A mistake on your credit report can cost you thousands in higher interest rates and rejected loan applications. Yet most people don’t realize they have powerful legal tools to fight back.

We at Hays Cauley, P.C. help South Carolina residents-including those in Greenville, Columbia, and Charleston-understand their credit report dispute rights and take action. This guide shows you exactly what leverage you have under federal law.

How Credit Report Errors Tank Your Financial Life

The Cost of a Single Mistake

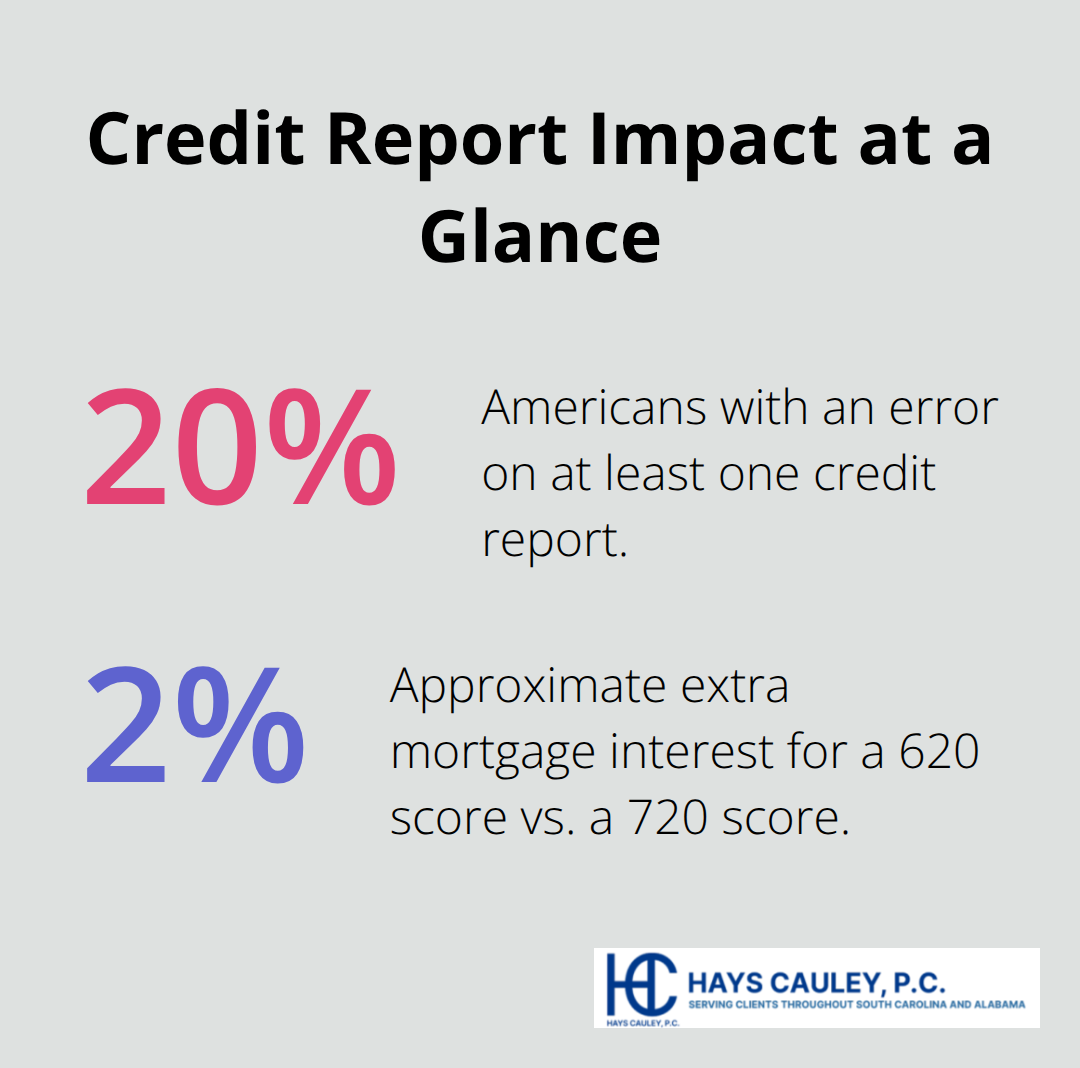

A single error on your credit report can cost you tens of thousands of dollars over time. About 20 percent of Americans have an error on at least one credit report, which means the problem is widespread and serious. When an error appears on your report, lenders immediately penalize you with higher interest rates.

A person with a 620 credit score pays roughly 2 percent more in interest on a mortgage than someone with a 720 score, and that gap widens for auto loans and personal credit lines.

Over a 30-year mortgage on a $300,000 home, a 2 percent rate increase means paying an additional $150,000 or more. Credit bureaus take weeks or months to investigate disputes, during which the damaging information stays active on your report and continues to hurt your score every single day.

Employment and Housing Rejection

The real damage extends far beyond borrowing costs. Employers in South Carolina increasingly pull credit reports before hiring, particularly for positions involving financial responsibility or access to company assets. A negative mark that shouldn’t be there can eliminate you from consideration without you ever knowing why.

Housing is equally brutal. Landlords routinely deny tenants based on credit reports, and a reporting error gives them a false reason to reject your application. A mistake on your file can cost you an apartment or house you would have otherwise qualified for.

The Emotional Toll

If you’re already stressed about finances, credit report errors pile on emotional weight that affects your sleep, relationships, and overall health. The frustration intensifies when you know the error isn’t your fault, yet you’re forced to navigate a complex dispute process while the false information actively destroys your financial opportunities.

This is why understanding your legal rights and taking immediate action matters so much. Every day you wait, the error costs you real money and real opportunities. The good news is that federal law gives you specific tools to fight back-and you have more leverage than most people realize.

Your Legal Rights Under the Fair Credit Reporting Act: Serving South Carolina, Including Greenville, Columbia, and Charleston

Federal law gives you three concrete powers that credit bureaus and creditors must respect. The Fair Credit Reporting Act, codified at 15 U.S.C. §§ 1681–1681x and updated as recently as March 2026, creates enforceable obligations that shift leverage to your side. Understanding these rights stops you from wasting time on weak dispute attempts and positions you to demand real action from the agencies holding your financial future hostage.

Access Your Report Before Disputing Anything

You cannot fight an error you haven’t seen. Pull your free credit reports from all three bureaus-Equifax, Experian, and TransUnion-through AnnualCreditReport.com, which is the only authorized source for truly free reports without hidden charges or credit card requirements. The FCRA guarantees you one free report per bureau per year, and if you place a fraud alert on your file, you get two free reports within a 12-month period.

Pull reports from each bureau at different times rather than all at once. Checking around day 20 after filing a dispute with one bureau can reveal removals before the official 30-day investigation deadline hits. Compare the three reports side by side because errors appear on some bureaus but not others. Look specifically for wrong names, addresses, Social Security numbers, accounts you don’t recognize, incorrect payment history, and balances that don’t match your statements.

Personal information mismatches are easy wins that cost bureaus nothing to fix and signal broader accuracy problems in your file. Once you identify what’s wrong, document it. Photograph or save your reports and highlight the specific errors you plan to challenge.

Demand Investigation and Verification Under Federal Law

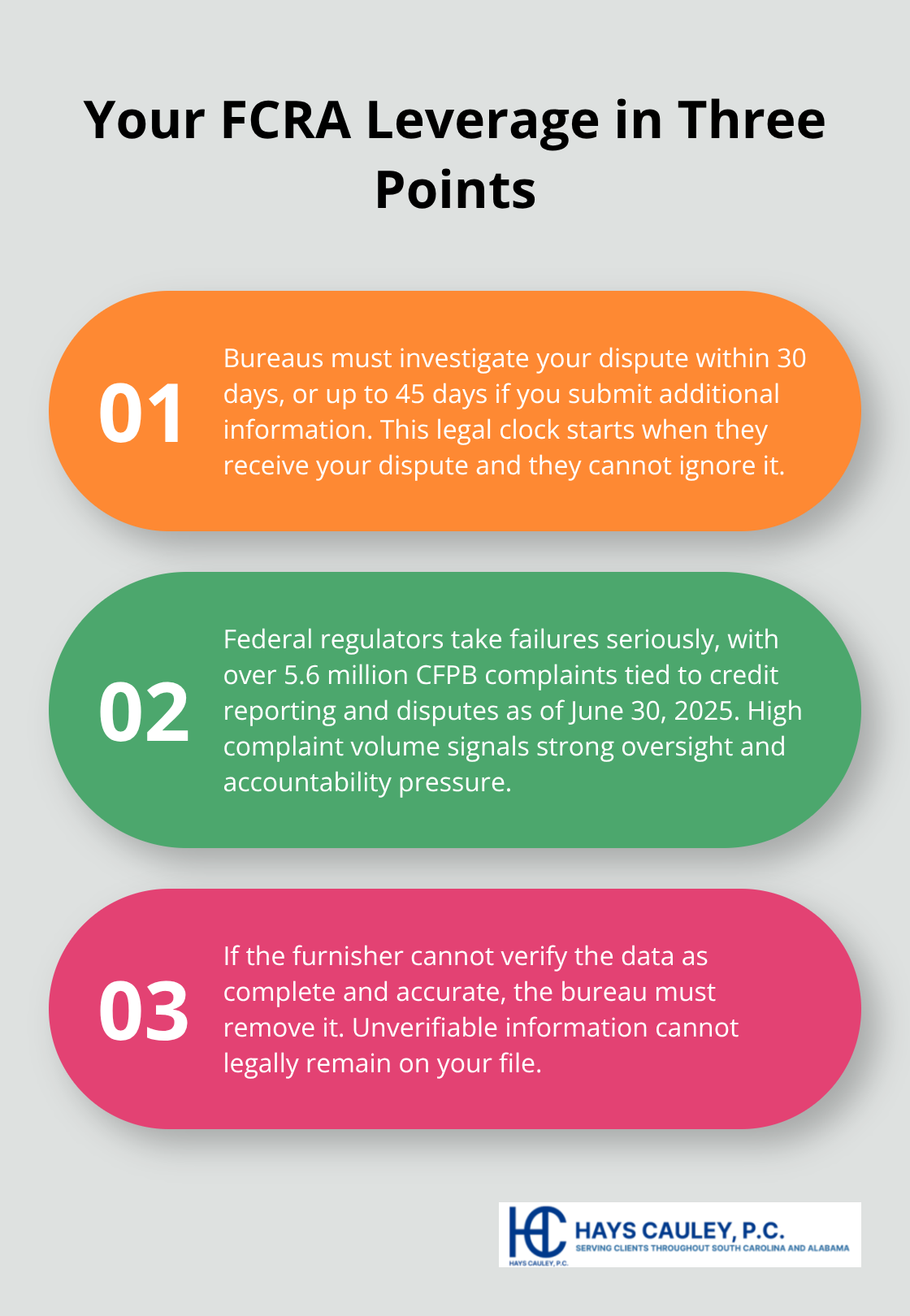

The FCRA gives you the absolute right to dispute any information you believe is inaccurate, and credit bureaus must investigate your claim within 30 days (extending to 45 days if you provide additional information during the process). This investigation requirement is not optional-it’s a legal mandate that furnishers and bureaus cannot ignore without facing enforcement action.

The Consumer Financial Protection Bureau tracked over 5.6 million complaints related to credit reporting and disputes as of June 30, 2025, showing how seriously federal regulators treat failures to investigate properly. When you file a dispute, the bureau must contact the creditor or data furnisher and request verification of the disputed information. Here’s the leverage: if the furnisher cannot verify that the information is complete and accurate, the bureau must remove it.

This standard comes from real court precedent, including Suluki v. Credit One Bank, which established that furnishers cannot legally report unverifiable data. Send your dispute to each bureau via certified mail with return receipt so you have proof of delivery and a clear start date for the 30-day clock. Include copies of supporting evidence-bank statements, creditor correspondence, payment records-but never send originals. File disputes simultaneously with both the bureaus and the creditor directly to create dual pressure; when furnishers face scrutiny from both sides, they investigate more thoroughly and faster.

Receive Notice When Your Information Affects You

The FCRA requires that any company using your credit report to make an adverse decision-denying your loan application, charging you a higher interest rate, or rejecting your rental application-must notify you in writing. This notice must include the name and contact information of the credit bureau that provided the report, and you have the right to request a free copy of that report within 60 days. This rule prevents silent rejections where you never know a credit error cost you an opportunity.

If you’re denied credit, insurance, or housing without explanation, demand the adverse action notice immediately and use it to pull the exact report the creditor saw. That report becomes your evidence for disputing. The CFPB provides free dispute letter templates you can adapt to your situation, removing any excuse about not knowing what to write. Weak disputes with vague language get nowhere; strong disputes identify the specific item, explain exactly why it’s wrong, and request a specific corrective action.

Push Back When Bureaus Reject Your Dispute

If a bureau denies your dispute, you have leverage to push back. Demand the exact verification evidence the bureau relied on to reject your challenge. Under Suluki, if that evidence doesn’t prove the item is accurate, the bureau violated the law by not removing it. At that point, you can file a complaint with the CFPB or explore further action.

Now that you understand your legal foundation, the next step is turning these rights into action. The dispute process itself requires strategy-knowing what documents to gather, how to write an effective dispute letter, and when to escalate your case separates successful challenges from wasted efforts.

Turn Your Evidence Into a Winning Dispute

Assemble Your Complete Evidence Packet

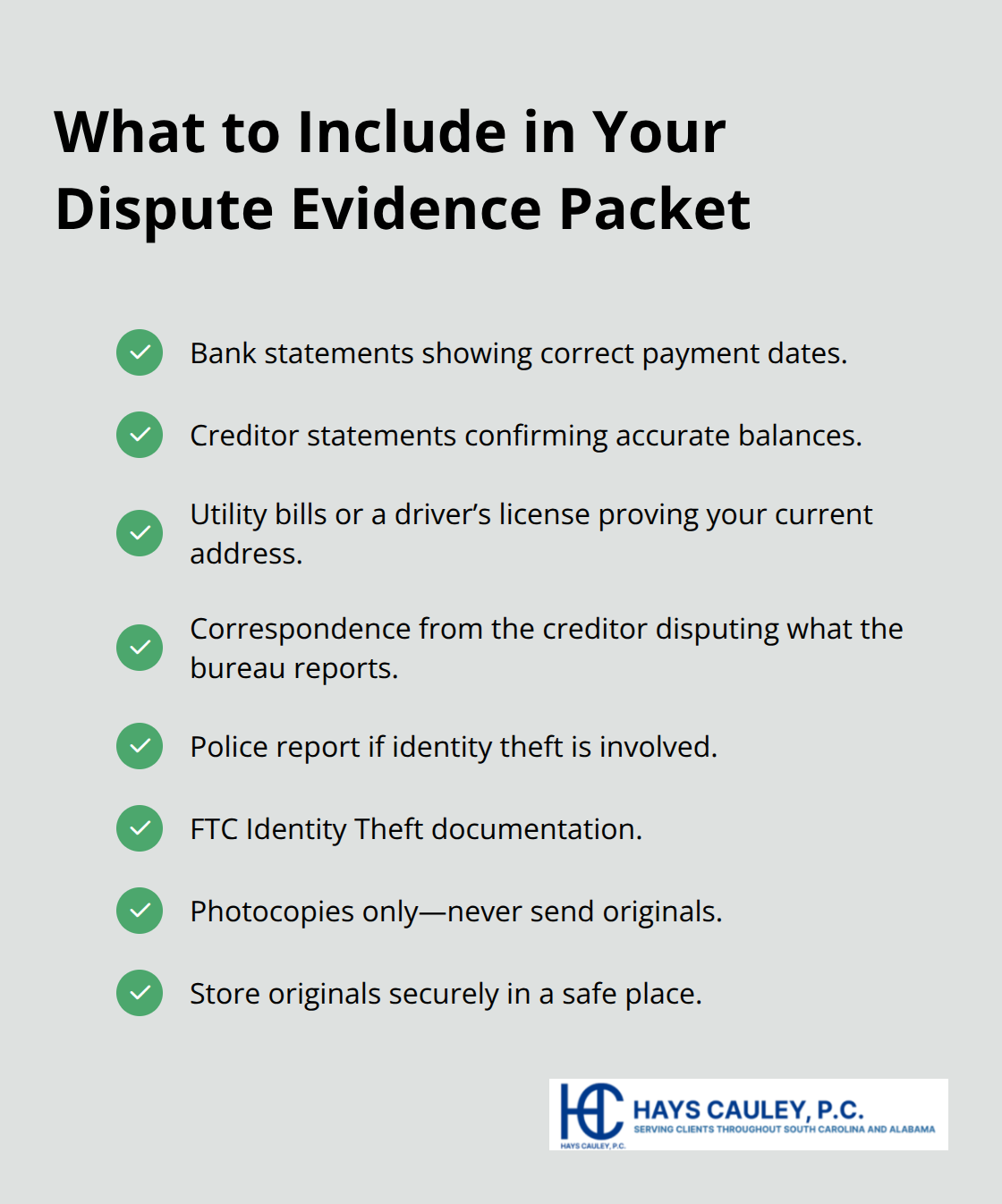

Start by assembling a dispute packet before you write a single word to the credit bureau. Pull copies of every document that supports your claim: bank statements showing correct payment dates, creditor statements with accurate balances, utility bills or driver’s licenses proving your current address, and any correspondence from the creditor disputing what the bureau reports. If the error involves identity theft or fraud, include your police report and identity theft documentation from the Federal Trade Commission.

Never send originals-photocopy everything and keep the originals in a safe place. This packet becomes your evidence that the furnisher cannot verify the information as accurate, which is the standard that forces removal under federal law.

Write a Clear, Factual Dispute Letter

Write your dispute letter in plain, factual language that avoids emotion or legal jargon. State your full name and current address, identify the specific item you’re disputing by account number or creditor name, explain exactly why it’s wrong (the payment was made on time, the account isn’t yours, the balance is incorrect), and request the specific action you want (removal or correction). The CFPB provides free templates, but your letter doesn’t need fancy language-clear and specific beats elaborate every time. Send copies of your supporting documents with the letter, not the originals.

File Disputes and Start the Investigation Clock

Mail your dispute to each of the three credit bureaus via certified mail with return receipt requested. This creates proof of delivery and starts the 30-day investigation clock. The certified mail receipt becomes your evidence that the bureau received your dispute on a specific date. File disputes simultaneously with both the credit bureaus and the creditor or data furnisher directly. When furnishers face dual investigation pressure from both the bureau and a direct challenge, they respond faster and more thoroughly than they do to bureau requests alone. This dual-filing strategy cuts investigation time and increases the odds that unverifiable information gets removed.

Monitor Progress and Escalate When Necessary

Track your progress starting at day 20 after filing. Pull your credit reports again from each bureau around that time to spot removals before the official 30-day deadline expires. The bureaus often complete investigations early, and checking early reveals what’s happening without waiting until day 30. Document every response you receive, including the date, the bureau’s name, and exactly what they said about your dispute. If you don’t hear back within 35 days, file a complaint with the Consumer Financial Protection Bureau immediately-the CFPB tracked over 50,000 credit reporting complaints in 2023, and your complaint triggers federal oversight of the bureau’s failure.

Demand Verification Evidence and Push Back on Denials

If a bureau denies your dispute, demand the exact verification evidence they relied on. Under Suluki v. Credit One Bank, if that evidence doesn’t prove the item is accurate and complete, the bureau violated the law. Push back in writing, cite the furnisher’s failure to verify, and escalate to the CFPB if the bureau won’t budge. We at Hays Cauley, P.C. help South Carolina residents navigate these disputes and demand accountability when bureaus or furnishers fail to investigate properly.

Final Thoughts

Your credit report dispute rights shift power back to you when errors damage your financial life. The Fair Credit Reporting Act gives you the right to access your reports, demand investigation of inaccurate information, and receive notice when credit decisions affect you. These rights exist because regulators recognize that credit reporting errors are widespread and costly-about 20 percent of Americans have errors on their reports, and the Consumer Financial Protection Bureau received over 5.6 million complaints related to credit reporting disputes as of June 30, 2025.

The dispute process itself is straightforward when you follow the steps outlined here. Pull your reports from all three bureaus, identify specific errors, gather supporting documentation, and file disputes via certified mail with return receipt. The leverage comes from a simple fact: furnishers cannot legally report information they cannot verify as accurate and complete. When you force verification through a properly filed dispute, unverifiable errors get removed.

Starting today matters more than waiting for the perfect moment, since every day an error remains on your report costs you real money through higher interest rates and lost opportunities. If disputes stall or bureaus reject your challenges without valid evidence, contact Hays Cauley, P.C. to explore your options for credit report dispute rights in South Carolina.