Debt collector harassment in SC is illegal, yet thousands of South Carolina residents face relentless calls, threats, and false claims every year. The Fair Debt Collection Practices Act and state laws give you real protections, but many people don’t know how to use them.

We at Hays Cauley, P.C. help residents fight back against abusive collectors and reclaim their peace of mind. This guide shows you exactly what harassment looks like, what rights you have, and how to stop it.

What Counts as Harassment Under South Carolina Law

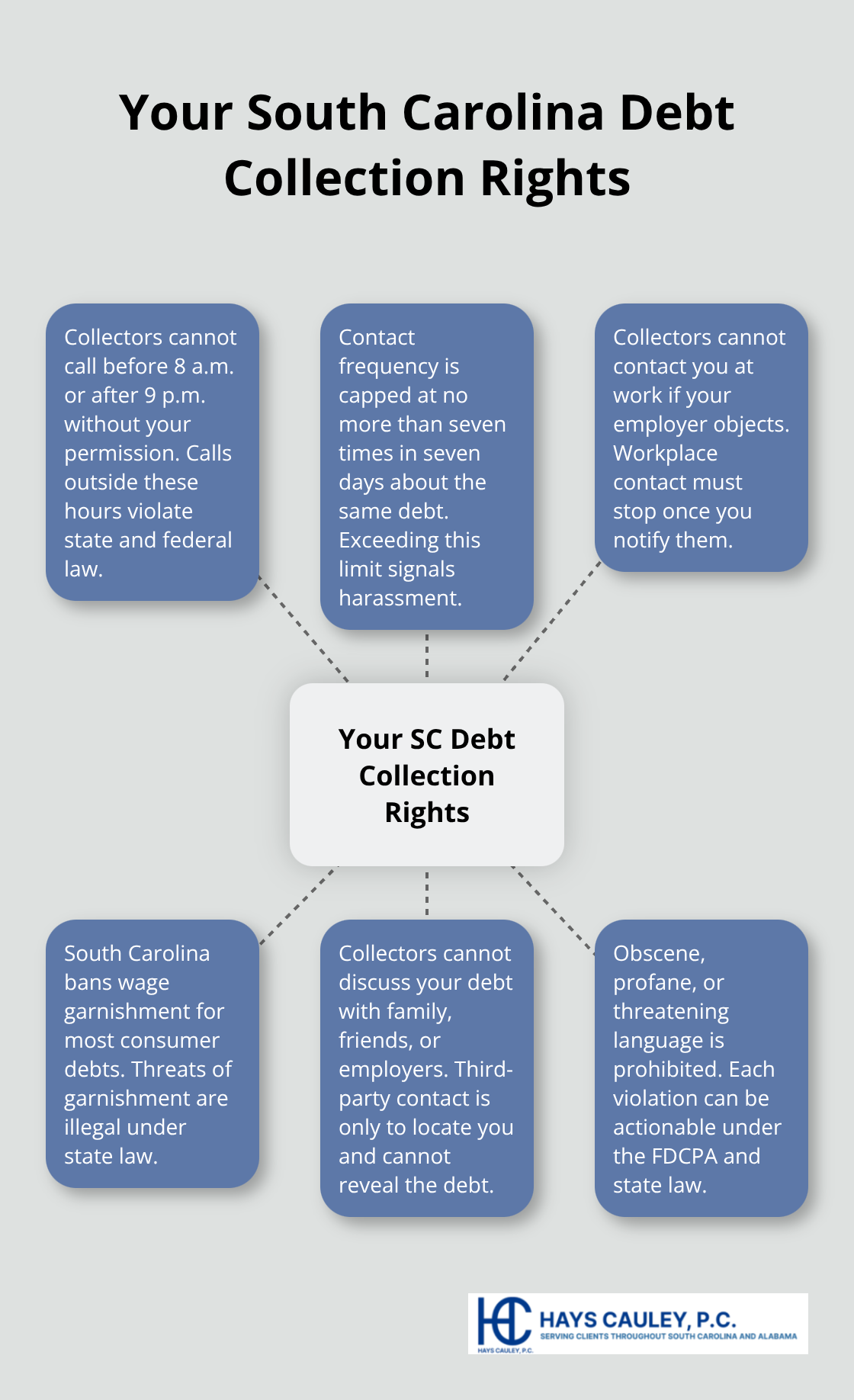

Debt collector harassment isn’t always obvious. South Carolina law and the Fair Debt Collection Practices Act draw clear lines around what collectors can and cannot do, and crossing those lines exposes them to legal liability. Collectors cannot call you before 8 a.m. or after 9 p.m. without your permission, and they cannot contact you more than seven times in seven days about the same debt. If you work somewhere your employer disapproves of collection calls, they cannot contact you there. South Carolina law goes further than federal protections by explicitly banning wage garnishment for most consumer debts, which means threats of wage garnishment are not just aggressive-they are illegal. Collectors also cannot contact your family, friends, employer, or anyone else to discuss your debt; they can only contact third parties to locate you, and even then, they cannot reveal the purpose of the call. Under South Carolina Code Section 37-5-107(b), repeated calls intended to annoy, abuse, or harass you violate state law and create grounds for damages.

False Claims and Deceptive Tactics Expose Collectors to Liability

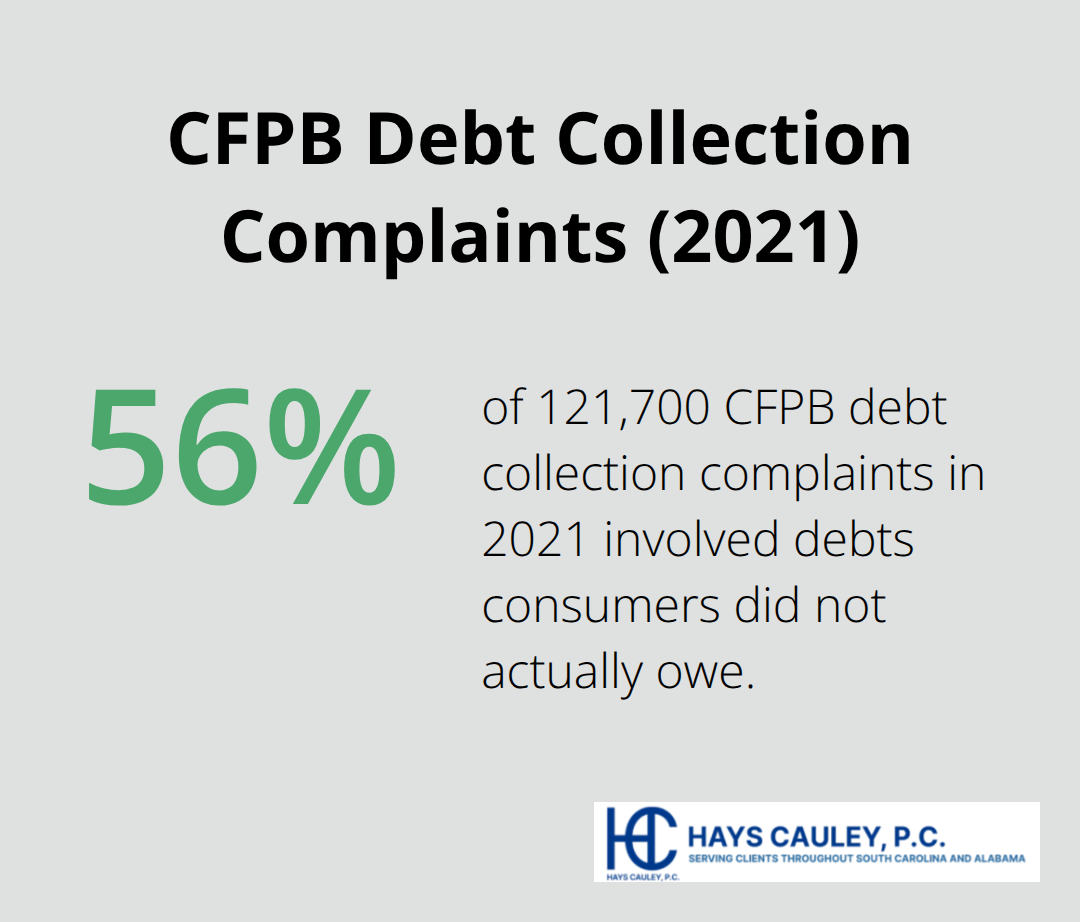

Collectors frequently misrepresent their identity, authority, and your obligations. They cannot claim to be attorneys, government representatives, or law enforcement officers when they are not. They cannot falsely state the amount you owe, misrepresent the involvement of an attorney, or send documents designed to look like official court papers when they are not. The Consumer Financial Protection Bureau received 121,700 debt collection complaints in 2021, and 56 percent of those involved debts consumers did not actually owe-a stark reminder that wrongful targeting remains endemic. South Carolina courts view these deceptions seriously because they undermine your ability to exercise your rights.

Threats of arrest, criminal prosecution, or property seizure violate federal law; collectors cannot threaten consequences they do not actually intend to pursue or do not have the legal authority to carry out.

Abusive Language and Intimidation Tactics Violate State and Federal Law

Collectors cannot use obscene, profane, or abusive language when communicating with you. They cannot threaten violence or imply threats of violence. They cannot use caller ID spoofing, repeated hang-ups, or other methods designed to harass. Collectors also cannot force collect calls on you or charge you fees beyond what you legitimately owe. South Carolina law specifically addresses unconscionable debt collection practices under Section 37-5-108, which means courts can find a collection effort unenforceable if the collector’s conduct shows a likelihood of violence or other egregious tactics. Each violation-each prohibited call, each false statement, each threat-counts as a separate violation under the FDCPA. This matters because willful violations carry statutory damages of $100 to $1,000 per violation, and damages accumulate quickly when a pattern of harassment exists.

How Violations Stack Up and Create Legal Exposure

A single call outside permitted hours counts as one violation. Eight calls in a week counts as at least one violation. Add a wage-garnishment threat and a third-party contact, and you have multiple actionable violations. Courts focus on patterns of harassment because they reveal intent and demonstrate that the collector’s conduct was not accidental or isolated. When you document each violation and report them to authorities, you build a record that strengthens your legal position. The next section covers your rights as a debtor and the specific steps you can take to stop the harassment before it escalates further.

Your Rights as a Debtor in South Carolina

South Carolina law and federal protections give you more power than most people realize. The Fair Debt Collection Practices Act sets a federal floor for your rights, but South Carolina built additional protections on top of it that directly benefit you. Collectors cannot call before 8 a.m. or after 9 p.m., cannot contact you more than seven times in seven days about the same debt, and cannot reach you at work if your employer objects. More importantly, South Carolina Code Section 37-5-107 prohibits collectors from using obscene language, threatening violence, or contacting your family and friends to discuss your debt. The state goes further than federal law by banning wage garnishment for most consumer debts, which means threats of wage garnishment are illegal-period.

The Five-Day Notice and Your 30-Day Window

Within five days of first contact, collectors must send you written notice showing the exact amount owed, the creditor’s name, and your right to dispute. This notice matters because it gives you a 30-day window to request written verification of the debt, and once you do, collectors must stop all collection efforts until they provide proof you actually owe it. If the debt is not yours or the amount is wrong, the burden falls on the collector to prove otherwise, not on you to prove your innocence. The notice also includes a tear-off form that allows you to dispute or request more information in writing.

How Debt Verification Stops Harassment

Requesting debt verification is your strongest immediate tool. Send a certified letter to the collector requesting written proof that you owe the debt and that they have the legal right to collect it. The verification must include the original creditor, your current balance, a breakdown of interest and fees, and the collector’s contact information. Many collectors cannot provide legitimate verification because they purchased the debt as a third party without complete documentation, and when they cannot verify, they must stop contacting you.

The Consumer Financial Protection Bureau data from 2021 showed that 56 percent of the 121,700 debt collection complaints involved debts consumers did not actually owe, which means requesting verification protects you from wrongful collection. Keep copies of everything you send and use certified mail with return receipt to prove delivery. Once you send this letter, document the date you mailed it and what you requested. If the collector continues contacting you after receiving your verification request, that violation alone can support a lawsuit for damages.

Building Your Paper Trail

Documentation transforms your situation from a he-said-she-said dispute into a legal record. Write down the collector’s name, company, phone number, date, time, and exact statements from each call. Save all letters, voicemails, text messages, and screenshots in order. This paper trail proves patterns of harassment and shows that violations were not accidental or isolated incidents. Courts focus on documented patterns because they reveal the collector’s intent and demonstrate systematic abuse rather than one-off mistakes.

When you combine verification requests with thorough documentation and certified mail receipts, you create evidence that strengthens your legal position significantly. The next section shows you exactly how to formalize your demand that collectors stop all contact and what to do when they ignore it.

How to Stop Collectors From Contacting You

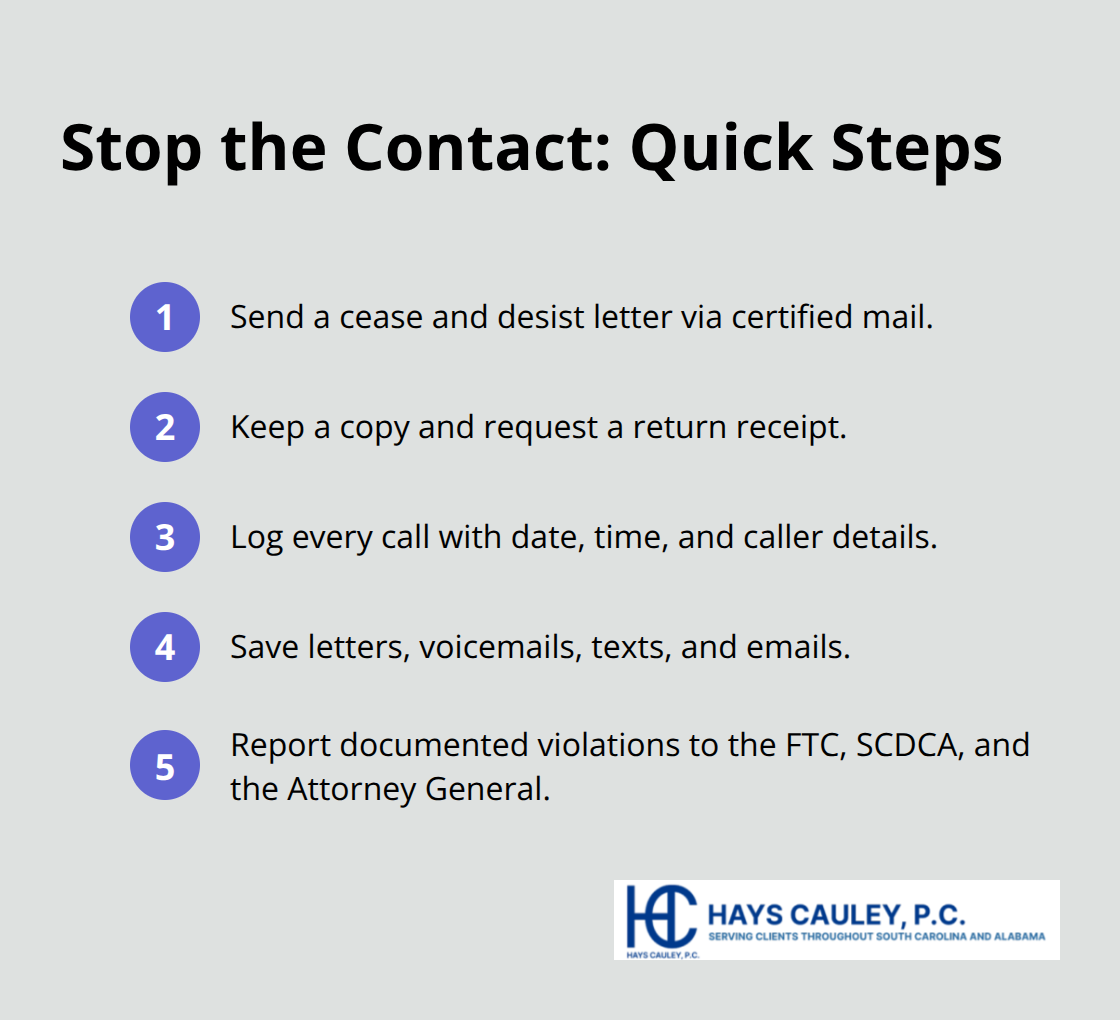

Your written demand to stop all contact is the legal line collectors cannot cross. The moment you send a cease and desist letter via certified mail, collectors must stop calling, emailing, and mailing you-with only two narrow exceptions: they can acknowledge receipt of your letter or notify you that they intend to file a lawsuit. This is not a suggestion or courtesy; it is a legal requirement under the FDCPA. Send your letter to the collector’s address shown on any documentation they provided, keep a copy for yourself, and request a return receipt so you have proof of delivery.

Why Collectors Ignore Cease and Desist Letters and What That Costs Them

Many collectors ignore cease and desist letters, and when they do, each subsequent contact after receiving your letter becomes a separate, documented violation worth $100 to $1,000 in statutory damages. The Federal Trade Commission emphasizes that this tool is one of the most effective ways to establish a clear boundary and create ironclad evidence of ongoing violations if the collector persists. A collector who receives your certified letter and then calls you three more times has just created three additional violations, each one actionable in court.

Build Your Documentation Record

Write down the date, time, caller’s name, company name, phone number, and the exact words used during each call-particularly any threats, false claims, or abusive language. Save every letter, voicemail, text message, and email in chronological order. Take screenshots of text messages and online communications immediately. This creates a timeline that proves pattern and intent, which courts use to calculate damages.

Report Violations to Authorities

Once you have documented violations, report them to the Federal Trade Commission at consumerfinance.gov, the South Carolina Department of Consumer Affairs at 800-922-1594 (toll-free) or scdca@scconsumer.gov, and your state Attorney General. These complaints create an official record that agencies use to identify patterns of abuse across multiple consumers and can trigger enforcement actions against the collector. If a collector calls eight times in seven days and makes a wage garnishment threat after you sent a cease and desist letter, you have documented multiple violations with agency complaints on file-a combination that gives you substantial leverage in settlement negotiations or litigation.

How Documentation Strengthens Your Position

Your paper trail transforms a he-said-she-said dispute into a legal record. When you combine a cease and desist letter with thorough documentation and certified mail receipts, you create evidence that substantially strengthens your legal position. Hays Cauley, P.C., a consumer protection law firm dedicated to helping consumers with debt-related issues, reviews these records to build strong cases for clients throughout South Carolina, including Greenville, Columbia and Charleston.

Final Thoughts

Willful FDCPA violations carry statutory damages of $100 to $1,000 per violation, and each call, threat, or false statement counts separately. When a collector contacts you after receiving your cease and desist letter, each subsequent contact adds to your damages. You can file a lawsuit in state or federal court within one year of the violation and recover damages, court costs, and attorney’s fees.

Debt collector harassment SC cases turn on the strength of your documentation and the clarity of your written demands. Many collectors exploit consumers who lack knowledge of their rights or fail to document violations. When you take both steps, you shift the power dynamic entirely and force collectors to answer for their conduct.

We at Hays Cauley, P.C. help consumers fight back against abusive collectors through thorough case review and aggressive legal action. If harassment continues despite your efforts to stop it, contact Hays Cauley, P.C. to discuss your situation and explore your legal options. We serve South Carolina, including Greenville, Columbia and Charleston, and we know the state and federal laws that protect you.