Debt collectors in South Carolina often cross the line, using intimidation and harassment to pressure people into paying. The Fair Debt Collection Practices Act gives you legal protections, but many people don’t know what rights they actually have.

At Hays Cauley, P.C., we help South Carolina residents fight back against illegal collection tactics. This guide walks you through your debt collection rights in SC and shows you exactly what to do if a collector harasses you.

What the Fair Debt Collection Practices Act Actually Protects, Serving South Carolina, Including Greenville, Columbia and Charleston

Federal Boundaries on Debt Collector Behavior

The Fair Debt Collection Practices Act sets hard boundaries on how debt collectors can treat you, and South Carolina law adds even stronger protections on top of that. Federal law prohibits debt collectors from harassing, deceiving, or abusing you, but understanding the specific rules matters because violations give you a legal claim for damages. The act covers personal, family, and household debts including auto loans, medical bills, and charge accounts. Debt collectors cannot contact you before 8 a.m. or after 9 p.m., and they cannot reach you at work if your employer objects. They also cannot call you more than seven times in seven days about the same debt.

What Collectors Must Tell You in Writing

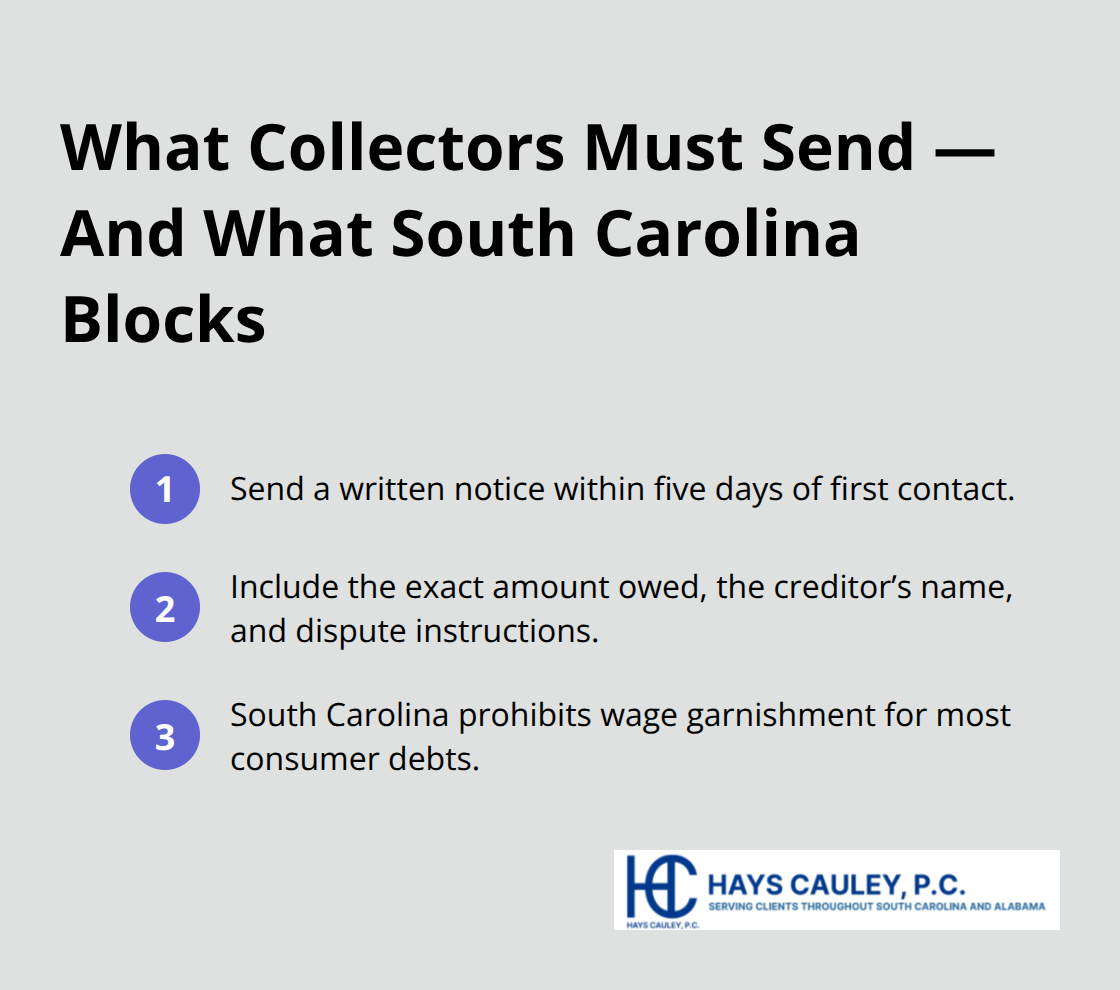

Within five days of their first contact, collectors must send you a written notice showing the exact amount owed, the creditor’s name, and instructions for disputing the debt. South Carolina goes further by prohibiting wage garnishment for most consumer debts, which means collectors cannot seize your paycheck even if they win a judgment against you. This state-level protection shields your income from aggressive collection tactics that remain legal in other states.

The Debt Validation Right: Your Strongest Tool

You have about 30 days from first contact to request written verification of the debt, and once you make that request in writing, collection efforts must stop until the collector provides proof. The verification must include the original creditor, current balance, a breakdown of interest and fees, and the collector’s contact information. If the debt isn’t yours or the amount is wrong, send a written dispute using Consumer Financial Protection Bureau templates and keep copies of everything. The Consumer Financial Protection Bureau reported in 2021 that 121,700 people filed debt collection complaints, with 56 percent involving debts consumers didn’t actually owe, showing that wrongful targeting happens regularly.

Building Your Paper Trail

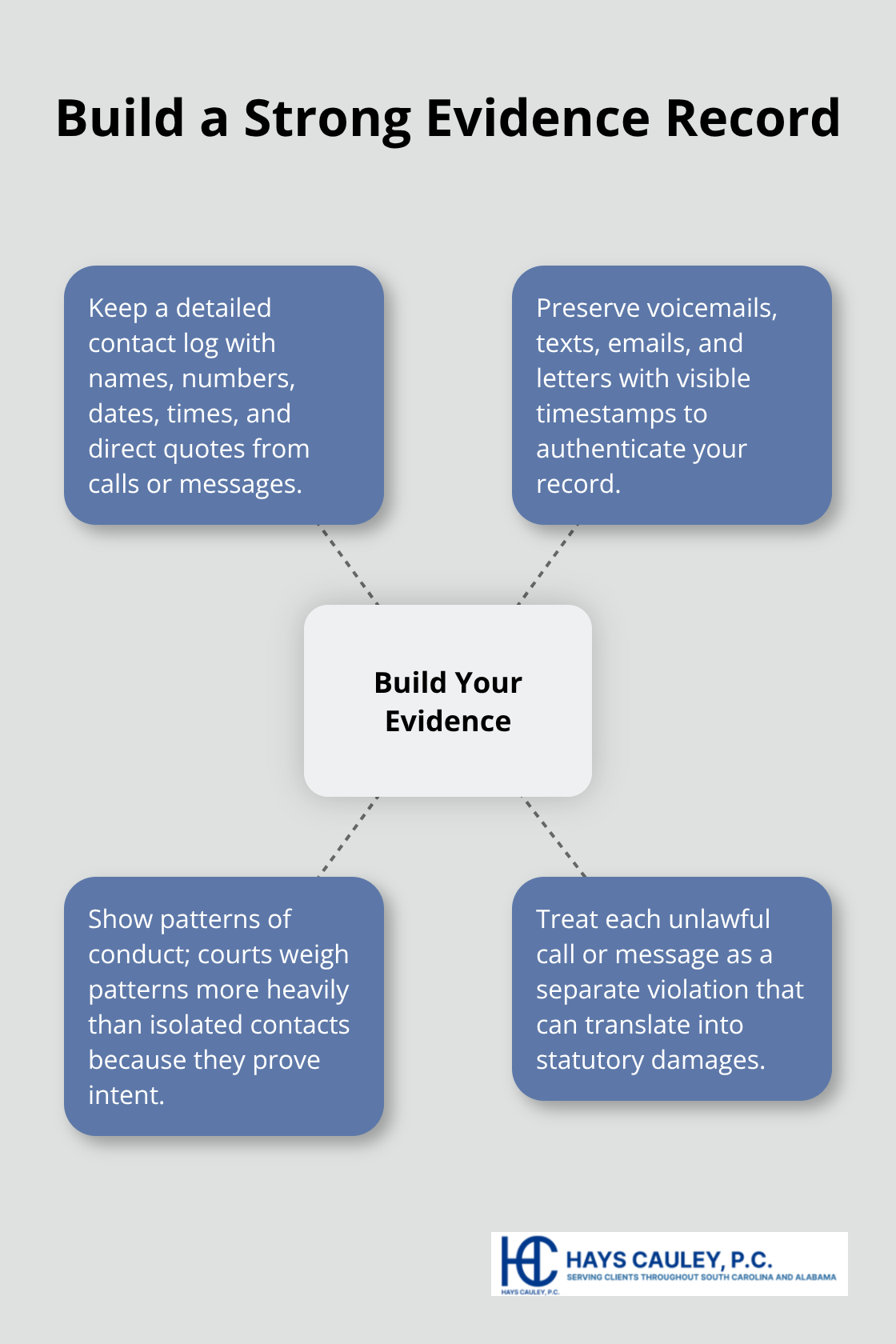

You can send a cease-and-desist letter via certified mail with return receipt requested, after which collectors can only acknowledge receipt or notify you of specific legal action like a lawsuit. Document every contact by maintaining a detailed log with the collector’s name, phone number, date, time, and exact statements they made. Save letters, voicemails, texts, and screenshots in chronological order to show patterns of violations rather than isolated incidents. This documentation becomes critical when you need to prove that a collector violated your rights.

How Debt Collectors Break the Law in South Carolina

Excessive Calling and Validation Violations

Debt collectors use predictable tactics to wear you down, and most of them violate federal law or South Carolina state protections. Repeated calling stands out as one of the most common violations we see. The FDCPA prohibits more than seven calls about the same debt within seven days, but collectors ignore this rule entirely, making ten or fifteen calls in a single week to pressure you into paying. Each call counts as a separate violation, which means a collector who calls you eight times in seven days has already committed one violation that can trigger statutory damages.

The moment you request debt validation in writing, all collection calls must stop until the collector sends proof of the debt. Yet many collectors keep calling anyway. This continued contact after a validation request is an intentional violation that courts take seriously. When a collector receives your written validation demand and ignores it, that collector has crossed into territory that exposes them to significant liability.

False Threats About Legal Consequences

Collectors frequently claim they will garnish your wages, seize your property, or have you arrested if you don’t pay immediately. In South Carolina, wage garnishment for consumer debts is prohibited by state law, so any threat to garnish your wages is a direct lie. Collectors also threaten lawsuits they have no intention of filing, claim they work for government agencies when they don’t, and falsely state they are attorneys.

These false statements violate the FDCPA because they deceive you into paying money you might not legally owe. A collector who threatens arrest for a debt violation commits a separate violation for each false statement made. Courts recognize that such threats cause real harm-they create fear and pressure that push people to pay debts they may have valid defenses against.

Illegal Contact With Third Parties

Contacting your employer, family members, or friends crosses another clear legal line. The FDCPA allows collectors to contact third parties only to locate you, and they cannot discuss your debt with anyone except you and your attorney. When a collector calls your boss and mentions the debt, or tells your neighbor about money you owe, that conversation is an illegal violation that damages your reputation and privacy.

South Carolina residents harassed this way have the right to file a lawsuit and recover actual damages plus statutory damages ranging from one hundred to one thousand dollars per violation. The more violations a collector commits, the higher your potential recovery becomes, which is why documenting each call, message, and improper contact matters so much. Building a strong record of these violations positions you to hold collectors accountable and recover compensation for the harm they cause.

Building Your Evidence Against Debt Collectors, Serving South Carolina, Including Greenville, Columbia and Charleston

Start Your Documentation Log Today

Documentation wins debt collection cases. Debt collectors count on people forgetting what was said, when calls came in, or how many times they contacted you. Start a detailed log immediately when harassment begins. Write down the collector’s name, the company they claim to work for, the phone number they called from, the exact date and time of contact, and word-for-word statements they made. If a collector threatens to garnish your wages, arrest you, or seize your property, record those exact words in your log. If they claim to be an attorney or government official, note that too.

Preserve Every Communication

Save every voicemail, text message, email, and letter in chronological order with dates clearly marked. Screenshot text messages and emails so the timestamp remains visible. This chronological record becomes your strongest evidence because it shows a pattern of violations rather than a single incident.

Courts care far more about patterns than isolated contacts because patterns prove intent to harass or deceive. Each call, message, or improper contact counts as a separate violation under federal law, so your detailed log directly translates into potential damages.

File Complaints With Government Agencies

File a complaint with the Consumer Financial Protection Bureau at consumerfinance.gov as soon as you have documented multiple violations. The CFPB received 121,700 debt collection complaints in 2021 alone, and your complaint helps regulators identify collectors who repeatedly break the law. Include your documentation log, copies of letters and notices, and transcripts of voicemail messages in your complaint. The CFPB shares complaint data with law enforcement, so your report contributes to investigations that can shut down repeat violators. Next, contact the South Carolina Department of Consumer Affairs to report the violations. South Carolina Code Section 37-5-107 makes fraudulent and deceptive debt collection practices unlawful at the state level, giving you additional legal grounds beyond federal law. Provide the same documentation to the Attorney General’s office. These complaints create an official record that supports your legal claim if you decide to file a lawsuit.

Calculate Your Potential Damages

Willful violations under the FDCPA result in statutory damages of one hundred to one thousand dollars per violation, and each call, message, or improper contact counts separately. Your detailed log determines how many separate violations you can prove, which directly affects the amount you can recover. A collector who calls you eight times in seven days (one violation), threatens wage garnishment (another violation), and contacts your employer (yet another violation) has already created three separate claims. When you have documented violations and filed complaints, contact Hays Cauley, P.C. at 843-665-1717 for a free consultation to review your documentation and identify which violations carry the strongest claims.

Final Thoughts

Once you have documented violations and filed complaints with the Consumer Financial Protection Bureau and South Carolina Department of Consumer Affairs, you have built a foundation for legal action. A cease-and-desist letter sent via certified mail with return receipt requested tells the collector to stop all contact immediately. After receiving your letter, collectors can only acknowledge receipt or notify you of specific legal action like a lawsuit.

When a collector ignores your cease-and-desist letter and continues calling, texting, or writing, that ongoing harassment strengthens your legal position significantly. Each contact after your letter counts as a separate violation, which multiplies your potential damages. This is why sending the letter via certified mail matters-you have proof the collector received it, which eliminates any claim they did not know you wanted them to stop.

At this stage, working with Hays Cauley, P.C. transforms your documentation into a lawsuit that holds collectors accountable and protects your debt collection rights SC. Hays Cauley, P.C. offers free initial consultations and handles many cases on a contingency basis, meaning you pay nothing unless you win. Contact them at 843-665-1717 to review your documentation and discuss your options.