A credit reporting error can damage your financial life for years. Inaccurate information on your credit report affects loan approvals, interest rates, and job opportunities.

We at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia and Charleston, navigate FCRA investigation steps when credit bureaus get things wrong. This guide walks you through disputing errors, escalating your case if needed, and protecting your credit going forward.

Understanding FCRA Violations and Your Rights: Serving South Carolina, Including Greenville, Columbia and Charleston

What the Fair Credit Reporting Act Actually Protects

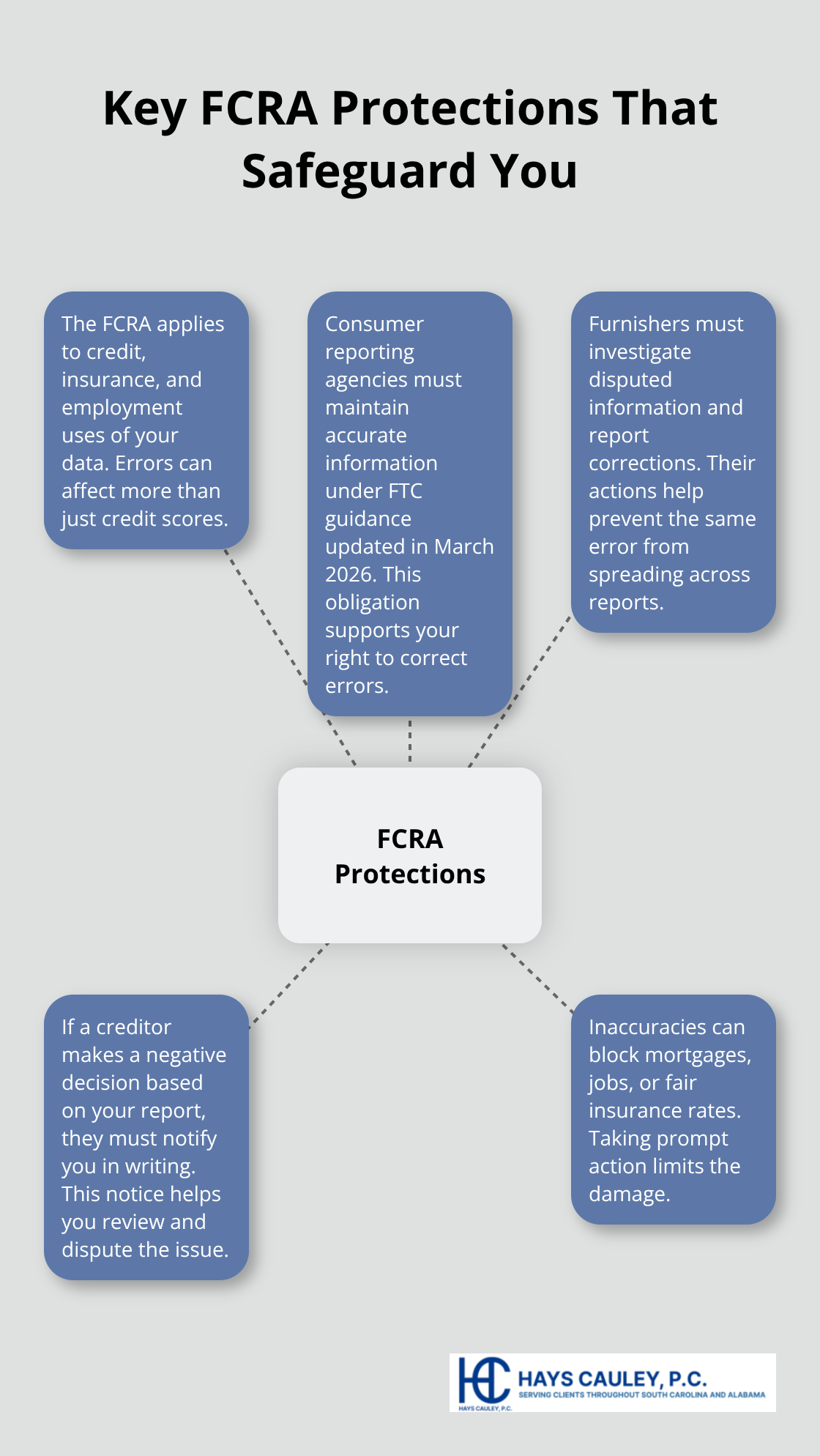

The Fair Credit Reporting Act governs how credit reporting agencies collect, use, and share your financial information. The law applies to decisions about credit, insurance, and employment-not just traditional credit scores. This means errors on your report can block you from getting a mortgage, securing a job, or obtaining reasonable insurance rates. The FTC maintains official FCRA guidance, updated as recently as March 2026, which clarifies that consumer reporting agencies must maintain accurate information. Furnishers (the companies that supply data to these agencies) have a legal duty to investigate disputed information.

If a creditor makes a negative decision based on your report, they must notify you in writing. This requirement exists because inaccurate information spreads quickly across lenders and employers who pull your file.

Common Mistakes That Damage Your Credit File

Late payments that you actually paid on time appear frequently on credit reports, especially when accounts transfer between servicers. Accounts belonging to someone else with a similar name land on your report due to identity theft or database errors. Duplicate entries of the same debt inflate what you owe and tank your score unnecessarily. Paid-off debts that still show as active accounts mislead future lenders into thinking you carry more debt than you actually do. Charge-offs listed without corresponding settlement information confuse potential creditors about your payment history.

The CFPB processes over 100,000 consumer financial complaints each week, and credit reporting errors remain among the most common grievances. These errors cost real money-a single inaccuracy can raise your interest rate by 1 to 2 percentage points on a mortgage or auto loan, translating to thousands of dollars over the life of the loan.

Your Power to Dispute and Correct

You have the right to challenge any information on your credit report at no cost. When you file a dispute with a credit reporting agency, the agency must investigate your claim within 30 days of receiving it. If you provide additional information during that initial 30-day window, the investigation extends by up to 15 days. The agency must notify you of the results within 5 business days after the investigation concludes and provide you with a free updated copy of your report.

If the furnisher determines the information is inaccurate, they must notify every credit reporting agency that previously received the incorrect data. This correction requirement prevents the same error from haunting you across multiple reports. If you dispute directly with the furnisher instead, they have 30 days to investigate and respond. Send your dispute by certified mail with return receipt to create documented proof of when the company received your complaint-a practical step that protects you if a dispute gets lost or ignored.

Understanding these protections sets the foundation for taking action. The next section walks you through the specific steps to file a dispute with credit bureaus and what to expect during the investigation process.

Filing Your Dispute and Getting Results: Serving South Carolina, Including Greenville, Columbia and Charleston

Start With the Right Documentation

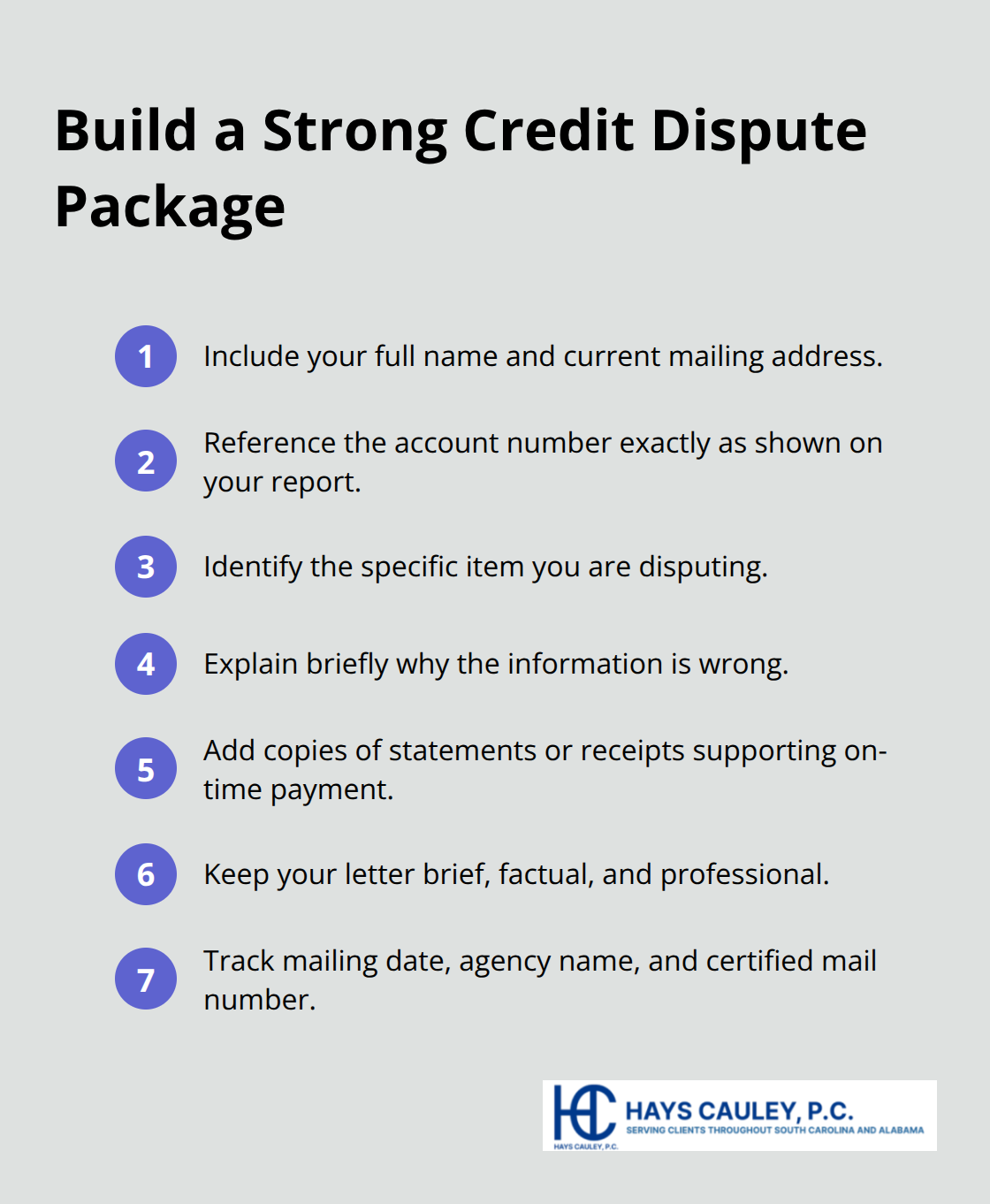

Starting your dispute correctly makes the difference between a quick resolution and months of back-and-forth. Gather your name, current address, account number from the report, the specific item you’re disputing, a clear explanation of why the information is wrong, and copies of supporting documents like bank statements or payment receipts showing the account was paid on time. Keep your dispute letter brief and factual-avoid emotional language or lengthy explanations that can confuse the investigation process.

The CFPB recommends keeping copies of everything you send and maintaining a record of when you mailed materials, so create a simple spreadsheet with the mailing date, agency name, and tracking number.

Send Your Dispute to the Right Agency

The three nationwide credit reporting agencies-Experian, Equifax, and TransUnion-must investigate your dispute within 30 days of receiving it, so your first move is sending a written dispute directly to the agency holding the error. Mail your dispute by certified mail with return receipt requested; this creates documented proof that the agency received your complaint on a specific date, which matters if you later need to prove they missed their 30-day deadline. Include all required information in your letter and keep the tone straightforward and professional.

Understand the Investigation Timeline

During their 30-day investigation window, the agency contacts the furnisher (the company that supplied the incorrect information) and reviews all relevant data in your file. If you submit additional information during those initial 30 days, the timeline extends up to 45 days total. Once the investigation concludes, you receive a free updated copy of your credit report showing whether the item was corrected, deleted, or remains unchanged. The agency must notify you in writing of the investigation results within 5 business days after completing their review.

What Happens When the Furnisher Responds

If the furnisher determines the information is inaccurate, they must notify all credit reporting agencies that previously received the incorrect data within six months. If the agency denies your dispute, they must explain their reasoning and provide contact information for the furnisher so you can follow up directly. Send disputes to furnishers at the address listed on your consumer report or at any address the furnisher specifies for credit reporting disputes, again using certified mail. Most companies respond to disputes within 15 days, with final responses often provided within 60 days if the initial reply indicates the investigation is ongoing.

When Disputes Don’t Produce Results

If the furnisher fails to correct the error or the credit bureau denies your dispute without valid reason, you have additional options available. Some situations warrant escalating your case beyond the standard dispute process, particularly when agencies ignore deadlines or furnishers refuse to investigate legitimate claims. The next section covers when legal action becomes necessary and what remedies you may pursue.

Escalating Your Case When Disputes Fail: Serving South Carolina, Including Greenville, Columbia and Charleston

Why Standard Disputes Stop Working

Disputes fail more often than most people realize. The CFPB receives over 100,000 complaints weekly, and many involve credit bureaus that ignore deadlines, furnishers that refuse to investigate, or agencies that deny disputes without legitimate reason. If your dispute gets denied or the error persists after 30 to 45 days, you’ve reached the point where legal action becomes practical rather than theoretical. The FCRA gives you concrete remedies when agencies violate the law.

Understanding Your Legal Remedies

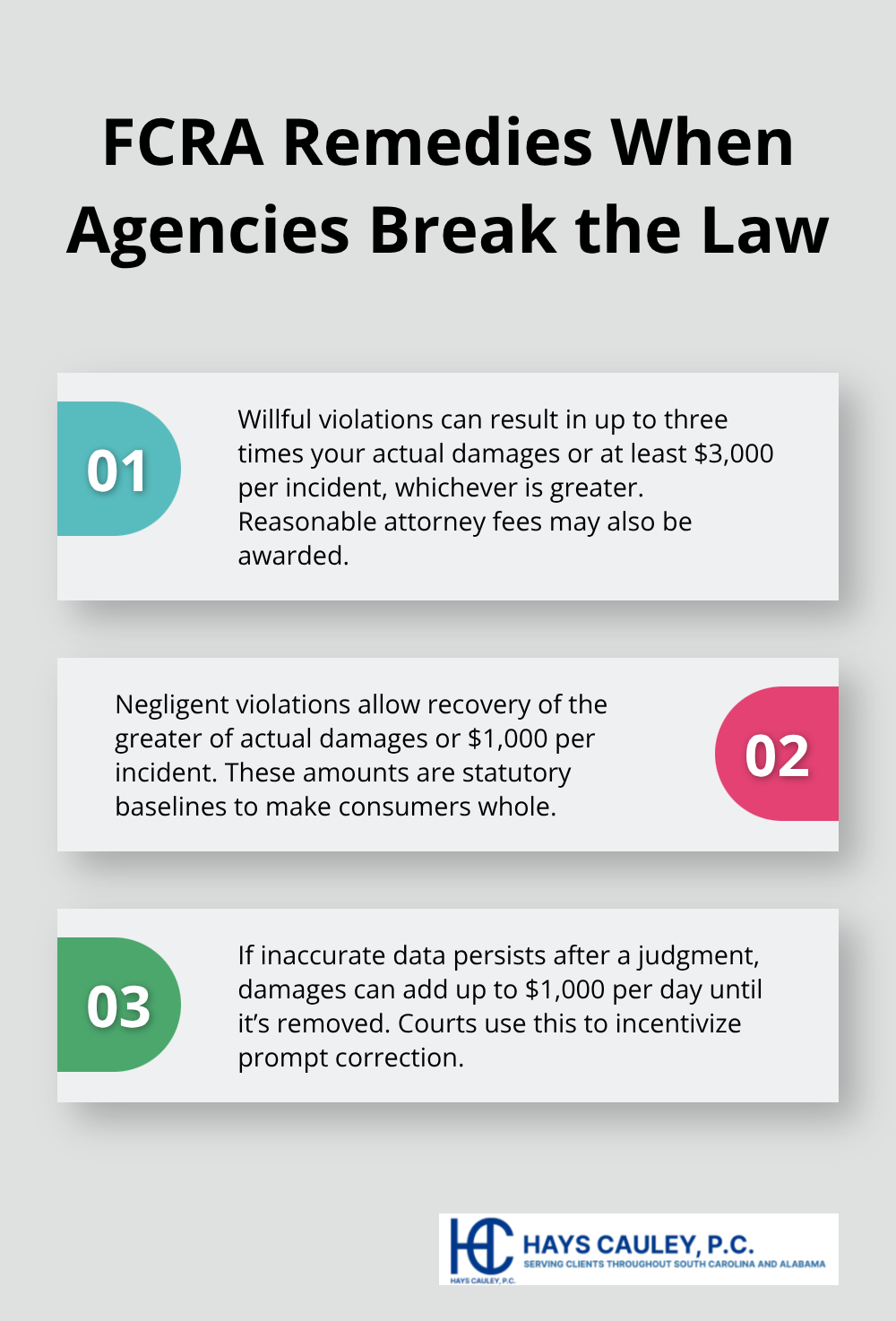

Willful violations carry penalties of three times your actual damages or at least $3,000 per incident, whichever is greater, plus reasonable attorney fees. Negligent violations result in the greater of actual damages or $1,000 per incident. If an inaccuracy damages your creditworthiness and the agency fails to correct it even after a judgment, damages can climb by up to $1,000 per day until the information is removed.

These aren’t hypothetical numbers-they reflect what federal courts actually award when credit bureaus and furnishers break the law.

Building a Strong Legal Case

A solid FCRA case rests on documented evidence of agency violations. Review whether the bureau missed its 30-day investigation deadline, whether the furnisher failed to respond within 30 days, or whether either party ignored your dispute altogether. Examine the investigation itself-did the agency actually contact the furnisher, or did they rubber-stamp a denial without effort? Pull your dispute letters, certified mail receipts, and credit reports to establish a clear timeline. The strongest cases involve agencies that simply ignore you or furnishers that never respond to your dispute.

When an agency denies your dispute, they must provide the basis for the denial and explain their verification method; if that explanation is vague or unsupported, that weakness strengthens your legal position. You also have the right to add a dispute statement to your credit file if you disagree with the agency’s investigation results, and you should document whether the agency honored that request.

Calculating Your Damages

Courts take FCRA violations seriously because the law explicitly creates a private right of action-you don’t need government approval to sue. Most cases settle before trial because the financial exposure forces agencies to negotiate. Your damages cover not just the statutory penalties but also real harms like a higher interest rate you paid because of the inaccuracy, a job you didn’t get, or insurance you were denied. Document these concrete impacts with loan estimates, job rejection letters, or insurance quotes, and your case value increases substantially.

Moving Forward After Correction

Correcting a credit reporting error is a victory, but your work doesn’t stop there. Check your credit reports from all three bureaus at least once yearly through AnnualCreditReport.com, which provides free reports without affecting your credit score. When you review your reports, look for the same types of errors that plagued you before-late payments marked as current, accounts that don’t belong to you, or duplicate entries. Catching errors early allows you to file a dispute immediately rather than letting inaccurate information damage your score for months.

Most errors stem from account transfers between servicers, identity theft, or data entry mistakes at furnishers. If you’ve experienced identity theft, place a security freeze on your credit file with all three bureaus at no cost (you can place a freeze within five business days of a written or electronic request and receive a unique PIN within ten business days). A freeze restricts access to your report unless you authorize a specific request, which stops fraudsters from opening accounts in your name. Document everything related to your accounts by keeping payment receipts, bank statements showing transfers, and correspondence with creditors, as this documentation becomes invaluable if another error appears and you need to dispute it quickly.

If errors persist despite your efforts or if you face resistance from credit bureaus and furnishers during FCRA investigation steps, contact us at Hays Cauley, P.C. for assistance with credit reporting disputes. Our team helps South Carolina residents, including those in Greenville, Columbia, and Charleston, navigate these situations when agencies fail to correct legitimate errors. Reach out if standard dispute procedures aren’t producing results or if you believe you have grounds for legal action under the FCRA.