Debt collectors often cross the line, using aggressive tactics and reporting false information to damage your credit. The Fair Credit Reporting Act gives you real protections and debt collection remedies in SC that many people don’t know about.

We at Hays Cauley, P.C. help South Carolina residents fight back against illegal collection practices. Understanding your rights is the first step toward stopping harassment and fixing your credit report.

What the Fair Credit Reporting Act Actually Protects

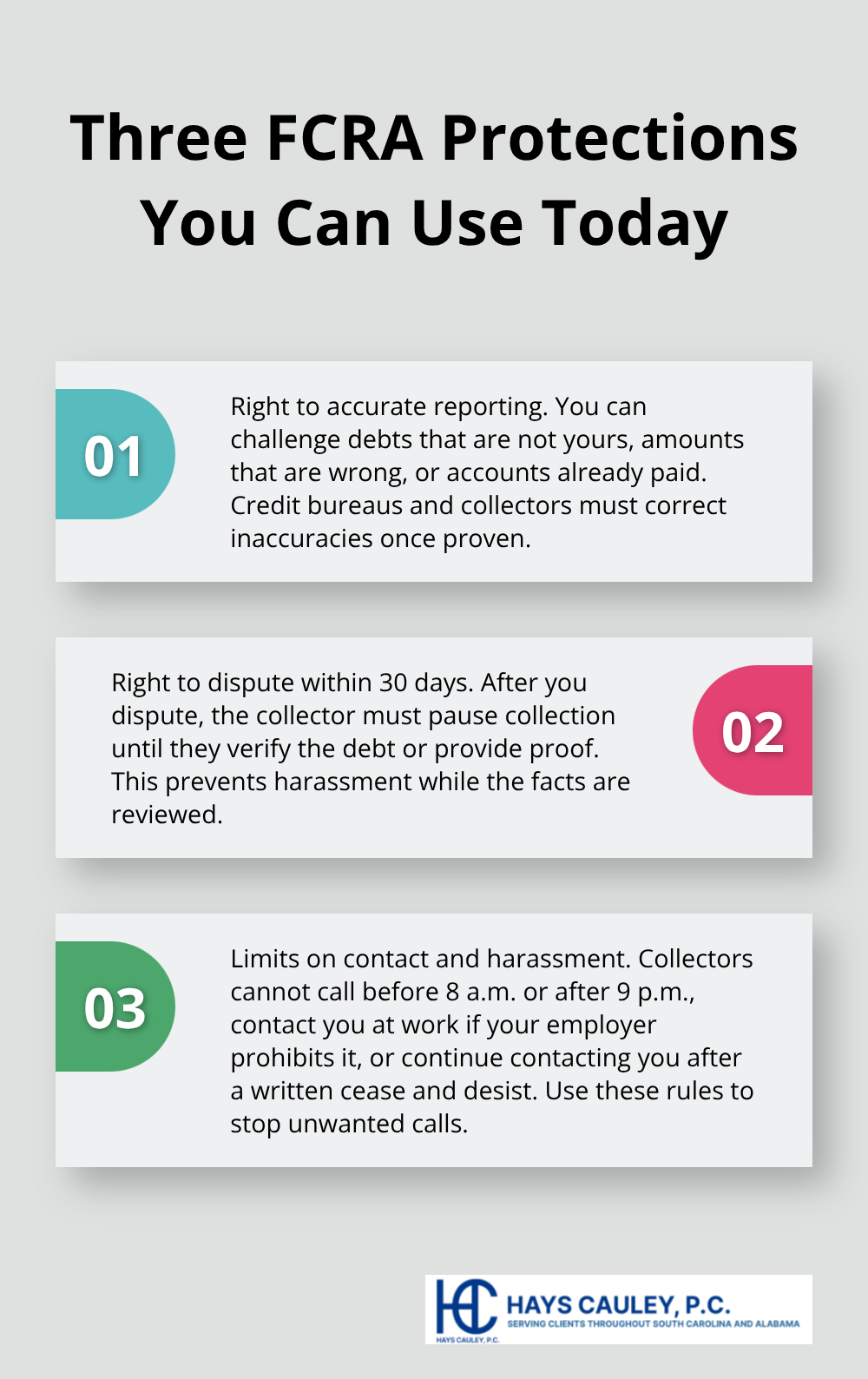

Three Core Protections Against Debt Collectors

The Fair Credit Reporting Act provides three concrete protections that directly impact debt collection. First, you have the right to accurate information on your credit report. If a debt collector reports a debt you’ve already paid, reports an incorrect amount, or lists a debt that isn’t yours, that’s a violation you can challenge. Second, you can dispute errors within 30 days of receiving a debt collection notice, and the collector must stop collection efforts until they verify the debt or provide proof. Third, debt collectors cannot contact you at work if your employer prohibits it, cannot call before 8 a.m. or after 9 p.m. in your local time zone, and must stop all contact if you send a written cease and desist letter.

South Carolina’s Additional Legal Safeguards

South Carolina law reinforces these protections through Title 37, Chapter 5. Creditors must provide a notice of right to cure before pursuing repossession, and they cannot garnish wages for certain consumer credit debts. The FDCPA also mandates that collectors provide a validation notice within five days of first contact, listing the debt amount, the creditor’s name, and your right to dispute. These aren’t suggestions-they’re legal requirements with real consequences when violated.

How Violations Happen in Practice

Inaccurate credit reporting happens constantly in South Carolina. Debt buyers often sue on credit card debt without proper documentation and frequently report wrong amounts or debts that have already been paid. When a collector violates these protections (by calling repeatedly to harass you, misrepresenting the debt amount, or reporting false information to credit bureaus), you can recover actual damages plus up to $1,000 in statutory damages per violation under the FDCPA. You can also recover court costs and attorney’s fees. In South Carolina, violations of consumer protection laws under Title 37, Chapter 5 carry similar remedies, with court-determined penalties available.

Real Financial Consequences for Collectors

If a collector reports a $5,000 debt when you actually owe $2,000, or if they call your workplace after you’ve told them not to, you have grounds for a lawsuit. These violations give you leverage to hold collectors accountable and stop the harassment. Understanding what constitutes a violation puts you in position to identify when a debt collector has crossed the line and what legal remedies you can pursue.

How Debt Collectors Violate Your Rights: Serving South Carolina, Including Greenville, Columbia and Charleston

Harassment Through Repeated Contact and Workplace Calls

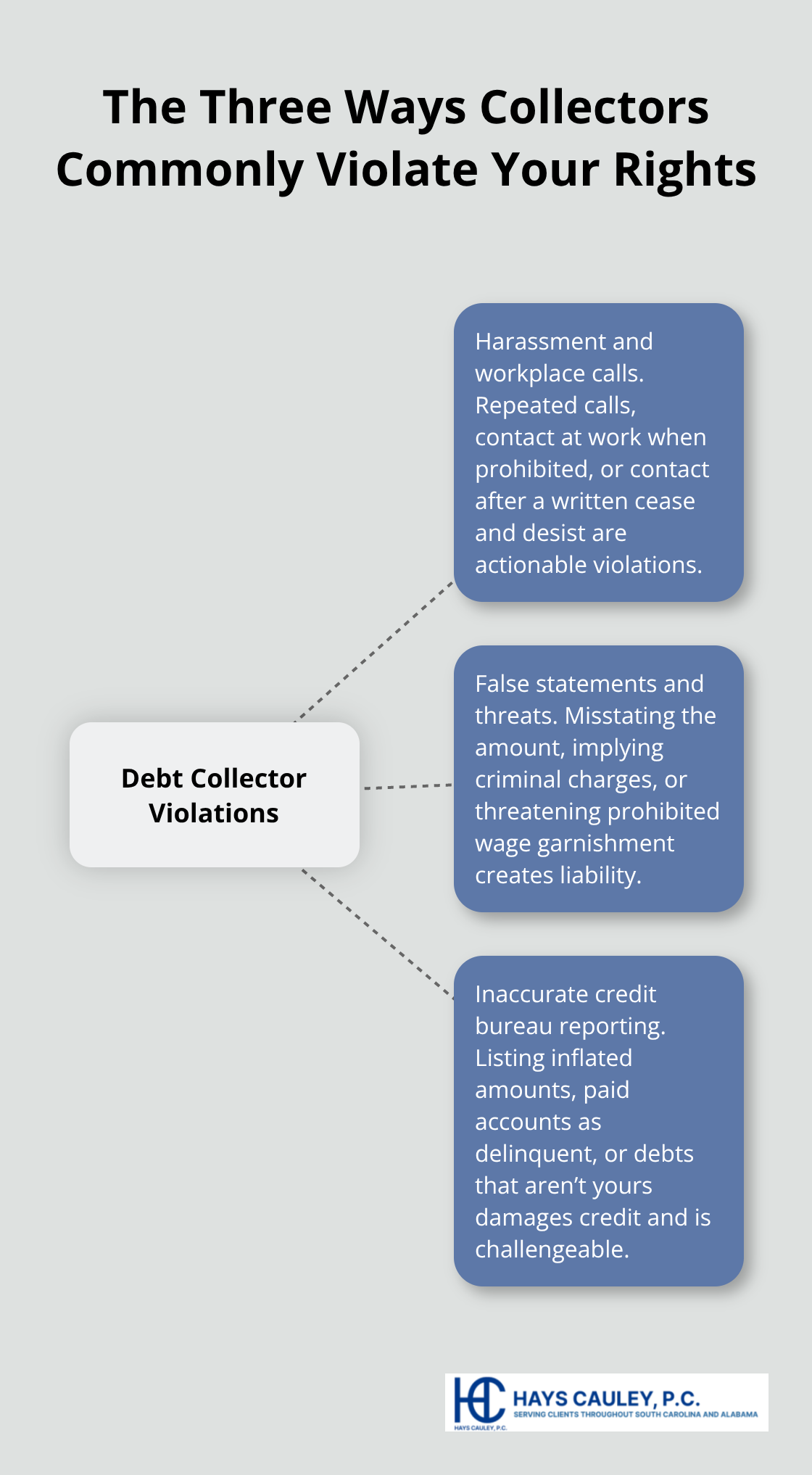

Debt collectors routinely violate the Fair Credit Reporting Act and South Carolina’s consumer protection laws in three distinct ways. The most common violation involves harassment through repeated calls and workplace contact. Under the FDCPA, debt collectors cannot call before 8 a.m. or after 9 p.m. in your local time zone, cannot contact you at work if your employer prohibits it, and must stop all contact if you send a written cease and desist letter. The Consumer Financial Protection Bureau receives thousands of complaints annually about collectors ignoring these rules. When a collector calls your workplace repeatedly after you’ve explicitly told them not to, or contacts your employer directly to pressure you into paying, that violation gives you grounds for legal action. South Carolina law under Title 37, Chapter 5 reinforces this protection, and violations result in actual damages plus court-determined penalties.

False Statements About Debt Amounts and Collection Authority

False or misleading statements represent the second major violation category. Debt collectors frequently misrepresent the debt amount, claim they’ll pursue criminal charges (which is illegal for consumer debt), threaten wage garnishment when state law prohibits it for certain debts, or pretend to be affiliated with government agencies or law firms. Debt buyers purchasing old credit card debt commonly report incorrect amounts or debts already paid. When you receive a collection notice, the FDCPA requires the collector to include a validation notice within five days listing the exact debt amount and your right to dispute within 30 days. If the amount listed differs from what you actually owe or from documentation you possess, that false statement creates liability for the collector. The FDCPA also includes a bona fide error defense only if the collector had reasonable procedures in place to prevent violations, meaning careless or systematic violations carry maximum penalties.

Inaccurate Credit Bureau Reporting

The third violation involves reporting inaccurate information to credit bureaus. A collector might report a debt as currently delinquent when you’ve already paid it, list an inflated amount, or report a debt that belongs to someone else entirely. These inaccuracies stay on your credit report for seven years unless you dispute them, damaging your ability to secure loans, housing, or employment. South Carolina Legal Services identified predatory lending practices and debt collection violations as priority areas for consumer protection in 2026, recognizing how frequently these violations harm low-income families. When collectors violate these protections, you can recover actual damages plus up to $1,000 in statutory damages under the FDCPA, along with court costs and attorney’s fees.

Understanding these three violation categories positions you to identify when a debt collector has crossed the line. The next section explains the specific remedies available to you when these violations occur.

Remedies Available to You Under the FCRA: Serving South Carolina, Including Greenville, Columbia and Charleston

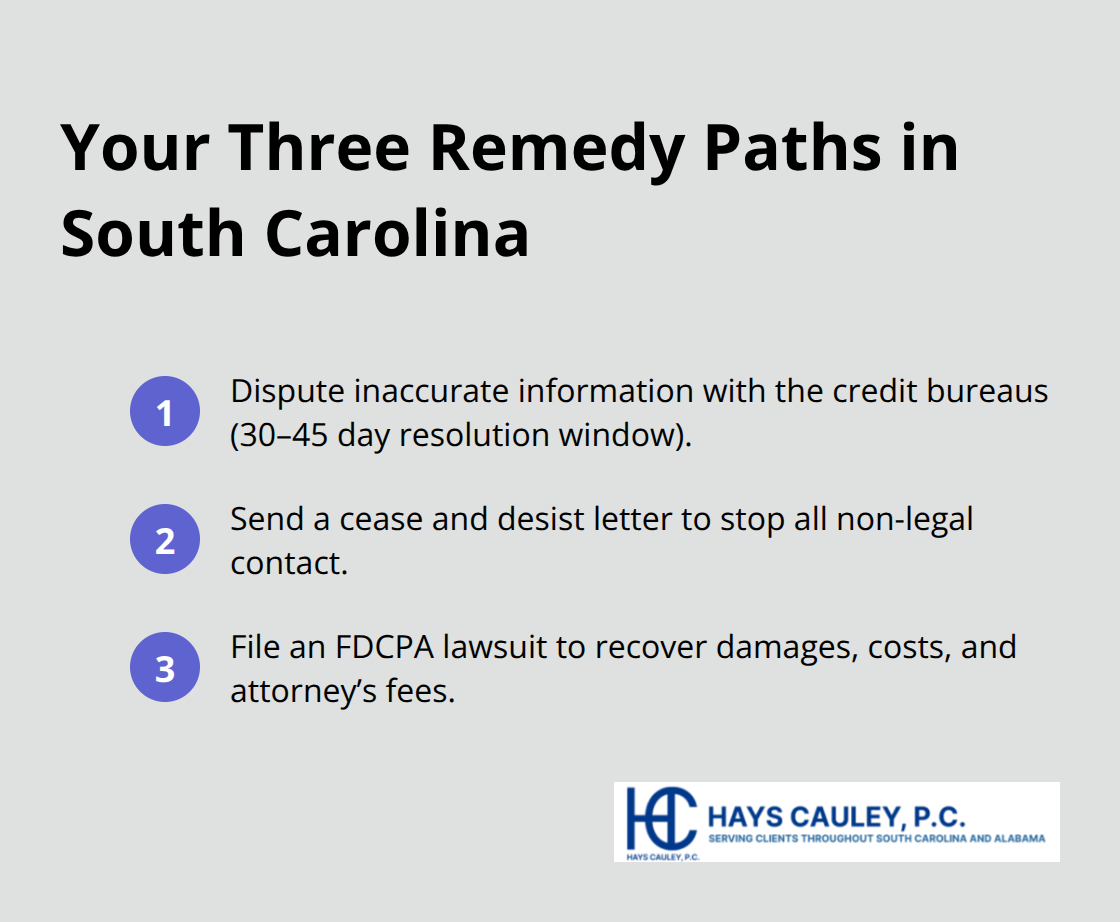

When a debt collector violates your rights, you have three concrete paths to hold them accountable and stop the damage to your credit and finances. The first and fastest step involves disputing the inaccurate information directly with credit bureaus, which costs nothing and can remove false entries within 30 to 45 days. The second requires sending a cease and desist letter, a written demand that forces collectors to stop all contact except for specific legal actions.

The third involves filing a lawsuit against the collector for FDCPA violations, where you can recover actual damages plus up to $1,000 in statutory damages per violation, along with court costs and attorney’s fees. Most collectors settle these cases quickly because the financial exposure is significant and defending against multiple violations becomes costly.

Dispute Inaccurate Information With Credit Bureaus

Start with disputing directly with the credit bureau reporting the false information. Under the Fair Credit Reporting Act, you have 30 days from receiving a debt collection notice to dispute the debt in writing, and the collector must stop collection efforts until they verify it or obtain a judgment. Send your dispute to Equifax, Experian, or TransUnion (whichever bureau reported the error) by certified mail with return receipt requested. Include documentation showing the debt is inaccurate, already paid, or not yours. The bureau must investigate within 30 days and remove the item if the collector cannot verify it. This method works particularly well when debt buyers report credit card debts with incorrect amounts or debts already paid, which happens frequently in South Carolina. If the collector ignores your dispute and continues collection efforts, that violation itself creates grounds for a lawsuit.

Send a Cease and Desist Letter

Send a cease and desist letter if the collector harasses you through repeated calls, workplace contact, or messages after you have told them to stop. This written demand must explicitly state you are requesting they cease all communication except for notification of specific legal actions like lawsuits or judgment enforcement. Mail it by certified mail with return receipt to the collector’s address listed on their collection notice. Once received, the FDCPA requires them to stop contacting you except to confirm they will cease contact or to notify you of specific legal action. Collectors violating this cease and desist order face statutory damages of up to $1,000 per violation, making this letter a powerful tool that costs only postage.

File a Lawsuit Against the Collector

If disputes and cease and desist letters do not resolve the violation, file a lawsuit in South Carolina state court where you reside. You can represent yourself or hire an attorney; under the FDCPA, a collector who violates your rights must pay your attorney’s fees and court costs if you prevail, making litigation financially accessible. Document every violation carefully: keep copies of collection notices, record dates and times of calls, save threatening letters, and note any false statements about debt amounts or threats of criminal charges. These records become your evidence in court. Hays Cauley, P.C. is a consumer protection law firm dedicated to helping consumers with credit reporting, identity theft, and debt-related issues and can evaluate whether your situation warrants legal action.

Final Thoughts

Your rights under the Fair Credit Reporting Act are real and enforceable, and South Carolina law protects you from harassment, false statements, and inaccurate credit reporting. When a debt collector harasses you through repeated calls, misrepresents the debt amount, or reports false information to credit bureaus, you have concrete debt collection remedies SC available to stop the violations and recover damages. Start by documenting every violation: save collection notices, record call dates and times, keep threatening letters, and note any false statements about the debt.

Dispute inaccurate information with the credit bureau in writing within 30 days, send a cease and desist letter by certified mail, and consider whether legal action fits your situation. Under the FDCPA, you can recover actual damages plus up to $1,000 in statutory damages per violation, along with court costs and attorney’s fees, which means pursuing these remedies does not require you to pay out of pocket. Many violations are straightforward to prove, and collectors often settle quickly rather than face the cost of litigation.

If you believe a debt collector has violated your rights, contact Hays Cauley, P.C. to discuss your situation and determine whether your case warrants legal action. We at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia, and Charleston, fight back against illegal collection practices and protect their financial futures. You do not have to handle this alone.