Debt collectors contact millions of Americans each year, and many people don’t know their rights. A debt validation letter is one of the most powerful tools you have under federal law to stop collection efforts and demand proof that a debt is actually yours.

At Hays Cauley, P.C., we’ve helped countless South Carolina residents, including those in Greenville, Columbia and Charleston, protect themselves from aggressive collection tactics. This guide shows you exactly how to write a validation letter that works.

What Debt Validation Really Means

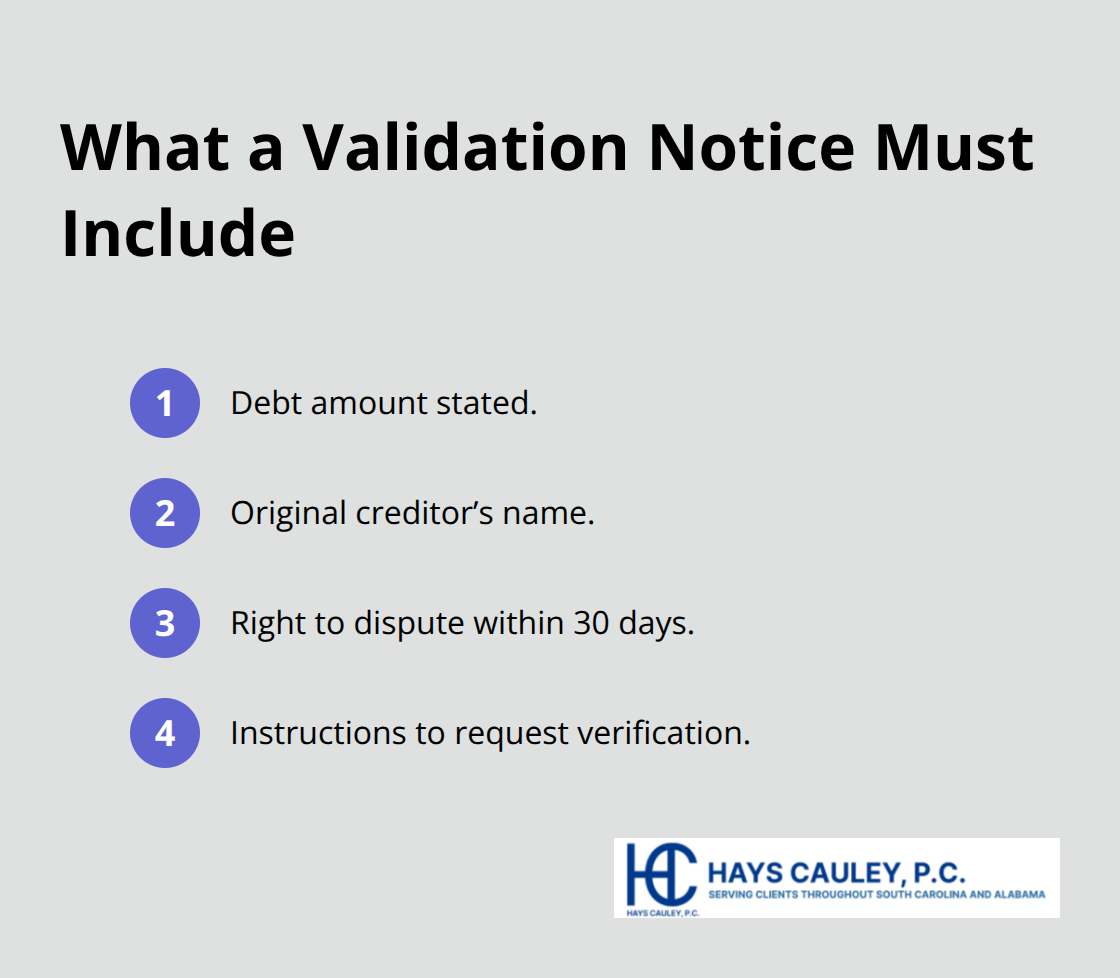

A debt validation letter is your formal demand for a debt collector to prove you actually owe the money they’re claiming. Under the Fair Debt Collection Practices Act, debt collectors must provide this proof within specific timeframes or stop collection efforts entirely. The FDCPA requires collectors to send a validation notice within five days of their first contact with you, and this notice must include the debt amount, the creditor’s name, your right to dispute within 30 days, and instructions on how to request verification. When you respond with your own validation letter, you invoke a federal protection that forces the collector to pause all collection activities until they provide adequate documentation.

This isn’t a suggestion or courtesy-it’s a legal requirement that protects you from paying debts that don’t belong to you, debts with incorrect amounts, or debts that have already been paid.

Why Collectors Must Actually Respond

Debt collectors ignore validation requests at their peril. When you send a written request for validation within 30 days of receiving their notice, the collector must halt collection efforts and provide verification of the debt or cease collection entirely. If they continue calling, sending letters, or reporting the debt to credit bureaus after you’ve properly disputed it in writing, they violate the FDCPA and expose themselves to lawsuits. The Consumer Financial Protection Bureau receives thousands of debt collection complaints annually, with many involving improper validation practices. The real power here lies in the fact that most debt collectors operate on thin margins and can’t afford to litigate over disputed debts, especially when you’ve created a paper trail through certified mail. Your validation letter shifts the burden entirely to them-they must prove the debt exists and belongs to you, not the other way around.

Your 30-Day Window

The 30-day period after receiving a validation notice is your critical window. Send your validation letter via certified mail with return receipt before day 30 expires, and the collector must pause collection immediately. This pause continues until they respond with adequate documentation, which often takes weeks or months. During this time, they cannot legally contact you about the debt, report it to credit bureaus as unpaid, or pursue legal action. Many consumers waste this advantage by waiting too long or sending letters without proof of delivery. The moment you mail that certified letter, you activate federal protections that are nearly impossible for collectors to overcome without proper documentation.

What Happens Next

Once you send your validation letter, the collector’s next move determines your path forward. They either provide adequate documentation proving the debt is valid and belongs to them, or they fail to respond sufficiently. If they respond with complete documentation, you’ll need to review it carefully against your own records and decide whether to dispute specific items, negotiate a settlement, or prepare for potential legal action. If they fail to respond adequately or at all, you have strong grounds to file complaints with the Consumer Financial Protection Bureau and pursue your own legal remedies. Understanding what comes after you mail that letter helps you prepare for the next steps in protecting your rights.

Essential Elements Your Debt Validation Letter Must Include

Start With Your Identifying Information

Your validation letter needs to be specific enough that the debt collector cannot ignore it or claim confusion about what you’re requesting. Start with your complete name exactly as it appears on their collection notice, your current mailing address, and your phone number. Include the account number they referenced in their validation notice, or if they didn’t provide one, write “Account number not provided by collector.” Add the exact debt amount they claimed, the creditor’s original name, and the current collector’s name and address. The CFPB requires validation notices to include these details, so your response should mirror that specificity.

Make Your Legal Request Crystal Clear

State clearly that you are requesting validation under 15 U.S.C. Section 1692g of the Fair Debt Collection Practices Act. Do not make this vague-use the actual statute citation. This legal language signals that you understand your rights and expect compliance.

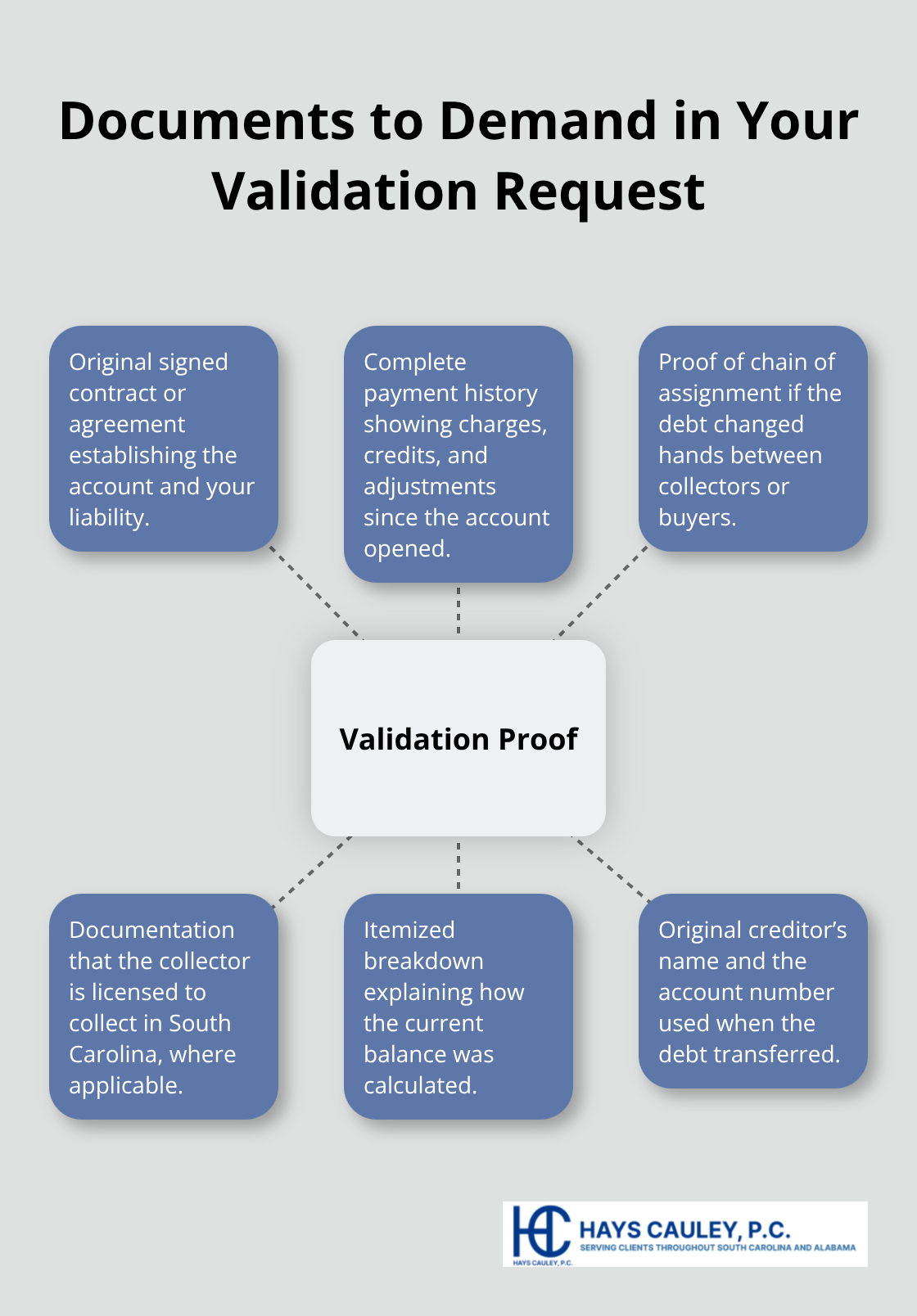

Demand that they provide the original signed contract or agreement, a complete payment history showing all charges, credits, and adjustments since the account opened, proof of the chain of assignment if the debt changed hands, and documentation that they are licensed to collect in South Carolina if state licensing applies. Request an itemized breakdown showing how they calculated the current amount, the original creditor’s name and account number used when the debt transferred, and any other documentation proving the debt belongs to them.

Provide Evidence If You Already Paid

If you believe you already paid this debt, attach copies of cancelled checks, bank statements, or payment receipts proving payment. This documentation strengthens your position significantly and forces the collector to address your specific evidence rather than rely on general claims. The more concrete proof you provide, the harder it becomes for them to dismiss your validation request.

Use Professional Language and Proper Delivery

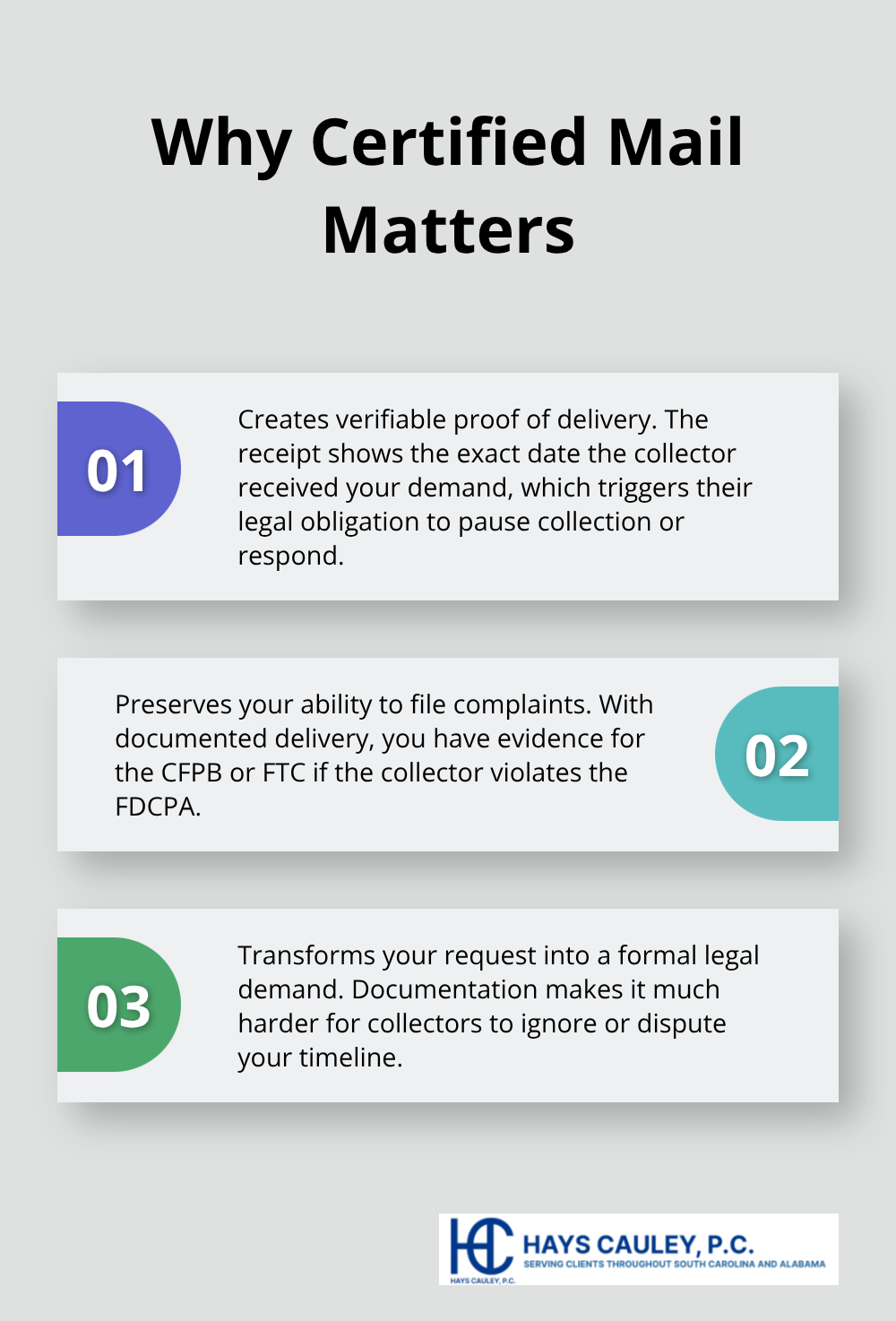

Do not include emotional language, personal grievances, or threats. Collectors dismiss letters that sound angry or unstable because those letters are easier to ignore legally. Keep your tone direct and businesslike. Send the letter via certified mail with return receipt requested, and keep a copy for yourself along with the receipt. Many consumers sabotage their own validation efforts by sending letters without proof of delivery, making it impossible to prove they met the 30-day deadline if the collector later claims they never received it. The certified mail receipt is your evidence that the collector received your request on a specific date, which triggers their legal obligation to respond or pause collection.

Once you mail that certified letter, the collector’s response-or lack thereof-determines your next move and what options become available to you.

Common Mistakes That Weaken Your Debt Validation Letter – Serving South Carolina, including Greenville, Columbia and Charleston

Most validation letters fail not because the legal argument is weak, but because people make preventable mistakes that give debt collectors an excuse to ignore them. The single most damaging error is mailing your validation letter without certified mail and return receipt. When you use regular mail, you have no proof the collector received your letter on any specific date. Debt collectors exploit this constantly by claiming they never got it, which means you missed your 30-day window and lost your legal leverage entirely. The CFPB receives complaints from consumers who did everything right except skip the certified mail step, only to discover months later that the collector continued collection efforts because there was no documentation of delivery.

Send Your Letter via Certified Mail With Return Receipt

Certified mail costs about three dollars and takes five minutes to arrange at any post office. Not using it is like filing a lawsuit without keeping a copy of the complaint for yourself. The certified receipt becomes your proof that the collector received your demand on a specific date, triggering their legal obligation to respond within 30 days. Without that receipt, you have no evidence to support any future complaint to the CFPB or FTC if the collector violates the FDCPA. This single step transforms your validation letter from a request the collector can dismiss into a documented legal demand they cannot ignore.

Keep Your Language Professional and Direct

Collectors dismiss validation letters that include angry language, personal complaints, or emotional appeals because those elements make the letter easier to attack legally. A collector’s attorney can point to your emotional tone and argue you were venting rather than making a formal legal demand. Your validation letter must sound like what it is: a formal legal request, not a complaint about how the collector treated you or how frustrated you feel about the debt. Keep your language direct and professional. State the facts, cite the statute, make your demands, and nothing else.

Emotional language also distracts from your substantive requests and gives the collector something to focus on other than proving the debt. Every sentence in your validation letter should serve a specific legal purpose. If a sentence doesn’t demand documentation or invoke a federal protection, it weakens your position by cluttering your request with irrelevant information.

Document Everything and Maintain Your File

Many consumers send a perfect validation letter but then lose the copy or misplace their certified mail receipt. Months later, when a debt collector claims they responded adequately or never received the letter, the consumer has no documentation to support their side. Create a file with the original validation letter, the certified mail receipt showing delivery and the date, and any response from the collector. If the collector calls after you’ve sent your validation letter, document the date, time, caller name, and what they said. Write these notes down immediately.

The FDCPA prohibits collectors from contacting you about a disputed debt until they respond to your validation request, so any contact after your certified letter was delivered is potential evidence of a violation. That documentation becomes invaluable if you file a complaint with the CFPB or pursue legal action against the collector for FDCPA violations. Your paper trail transforms scattered communications into concrete proof of collector misconduct.

Final Thoughts

A debt validation letter forces collectors to prove their case rather than relying on your silence or confusion about your rights. You must identify the exact debt, cite the specific federal statute, demand concrete proof, and send everything via certified mail with return receipt. Collectors count on consumers making mistakes or abandoning their efforts after mailing a validation letter, so your attention to these details eliminates their excuses and compels them to either produce documentation or halt collection efforts.

After you mail your debt validation letter, expect a response within 30 days and review whatever documentation they send against your own records. If they provide complete proof and the debt is legitimate, you can negotiate a settlement, set up a payment plan, or prepare for potential legal action. If their response is incomplete or they fail to respond at all, file complaints with the Consumer Financial Protection Bureau and the Federal Trade Commission, and document every communication from that point forward.

Many consumers discover that debt collectors cannot produce adequate documentation when challenged, while others find errors in amounts, outdated debts, or debts that don’t belong to them at all. If you face collection efforts and need guidance on protecting yourself, we at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia, and Charleston, navigate debt collection issues and defend your consumer rights. Visit us to learn how we can assist you.