The Fair Credit Reporting Act affects how your business handles consumer information, and getting it wrong carries serious financial consequences. Non-compliance can result in penalties ranging from hundreds to millions of dollars, depending on the violation.

We at Hays Cauley, P.C. created this practical checklist to help you navigate FCRA compliance requirements step by step. This guide walks you through disclosure procedures, accuracy standards, and the systems you need to stay compliant.

What the Fair Credit Reporting Act Actually Covers

The Fair Credit Reporting Act, enacted in 1970, governs how consumer reporting agencies collect, use, and share credit information. The law applies to any business that accesses consumer reports to make decisions about employment, credit, insurance, housing, or other transactions. If you pull a background check before hiring someone, obtain a credit report before extending a loan, or use any third-party information to deny services, the FCRA applies to you.

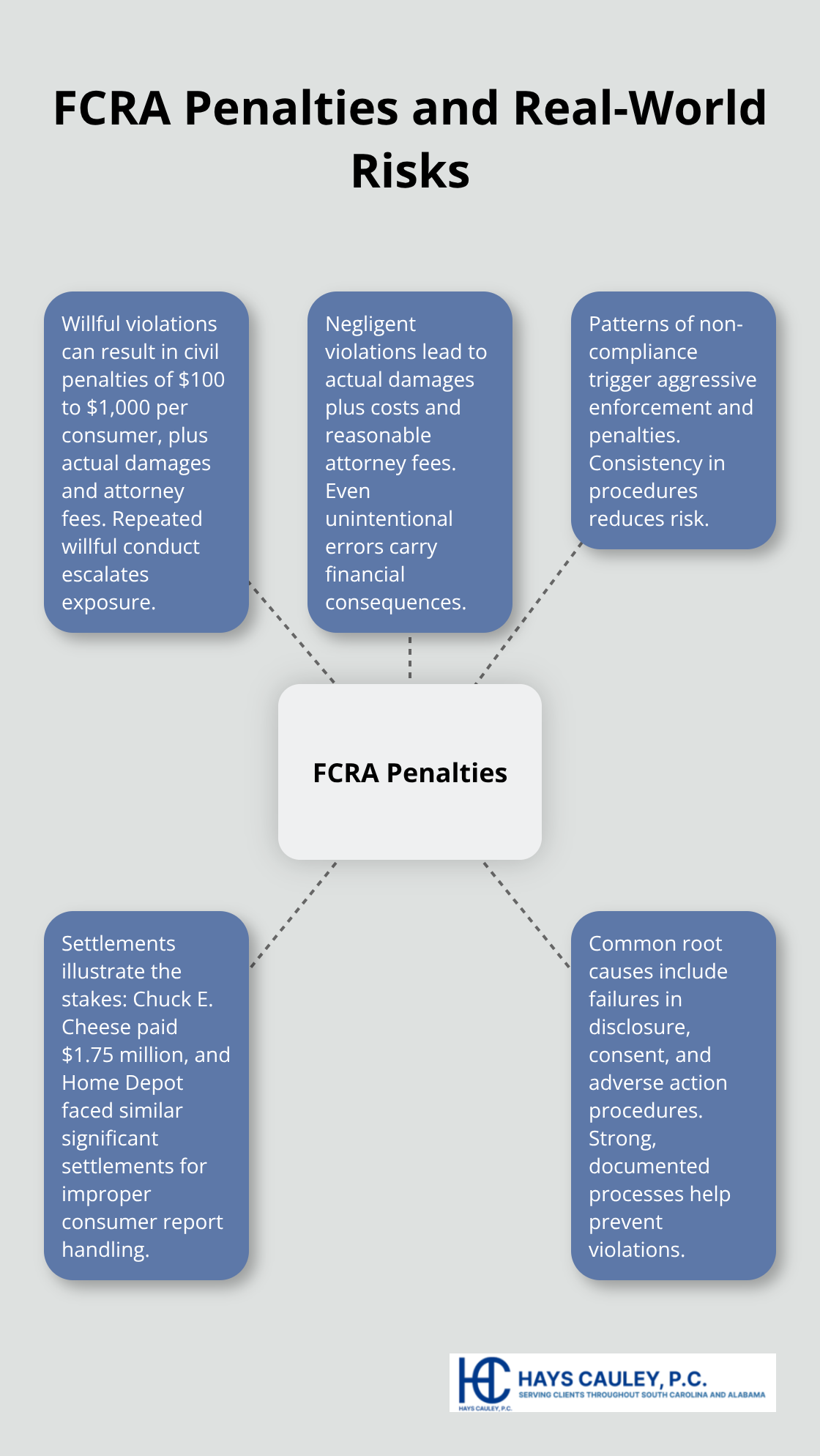

The scope extends far beyond credit bureaus. Employers, landlords, insurance companies, and government agencies all fall under FCRA obligations. Willful violations carry civil penalties of $100 to $1,000 per consumer, plus actual damages and attorney fees. Negligent violations result in actual damages plus costs and reasonable attorney fees. Patterns of non-compliance trigger the most aggressive penalties. Chuck E. Cheese settled an FCRA background screening case for $1.75 million, and Home Depot faced similar significant settlements for improper consumer report handling. These weren’t isolated mistakes-they reflected systematic failures in disclosure, consent, and adverse action procedures.

Where Compliance Breaks Down Most Often

Most violations stem from three areas: inadequate disclosure before obtaining reports, failure to provide proper adverse action notices, and poor record-keeping. Many employers skip the standalone written disclosure step and instead bury disclosure language in job applications or employment contracts. The FCRA requires a separate, conspicuous written document that informs applicants a background check will occur, what information will be collected, and the agency’s contact details. Combining this with other documents creates liability.

Second, when adverse employment decisions rest on consumer reports, you must provide a pre-adverse action notice giving the applicant at least five working days to dispute the report before final action. Then, if you proceed with the adverse decision, a final adverse action notice must follow, clearly stating the action taken and the reporting agency’s contact information. Third, documentation matters intensely. You need written consent forms signed by the applicant, copies of the reports used, records of the timeline for notices, and evidence the consumer had opportunity to dispute.

The FTC enforces FCRA rules and pursues civil penalties up to $2,500 per violation for patterns of non-compliance. Willful violations can lead to criminal penalties including fines and up to two years imprisonment for obtaining consumer information under false pretenses or unauthorized disclosure.

Creating Systems That Prevent Violations

The compliance solution remains straightforward if you treat it as a documented process. Start by reviewing your current background screening procedures and identify where disclosures happen, how consent gets collected, and whether you’re providing proper notices. Map the timeline from initial disclosure through final adverse action. Many businesses discover they’re missing the pre-adverse action step entirely or providing notices too late.

Next, separate your disclosure and authorization documents from the job application. Create a standalone disclosure form that explains the background check, its purpose, the agency involved, and consumer rights. Require the applicant’s written authorization on a separate form. Then establish a pre-adverse action workflow that automatically triggers when a report might lead to a hiring decision. Document the five-day dispute period and track whether the applicant responds.

If you move forward with an adverse decision, issue a final notice that includes the agency’s name, address, and phone number, making clear the agency did not make your hiring decision. Maintain copies of all notices, timelines, and applicant responses. Consider using a background screening provider that handles these procedural requirements, reducing your internal compliance burden. Regardless of your approach, a documented FCRA compliance checklist applied consistently across all hires eliminates most violations.

The investment in proper procedures costs far less than defending litigation or settling violations. With these systems in place, you’re ready to build the specific disclosure and consent procedures that form the foundation of your compliance program.

Building Your FCRA Compliance Checklist

Disclosure and Consent Procedures

Your disclosure and consent procedures form the legal foundation of your entire compliance program, and they must be airtight. The FCRA requires a separate, standalone written disclosure before you obtain any consumer report for employment decisions. This document cannot be buried in an employment application or employee handbook. It must be a distinct form that clearly states a consumer report will be obtained, explains what information will be collected, identifies the consumer reporting agency by name and contact information, and describes the consumer’s rights.

After disclosure comes written authorization on a separate form signed by the applicant. The authorization must explicitly state the purpose and scope of the background check. Many businesses fail at this stage by combining disclosure and authorization into a single document or by treating authorization as a checkbox within the application. Courts and the FTC view these shortcuts as violations. Keep these documents separate.

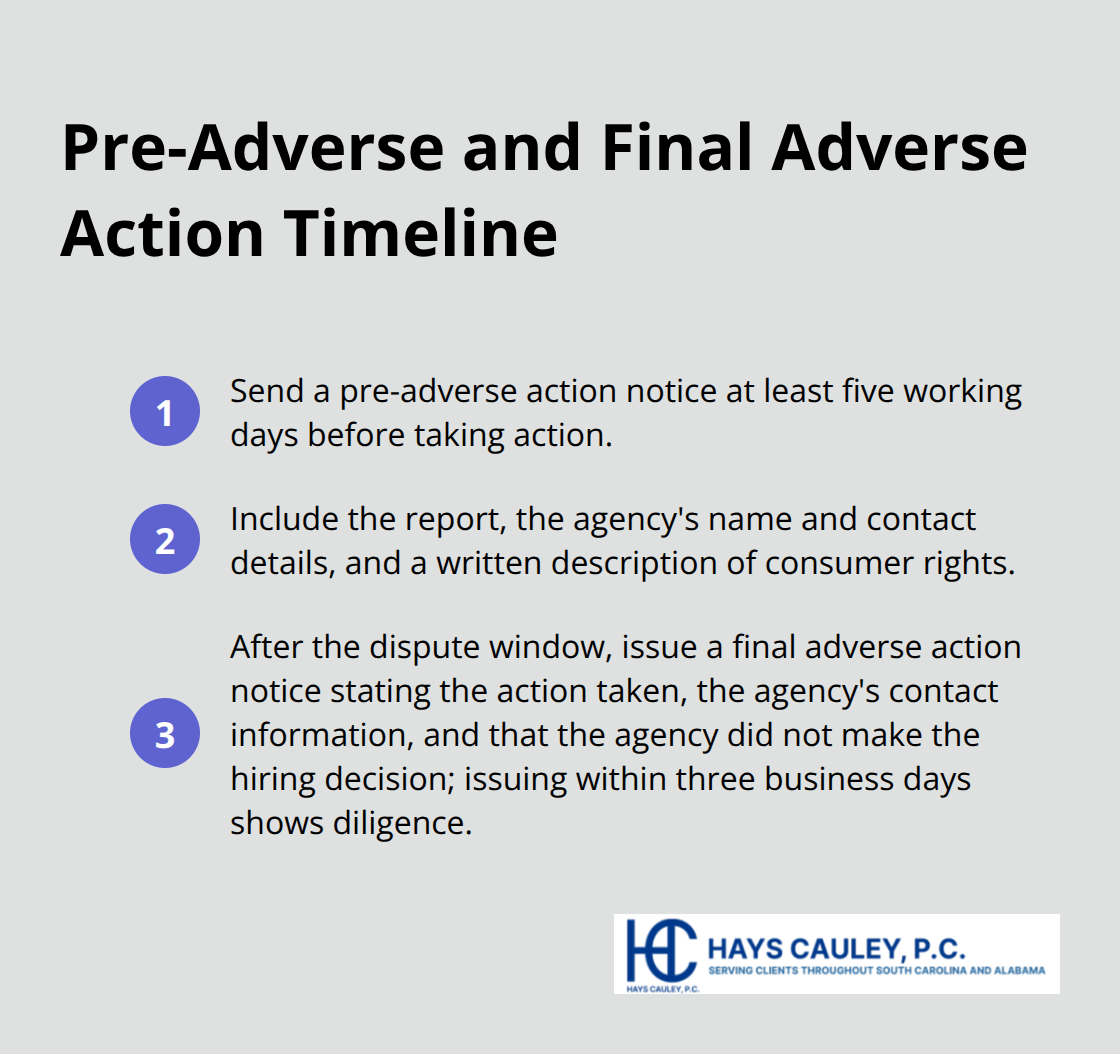

When adverse action might result from the report, you must provide a pre-adverse action notice at least five working days before taking the action. This notice includes the intended action, a copy of the report, the agency’s name and contact details, and a written description of consumer rights. Applicants need genuine time to dispute inaccurate information.

If you proceed with the adverse decision after the dispute period, issue a final adverse action notice stating the action taken, the agency’s contact information, and a statement that the agency did not make your hiring decision. The FCRA does not specify a strict timing window for the final notice, but issuing it within three business days of the decision demonstrates diligence.

Accuracy and Dispute Resolution Processes

Your accuracy and dispute resolution processes must be documented and consistently applied. When a consumer disputes information in a report, you have 30 days to reinvestigate, verify accuracy, and update the consumer on status. This is not optional. The FTC views reinvestigation delays as negligence, exposing you to actual damages plus attorney fees. Establish a written procedure that assigns responsibility for receiving disputes, initiating reinvestigation with the reporting agency, documenting the investigation timeline, and notifying the consumer of results.

Record-Keeping and Documentation Standards

Record-keeping requirements are equally strict. Maintain signed disclosure forms, authorization documents, copies of the reports used, written notes on the timeline for each notice, proof that notices were delivered, and records of any consumer disputes or responses. These documents protect you during audits or litigation by demonstrating you followed proper procedures. The FTC and state attorneys general conduct FCRA audits, and inadequate documentation signals negligence even if your procedures were technically correct.

A compliance checklist applied consistently across all hiring decisions eliminates confusion and gaps. Document your checklist, assign an owner responsible for updates, and review it at least annually as regulations evolve. The 2025 amendments to the FCRA introduced new restrictions on prescreening for residential mortgage transactions, effective 180 days after September 5, 2025. These changes limit which entities can furnish mortgage-related reports without consumer authorization. If your business touches mortgage lending or prescreening, update your procedures immediately.

The cost of implementing proper disclosure, authorization, and documentation procedures is minimal compared to defending an FCRA violation or settling a claim. A single documented process applied consistently reduces your litigation risk and demonstrates good faith compliance to regulators. With these foundational procedures in place, you’re ready to train your team on how to execute them correctly and establish the monitoring systems that catch gaps before they become violations.

Making FCRA Compliance Stick Across Your Business

Training Your Team on FCRA Rules

FCRA compliance fails when procedures exist on paper but vanish in practice. Your team needs hands-on training that moves beyond general awareness into specific execution. Start with your hiring managers and HR staff who pull background checks. They must understand that obtaining a consumer report without proper disclosure and written consent exposes your company to liability.

Run quarterly training sessions covering the exact documents they must use, the timeline they must follow, and the consequences of shortcuts. Include real scenarios: what happens if a hiring manager requests a background check without authorization, what the pre-adverse action notice must contain, and how to respond when an applicant disputes information in a report. The FTC pursues cases against companies where training was absent or generic.

Make training mandatory and documented. Track who attended, what was covered, and when refresher training occurred. When new regulations like the 2025 mortgage prescreening restrictions take effect, update your training immediately rather than waiting for violations to surface.

Regular Audits and Monitoring Systems

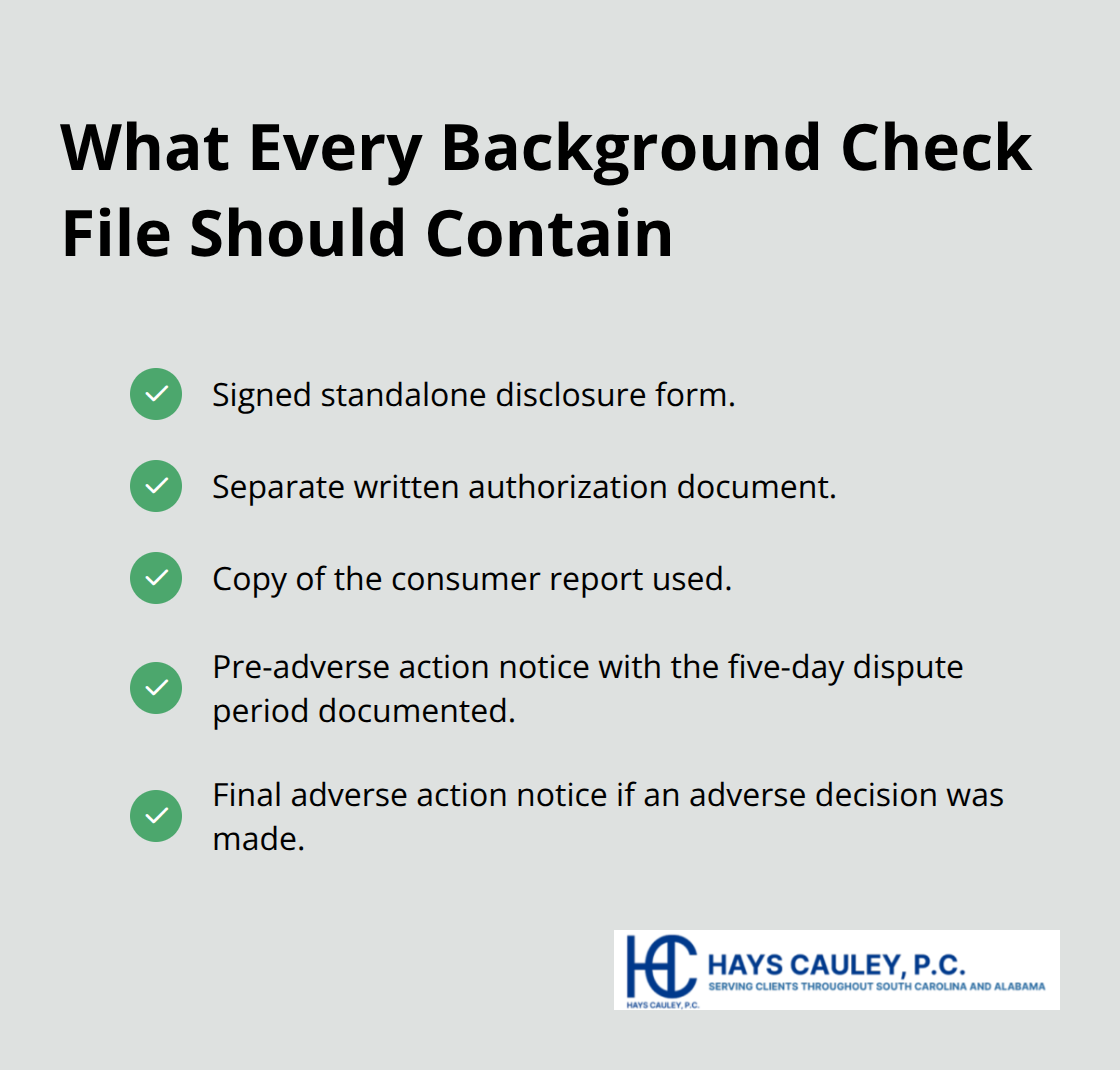

Audits and monitoring systems catch compliance gaps before regulators do. Conduct internal audits every six months by pulling a sample of background check files and verifying that each one includes a signed disclosure form, a separate authorization document, a copy of the report used, a pre-adverse action notice with the five-day dispute period documented, and a final adverse action notice if an adverse decision was made.

Many companies discover they issue notices late, combine forms inappropriately, or fail to document the dispute period. Assign someone to own this audit process and report findings to leadership quarterly. This ownership prevents compliance from slipping through organizational cracks.

Working with Third-Party Vendors and Partners

Third-party vendors and background screening providers introduce additional compliance risk. When you use an outside provider, verify they understand your disclosure and consent procedures and that they deliver notices on your timeline. Request documentation showing how they handle reinvestigations when consumers dispute information within the 30-day window.

Ask whether they maintain records proving they placed security freezes within the required timeframe if a consumer requests one. Some providers automate compliance better than others. Evaluate whether they can integrate with your hiring system, automatically trigger the pre-adverse action notice at the right moment, and maintain audit trails proving compliance (these capabilities reduce manual errors significantly).

Establish a written agreement with vendors that requires them to comply with all FCRA provisions and hold them accountable for their performance. If a vendor makes mistakes, your company still faces liability.

Final Thoughts

FCRA compliance requires three core commitments: documented procedures, consistent execution, and regular monitoring. Your disclosure and consent forms must remain separate and signed. Your pre-adverse action and final adverse action notices must follow the proper timeline. Your records must prove you followed these steps, or violations become inevitable.

The practical next step is to audit your current background screening process by pulling five recent hiring files and checking whether each contains a standalone disclosure form, a separate authorization document, a copy of the report used, documentation of the pre-adverse action notice with the five-day dispute period, and a final adverse action notice if an adverse decision occurred. Most companies discover gaps immediately and can then assign responsibility for fixing each gap and set a deadline for implementation. Establish quarterly audits to catch new gaps before they accumulate, train your hiring managers and HR staff on the exact documents they must use, and update your training whenever regulations change (as they did with the 2025 mortgage prescreening restrictions).

FCRA compliance help becomes straightforward when you treat it as a repeatable process rather than a one-time project. The investment in proper procedures costs far less than defending litigation or settling violations. We at Hays Cauley, P.C. work with businesses to strengthen their compliance programs and protect themselves from costly violations-contact us to learn how we can support your efforts.