Dealing with Inaccurate Information in Your Credit Report in South Carolina

Credit reports play a vital role in your financial life, but what happens when they contain errors? At Hays Cauley, P.C., we understand the frustration and potential harm caused by inaccurate information in credit reports.

The Fair Credit Reporting Act (FCRA) provides protection against inaccurate information in your credit report, but many South Carolina residents are unaware of their rights. This blog post will guide you through the process of identifying and disputing errors, helping you maintain a healthy financial profile.

What’s in Your South Carolina Credit Report?

The Anatomy of a Credit Report

A credit report serves as a financial biography for South Carolina residents. It contains a detailed record of your credit history, which lenders, employers, and landlords use to assess your financial reliability. This document includes your personal information, credit account details, inquiry records, and relevant public records.

Key Components of Your Credit Report

- Personal Information: Your name, address, and Social Security number

- Credit Account Details: Current and past credit cards, loans, and payment histories

- Inquiry Records: A list of entities that have checked your credit

- Public Records: Information on bankruptcies or tax liens (if applicable)

Common Errors That Can Damage Your Score

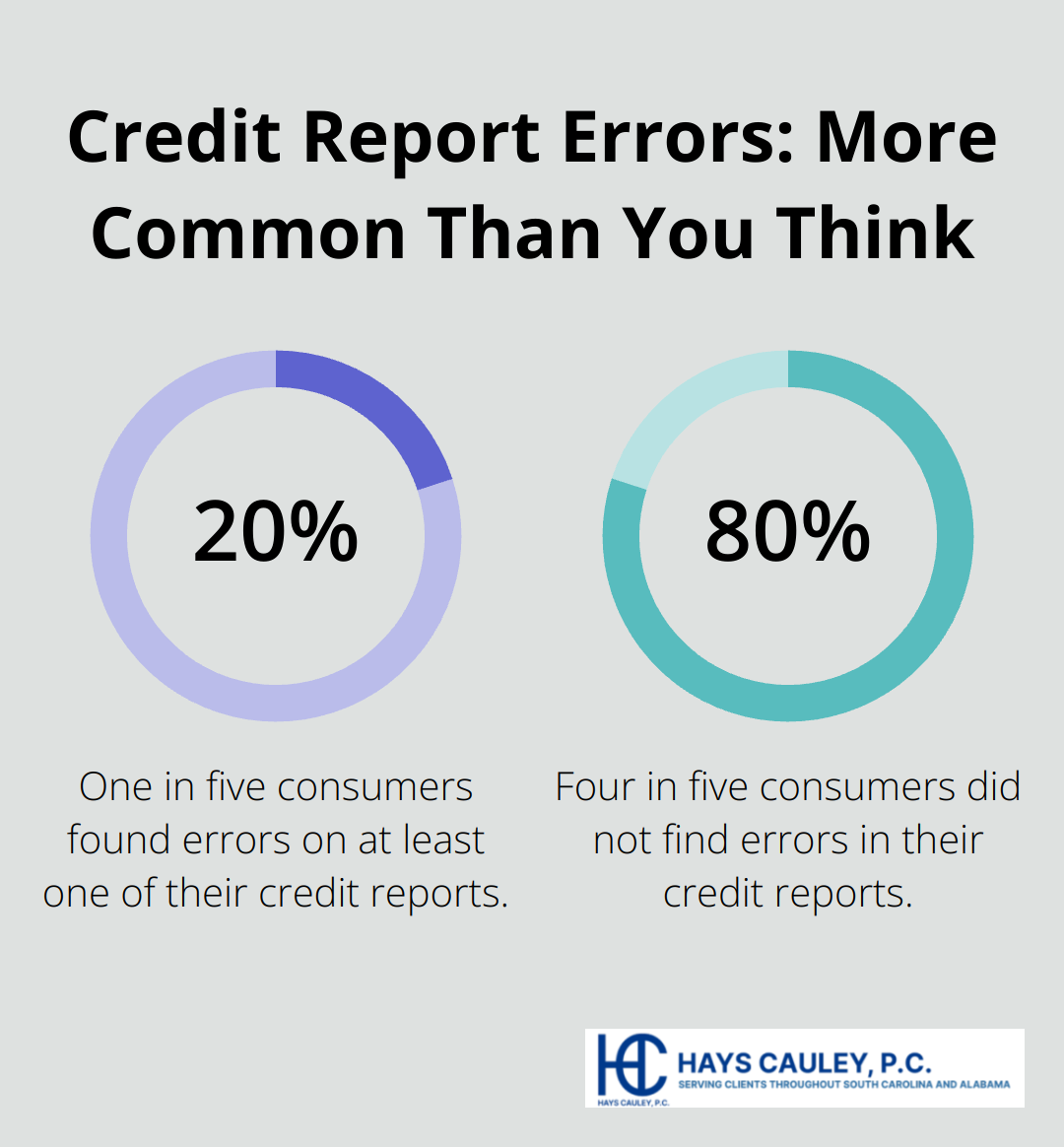

Credit report inaccuracies occur more frequently than most people realize. A Federal Trade Commission study revealed that one in five consumers found errors on at least one of their credit reports. These mistakes range from minor issues (like misspelled names) to major problems (such as accounts falsely reported as delinquent).

Frequent errors include:

- Outdated information that should no longer appear

- Accounts belonging to individuals with similar names

- Incorrect account balances or credit limits

- Closed accounts reported as open

- Duplicate listings of the same debt

The Financial Consequences of Credit Report Mistakes

Errors in your credit report can significantly impact your financial health. A lower credit score resulting from these mistakes can lead to:

- Higher interest rates on loans

- Denied credit applications

- Lost job opportunities

For example, a single late payment incorrectly reported can reduce your credit score by up to 110 points. This drop could potentially cost you thousands of dollars in higher interest rates over the life of a mortgage.

In South Carolina, where the average credit score is 681 (according to Experian’s 2024 State of Credit report), even a small decrease can push you below the “good” credit threshold. This change limits your financial options and can affect your ability to secure favorable terms on loans or credit cards.

The prevalence of these errors and their potential impact underscores the importance of regularly reviewing your credit reports. You should take immediate action if you spot any inaccuracies. In the next section, we’ll explore your rights under the Fair Credit Reporting Act and how you can use them to protect your financial future in South Carolina.

Your FCRA Rights in South Carolina

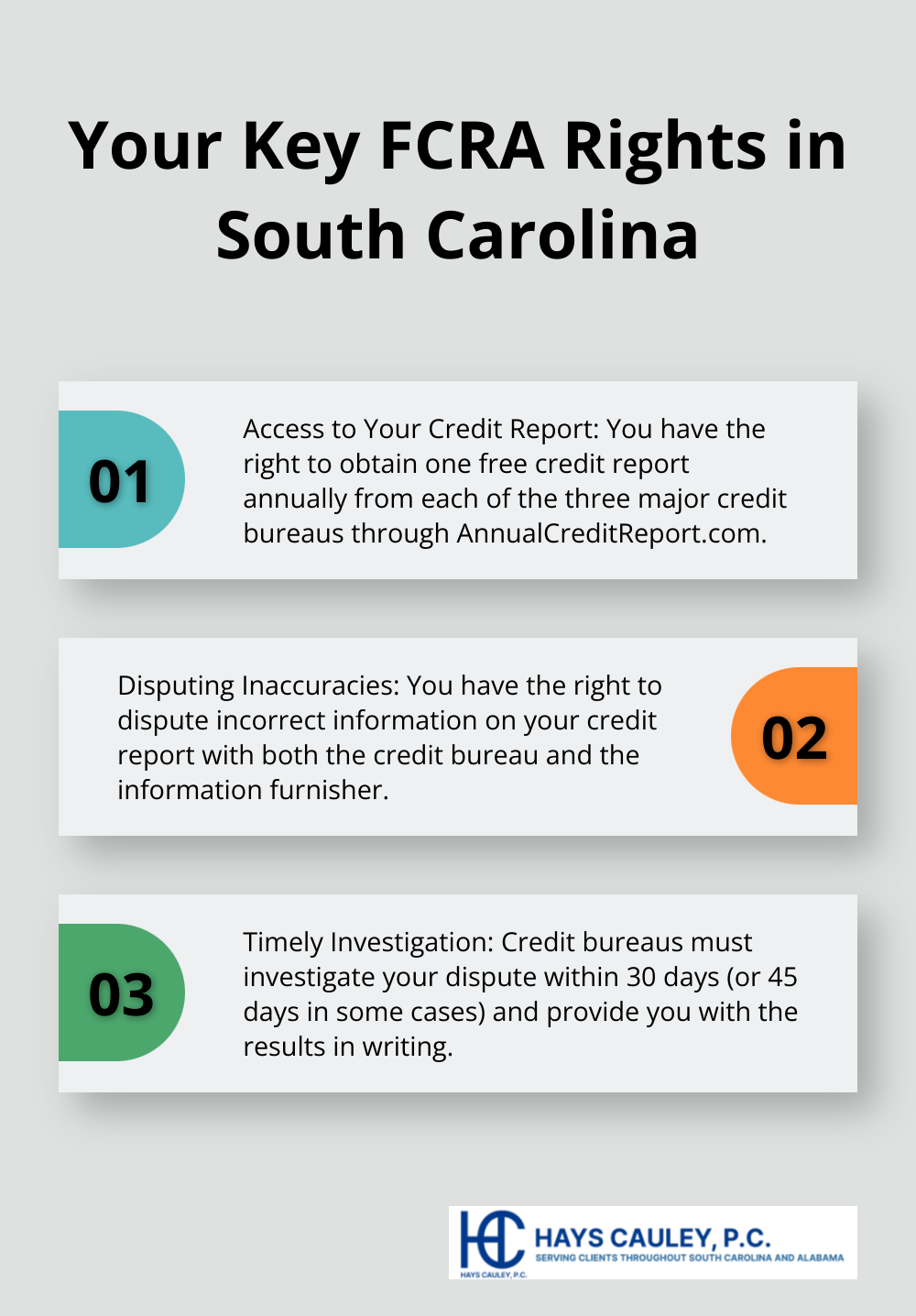

Access to Your Credit Report

The Fair Credit Reporting Act (FCRA) provides South Carolina residents with essential protections for their credit information. This federal law grants you the right to obtain one free credit report annually from each of the three major credit bureaus (Equifax, Experian, and TransUnion) through annualcreditreport.com. This free access allows you to review your credit information regularly and identify potential errors.

Disputing Inaccuracies

If you find incorrect information on your credit report, the FCRA empowers you to dispute it. You can file a dispute directly with the credit bureau or the company that provided the information (known as the furnisher). For maximum effectiveness, you should dispute with both parties.

When you file a dispute, you must:

- Specify the information you believe is incorrect

- Explain why you think it’s inaccurate

- Include supporting documentation (e.g., payment receipts or bank statements)

Time Limits for Investigation

Credit bureaus must investigate your dispute within 30 days of receipt. This period can extend to 45 days if you provide additional relevant information during the initial 30-day window. The credit bureau must forward all pertinent data about the dispute to the furnisher, who must then investigate and report back to the credit bureau.

If the investigation results in a change to your credit report, the credit bureau must provide you with:

- The results in writing

- A free copy of your updated credit report (This doesn’t count as your annual free report)

Protection Against Outdated Information

The FCRA limits how long negative information can remain on your credit report. Most negative information should disappear after seven years. However, certain types of bankruptcies can stay for up to 10 years. South Carolina residents should ensure that old negative items are removed when they should be.

Right to Know Who Accessed Your Report

The FCRA gives you the right to know who has accessed your credit report in the last two years for employment purposes, and in the last year for any other purpose. This information (included in your credit report) can help you identify potential unauthorized access or identity theft.

Understanding and exercising your FCRA rights is vital for maintaining accurate credit reports and protecting your financial health in South Carolina. In the next section, we’ll outline the steps you can take to dispute inaccurate information effectively and assert your rights under the FCRA.

How to Dispute Credit Report Errors in South Carolina

Obtain Your Free Credit Reports

Start your process by requesting free credit reports from annualcreditreport.com. This website serves as the only authorized source for free annual reports from Equifax, Experian, and TransUnion. As of 2025, South Carolina residents can access their reports weekly at no cost. Use this opportunity to monitor your credit regularly.

Identify Errors in Your Reports

After you receive your reports, review them thoroughly. Look for discrepancies in personal information, account details, and payment histories. Focus on:

- Accounts you don’t recognize

- Incorrect balances or credit limits

- Late payments you believe were on time

- Negative information older than seven years (except for certain bankruptcies)

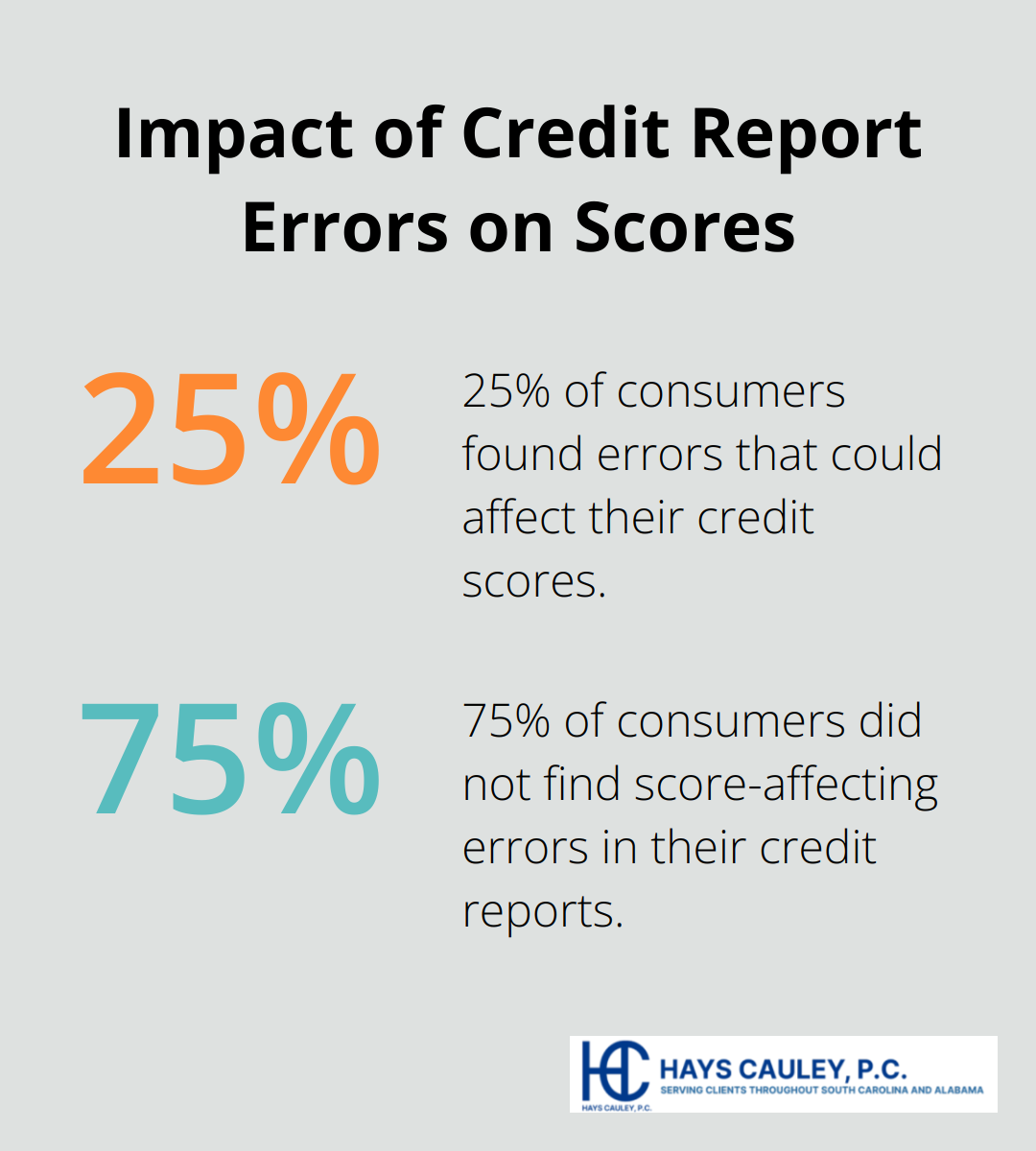

A 2024 Federal Trade Commission study revealed that 25% of consumers found errors that could affect their credit scores. Don’t ignore seemingly minor issues-they can have significant impacts.

Collect Supporting Evidence

For each error you find, gather supporting documentation. This might include bank statements, canceled checks, or correspondence with creditors. Create a file for each dispute and organize your evidence clearly. This preparation will strengthen your case and speed up the resolution process.

Submit Your Dispute

You can file disputes online, by mail, or by phone. However, sending disputes via certified mail with return receipt requested often proves most effective. This method provides a paper trail and proof of receipt, which can be crucial if further action becomes necessary.

When you file your dispute:

- Write a clear, concise letter explaining each error

- Include copies (not originals) of your supporting documents

- Provide your contact information and report details

Send your dispute to both the credit bureau and the information furnisher. The Consumer Financial Protection Bureau offers template letters on their website to help you craft your dispute.

Monitor and Follow Up

Mark your calendar for 30 days from the date you file your dispute. Credit bureaus must investigate and respond within this timeframe (45 days in some cases). If you don’t receive a response, follow up promptly.

If the bureau confirms an error, they must provide you with a free, updated copy of your credit report. Review this carefully to ensure all corrections appear accurately.

Persistence proves key in this process. If your initial dispute fails, you have the right to add a brief statement to your credit report explaining your side of the story. You can also contact us to seek legal assistance.

A 2024 study by the National Consumer Law Center found that 70% of consumers who persistently disputed errors saw improvements in their credit reports within six months. This statistic underscores the importance of diligent follow-up in the dispute process.

Final Thoughts

Accurate credit reports form the foundation of financial well-being in South Carolina. Errors can result in higher interest rates and denied loan applications. You should review your credit reports at least once a year to catch and address any inaccuracies promptly. This practice will minimize potential impacts on your credit score and overall financial health.

The Fair Credit Reporting Act protects consumers against inaccurate information in credit reports. However, dealing with credit report errors often proves complex and time-consuming. You don’t have to navigate this process alone (we can help you address these issues effectively).

We at Hays Cauley, P.C. have helped many South Carolina residents with credit reporting issues. Our team can guide you through the dispute process and work to resolve Fair Credit Reporting Act inaccurate information problems. Your credit report reflects your financial responsibility, and we strive to keep it accurate for your future financial success in South Carolina.