A mistake on your credit report can cost you thousands of dollars in higher interest rates or denied loan applications. Credit report errors in SC are more common than you’d think, and many people don’t realize they have inaccurate information dragging down their credit score.

We at Hays Cauley, P.C. help South Carolina residents fix these problems and protect their financial futures. This guide walks you through identifying errors, disputing them with credit bureaus, and reclaiming your credit file.

How Credit Report Errors Happen

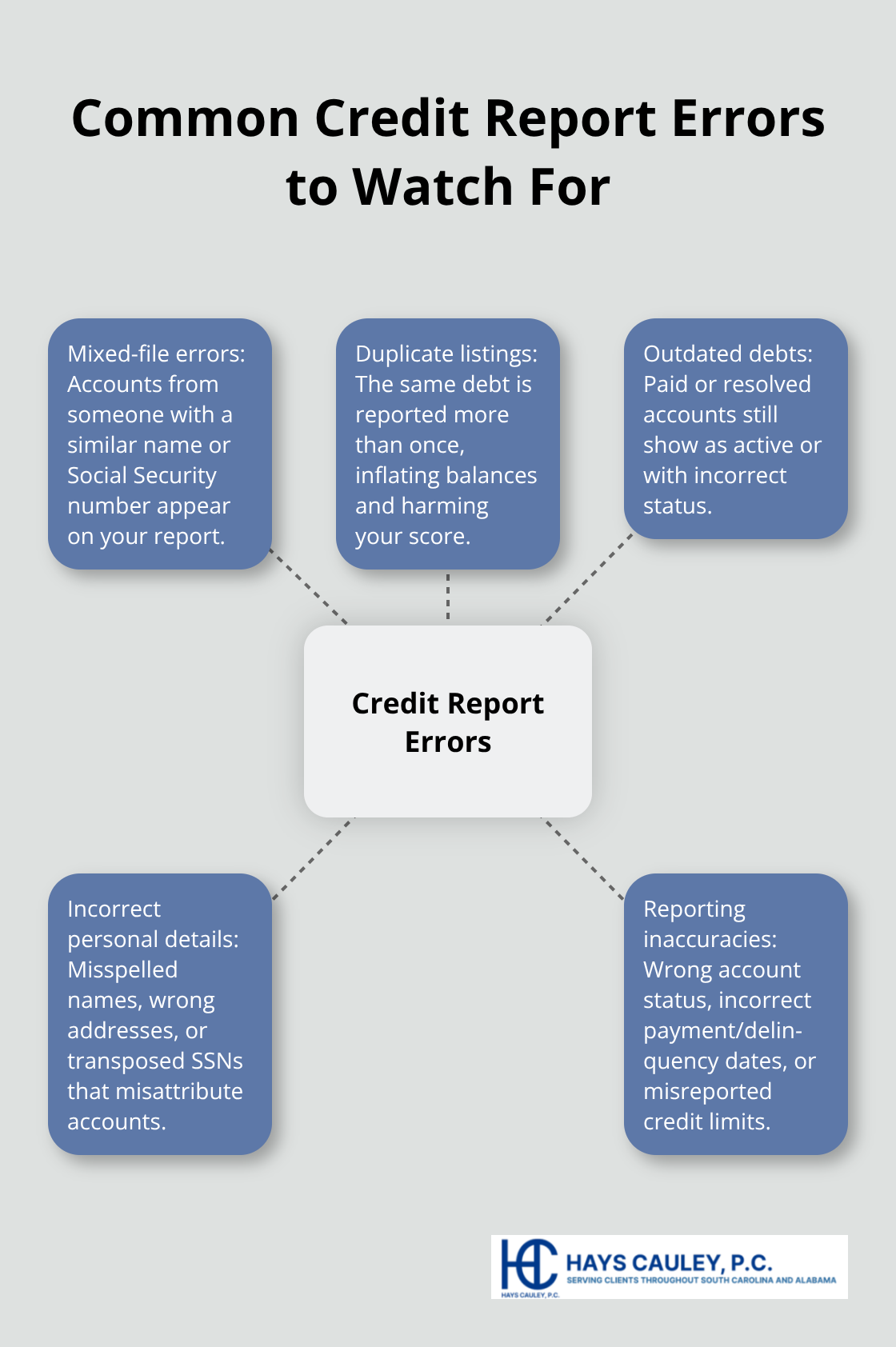

Common Types of Mistakes Found on Credit Reports

Credit report errors fall into several distinct categories, and understanding which ones plague your file matters for fixing them fast. Accounts that don’t belong to you appear frequently-these mixed-file errors occur when a credit bureau combines information from two consumers with similar names or Social Security numbers. Duplicate listings of the same debt also wreak havoc, artificially inflating your outstanding balance and tanking your score. Outdated debts show as active balances instead of paid or resolved accounts, creating another common problem. Incorrect personal details like misspelled names, wrong addresses, or transposed Social Security numbers cause accounts to be misattributed to your file entirely. Even small reporting errors-wrong account status, incorrect dates for payment or delinquency, or misreported credit limits-compound damage over time.

You’ll catch some of these errors immediately when reviewing your reports, but others hide in plain sight because they match your legitimate history closely enough to slip past a quick scan. The variety of mistakes means you need to look carefully at every section of your credit file.

Why Lenders and Credit Bureaus Make These Errors

Credit bureaus process millions of reports monthly, and furnishers (creditors and debt collectors) submit information with varying levels of accuracy and consistency. Many furnishers use outdated systems or fail to verify information before reporting, meaning errors propagate automatically. The volume alone creates inevitable mistakes.

These aren’t rare occurrences. Inaccurate information on your credit report costs real money-even small errors reduce your credit score, which directly raises your borrowing costs. A 50-point drop in your score can increase mortgage interest rates by roughly 0.5 percent, costing you tens of thousands over a 30-year loan. Car loans, credit cards, and employment opportunities all hinge on accurate reporting.

Impact of Inaccuracies on Your Credit Score and Finances

Correcting errors promptly protects your financial opportunities. The Fair Credit Reporting Act gives you the right to dispute inaccurate information, with credit bureaus required to investigate within 30 days at no charge. This legal protection exists specifically because errors happen so often and cause measurable harm to consumers.

The next step involves pulling your actual credit reports and learning exactly what information the bureaus hold about you.

Steps to Identify and Document Credit Report Errors Serving South Carolina, including Greenville, Columbia and Charleston

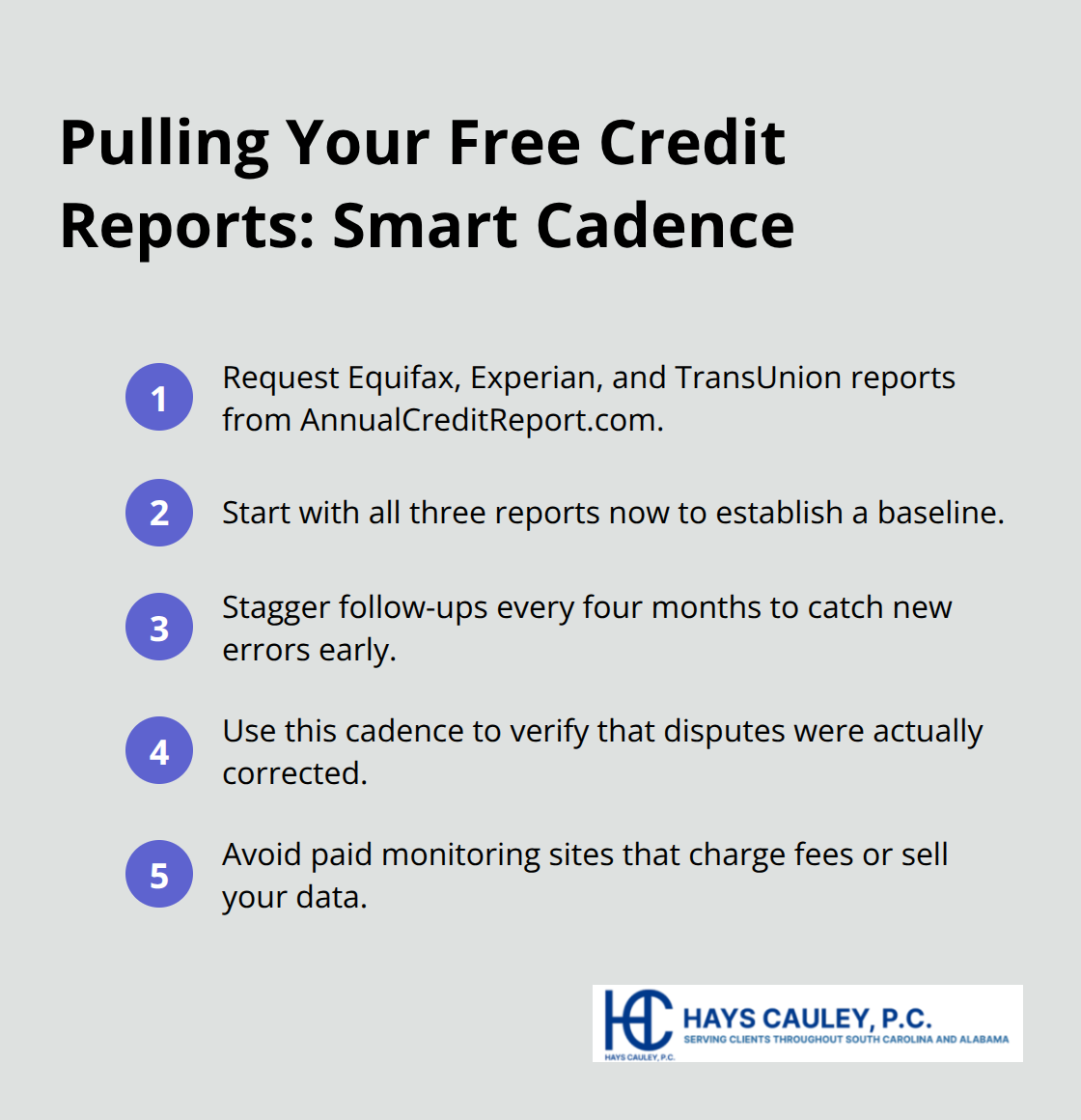

Obtain Your Free Credit Reports from All Three Bureaus

Pull all three credit reports from Equifax, Experian, and TransUnion through AnnualCreditReport.com, the official FTC-authorized source. You can request one report from each bureau immediately, then pull additional reports every four months throughout the year to monitor for new errors or fraud. This staggered approach catches mistakes early and tracks whether disputes actually resolved the problems. Don’t use credit monitoring services or third-party sites-they charge fees or sell your data, and the official government resource costs nothing.

Review Your Reports Thoroughly for Discrepancies

Once you have all three reports in hand, scan the personal information section first. Look for misspelled names, incorrect addresses, wrong phone numbers, or transposed Social Security numbers, as these details signal mixed-file errors or identity theft. Next, examine every account listed and flag any accounts you don’t recognize immediately-these often belong to someone else entirely or resulted from fraudulent applications.

Check the account status for each one: closed accounts must show closed, current accounts must not appear late or delinquent, and opening dates plus last payment dates must match your records. Watch for duplicate listings of the same debt under different names or account numbers (this is one of the most damaging yet fixable errors). Look at hard inquiries too; unauthorized inquiries indicate potential fraud or a creditor pulling your report without permission.

Gather Evidence and Documentation of Errors

Pull receipts, statements, cancelled checks, court documents, and any correspondence proving you paid an account or that an account never belonged to you. Organize these materials in a single folder with your marked-up credit reports. Create a simple spreadsheet listing each error: the account number, the inaccuracy, why it’s wrong, and which bureau reported it. This organization prevents errors from slipping through during the dispute process and gives you a clear record if you later need to escalate to an attorney.

The Federal Trade Commission provides sample dispute letters on their website that you can customize for each error, which streamlines the process and ensures you include all required details. Send disputes by certified mail with return receipt to both the credit bureau and the furnisher (the creditor that reported the information), as this creates an undeniable delivery record. The furnisher has approximately 30 days to investigate and respond; if the information is found inaccurate, they must notify all three bureaus of the correction.

With your documentation complete and disputes submitted, you now move into the critical phase of tracking responses and following up on results.

How to Dispute Credit Report Errors Serving South Carolina, including Greenville, Columbia and Charleston

File Your Dispute with the Credit Bureau

Start your dispute process immediately after gathering your documentation. Contact the credit bureau that reported the error first by sending a formal dispute letter via certified mail with return receipt. The Fair Credit Reporting Act requires credit bureaus to investigate your claim within 30 days at no cost, and certified mail proves you sent the letter and when it arrived. Address your dispute to the specific bureau’s dispute department (Equifax at 1-800-685-1111, Experian at 1-888-397-3742, or TransUnion at 1-800-916-8800), include your full name and current address, reference your credit report confirmation number, list the specific account number and the exact inaccuracy, and clearly state what correction you want. Never send original documents; include only copies of your supporting evidence like receipts, statements, or court records.

Send a Dispute Letter to the Furnisher

Send an identical dispute letter to the furnisher (the creditor or debt collector that reported the information) on the same day, using certified mail as well. The furnisher also has 30 days to investigate, and if they find the information inaccurate, they must notify all three bureaus of the correction. This dual approach forces both parties to verify the claim independently, which significantly increases your odds of success.

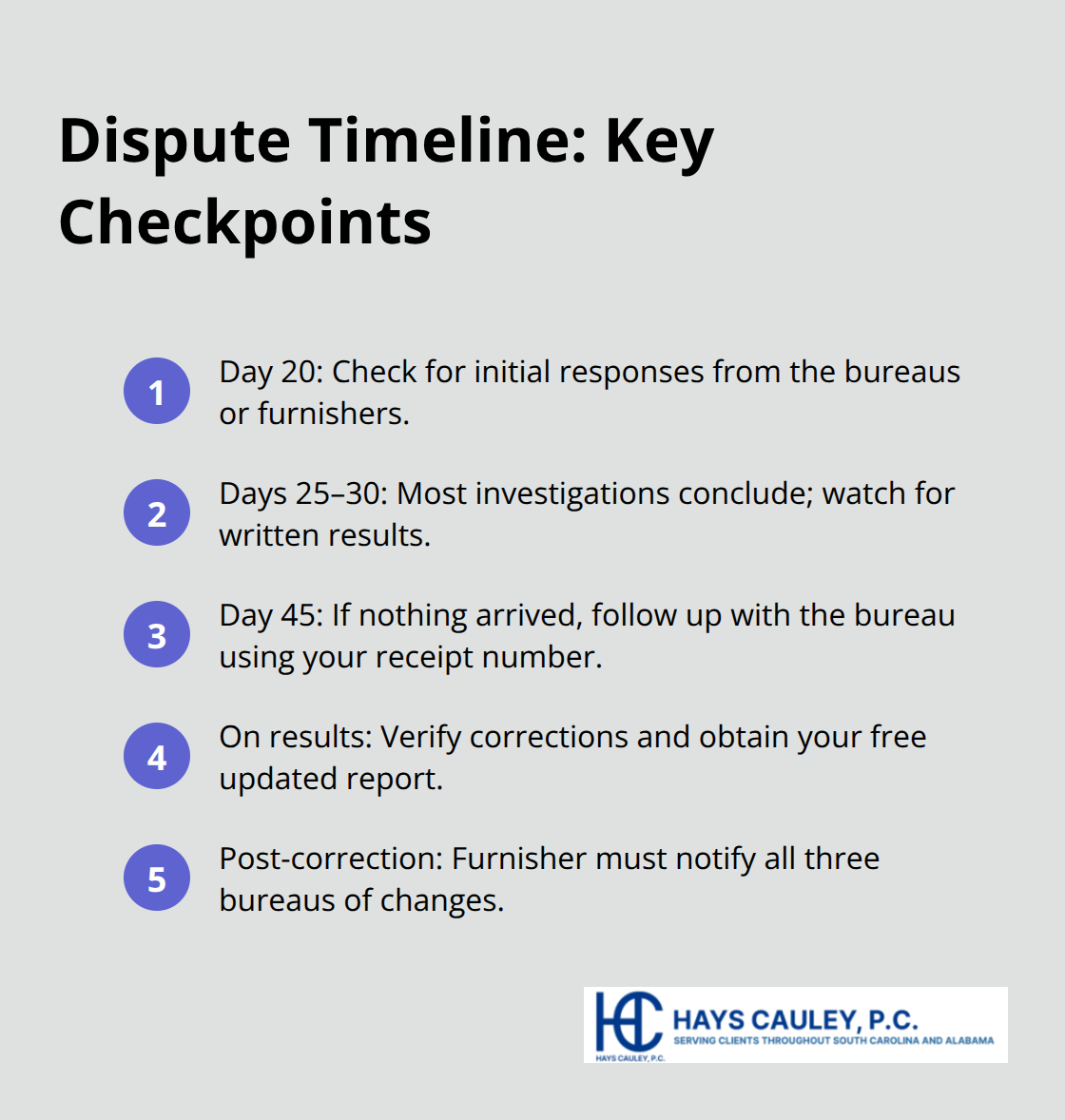

Track Your Dispute Progress

After mailing your disputes, mark your calendar for day 20 and check for responses. Most investigations complete between days 25 and 30, so contact the bureau on day 45 if you haven’t received written results. Reference your certified mail receipt number when following up. Once you receive the investigation results, review them carefully; if the bureau corrected the error, you’ll get a free updated credit report and the furnisher must notify all three bureaus.

Handle Denied Disputes and Next Steps

If the dispute was denied, the bureau must provide the reason, the furnisher’s contact information, and a description of their investigation procedures. If corrections still haven’t been made and you believe the error remains, you can request a dispute statement to be included in your file and on future reports, or you can escalate to legal action. A consumer protection attorney can file formal complaints, draft demand letters, and represent you in court if necessary to enforce your rights under federal law. We at Hays Cauley, P.C. help South Carolina residents pursue these escalated disputes when credit bureaus and furnishers fail to correct errors.

Final Thoughts

The Fair Credit Reporting Act protects your right to accurate information on your credit file, and credit report errors SC happen frequently enough that federal law mandates free dispute investigations within 30 days. Correcting errors on your credit file opens doors that inaccuracies had closed-a corrected report improves your approval odds for mortgages, car loans, and credit cards while lowering your borrowing costs significantly. A single error costing you a half-point increase in mortgage interest rates translates to tens of thousands of dollars over the life of a loan.

Start protecting your credit immediately by pulling your free annual reports from all three bureaus through AnnualCreditReport.com, then review them carefully for mixed-file errors, duplicate debts, outdated information, and accounts you don’t recognize. Document every discrepancy with supporting evidence and send formal dispute letters via certified mail to both the credit bureau and the furnisher, tracking your disputes and following up if responses don’t arrive by day 45. If credit bureaus or furnishers ignore your disputes or refuse to correct errors despite clear evidence, you have legal remedies available through complaints to the Consumer Financial Protection Bureau or civil action to enforce your rights.

We at Hays Cauley, P.C. help South Carolina residents navigate escalated disputes when the standard process fails, handling credit reporting and identity theft issues for residents throughout Greenville, Columbia, and Charleston. Contact us if disputes stall or if you need guidance pursuing corrections that credit bureaus refuse to make.