Credit report errors can wreck your finances, and debt collectors often break the rules to pressure you into paying. We at Hays Cauley, P.C. help South Carolina residents fight back against these violations.

An FCRA attorney South Carolina can recover money from companies that harm your credit rights. This guide shows you how to find the right firm to protect yourself.

What the FCRA Actually Does for You

The Fair Credit Reporting Act is a federal law that gives you the power to challenge companies when they report false information about you. Passed in 1970, the FCRA requires credit reporting agencies to maintain accurate records and gives you the right to dispute errors within 30 days of discovery. Credit reporting agencies process hundreds of millions of transactions daily, which means errors slip through constantly. Your credit report determines whether you qualify for loans, mortgages, rental housing, and even some jobs, making accuracy non-negotiable. When inaccurate information stays on your report, it can cost you thousands in higher interest rates or rejection from housing and employment opportunities.

The Most Common Errors That Destroy Your Credit

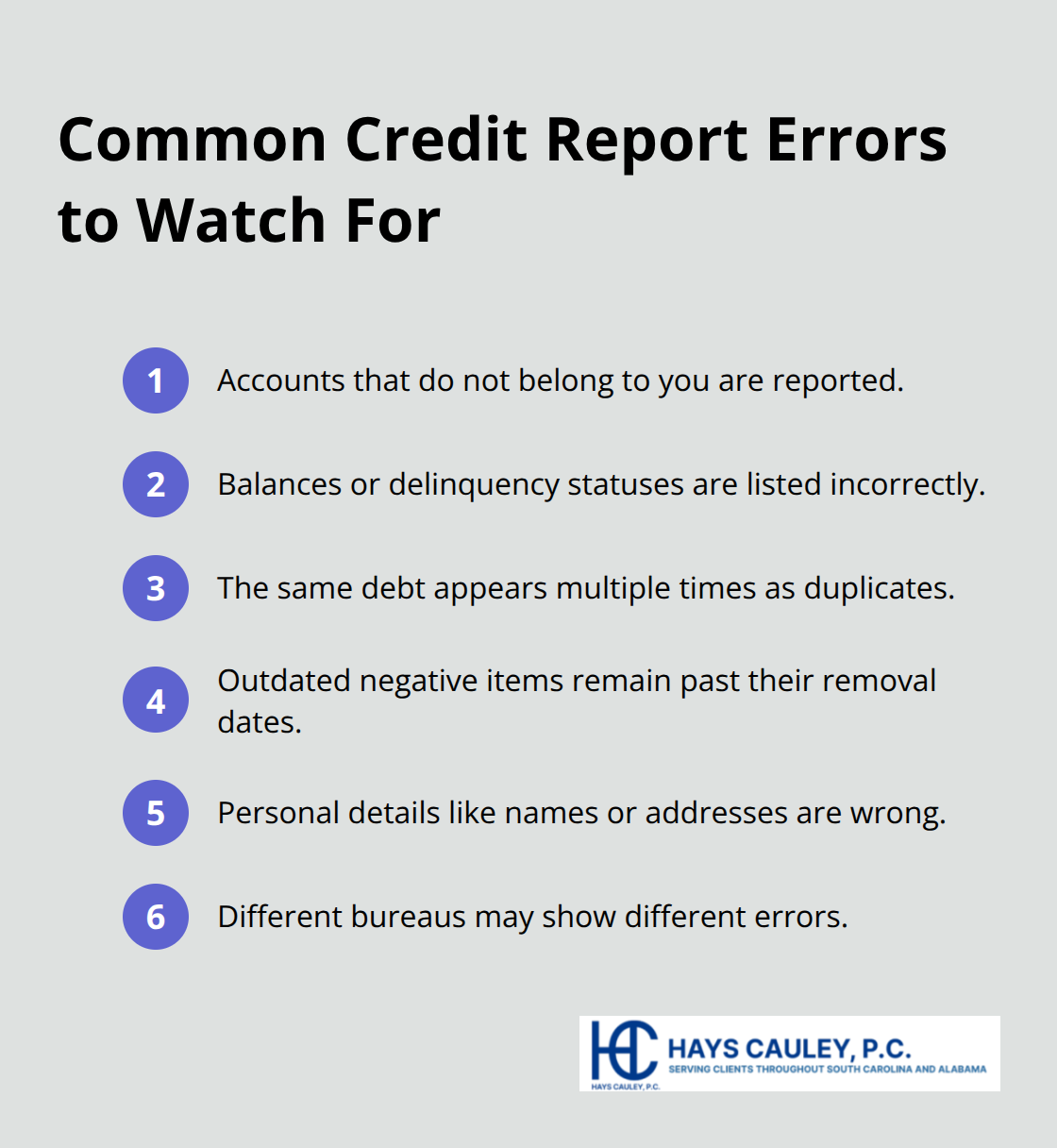

Account errors appear frequently on credit reports and include accounts that do not belong to you, incorrect balances, or wrong delinquency statuses. Duplicate accounts listing the same debt multiple times can tank your credit score unnecessarily. Outdated information that should have been removed years ago still haunts many South Carolina residents, with negative items appearing well past their expiration dates. Personal information errors like incorrect names, addresses, or Social Security numbers create chaos when lenders cannot match your report to your identity.

The four major agencies-Equifax, Experian, TransUnion, and Innovis-maintain these reports, and each one can contain different errors.

Why Credit Bureaus Resist Fixing Mistakes

Credit reporting agencies have little intrinsic motivation to correct inaccuracies because they profit from volume, not accuracy. When you dispute an error, the agency must investigate within 30 days, but many ignore disputes or conduct cursory reviews instead. Debt collectors and creditors who report false information face minimal consequences unless you take legal action. This is where the FCRA gives you teeth. If a bureau or furnisher fails to correct a verified mistake, you have a private right of action to sue for actual damages, statutory damages up to $1,000 per violation, and attorney’s fees. Willful violations result in punitive damages. In South Carolina, the statute of limitations runs two years from discovery or five years from the date of the violation, so acting promptly protects your remedies and deters further misconduct.

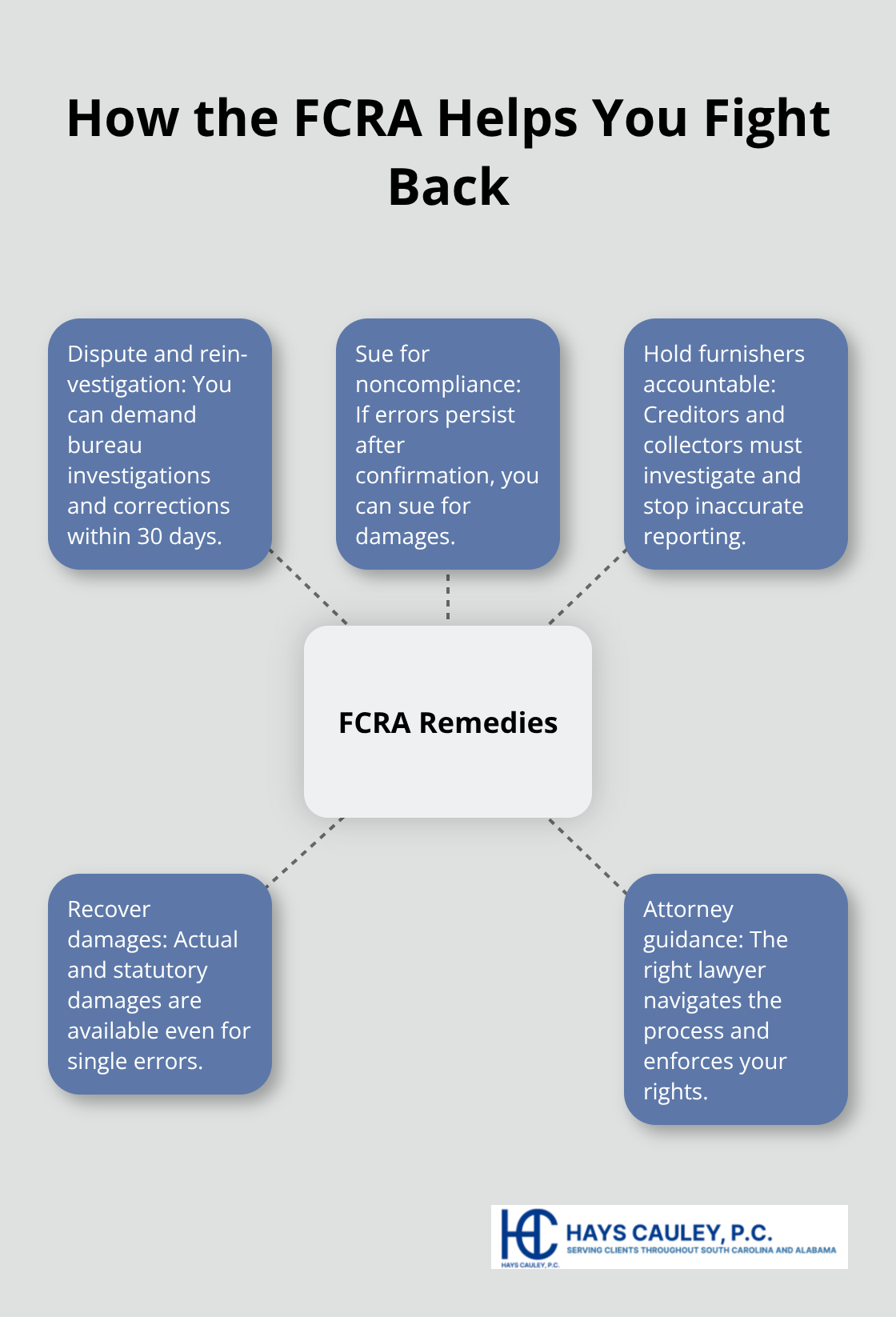

How the FCRA Empowers You to Fight Back

The FCRA provides specific tools to recover money from companies that harm your credit rights. You can demand that credit bureaus investigate disputed items and correct verified errors (within 30 days). If they refuse to fix a mistake they confirmed, you can pursue legal action for damages. The law also requires that creditors and debt collectors who furnish false information to bureaus must investigate your disputes and stop reporting inaccurate data. Many South Carolina residents do not realize they can recover actual damages plus statutory damages, making legal action a realistic option even for single errors.

The right attorney helps you navigate these remedies and hold violators accountable.

Why You Need an FCRA Attorney in South Carolina

Credit Report Errors Cost Real Money

Most South Carolina residents assume they can handle credit report disputes alone, but the math tells a different story. A single error on your credit report costs the average consumer between $5,000 and $10,000 in additional interest charges over a lifetime, according to consumer advocacy data. When a credit bureau ignores your dispute or a debt collector continues reporting false information after you’ve challenged it, you need legal firepower to recover damages. The FCRA allows you to sue for actual damages plus statutory damages up to $1,000 per violation, and if the violation was willful, you can pursue punitive damages on top of that. Most people do not realize this leverage exists, which means credit bureaus and debt collectors operate without real consequences until an attorney gets involved.

Debt Collectors Break FCRA Rules Constantly

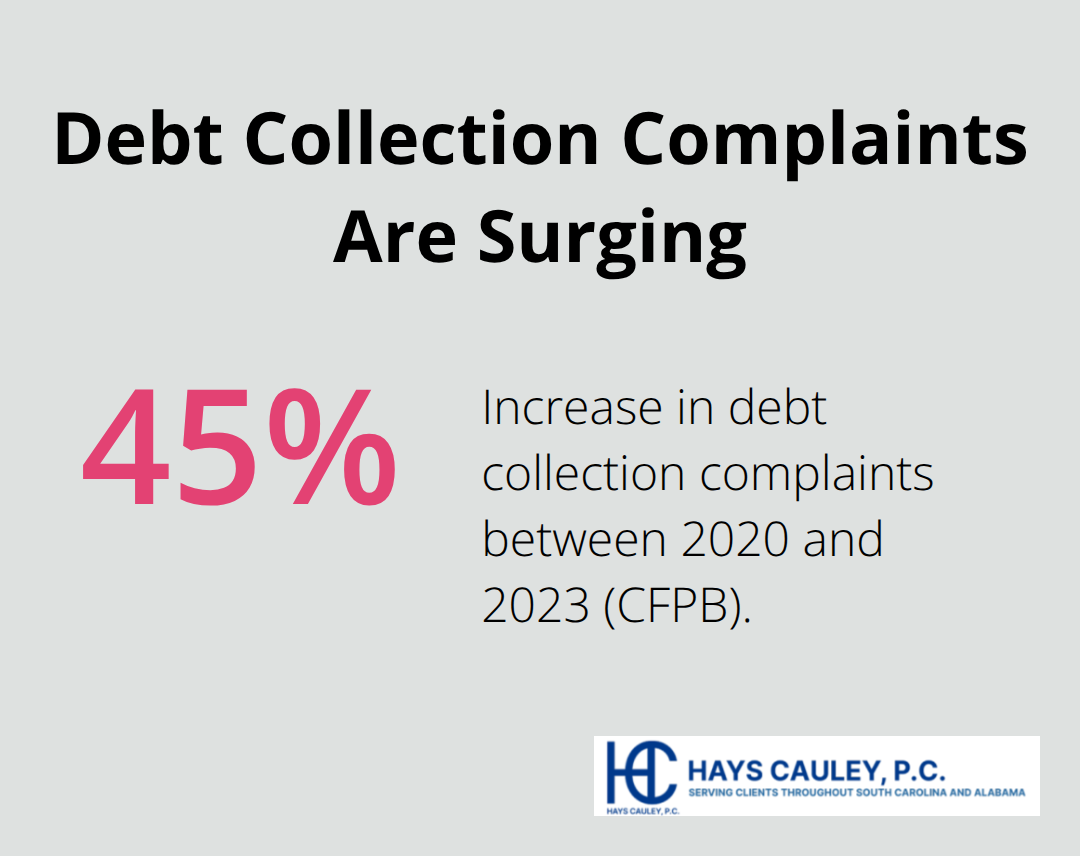

Debt collectors represent another urgent reason to hire representation immediately. The Consumer Financial Protection Bureau reported that debt collection complaints increased 45 percent between 2020 and 2023, with many complaints involving FCRA violations like reporting debts after the statute of limitations expired or continuing collection efforts after receiving a cease-and-desist letter.

When a collector reports a debt you already paid or disputes an amount, the FCRA gives you the right to demand investigation, but collectors ignore these demands constantly because they face minimal penalties without legal action.

Identity Theft Demands Immediate Action

Identity theft situations demand even faster action. Fraudulent accounts opened in your name can take months to remove from your credit report, and the longer false information stays active, the more damage compounds. South Carolina gives you a two-year window from discovery to file suit for FCRA violations, but waiting costs you in lost opportunities for better loan rates, housing approvals, and employment offers. The sooner you contact an attorney after discovering an error that affects your financial opportunities, the sooner you can stop the damage and recover what you’ve lost.

What to Look for in an FCRA Attorney Serving South Carolina, Including Greenville, Columbia and Charleston

Seek Attorneys with Real FCRA Experience

Finding the right attorney matters more than most South Carolina residents realize because FCRA cases require specific knowledge that general practitioners simply do not possess. An attorney handling FCRA violations needs deep familiarity with credit reporting mechanics, the statutory damages framework, and how credit bureaus actually operate in practice. Look for firms with dedicated consumer protection practices, not attorneys who handle FCRA cases alongside divorce law or personal injury work. When you contact potential attorneys, ask directly how many FCRA cases they have handled in the past three years and what the average recovery was per case. This question separates attorneys with real experience from those who claim competence without results.

Understand Fee Structures and Payment Options

Fee structure determines whether you can actually afford representation, and this is where you need to be direct about what you can pay. Many FCRA attorneys work on contingency, meaning you pay nothing upfront and the firm recovers fees from the defendant if you win. This arrangement aligns the attorney’s financial incentive with your recovery. Verify that any firm you consider offers free initial consultations so you can discuss your case without financial commitment. Ask whether they charge hourly rates, contingency fees, or hybrid arrangements where you pay some costs upfront.

Verify Credentials and Check References

Request references from past clients and check online reviews on Google and the Better Business Bureau, but treat extremely positive reviews with the same skepticism as extremely negative ones. Confirm that the attorney holds a current South Carolina bar license and has no disciplinary history through the South Carolina Bar’s public records. Contact information matters too, so choose a firm with local presence in South Carolina rather than an out-of-state operation that handles cases remotely. A local firm understands South Carolina’s specific consumer protection landscape and maintains relationships with state courts where your case may be filed.

Final Thoughts

FCRA violations damage your finances and your future, but they are fixable when you take action. Credit report errors, fraudulent accounts, and debt collector harassment do not have to define your financial life. The Fair Credit Reporting Act gives you real legal tools to recover money and force corrections, but only if you use them within the statute of limitations window (two years from discovery or five years from the violation date).

The right FCRA attorney in South Carolina makes the difference between accepting false information on your report and recovering actual damages plus statutory penalties. An attorney with real consumer protection experience knows how credit bureaus operate, understands the leverage points in FCRA cases, and can negotiate or litigate on your behalf. They handle the complexity while you focus on rebuilding your financial stability, and contingency fee arrangements mean you pay nothing upfront.

Your credit report determines whether you qualify for housing, employment, loans, and financial opportunities. Inaccurate information should not block your path forward. We at Hays Cauley, P.C. help South Carolina residents with credit reporting, identity theft, and debt-related issues-contact us for a free consultation to discuss your case and learn what recovery looks like for your situation.