Debt collectors in South Carolina often cross legal lines, using aggressive tactics that violate your rights. Repeated calls, threats, and contact with your employer or family members are harassment tactics we see regularly.

The Fair Debt Collection Practices Act gives you real protections, and debt collection remedies SC residents can use are stronger than most people realize. We at Hays Cauley, P.C. help South Carolina residents stop this harassment and repair the damage to their credit reports.

How Debt Collectors Harass Consumers in South Carolina

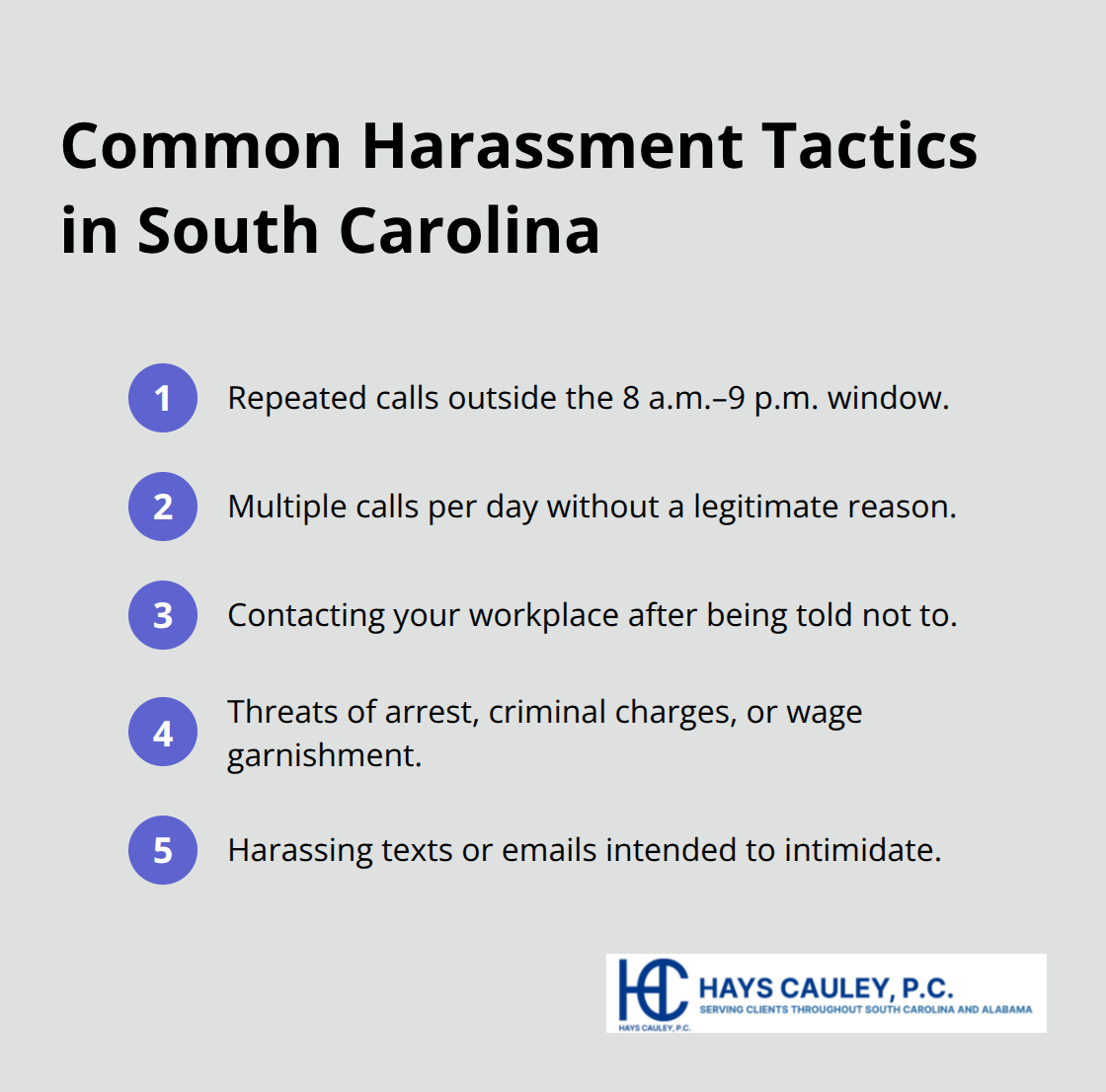

Illegal Phone Calls and Messages

Debt collectors in South Carolina use relentless phone calls as their primary harassment weapon, and the Fair Debt Collection Practices Act prohibits calls before 8 a.m. or after 9 p.m., yet collectors frequently ignore these hours. Multiple calls per day to your home or cell phone, especially without legitimate reason, cross into harassment territory. Collectors also contact your workplace despite knowing your employer disapproves, which violates the FDCPA directly. Some send threatening messages via text or email stating they will pursue criminal charges, wage garnishment, or arrest-actions they cannot legally take. These false threats constitute deliberate violations that expose collectors to damages under South Carolina law.

Contacting Your Employer and Family Members

Contacting family members, neighbors, or your employer without a legitimate purpose to locate you violates federal law regularly. The FDCPA allows collectors to contact third parties only to find your location and prohibits them from revealing debt details to anyone. Yet many collectors disregard this rule, telling your boss about your debt or calling relatives repeatedly. South Carolina law goes further than federal protections, prohibiting wage garnishment for consumer debts entirely and protecting your employment from retaliation if your wages are garnished.

Document Every Violation

If a collector threatens to tell your employer or contacts them after you request they stop, document the date, time, and exactly what was said. Keep records of all calls, texts, and letters-this documentation becomes critical evidence if you pursue legal action. The financial exposure collectors face when violating these rules is substantial (which is why detailed records often lead to quick settlements before litigation costs mount). Your written records transform vague complaints into provable violations that courts recognize and remedy.

Understanding these harassment tactics prepares you to identify when collectors cross legal lines. The next section explains the specific protections the Fair Debt Collection Practices Act provides and how you can use them to stop the harassment.

Your Legal Rights Under the Fair Debt Collection Practices Act

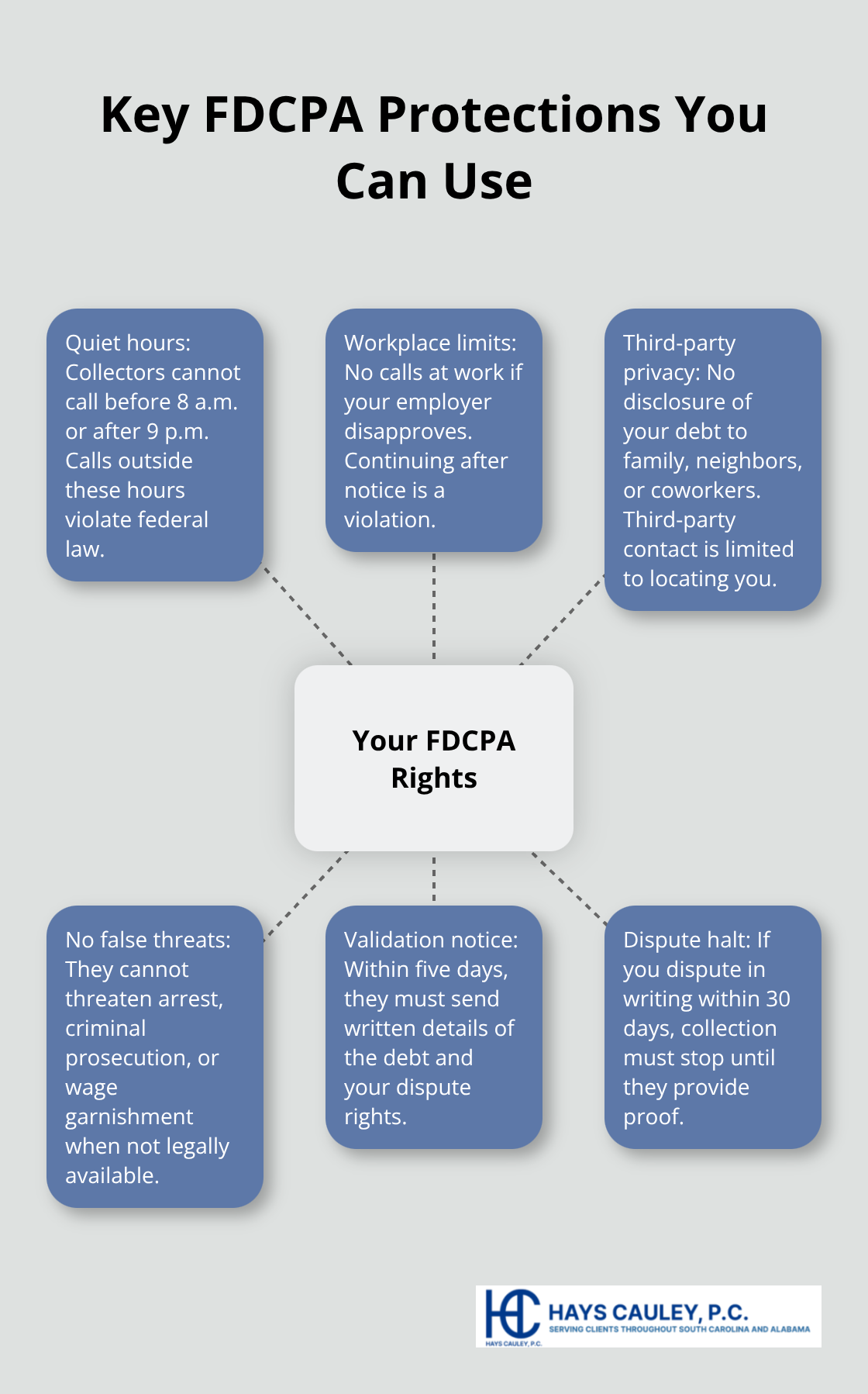

The Fair Debt Collection Practices Act creates a specific list of prohibited behaviors, and knowing these rules transforms you from a passive target into someone who can identify violations immediately. Debt collectors cannot call before 8 a.m. or after 9 p.m., contact you at work if your employer disapproves, or reach out to family members and neighbors except to locate you. They cannot threaten criminal prosecution, arrest, or wage garnishment when these actions are not legally available to them. False statements about the debt amount, claims that they are attorneys when they are not, and threats to take actions they do not intend to take all violate the FDCPA directly. The law also prohibits unfair practices like collecting more than you owe, depositing post-dated checks early without permission, or demanding payment through collect calls. Within five days of first contact, collectors must send written notice stating the exact amount owed, the creditor’s name, and your right to dispute. If you dispute the debt in writing within 30 days, they cannot contact you further until they provide written proof that the debt is valid.

What Debt Collectors Cannot Do

Collectors face substantial financial consequences when they violate these rules, which is why documentation of each violation strengthens your position significantly. They cannot misrepresent themselves as government officials or claim they will pursue actions outside their legal authority. They also cannot contact you repeatedly on the same day, use obscene language, or disclose your debt status to unauthorized third parties. South Carolina law reinforces these federal protections and adds its own safeguards, including a complete prohibition on wage garnishment for consumer debts and protection against employer retaliation.

Track Every Violation With Precision

Write down the date, time, phone number used, name of the person who called, and the exact words spoken or threats made the moment you suspect a collector has crossed the line. Save all letters, emails, and text messages without deleting anything. If a collector calls repeatedly on the same day or at prohibited hours, note each call separately with timestamps. The Federal Trade Commission reports that patterns of violations prove most effective when you can show multiple instances rather than isolated incidents. Your documentation becomes the foundation for complaints to the Consumer Financial Protection Bureau, disputes with credit bureaus, and potential lawsuits. Many collectors settle cases quickly once they see detailed records because the financial exposure under South Carolina law and the FDCPA is substantial, with damages ranging up to $1,000 per violation plus court costs and attorney fees.

File Complaints That Create Official Records

Submit complaints to the Consumer Financial Protection Bureau through their online portal or call 855-411-CFPB, which creates an official record even if the CFPB does not intervene in your specific case. The CFPB uses individual complaints to identify patterns of violations across collectors, which can lead to enforcement actions against repeat offenders. You should also report violations to the South Carolina Department of Consumer Affairs, which conducts a 30-day investigation period for unconscionable debt collection practices. Include copies of your documentation with both complaints, as specific details and dates carry far more weight than general accusations. If you win a case against a collector, the court can require them to pay your attorney fees and court costs, making legal representation affordable even for consumers with limited means.

Once you understand what collectors cannot do and you have documented their violations, you can take concrete action to stop the harassment. The next section shows you how to send a cease and desist letter and dispute inaccurate entries on your credit report.

How to Stop Harassment and Fix Your Credit Report, Serving South Carolina, Including Greenville, Columbia, and Charleston

Send a Cease and Desist Letter Immediately

A cease and desist letter is your first formal action and should go out immediately if a collector continues calling after you request they stop. Write a simple letter stating that all contact must cease except for notification of specific legal actions like filing a lawsuit or confirming no further contact will occur. Send it by certified mail with return receipt requested to the collection agency’s address, and keep a copy for your records. Once the collector receives this letter, any additional contact violates the FDCPA and gives you grounds for legal action. Many collectors stop immediately because they know the financial exposure is substantial-you can recover up to $1,000 per violation plus court costs and attorney fees if they ignore your cease and desist letter.

Dispute Inaccurate Entries With the Credit Bureaus

Disputing inaccurate entries on your credit report requires action with the three major credit bureaus: Equifax, Experian, and TransUnion. Send a written dispute to each bureau within 30 days of receiving the debt collection notice, and include copies of documentation showing the debt is inaccurate, paid, or belongs to someone else. The bureaus must investigate your dispute within 30 days and remove items they cannot verify, which often happens quickly because debt buyers frequently lack proper documentation. If a debt collector reported false information without meeting FDCPA obligations like sending a validation notice, this becomes grounds for both a credit bureau dispute and a separate FDCPA violation claim. Many inaccurate entries disappear within 30 to 45 days after verification fails, immediately improving your credit score.

Request Debt Validation in Writing

If the collector refuses to provide proof of the debt after you request validation in writing, the credit bureaus will typically remove the entry entirely since unverified debt cannot legally remain on your report. This validation request creates a paper trail that strengthens your position in disputes with both the collector and the credit bureaus. The FDCPA requires collectors to respond to validation requests within 30 days, and their failure to do so constitutes a violation that exposes them to damages.

Pursue Legal Action Against Violating Collectors

Consider legal action against collectors who knowingly report false information or continue contacting you after receiving your cease and desist letter. South Carolina law allows you to sue for actual damages plus up to $1,000 in statutory damages per violation, and if you prevail, the collector must pay your attorney fees and court costs. Filing suit in your county of residence creates leverage for settlement negotiations because many collectors calculate that defending a lawsuit costs more than paying damages. We at Hays Cauley, P.C. help South Carolina residents pursue these claims and recover compensation for harassment and credit damage, serving communities throughout Greenville, Columbia, and Charleston. Document everything before contacting an attorney so you have a complete record of violations ready for review.

Final Thoughts

South Carolina law and the Fair Debt Collection Practices Act provide real power to stop harassment and repair your credit. Debt collectors cannot call before 8 a.m. or after 9 p.m., contact your workplace after you object, threaten arrest or wage garnishment they cannot legally pursue, or report false information to credit bureaus without meeting their validation obligations. Your documentation of each violation-dates, times, names, and exact words spoken-transforms complaints into provable cases that collectors take seriously because the financial exposure is substantial.

The debt collection remedies SC residents can pursue include sending a cease and desist letter, disputing inaccurate entries with the three major credit bureaus, and filing complaints with the Consumer Financial Protection Bureau and South Carolina Department of Consumer Affairs. These steps often resolve harassment quickly because collectors know that defending violations costs more than settling. If a collector ignores your cease and desist letter or continues reporting false information after you dispute it, legal action becomes your next option, and prevailing plaintiffs recover damages up to $1,000 per violation plus attorney fees and court costs.

Start by documenting everything immediately and writing down call dates and times, saving all letters and messages, and requesting debt validation in writing if you have not already done so. Send your cease and desist letter by certified mail within the next week, and submit disputes to Equifax, Experian, and TransUnion within 30 days of receiving the debt collection notice. If harassment continues or you need guidance on whether your case warrants legal action, contact us to discuss your situation, and we at Hays Cauley, P.C. will evaluate your violations and explain the remedies available under state and federal law while serving South Carolina, including Greenville, Columbia, and Charleston.