A credit report error can tank your credit score and cost you thousands in higher interest rates. These mistakes happen more often than you’d think-from identity theft to simple data entry errors by creditors and bureaus.

We at Hays Cauley, P.C. help people fight back against these errors and recover damages. A credit report errors attorney can guide you through your legal options and hold the responsible parties accountable.

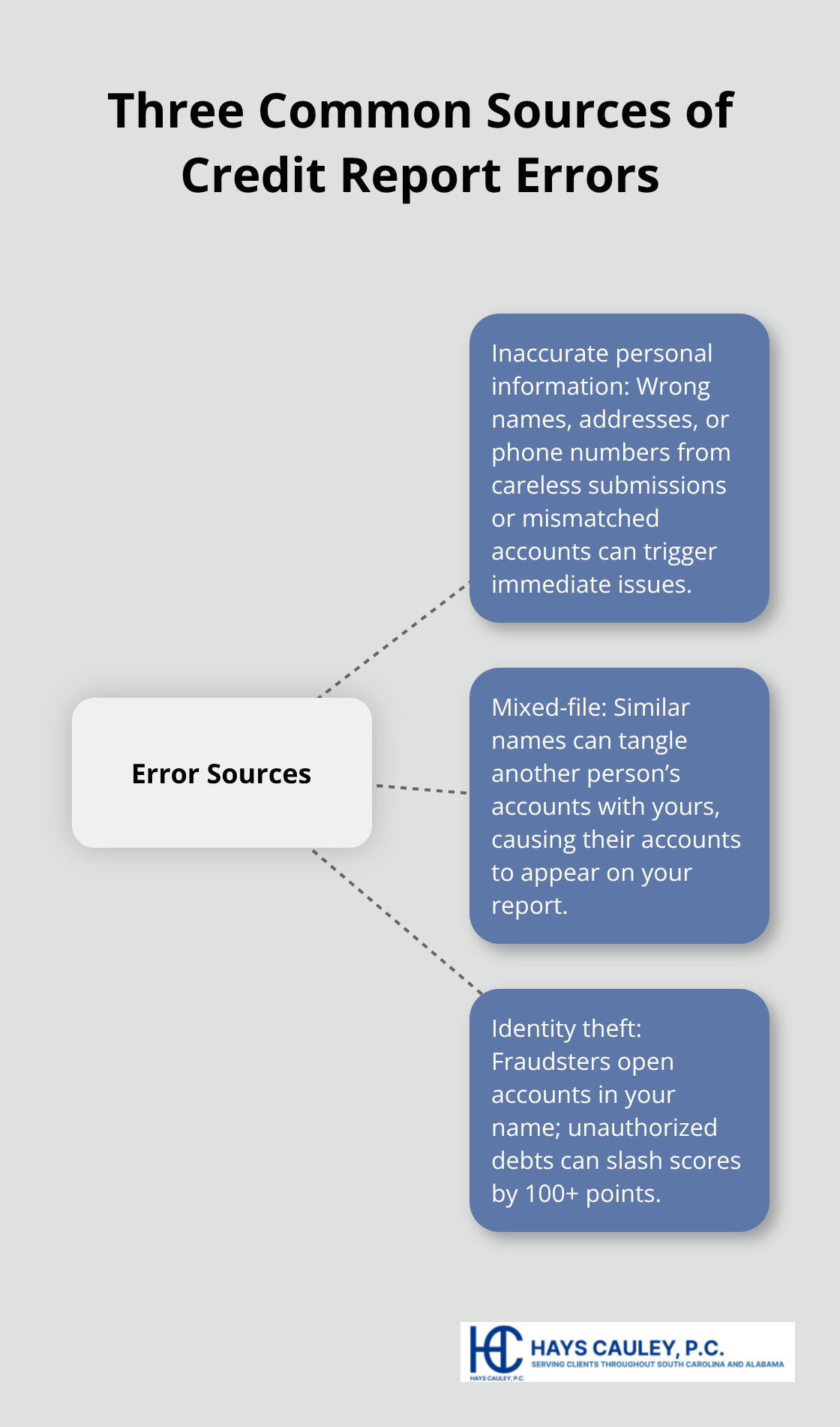

How Credit Report Errors Actually Start

Credit report errors stem from three main sources, and understanding where mistakes originate helps you identify what went wrong on your file. Inaccurate personal information creates immediate problems-wrong names, addresses, or phone numbers land on your report when creditors submit data carelessly or when bureaus fail to match accounts correctly. Mixed-file situations occur when someone with a similar name gets their accounts tangled with yours, a problem that affects roughly one in five consumers according to identity theft reports. Identity theft represents the most damaging scenario, where fraudsters open accounts in your name and those unauthorized debts appear on your credit file, potentially lowering your score by 100 points or more (depending on the account size and activity level).

Payment History Gets Reported Wrong

Payment reporting mistakes happen constantly because creditors and debt collectors frequently submit inaccurate information to the three major bureaus. An account marked as 30 days late when you paid on time, a closed account reported as open, or a settled debt still showing as unpaid-these data entry errors cost you real money in higher interest rates and loan denials. The Fair Credit Reporting Act requires furnishers to verify information accuracy, yet many ignore this obligation entirely. Duplicate debts listed under slightly different names or accounts reported with incorrect balances are equally common mistakes that demand immediate action.

Where Errors Hide on Your Report

Closed accounts reported as active, wrong credit limits that artificially inflate your debt-to-income ratio, and incorrect dates on when accounts opened or payments were missed all damage your creditworthiness. Accounts belonging to another person appearing on your report due to similar identifying information create serious obstacles when you try to qualify for mortgages or employment opportunities. The problem intensifies when you attempt to dispute these errors and bureaus dismiss your claim as frivolous without proper investigation-a violation of the Fair Credit Reporting Act that gives you grounds for legal action.

Why Bureaus Resist Corrections

Credit reporting agencies often reject disputes without conducting thorough investigations, treating legitimate claims as nuisance complaints rather than legitimate concerns. This resistance to correction means you face a choice: accept the damage to your credit score or pursue legal remedies. Understanding how these errors originate and where they hide on your report sets the foundation for taking action. The next step involves knowing your legal rights and what protections the law actually provides when you face these inaccurate entries.

Your Legal Rights When Facing Credit Report Errors – Serving South Carolina, including Greenville, Columbia and Charleston

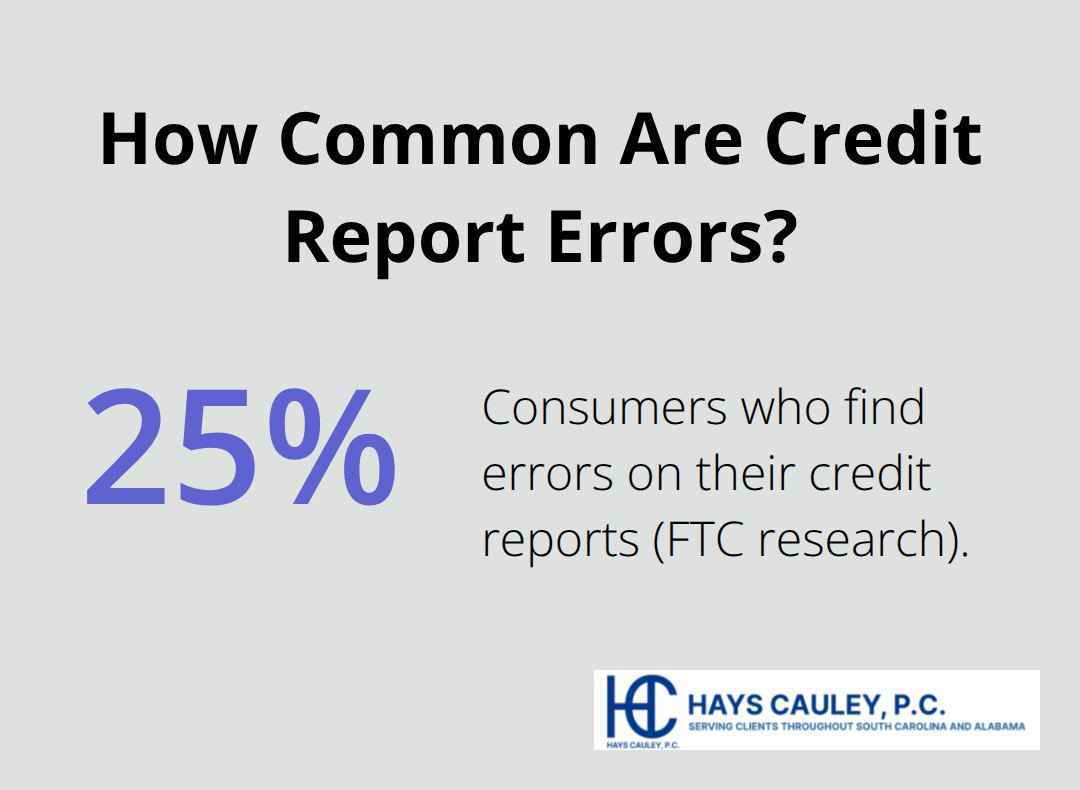

The Fair Credit Reporting Act gives you concrete rights that credit bureaus must follow, and understanding these protections is your foundation for fighting back. Under the FCRA, credit reporting agencies must maintain reasonable procedures to ensure the information they report is accurate, and furnishers-the creditors and debt collectors supplying that data-must verify information when you dispute it. This means when you file a dispute, the bureau has exactly 30 days to investigate and determine whether the information is accurate or not. If the furnisher cannot verify the information, it must be deleted from your report. The FCRA also requires that if an adverse action is taken against you based on a credit report, the company must notify you. This notification gives you proof of what information harmed your chances of getting a loan, job, or housing. The Dodd-Frank Act transferred most rulemaking authority to the Consumer Financial Protection Bureau, which now oversees credit reporting standards alongside the FTC’s enforcement role. These laws exist because roughly 25 percent of consumers find errors on their credit reports that could impact their scores, according to FTC research.

How to File a Written Dispute

You must file a written dispute with the credit reporting agency-do not rely on phone calls or online portals alone without documentation. Send your dispute letter by certified mail with return receipt to Equifax, Experian, or TransUnion, including your contact information, the account number of the disputed item, a clear explanation of what is wrong, and copies of supporting documents like bank statements or payment histories. Include a copy of the portion of your credit report showing the error, highlighted or circled. The furnisher then has 30 days to investigate and either verify the information or correct it. Tracking everything in writing matters because many bureaus deny legitimate disputes outright.

What Happens When Bureaus Refuse to Correct Errors

If the furnisher concludes the information is accurate but you disagree, you have the right to add a dispute statement to your credit file that will appear to anyone who requests your report in the future. This statement does not remove the error, but it documents your objection. If the bureau fails to respond within 30 days or dismisses your dispute as frivolous without proper investigation, you have grounds for legal action. Bureaus often ignore legitimate disputes entirely, which is why legal representation becomes necessary when they refuse to comply with the law.

Understanding Statute of Limitations on Reporting Errors

Statute of limitations rules protect you for a limited time. Negative items like late payments, charge-offs, and collections can be reported for seven years from the date of first delinquency, while bankruptcies remain for ten years. This timeline matters because errors become harder to challenge once items age, yet bureaus continue reporting inaccurate information well into that seven-year window. If a furnisher provides wrong information and refuses to correct it after your dispute, or if a bureau ignores your dispute entirely, you need legal representation to compel action.

What Damages You Can Recover

You may be entitled to actual damages from financial harm-denied loans, higher interest rates, lost job opportunities-plus statutory damages up to one thousand dollars per violation, regardless of whether you suffered financial loss. If a bureau’s negligence caused the error, you have a claim. If they acted recklessly by ignoring your dispute, the damages increase. The CFPB complaint process is free but slow; legal action moves faster and holds companies accountable when they refuse to comply. When bureaus and creditors violate your rights under the FCRA, a consumer protection law firm can help you recover what you lost and hold them responsible for their actions.

When DIY Disputes Fail, You Need Legal Firepower

Credit bureaus count on you giving up. They know most people file one dispute, receive rejection, and accept the damage to their credit score rather than fight back. The Fair Credit Reporting Act theoretically protects you, but enforcement falls on your shoulders unless you hire an attorney. When you dispute an error yourself, bureaus often respond with form letters claiming they investigated and found nothing wrong, even when they never contacted the furnisher or reviewed your supporting documents.

Why Bureaus Ignore Your Disputes

The FTC received over 4,500 complaints about credit reporting agencies in 2024 alone, with the most common complaint being that bureaus failed to properly investigate disputes. These rejections happen because credit reporting agencies face minimal consequences for ignoring your claims. An attorney changes that equation immediately. The moment a law firm sends a formal demand letter, credit bureaus take your case seriously because they know litigation costs them far more than correcting the error. A consumer protection law firm sends legal notices that force bureaus to conduct actual investigations instead of dismissing your dispute as routine.

How Furnishers Respond to Attorney Involvement

Furnishers also respond differently to attorney involvement. Debt collectors and creditors who ignore your written disputes suddenly prioritize verification requests from lawyers. Many furnishers deliberately provide inaccurate information because individual consumers rarely sue over it. When a law firm demands verification of a debt, furnishers must produce actual documentation proving the account belongs to you and the balance is correct. If they cannot verify it within 30 days, the law requires deletion from your report. Most cannot produce this documentation because they rely on outdated or incomplete records sold in bulk. An attorney handling your case knows exactly what documentation to demand and how to challenge incomplete responses.

Quantifying Your Financial Harm

Building a compensation claim requires documenting the specific financial harm caused by the error. If a credit report error caused a mortgage lender to deny your application, you need the lender’s written denial and the interest rate difference between what you would have qualified for and what you eventually paid. If identity theft accounts destroyed your credit score, you need proof of the fraudulent accounts and documentation of higher interest rates you paid on legitimate accounts. A legal team knows how to quantify these damages and prove causation. The FCRA allows statutory damages of up to one thousand dollars per violation, meaning multiple errors on your report create multiple damage claims. Courts have awarded consumers tens of thousands of dollars when bureaus violated their rights. A consumer protection law firm gathers this documentation systematically and presents it to bureaus and furnishers as leverage for settlement. Most cases settle without trial because companies would rather pay damages than face discovery and trial costs.

Why You Cannot Negotiate Alone

Attempting to negotiate with credit bureaus alone puts you at a disadvantage because you lack the legal knowledge to identify all violations and the credibility that comes with attorney representation. Bureaus employ teams of lawyers to defend against claims. Matching that firepower yourself is impossible.

Taking Action Now

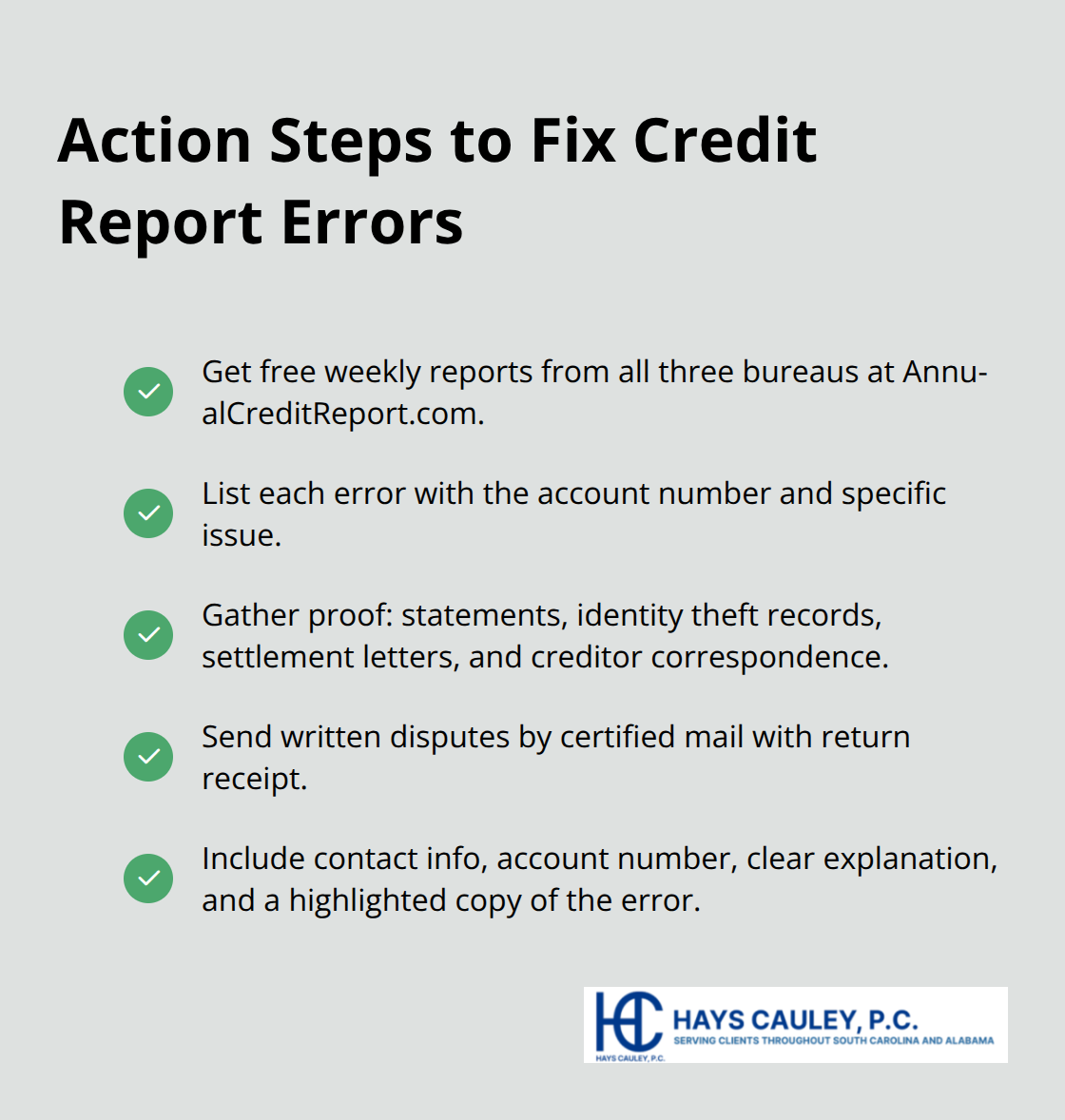

Start by obtaining your credit reports from all three bureaus at AnnualCreditReport.com, which provides free weekly access, then review each report carefully for errors including wrong personal information, accounts you never opened, payment history mistakes, duplicate debts, and incorrect balances or credit limits. Write down every error with the account number and the specific problem, then gather supporting documents before filing any dispute-bank statements showing on-time payments, proof of identity theft, settlement letters, or correspondence with creditors (these documents strengthen your case significantly). File written disputes with each bureau reporting the error, sending them by certified mail with return receipt, and include your contact information, the account number, a clear explanation of what is wrong, copies of your supporting documents, and a highlighted copy of the error from your credit report.

The bureau must investigate within 30 days and forward your dispute to the furnisher, so track everything in writing because phone calls leave no record. If the bureau rejects your dispute or fails to respond within 30 days, or if the furnisher cannot verify the information but the bureau refuses to delete it, you have reached the point where legal representation becomes necessary. A credit report errors attorney understands FCRA violations that you might miss and knows how to demand proper investigation from bureaus and furnishers.

We at Hays Cauley, P.C. help consumers throughout South Carolina recover damages from credit reporting violations. Contact us to discuss your situation and learn what compensation you may be entitled to recover.