Inaccurate information on your credit report can damage your financial future. The Fair Credit Reporting Act gives you the right to challenge errors, and understanding the FCRA reinvestigation process is your first step toward fixing them.

We at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia, and Charleston, navigate credit reporting disputes. This guide walks you through requesting a proper reinvestigation and protecting your rights.

What the Fair Credit Reporting Act Actually Does for You

The FCRA Gives You Real Legal Power

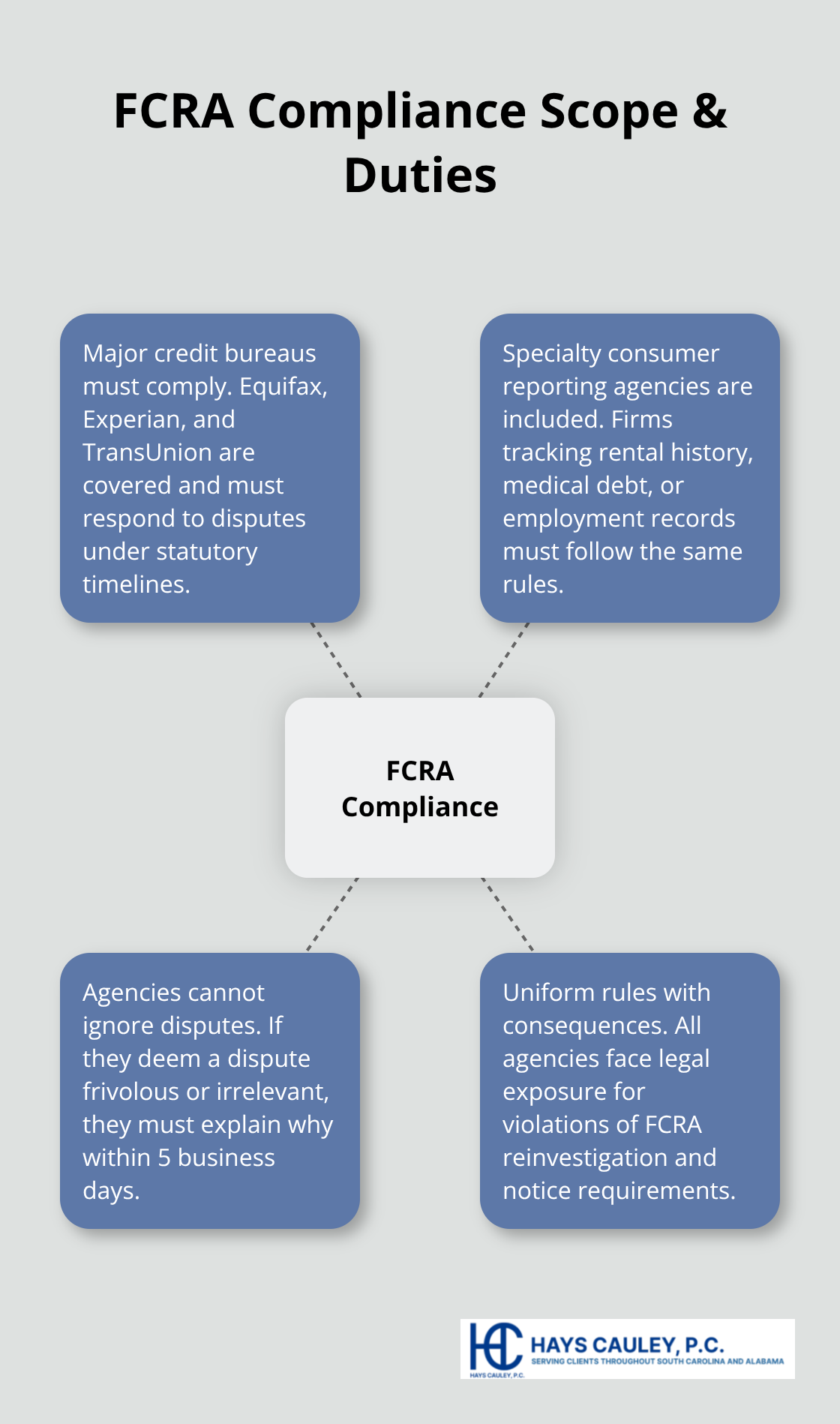

The Fair Credit Reporting Act is not theoretical-it’s a federal law with real teeth that gives you the power to challenge errors on your credit report. Under 15 U.S.C. § 1681i, credit reporting agencies must reinvestigate disputed information at no cost to you within 30 days of receiving your dispute. This timeline can extend to 45 days if you provide additional relevant information during the process. This is not optional for the agencies; it’s mandatory. The FCRA also requires credit reporting agencies to delete information that turns out to be inaccurate or unverifiable, and they must notify you in writing within 5 business days after the reinvestigation completes.

What Happens When Agencies Ignore You

If a credit reporting agency determines your dispute is frivolous or irrelevant, they must tell you why within 5 business days-they cannot simply ignore you. The law applies to the three major credit reporting agencies (Equifax, Experian, and TransUnion) as well as specialty consumer reporting agencies that track rental history, medical debt, or employment records. Each agency must follow the same rules, and violations carry real consequences.

Your Right to Challenge Information Sources

Your right to dispute goes beyond just credit reports. You can challenge information furnished by banks, credit card companies, landlords, collection agencies, and any other entity that supplies data to credit reporting agencies. When you file a dispute, the furnisher (the company that reported the information) has a legal obligation to investigate your claim and either correct or delete the error.

Protection Against Repeated Errors

If a furnisher reinserts information that was previously deleted, they must certify in writing that the information is accurate. The credit reporting agency must notify you within 5 business days with the furnisher’s name, address, and contact information. The FCRA also requires credit reporting agencies to maintain procedures that prevent deleted information from reappearing in your file. This means errors should not haunt you indefinitely.

What Happens When Reinvestigation Doesn’t Resolve Your Dispute

If the reinvestigation does not resolve your dispute, you have the right to file a brief statement (up to 100 words) describing the nature of the dispute, and this statement must be included in any subsequent consumer reports. You can also file a complaint with the Consumer Financial Protection Bureau if a credit reporting agency violates the FCRA. Understanding these protections sets the stage for taking action-and the first step is knowing exactly what error you need to challenge and what documentation you’ll need to support your claim.

How to File Your FCRA Reinvestigation Request, Serving South Carolina, Including Greenville, Columbia, and Charleston

Collect Your Evidence First

Start with your credit reports from all three agencies-Equifax, Experian, and TransUnion. Circle or highlight the disputed item on each report. Then assemble your documentation: payment receipts, bank statements, emails, correspondence with the creditor, or any other proof that shows the information is wrong or incomplete. The FTC recommends including copies (not originals) of supporting documents with short descriptions attached. This documentation forms your foundation for the dispute letter. Without it, the credit reporting agency and furnisher have little reason to investigate thoroughly.

Write and Send Your Dispute Letters

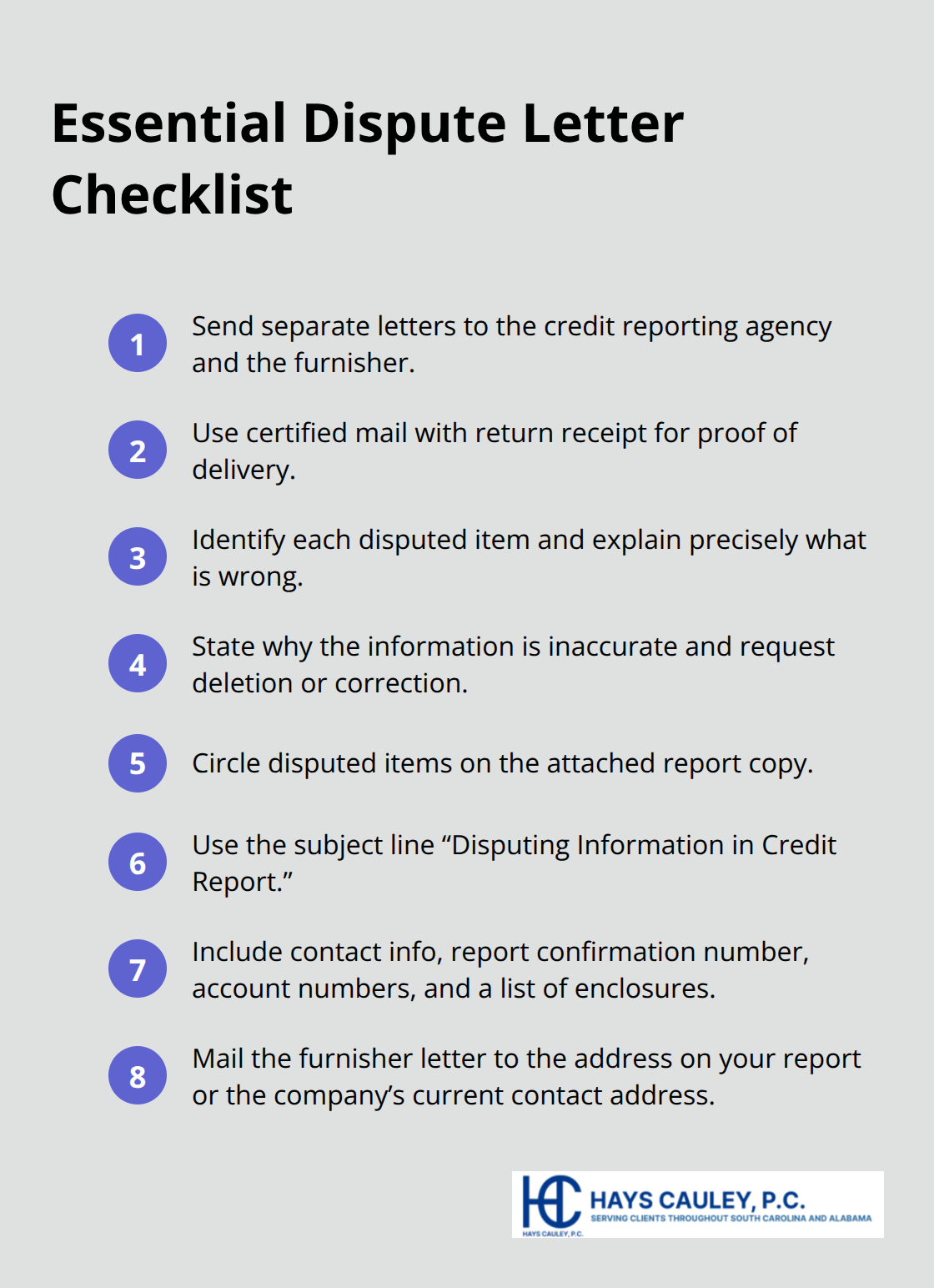

Send your dispute letter directly to the credit reporting agency and separately to the furnisher (the company that reported the information). Use certified mail with return receipt requested so you have proof of delivery. Your letter must identify each disputed item, explain specifically what is inaccurate or incomplete, state why the information is wrong, and request deletion or correction.

Circle the disputed items on your attached credit report copy to make your challenge crystal clear. According to the FTC, use the subject line “Disputing Information in Credit Report” and include your contact information, the report confirmation number if available, each disputed account number, and a list of all enclosed documents. Send the furnisher letter to the address shown on your credit report or the company’s current contact information.

Understand the 30-Day Timeline

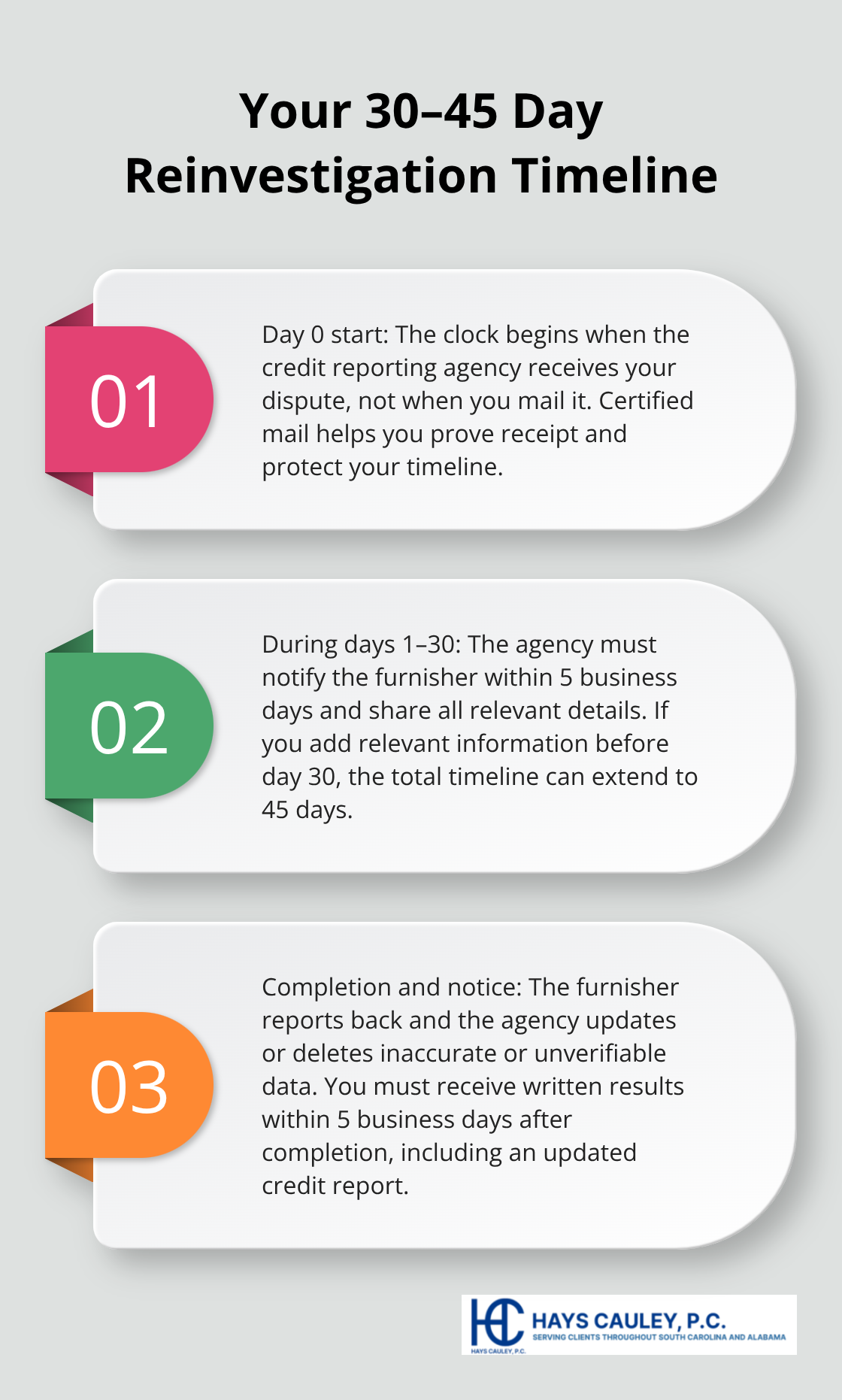

The 30-day reinvestigation clock starts the moment the credit reporting agency receives your dispute, not when you mail it-which is why certified mail matters. During those 30 days, the agency must notify the furnisher within 5 business days and provide all relevant dispute information. If you submit additional relevant information before day 30, the timeline extends to 45 days total (but only if that new information actually affects the investigation).

The furnisher investigates your claim and reports back to the credit reporting agency, which then updates or deletes the information if it turns out to be inaccurate or unverifiable. The credit reporting agency must send you written notice of the results within 5 business days after completion, including an updated copy of your credit report.

Track Everything During Reinvestigation

Do not wait passively during these 30 to 45 days. Keep detailed records of every communication, document the dates you mailed your letters, save the return receipts, and note any phone calls or emails. If the agency determines your dispute is frivolous or irrelevant, they must tell you why within 5 business days-and you have the right to challenge that determination. Request the furnisher’s contact details from the credit reporting agency so you can verify whether corrections were actually made and whether the information might be reinserted later. This documentation protects you if disputes arise later or if you need to escalate your case.

What Happens When Reinvestigation Completes

Once the reinvestigation concludes, the credit reporting agency sends you written results within 5 business days. You receive an updated copy of your credit report showing any corrections or deletions. If the furnisher reinserts information that was previously deleted, they must certify in writing that the information is accurate, and the agency must notify you within 5 business days with the furnisher’s name, address, and contact information. If the reinvestigation does not resolve your dispute, you have additional options available to you.

Common Mistakes That Derail Your Reinvestigation Request, Serving South Carolina, Including Greenville, Columbia, and Charleston

Vague Disputes Give Furnishers an Easy Out

Most reinvestigations fail because people submit disputes that lack the specificity credit reporting agencies and furnishers need to actually investigate. Vague complaints like “this account is wrong” give the furnisher an excuse to respond that they verified the information without doing real work. The FTC’s guidance on disputing emphasizes that you must identify each disputed item, present the facts, explain exactly why it’s inaccurate, and request specific removal or correction. If your dispute letter says only “I didn’t owe this debt,” the furnisher will likely tell the credit reporting agency they verified it and the item stays on your report. Instead, write “I paid this account in full on March 15, 2023, as shown by the bank statement enclosed, yet your records show it as unpaid.” That specificity forces actual investigation.

Missing Documentation Weakens Your Case

Without documentation attached to your letter-bank statements, payment receipts, correspondence with the creditor, proof of identity theft-the furnisher has minimal incentive to investigate thoroughly. The FTC recommends including copies (not originals) of supporting documents with short descriptions attached to your dispute. Certified mail with return receipt is non-negotiable because it proves delivery to the credit reporting agency and furnisher. If you mail your dispute via regular mail and it never arrives, the 30-day clock never starts and your rights disappear. The FTC recommends certified mail as the standard method precisely because disputes sent other ways create disputes about whether they were received at all.

Poor Record-Keeping Costs You Later

Keep copies of every page you send: your letter, the credit report with items circled, all supporting documents, and the certified mail receipt showing delivery confirmation. Many people send disputes, forget what they included, and later cannot prove what they claimed or what evidence they provided. This documentation becomes critical if you need to escalate your case or file a complaint with the Consumer Financial Protection Bureau. Without records, you have no proof of what you submitted or when you submitted it.

Missing Follow-Up Deadlines Kills Your Momentum

The 30-day reinvestigation timeline moves fast, and missing follow-up deadlines costs you real leverage. Once you receive the reinvestigation results within 5 business days after completion, you have limited time to act if the dispute was not resolved. If the furnisher reinserted information that was previously deleted, the credit reporting agency must notify you within 5 business days with the furnisher’s contact details. Waiting weeks to follow up means you lose momentum and the reinserted information stays on your report longer.

Acting Quickly After Results Arrive Matters

Request the furnisher’s contact information immediately after receiving the reinvestigation results and verify that corrections were actually made on your updated credit report. If corrections are missing or inaccurate items reappeared, contact the furnisher in writing again with your previous documentation and the updated report showing the problem. The 45-day extended timeline only applies if you submit additional relevant information during the initial 30 days, so timing matters enormously. If you wait until day 45 to add new evidence, you may have already missed the window for extension. Document the exact dates you received notices and results-do not rely on memory. If the reinvestigation fails to resolve your dispute, you have the right to file a brief statement up to 100 words describing the dispute, but this statement must be filed with the credit reporting agency, not just mentioned in a follow-up email. Sending written documentation through certified mail protects you if you later need to prove you took action within required timeframes. Many people lose reinvestigation disputes because they wait passively for results rather than actively tracking progress and responding within the narrow windows the law provides.

What to Do When Reinvestigation Fails

A failed reinvestigation does not mean your options end. Under 15 U.S.C. § 1681i(b), you have the right to submit a brief written statement (up to 100 words) that describes the nature of your dispute, and you must send this statement by certified mail to the credit reporting agency. The agency must include your dispute statement in any subsequent consumer reports about you, and they must provide it to anyone who receives your report for employment purposes within the next two years or for other purposes within six months.

If the credit reporting agency violated the FCRA reinvestigation process, file a complaint with the Consumer Financial Protection Bureau. Document exactly what went wrong: whether the agency missed the 30-day deadline, failed to notify you of results within 5 business days, or refused to investigate your dispute. Include copies of your original dispute letter, the agency’s response, your documentation, and any correspondence that shows the violation.

When reinvestigation fails and the CFPB complaint process moves slowly, you need someone who understands credit reporting law. We at Hays Cauley, P.C. help South Carolina residents, including those in Greenville, Columbia, and Charleston, fight inaccurate credit reports and hold credit reporting agencies accountable.