumer protection attorneys play a vital role in enforcing the FCRA and holding violators accountable. They guide consumers through the law’s complexities, help with disputes, and pursue legal action to secure Fair Credit Reporting Act penalties against non-compliant entities. Their expertise becomes invaluable when facing persistent violations or complex FCRA issues.

South Carolina residents who need assistance with credit reporting issues, identity theft, or debt-related problems can turn to consumer protection law firms like Hays Cauley, P.C. Their knowledge of FCRA cases can resolve disputes and protect your rights under the law. The FCRA empowers you to take control of your credit information and seek recourse when your rights face violation.