Credit reporting errors can wreck your finances and your future. The Fair Credit Reporting Act gives you powerful protections, but most people don’t know how to use them.

At Hays Cauley, P.C., we help South Carolina residents fight back against FCRA violations and inaccurate credit reports. Your FCRA rights in SC are real-and we’ll show you how to claim them.

What the FCRA Actually Protects

The Fair Credit Reporting Act gives you three concrete rights that most South Carolina residents never use. First, you have the absolute right to know what information credit bureaus hold about you. You can pull your credit report from Equifax, Experian, and TransUnion once every 12 months for free through AnnualCreditReport.com. Better yet, these three bureaus have permanently extended a program allowing you to check each report for free once per week at the same site. Through 2026, you can also get six additional free credit reports per year by visiting the Equifax website or calling 1-866-349-5191. This means you can monitor your file far more frequently than most people realize, catching identity theft or reporting errors before they damage your creditworthiness.

Dispute Inaccurate Information at No Cost

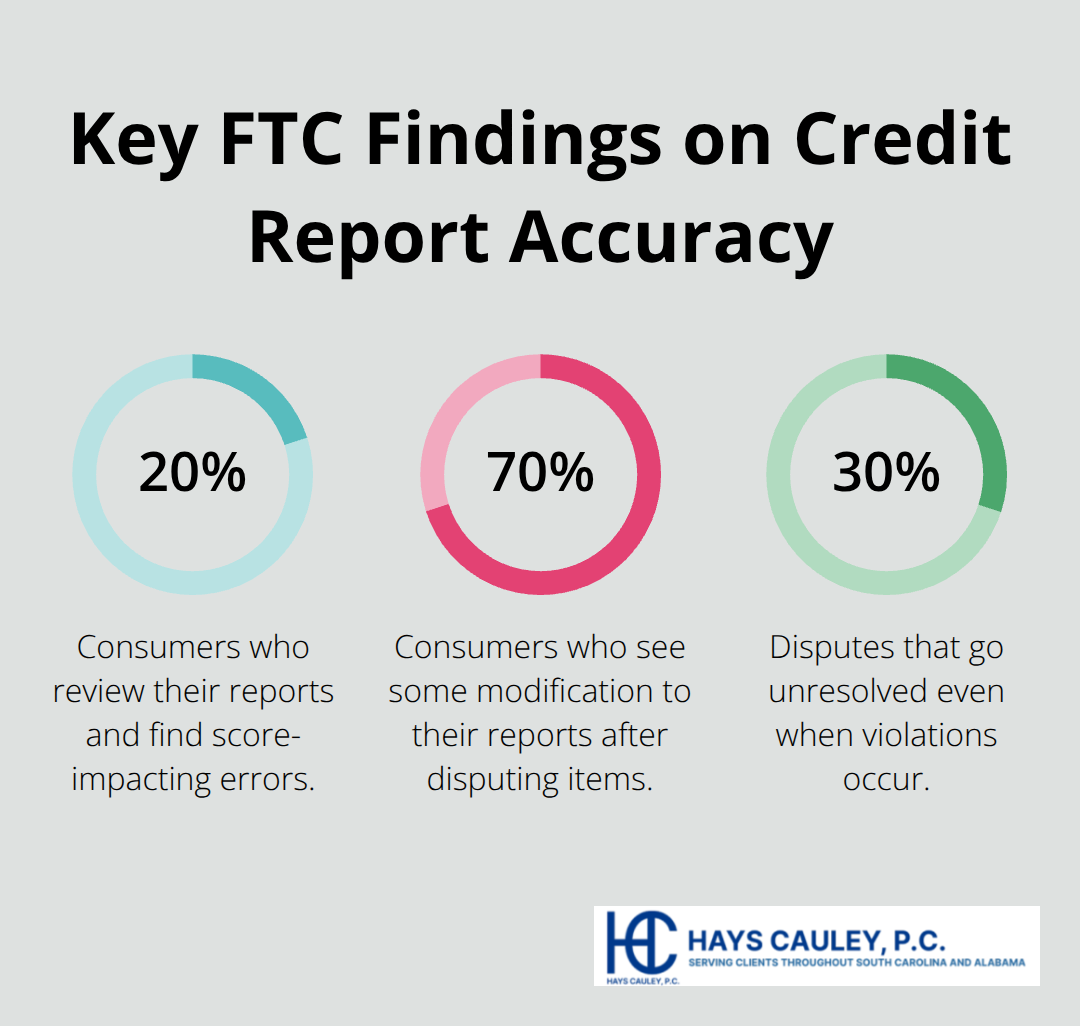

Your second major right is the power to dispute inaccurate information at no cost. When you find an error, both the credit bureau and the business that supplied the information must correct it for free. The FTC reports that roughly 20% of consumers who review their reports find errors affecting their scores, yet most never dispute them. South Carolina law strengthens this right further: credit bureaus must reinvestigate disputed items within 30 days at no charge and provide you with the results. If an inaccuracy damages your creditworthiness and a judgment exists, South Carolina law allows damages up to $1,000 per day until the item is removed. Correcting errors can meaningfully improve your score; moving from a 650 to a 750 can save about $68,000 in interest on a $200,000 30-year mortgage.

To dispute effectively, send written requests via certified mail with return receipt to each bureau that has the error, clearly identifying each item and including copies of supporting documents (bank statements, payment receipts, or creditor correspondence). The credit bureau typically has 30 days to investigate and forward your evidence to the reporting business. If the reporting business finds the information inaccurate, it must notify all three bureaus to correct it.

Control Who Accesses Your Information

Your third right restricts who can access your credit report and for what reasons. The FCRA limits access to specified purposes only, meaning employers generally must obtain your written consent before pulling your credit for employment decisions. If a company takes adverse action based on your credit report, they must notify you and provide a copy of the report used in making that decision. South Carolina adds extra protection through its Consumer Identity Theft Protection law: you can place a security freeze on your consumer file at no cost, and credit bureaus must implement it within five business days. You can lift or remove the freeze within three business days after requesting it, or temporarily lift it within about 15 minutes for an electronically designated period.

This freeze prevents unauthorized accounts from being opened in your name without your explicit permission-a critical shield against identity theft. Yet many South Carolina residents face violations of these protections every day, from bureaus that ignore disputes to furnishers that fail to investigate claims properly.

How Bureaus and Creditors Violate Your FCRA Rights

Credit bureaus and furnishers routinely ignore the legal obligations that the FCRA imposes on them, and these violations cause real financial damage. One of the most common violations is reporting inaccurate or outdated negative items that should have fallen off your report years ago.

Reporting Items Past Their Legal Expiration Date

Negative information that is accurate can stay on your report for seven years, but bankruptcy information can remain for ten years. Yet many bureaus fail to remove items once they age past these deadlines, artificially tanking your score. The FTC reports that around 70% of consumers who dispute items see some modification to their credit reports, which means 30% of disputes go unresolved even when violations occur. When a bureau reports an item past its legal expiration date or reports a balance that doesn’t match your records, that’s a willful violation under South Carolina law.

Willful violations can trigger treble damages or up to $1,000 per incident plus attorney fees.

Conducting Sham Investigations Instead of Real Ones

Another widespread violation happens when bureaus and furnishers fail to investigate your disputes properly. You have the right to dispute inaccurate information, and the law requires the bureau to investigate within 30 days and forward your evidence to the furnisher. Many bureaus conduct perfunctory investigations that amount to little more than a phone call to the furnisher, who simply re-verifies the disputed item without actually reviewing your evidence. Furnishers themselves often ignore their obligation to investigate timely and thoroughly, simply confirming the accuracy of items without examining the documents you provided.

Accessing Your Report Without Permission

A third critical violation involves using your credit report without your permission. Employers must obtain your written consent before pulling your credit for employment purposes, yet some companies access your report without authorization or for impermissible purposes. If a company takes adverse action based on your credit report, they must notify you and provide a copy of the report used in making the decision. Many employers fail to send this adverse action notice, violating your right to know why you were denied a job.

The Real Cost of These Violations

An inaccuracy that lowers your credit score from 750 to 650 can cost you approximately $68,000 in additional interest on a $200,000 30-year mortgage. If a bureau fails to remove an inaccurate item that damages your creditworthiness after a judgment is entered, South Carolina law allows you to recover up to $1,000 per day until the item is removed. This means a single violation that persists for 30 days can result in $30,000 in damages before attorney fees are even considered.

How to Spot and Document Violations

Many South Carolina residents accept these violations as inevitable, but the law gives you concrete remedies. Pull all three reports from Equifax, Experian, and TransUnion and compare line-by-line against your own records to flag unrecognized accounts and verify balances. Send dispute notices to both the bureaus and the furnishers via certified mail with return receipt, clearly identifying each error and including supporting documents like bank statements and creditor correspondence. Document every communication attempt and keep copies of everything you send. If the bureau or furnisher ignores your rights or conducts a sham investigation, you have grounds for legal action under the FCRA. The next step is understanding exactly how to file that action and what remedies you can recover.

How to Fight Back Against FCRA Violations: Serving South Carolina, including Greenville, Columbia and Charleston

Start with pulling all three of your credit reports from Equifax, Experian, and TransUnion through AnnualCreditReport.com at no cost. Most South Carolina residents never take this step, which means they miss errors that actively destroy their credit scores. Once you have the reports, compare them line-by-line against your own financial records. Look for accounts you don’t recognize, balances that don’t match what you owe, hard inquiries you didn’t authorize, and negative items that should have aged off after seven years. Document everything. Write down the exact error, the date you found it, and which bureau reported it. This documentation becomes critical evidence if you later file a lawsuit.

Send Your Dispute in Writing, Not Online

The FCRA requires you to dispute inaccurate information, but the method matters far more than most people realize. Do not use the online dispute tools that the bureaus offer. These systems process disputes quickly, not thoroughly. Instead, send your dispute letter via certified mail with return receipt requested to each bureau that has the error. Your letter should identify the specific item you’re disputing, explain why you believe it’s inaccurate, and include copies of supporting documents like bank statements, payment receipts, or creditor correspondence that prove your point. The bureau has 30 days to investigate and respond. Send a second dispute letter directly to the furnisher-the business that originally reported the information to the bureau. The furnisher also has a legal obligation to investigate disputes timely and thoroughly. Many furnishers ignore disputes sent through bureaus, but they take direct disputes more seriously because they create a paper trail that can be used against them in court. Keep copies of everything you send and maintain a log of dates and certified mail tracking numbers.

File a Complaint with the CFPB When Bureaus Ignore You

If the bureau doesn’t respond within 30 days or conducts what appears to be a sham investigation without actually reviewing your evidence, file a complaint with the Consumer Financial Protection Bureau at ConsumerFinance.gov. The CFPB has enforcement authority over credit bureaus and furnishers, and they take complaints seriously. When you file, include copies of your dispute letter, the certified mail receipts proving you sent it, the bureau’s response (or lack thereof), and your supporting documents. The CFPB will forward your complaint to the bureau, which then has 15 days to respond. This creates official pressure that often forces bureaus to conduct actual investigations instead of rubber-stamping the furnisher’s re-verification. If the bureau still refuses to correct the error after the CFPB investigation, you have grounds to file a lawsuit under the FCRA. South Carolina law allows you to recover actual damages, statutory damages up to $1,000 per violation, and attorney fees if you win. Willful violations can result in treble damages, meaning three times your actual damages.

Final Thoughts

Fighting FCRA violations on your own takes time, persistence, and legal knowledge most people don’t have. You must pull reports, document errors, send certified letters, file CFPB complaints, and track deadlines across multiple agencies. Many South Carolina residents start this process only to abandon it when bureaus ignore disputes or conduct sham investigations. At Hays Cauley, P.C., we handle the legal work so you don’t have to.

We’re a consumer protection law firm that helps South Carolina residents assert their FCRA rights SC and fight credit reporting violations. We investigate your credit reports thoroughly, identify every violation, and build cases with the documentation needed to win. We handle all communication with bureaus and furnishers, file complaints with the CFPB when necessary, and prepare your case for litigation if violations persist.

Most importantly, we work on a contingency basis, which means you pay nothing unless we recover money for you (your FCRA rights in South Carolina are worth real money, and you shouldn’t have to pay upfront legal fees to claim them). If you’ve found errors on your credit report, contact us today for a free review of your reports and an explanation of what violations exist and what you can recover.