Can You Sue Under the Fair Credit Reporting Act in South Carolina?

Credit report errors can wreak havoc on your financial life. At Hays Cauley, P.C., we often see South Carolina residents struggling with inaccurate information on their credit reports.

The Fair Credit Reporting Act (FCRA) provides powerful protections for consumers, including the right to dispute errors and seek compensation through a Fair Credit Reporting Act lawsuit. This federal law applies to all South Carolinians and offers a way to fight back against credit reporting mistakes.

What Does the Fair Credit Reporting Act Mean for South Carolinians?

Key Protections Under the FCRA

The Fair Credit Reporting Act (FCRA) is a federal law that sets rules for how credit reporting agencies handle your personal information. This law provides important protections and rights for South Carolina residents regarding their credit reports.

The FCRA requires credit reporting agencies to follow strict guidelines to maintain the accuracy and privacy of your credit information. Companies like Equifax, Experian, and TransUnion cannot add any information they want to your credit report. They must verify the accuracy of the data they receive and update it regularly.

Your Right to Access Your Credit Report

One of the most significant rights the FCRA grants is the ability to obtain a free copy of your credit report from each of the three major credit bureaus once every 12 months. This allows you to review your credit information and identify any potential errors or fraudulent activity. You can get your free reports at annualcreditreport.com (the only federally authorized website for this purpose).

Disputing Errors on Your Credit Report

The FCRA gives you the right to dispute inaccuracies on your credit report. Credit reporting agencies must investigate these disputes within 30 days (45 days in some cases) and correct any errors they find. This process is free, and you can start it by contacting the credit bureau directly or the company that provided the incorrect information.

Impact of Credit Report Errors

Credit report errors can significantly affect South Carolina residents. These mistakes can lead to serious financial consequences, such as:

- Loan denials

- Higher interest rates

- Difficulty renting an apartment

- Challenges in securing employment

Taking Action Against FCRA Violations

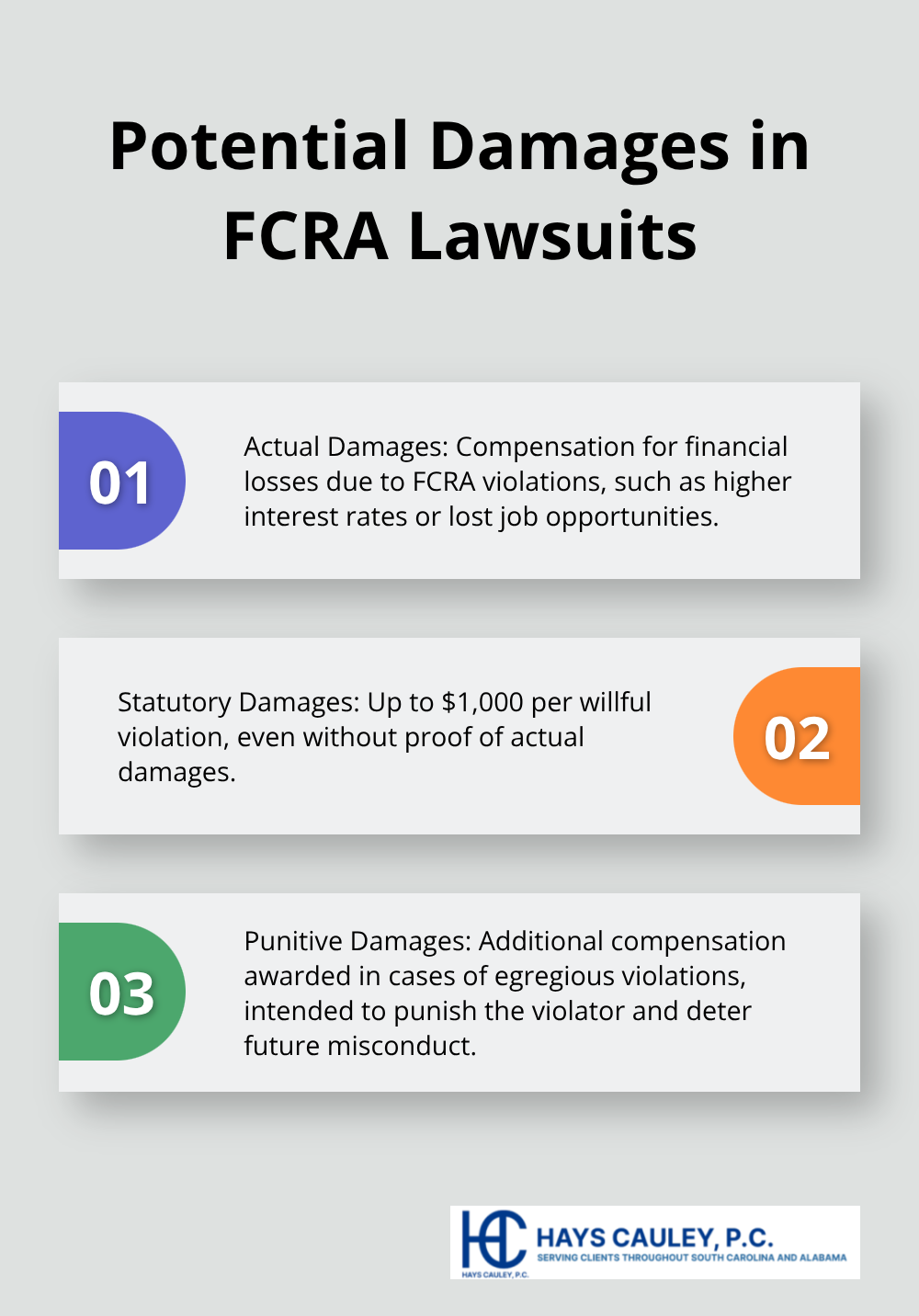

If a credit reporting agency or a furnisher of information (e.g., a creditor) violates your rights under the FCRA, you may have grounds for legal action. The FCRA allows consumers to sue for damages in federal court. Potential remedies include:

- Actual damages (financial losses you’ve suffered)

- Statutory damages (up to $1,000 per violation)

- Punitive damages (in cases of willful noncompliance)

- Attorney’s fees and court costs

Understanding your rights under the FCRA is the first step in protecting your credit and financial well-being. The next section will explore common FCRA violations that South Carolina residents might encounter and how to identify them.

Common FCRA Violations That Harm South Carolina Consumers

The Fair Credit Reporting Act (FCRA) protects South Carolina residents from unfair credit reporting practices. However, violations occur frequently, causing financial hardship and stress for many consumers. Here are some of the most prevalent FCRA violations in South Carolina:

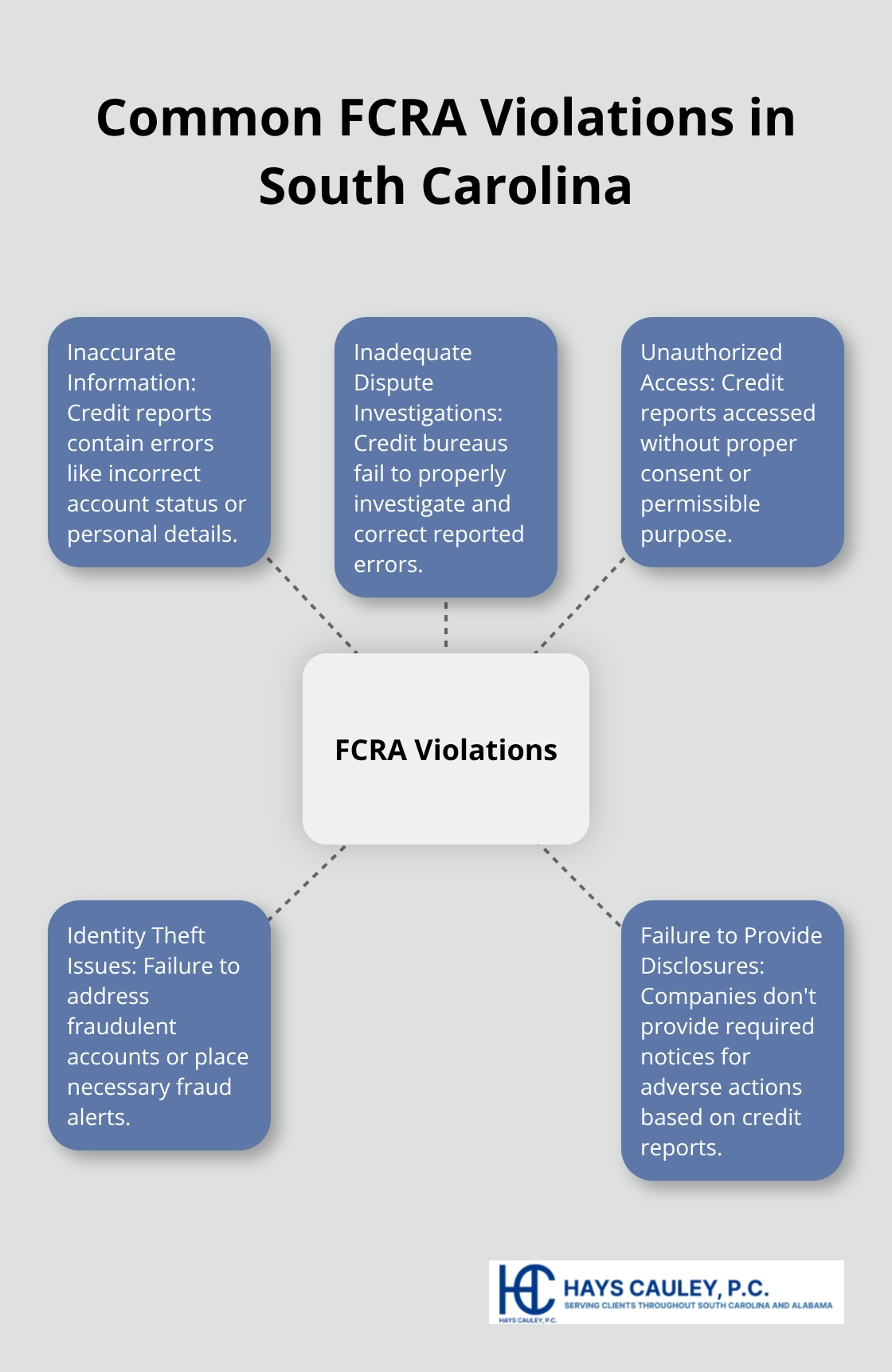

Inaccurate Information in Credit Reports

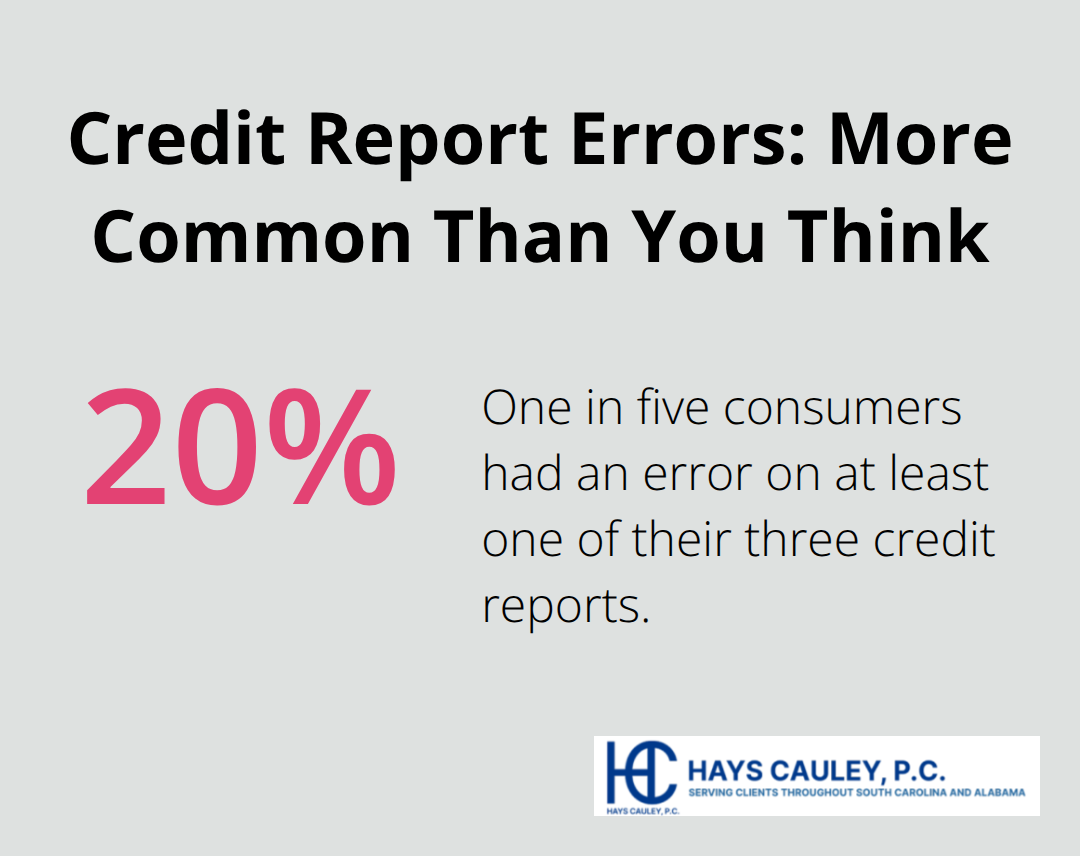

Credit reporting errors are alarmingly common. A Federal Trade Commission study found that one in five consumers had an error on at least one of their three credit reports. These inaccuracies can range from minor mistakes to major errors that significantly impact credit scores. Examples include:

- Accounts incorrectly reported as late or delinquent

- Debts listed multiple times

- Incorrect personal information (name, address, Social Security number)

- Accounts belonging to someone else with a similar name

If you spot an error on your credit report, dispute it immediately with the credit bureau and the information furnisher. Keep detailed records of all communications during this process.

Inadequate Dispute Investigations

When you submit a dispute, credit bureaus and furnishers must conduct a reasonable investigation. Unfortunately, many fail to do so adequately. They might:

- Rely solely on automated verification systems

- Ignore supporting documentation you provide

- Fail to correct errors even after you present clear evidence

If you’ve disputed an error and it wasn’t properly investigated or corrected, you may have grounds for legal action under the FCRA.

Unauthorized Credit Report Access

Your credit report contains sensitive personal and financial information. The FCRA strictly limits who can access it and for what purposes. Common violations include:

- Employers pull credit reports without written consent

- Creditors access reports without a permissible purpose

- Ex-spouses or other individuals obtain reports fraudulently

Check your credit reports regularly for hard inquiries you don’t recognize. If you suspect unauthorized access, file a complaint with the credit bureau and consider seeking legal advice.

Identity Theft-Related Issues

Identity theft can lead to numerous FCRA violations. Thieves may open accounts in your name, leading to inaccurate information on your credit report. Credit bureaus must take specific steps to address identity theft (such as placing fraud alerts), and failure to do so can constitute an FCRA violation.

Failure to Provide Required Disclosures

The FCRA mandates that consumers receive certain disclosures in specific situations. For example, if a company takes adverse action based on information in your credit report (such as denying you credit), they must provide you with a notice explaining this decision and your rights. Failure to provide these required disclosures is a violation of the FCRA.

These violations can have serious consequences for South Carolina consumers. They can lead to loan denials, higher interest rates, difficulty renting apartments, and even challenges in securing employment. Understanding these common violations is the first step in protecting your rights. In the next section, we’ll explore the legal process for addressing FCRA violations in South Carolina.

How to File an FCRA Lawsuit in South Carolina

Preparation and Evidence Collection

The first step to file a Fair Credit Reporting Act (FCRA) lawsuit in South Carolina involves thorough preparation. You must collect all relevant evidence, including copies of your credit reports, correspondence with credit bureaus and furnishers, and documentation of any financial harm you’ve experienced due to FCRA violations. Before you file a lawsuit, try to resolve the issue directly with the credit bureau or furnisher. Submit a formal dispute to each credit bureau, keeping copies of your letters and proof of delivery. Track responses and note any missed deadlines. Document all these efforts meticulously, as they can strengthen your case if you need to go to court.

Filing a Complaint in Federal Court

Once you have your evidence in order, you need to file a complaint in federal court. The U.S. District Court for the District of South Carolina handles FCRA cases. The complaint should outline the specific violations of the FCRA and the damages you’ve suffered as a result.

Statute of Limitations

In South Carolina, the statute of limitations for FCRA claims is generally two years from the date you discover the violation, or five years from the date the violation occurred (whichever comes first). You must file your lawsuit within this timeframe, or you may lose your right to sue. The statute of limitations can be complex, especially in cases of ongoing violations. Each new report of inaccurate information after you’ve disputed it could be considered a separate violation, potentially extending the timeline for legal action.

Potential Damages and Remedies

If your FCRA lawsuit succeeds, you may receive various forms of compensation:

The Consumer Financial Protection Bureau reported that the average FCRA settlement in 2020 was approximately $4,800. However, settlements can vary widely depending on the specifics of each case.

The Value of Legal Representation

While you can file an FCRA lawsuit on your own, working with an experienced consumer protection attorney can significantly improve your chances of success. These attorneys understand the nuances of FCRA law and can help you navigate the complex legal process. They can assess the strength of your case, gather necessary evidence, and represent your interests in court or settlement negotiations.

Credit reporting agencies and furnishers often have teams of lawyers on their side. Having a knowledgeable attorney in your corner can level the playing field and increase your chances of obtaining fair compensation for FCRA violations.

Final Thoughts

The Fair Credit Reporting Act empowers South Carolina residents to protect their financial well-being. You have the right to dispute inaccuracies, and credit bureaus must investigate these disputes promptly. If they fail to do so, or if other FCRA violations occur, you may have grounds for a Fair Credit Reporting Act lawsuit.

Credit reporting errors can derail your financial future. We recommend you stay vigilant and know your rights. Don’t hesitate to seek professional help when needed to ensure your credit report accurately reflects your financial history.

At Hays Cauley, P.C., we focus on helping South Carolina consumers with credit reporting issues, identity theft, and debt-related problems. Our team understands the intricacies of FCRA law and can guide you through the process of disputing errors, filing complaints, and pursuing legal action (if necessary). Contact us today to protect your economic opportunities in South Carolina.