Your credit report just got more complicated. South Carolina’s credit reporting laws have shifted, and these changes directly impact how your credit score is calculated and protected.

At Hays Cauley, P.C., we’re breaking down what’s changed and what it means for you. This SC credit report update affects everything from dispute timelines to your access rights.

What’s Actually Changed in South Carolina’s Credit Laws

Federal Fee Changes and Free Monitoring Options

Federal credit reporting rules shifted significantly in 2026, and South Carolina lawmakers are moving to add their own protections on top. The Fair Credit Reporting Act fee structure changed this year, with the FCRA file disclosure fee increasing to $16 in 2026, according to the Federal Register. However, free weekly credit file disclosures from Equifax, Experian, and TransUnion remain available throughout 2026, meaning you can monitor your credit reports at no cost every seven days if you choose. This matters because about 20% of consumers have errors on at least one credit report, and catching those errors early prevents them from tanking your score.

Employment and Credit Score Protections

Two significant South Carolina bills are reshaping how credit information gets used. House Bill 3462 would prohibit employers from using your credit score in hiring, promotion, or termination decisions, with violations classified as misdemeanors. This protection addresses a real concern: employers have historically pulled credit reports for employment screening, but your credit history has nothing to do with job performance. If enacted, even granting you an interview could not be based on your credit score.

Medical Debt Reporting Restrictions

House Bill 4149 targets medical debt specifically. It would prohibit creditors and debt collectors from reporting South Carolina medical facility debt to consumer reporting agencies, and it would bar the bureaus from including such debt on consumer reports. This change covers debts from hospitals, nursing facilities, medical offices, physical therapists, and other Title 44-licensed providers operating in South Carolina. Medical debt has historically crushed credit scores unfairly, and this bill recognizes that reality.

Student Loans and Mortgage Threshold Updates

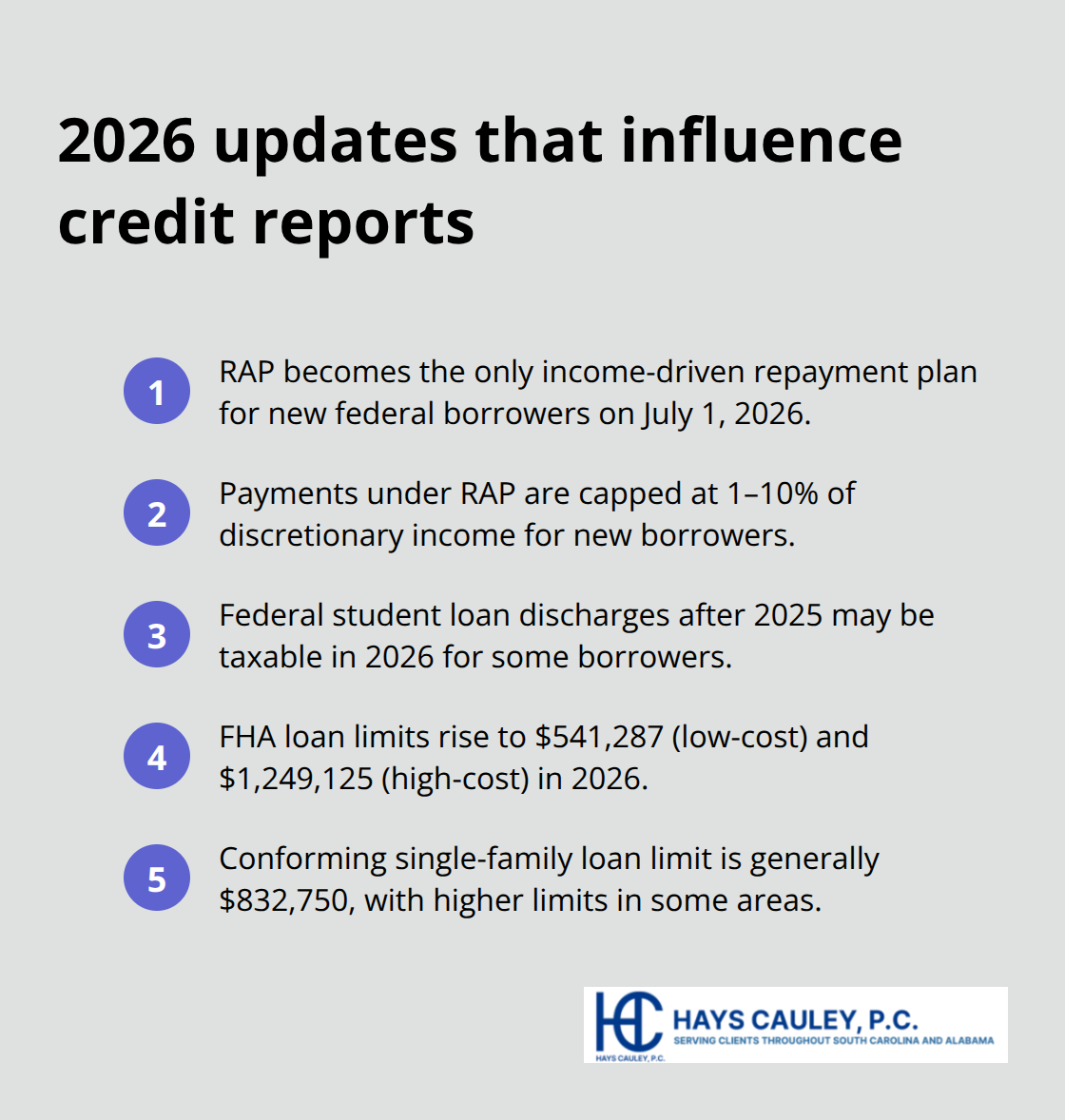

Federal student loan discharges after 2025 may create taxable income in 2026, potentially increasing tax burdens for South Carolina borrowers and affecting overall debt-to-income ratios that lenders evaluate. Additionally, the new Repayment Assistance Plan becomes the only income-driven repayment option for new federal borrowers starting July 1, 2026, which means student loan payments will be reported differently on credit histories going forward. Mortgage rules also tightened in 2026. FHA loan limits increased to $541,287 for low-cost areas and $1,249,125 for high-cost areas, and conforming loan limits for single-family Fannie Mae and Freddie Mac loans are generally $832,750 (with higher limits in some areas). These threshold changes affect which borrowers qualify for certain loan products and how those loans appear on credit reports.

Taking Action on Your Credit Report

South Carolina residents should expect credit bureaus to update their systems throughout 2026 as these state and federal changes roll out. If H.4149 becomes law, you should review your credit reports from all three bureaus and dispute any South Carolina medical facility debt that appears in error. Correcting errors can meaningfully improve your score, sometimes by 50 points or more. If you suspect any inaccuracy on your report, submit a dispute directly to the bureau with specific details and supporting documents. The bureaus must investigate within 30 days and correct verified inaccuracies at no cost to you. These changes create both challenges and opportunities-understanding your rights under the updated laws positions you to protect your financial future.

How Your Credit Score Changes in 2026

Medical Debt Removal Creates Immediate Score Improvements

Medical debt removal represents the most direct way these changes will improve your credit score. If House Bill 4149 becomes law, South Carolina medical facility debt will disappear from credit reports, and for many borrowers this means an immediate score boost. Medical debt currently crushes scores unfairly because it reflects medical necessity, not financial irresponsibility. A consumer with a $5,000 hospital bill in collections suffers the same credit damage as someone who maxed out credit cards for discretionary purchases. Once H.4149 takes effect, creditors and debt collectors cannot report South Carolina medical facility debt to Equifax, Experian, or TransUnion, and the bureaus must exclude it from reports.

This creates a tangible advantage for South Carolina consumers compared to residents in other states still burdened by medical debt reporting. If you have existing medical debt on your report from South Carolina providers, file a dispute immediately after the law passes. The 30-day investigation window means you could see corrections within a month, potentially raising your score by 50 points or more (depending on the debt amount and your overall credit profile).

Student Loan Payment Reporting Changes

Student loan payment reporting changes also affect how lenders view your creditworthiness starting July 1, 2026. The new Repayment Assistance Plan caps payments at 1 to 10 percent of discretionary income for new federal borrowers, eliminating negative amortization and offering forgiveness after 30 years. This means your student loan payment history will look different on credit reports going forward, potentially showing lower monthly obligations than previous income-driven plans reported. Additionally, federal student loan discharges after 2025 may create taxable income in 2026, which increases your tax burden but does not directly damage your credit unless you fail to pay the resulting tax debt.

These shifts require you to review your credit reports quarterly through 2026 to verify that lenders are reporting your accounts correctly under the new rules. Use the free weekly disclosures available from all three bureaus to catch reporting errors early. If a lender reports your student loan payment incorrectly or fails to reflect the new payment structure, dispute it within 30 days of discovering the error so the bureau investigates and corrects it at no cost to you.

Monitoring Your Reports During the Transition

The transition period through 2026 demands active attention from you. Credit bureaus will update their systems as state and federal changes roll out, and reporting inconsistencies may occur during this time. Check your reports from all three bureaus using the free weekly disclosure option rather than waiting for annual reports. This approach (staggering your checks every few weeks) allows you to spot errors before they compound and damage your score further. When you identify an inaccuracy, submit your dispute with specific details and supporting documents to accelerate the investigation process.

The changes unfolding in 2026 create both challenges and opportunities for South Carolina borrowers. Understanding how medical debt removal and student loan reporting changes affect your score positions you to take action before these shifts fully take effect. Your next step involves understanding which specific protections apply to you and how to exercise your rights under South Carolina’s evolving credit laws.

What Rights Do You Actually Have Under South Carolina’s New Credit Laws

Access Your Credit Reports for Free Every Week

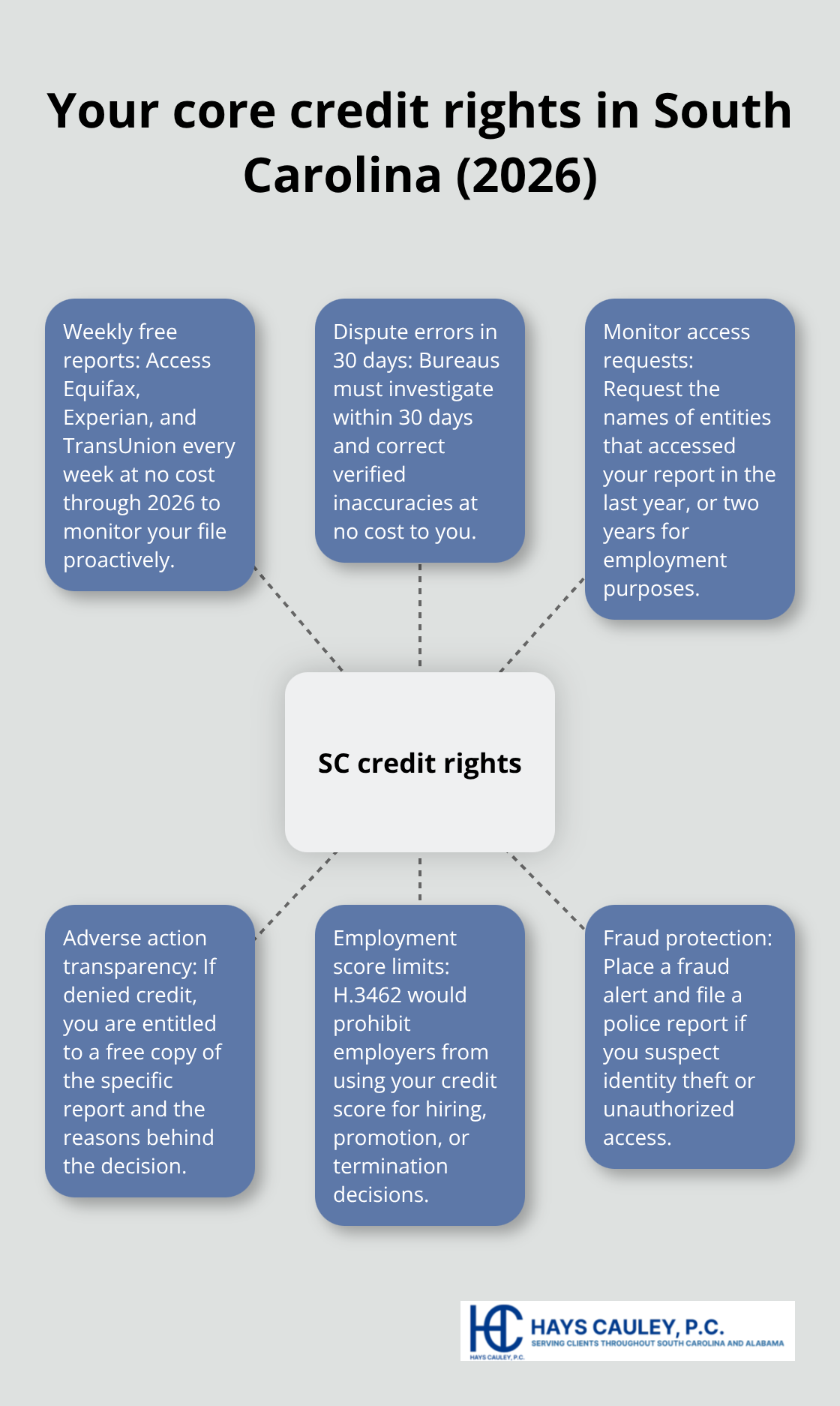

South Carolina’s updated credit laws give you concrete rights that work in your favor, and the 2026 changes strengthen your position significantly. You can access your credit report from Equifax, Experian, and TransUnion for free every week through the end of 2026, which means you have 52 opportunities per year to monitor what lenders and creditors see about you. This matters because the Federal Register noted that the FCRA file disclosure fee increased to $16 in 2026, but the free weekly option remains available indefinitely, making it the smart choice for ongoing monitoring. Use this access to catch errors early.

About 20% of consumers have errors on at least one credit report according to the FTC, so regular checks aren’t optional-they’re necessary.

Challenge Inaccuracies at No Cost

When you spot an inaccuracy, you have the right to challenge it directly with the bureau at no cost. The bureau must investigate within 30 days and correct verified errors, and you can request the investigation results in writing. Submit your dispute with specific details about which item is wrong and include copies of supporting documents that prove your claim. Most negative information stays on your report for seven years, but errors corrected early prevent years of damage to your credit score. Correcting errors can meaningfully improve your score, sometimes by 50 points or more (depending on the debt amount and your overall credit profile).

Spot Unauthorized Access and Fraud

Your right to protect against unauthorized inquiries gives you another layer of defense. You can request the names of individuals or organizations that accessed your credit report in the last year, or two years for employment purposes, allowing you to spot unauthorized access immediately. If you suspect fraud, place a fraud alert on your file and file a police report with law enforcement. South Carolina had 18,935 identity theft cases reported in 2022, so this protection matters.

Know Why You Were Denied Credit

If you’re denied credit based on information in your report, you’re entitled to a free copy of that specific report and the right to know which items influenced the decision. This lets you challenge the decision if the information was inaccurate. Under House Bill 3462, employers also cannot use your credit score as the basis for hiring, promotion, or termination decisions if that bill becomes law, adding employment protection on top of your existing rights. These rights exist to keep your credit file accurate and protect you from discrimination based on credit information that may not reflect your actual financial responsibility.

Final Thoughts

Access your free weekly credit reports from Equifax, Experian, and TransUnion to monitor what lenders see about you. About 20% of consumers have errors on at least one credit report, so regular checks prevent years of score damage. When you spot an inaccuracy, submit a dispute with specific details and supporting documents-the bureau must investigate within 30 days and correct verified errors at no cost to you.

Once House Bill 4149 becomes law, review your reports for any South Carolina medical facility debt and dispute it immediately. This SC credit report update could boost your score significantly by removing debt that reflects medical necessity, not financial irresponsibility. Request the names of individuals or organizations that accessed your credit report in the last year to monitor for unauthorized access, and place a fraud alert on your file if you suspect identity theft.

We at Hays Cauley, P.C. help South Carolina consumers navigate credit reporting, identity theft, and debt issues. If you need guidance on exercising your rights under these updated laws or addressing errors on your credit report, contact us for support. Your credit file directly affects your ability to borrow, rent, and build wealth.