Your credit report affects your ability to borrow money, rent an apartment, and sometimes even get hired for a job. The Fair Credit Reporting Act gives you specific rights to protect yourself from errors and unfair practices.

At Hays Cauley, P.C., we help South Carolina consumers understand their SC FCRA obligations and fight back when those rights are violated. This guide walks you through what the law requires and what you can do if someone breaks the rules.

Understanding How Your Credit Report Works

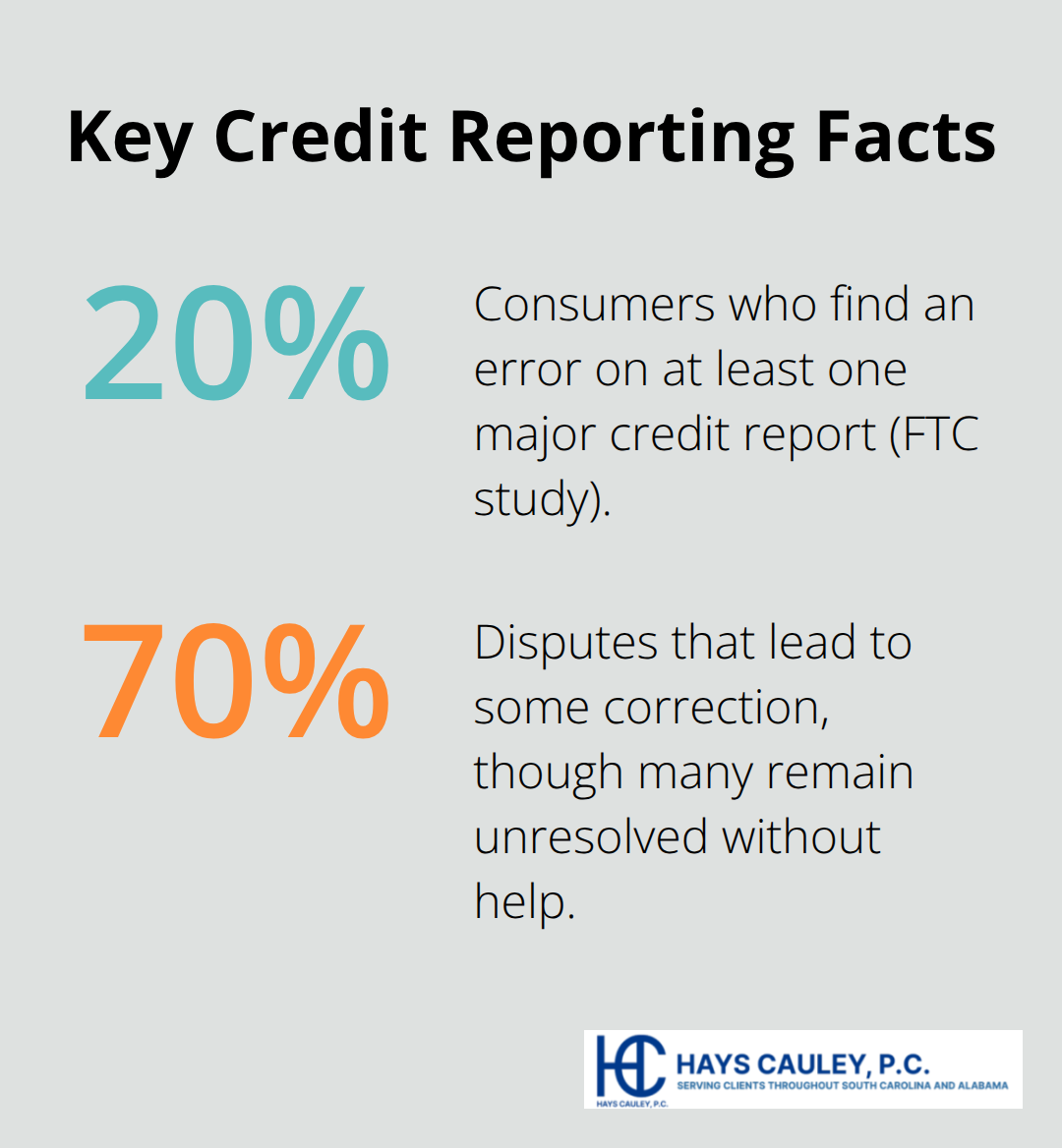

Credit reporting agencies collect information about you from creditors, lenders, and other data furnishers every single day. When you apply for a credit card, take out a loan, or pay your utility bills, that information flows to Equifax, Experian, and TransUnion. These three major bureaus compile your financial history into a report that lenders, employers, and landlords use to make decisions about you. The FCRA requires these agencies to maintain reasonable procedures to ensure the information they collect stays accurate and current. A Federal Trade Commission study found that about 20% of consumers find an error on at least one major credit report, which means inaccuracies happen far more often than most people realize.

Access Your Report Before Problems Arise

Getting your free credit reports costs nothing and takes minimal effort. You can obtain one free report from each of the three major bureaus every 12 months through AnnualCreditReport.com. The FTC recommends rotating your requests every four months so you spot errors sooner rather than waiting until an error damages your credit score. When you review your reports, look for unfamiliar accounts, incorrect personal details, and negative items that should have aged off after seven years. Payment history, account balances, and credit limits should all match your own records. If you notice something wrong, document it immediately with bank statements, receipts, or creditor communications before the details fade from memory.

Challenge Inaccurate Information Directly

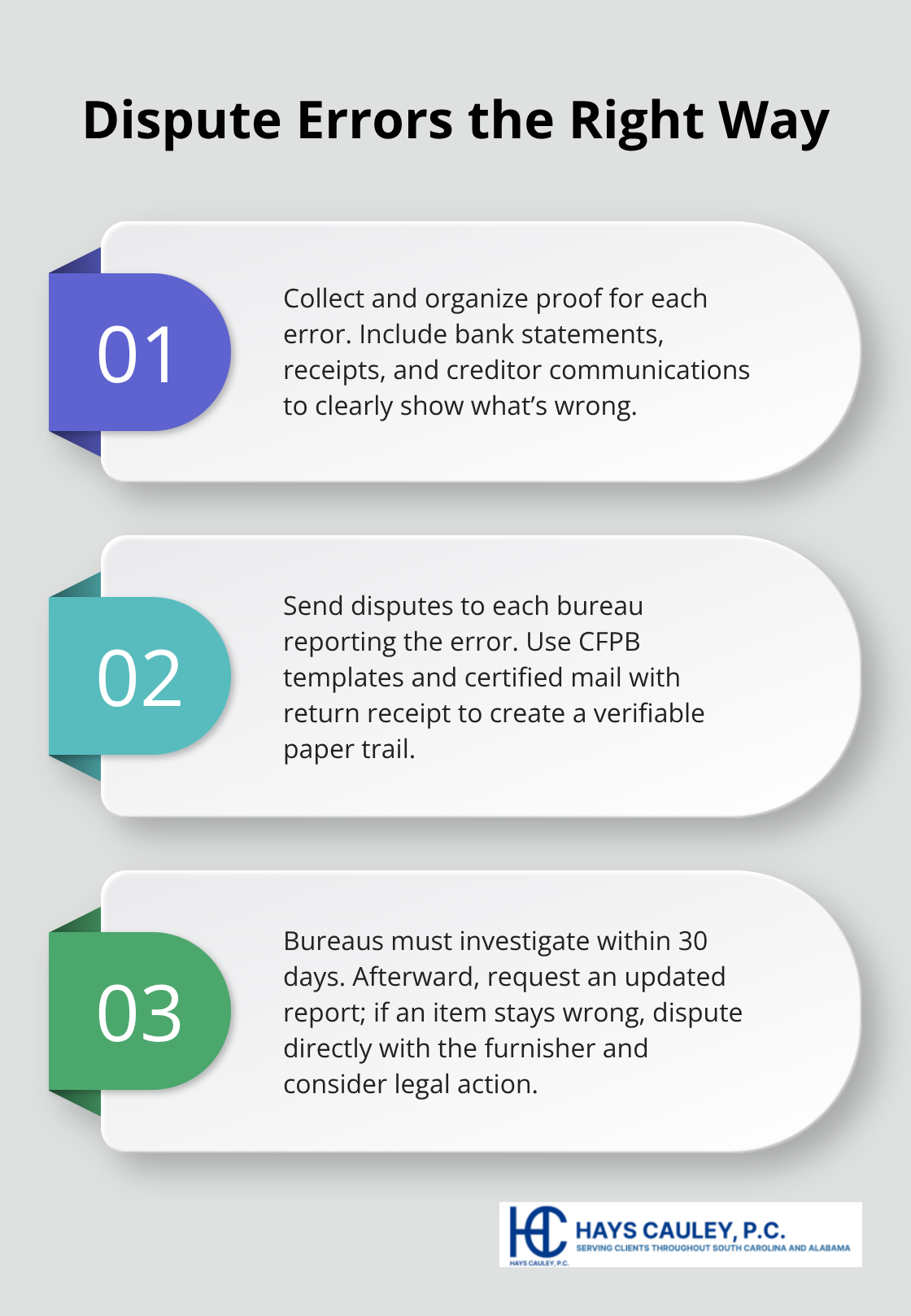

Disputing errors requires action on your part. Gather all supporting documents that prove the information is wrong, organize them by error, and file disputes with each credit bureau reporting the incorrect data.

Use the CFPB dispute templates and send your disputes by certified mail with return receipt to create a verifiable paper trail that proves you took action. The credit bureaus must complete their investigation within 30 days of receiving your dispute. After the investigation concludes, request an updated credit report to verify whether corrections were made. If an error is verified but still incorrect, dispute directly with the furnisher-the company that provided the data to the bureau in the first place. A furnisher’s failure to correct information can support legal action under the FCRA if they refuse to fix what you’ve proven is wrong.

What Happens When Bureaus Ignore Your Dispute

Sometimes credit bureaus remain unresponsive to your dispute efforts. Document all communications and file a CFPB complaint when a bureau fails to investigate properly. The CFPB logged hundreds of thousands of credit reporting complaints (about 175,000 in 2020), showing how widespread these problems are. If disputes persist with limited success, consider seeking legal assistance from a consumer protection attorney. About 70% of disputes lead to some correction, though many issues remain unresolved without professional help. Identity theft complicates disputes further, so place fraud alerts on your reports and file police reports to strengthen your position and coordinate with authorities.

Understanding your rights under the FCRA gives you the tools to fix errors, but creditors and debt collectors also have strict rules they must follow when they interact with you.

How Creditors and Debt Collectors Must Follow FCRA Rules – Serving South Carolina, including Greenville, Columbia and Charleston

Creditors and debt collectors operate under strict FCRA rules that prohibit deceptive, unfair, and abusive practices. Many creditors ignore these restrictions, counting on consumers not knowing what’s actually illegal. The FCRA forbids creditors from misrepresenting the amount you owe, the status of your debt, or your legal rights. They cannot threaten you with jail time for owing money because debtor’s prisons don’t exist in America.

What Creditors Cannot Do When Collecting Debts

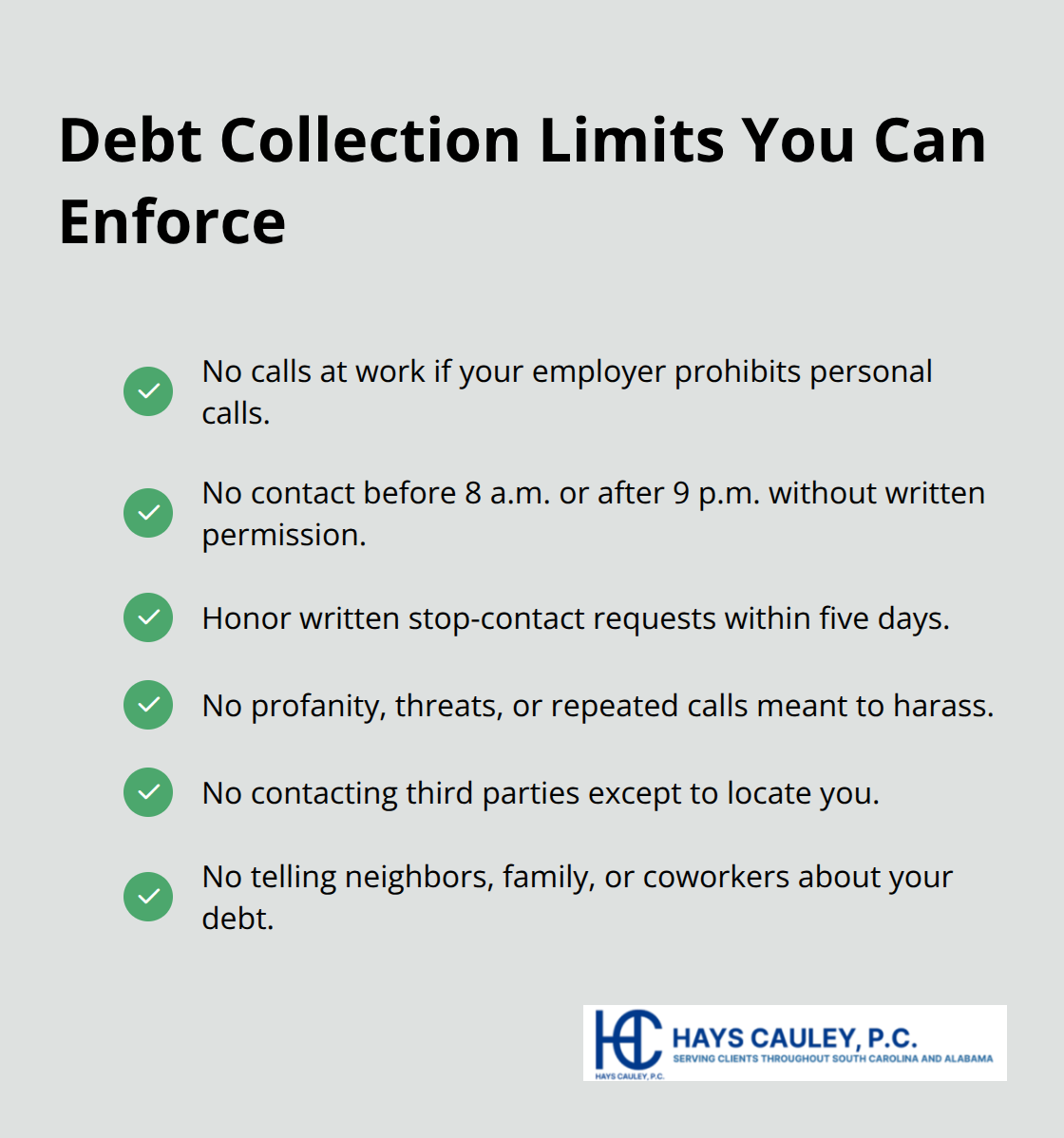

Creditors face clear legal boundaries under the FCRA and the Fair Debt Collection Practices Act. They cannot contact you at work if they know your employer prohibits personal calls, and they cannot contact you before 8 a.m. or after 9 p.m. without your written permission.

If you send a written request to stop contact, creditors must honor it within five days. Collectors cannot use profanity, threats of violence, or repeated calls designed to harass you. They also cannot contact third parties about your debt unless they’re trying to locate you, and they absolutely cannot tell your neighbors, family members, or coworkers about what you owe.

Violations carry real consequences. If a creditor breaks these rules, you have the right to sue for actual damages, statutory damages of up to $1,000 per violation, and attorney’s fees. Document every violation by writing down the date, time, caller’s name, and exact words used during any problematic contact. This documentation becomes your evidence if you need to pursue legal action.

Verify Debts Before You Pay Anything

When a debt collector contacts you, your first move should be sending a written debt verification request within 30 days. The collector must then stop collection efforts until they provide proof that the debt is yours and the amount is correct. Many collectors cannot produce this verification because they bought old debts in bulk without proper documentation. If they cannot verify the debt, they cannot legally collect it.

Send your verification request by certified mail with return receipt so you have proof of the date sent. Keep copies of everything. If the collector continues pursuing you without providing verification, that violation supports your case in court. Some debts are too old to collect anyway-debts older than the statute of limitations in South Carolina (which ranges from three to ten years depending on the debt type) cannot be enforced in court. A collector can still contact you about an old debt, but they cannot sue you to collect it. Many consumers don’t realize this protection exists and pay debts they never legally had to pay.

Control Who Contacts You and When

You have the legal right to opt out of marketing calls, texts, and emails from creditors and their agents. The National Do Not Call Registry stops telemarketing calls, but creditors with whom you have an existing relationship can still contact you unless you specifically tell them to stop. Send a written opt-out request to the creditor’s billing department, keep a copy, and send it certified mail. For debt collectors specifically, send written notice that you revoke permission for any contact. Once they receive your written request, further contact violates the FCRA.

Pre-screened credit offers also fall under opt-out rules. You can call 1-888-5-OPTOUT or visit OptOutPrescreen.com to remove your name from pre-screened marketing lists for five years or permanently. This simple step reduces the volume of credit offers arriving at your home and lowers your identity theft risk since fewer creditors have access to your personal information. If a creditor ignores your opt-out request, document the date and details of each unwanted contact-these violations can support a claim for damages.

Understanding what creditors cannot do protects you from harassment and illegal collection tactics. However, knowing your rights means little if you cannot enforce them when violations occur.

Taking Action When Your Rights Are Violated – Serving South Carolina, including Greenville, Columbia and Charleston

FCRA violations only matter if you document and report them. Start a detailed record the moment you suspect a violation occurred. Write down the date, time, caller’s name, phone number, and word-for-word what was said during any problematic contact with a creditor or debt collector. If you receive written communications like letters or emails containing false information about your debt, save the originals. For credit report errors, take screenshots of the inaccurate information and note the exact date you discovered it. This documentation becomes your evidence if you need to file a complaint or pursue legal action. Many consumers fail at this stage because they assume they will remember details later, but memories fade quickly and creditors know this. The stronger your paper trail, the more seriously regulators and courts treat your claim.

File a Complaint with the Consumer Financial Protection Bureau

Filing a complaint with the CFPB takes about 15 minutes online and costs nothing. Visit ConsumerCompliance.gov and submit your complaint with your documentation attached. The CFPB logged approximately 175,000 credit reporting complaints in 2020 alone, which shows how common these violations are and how seriously the agency takes them. The CFPB forwards your complaint to the company you named, gives them 15 days to respond, and publishes complaint data that helps identify patterns of illegal behavior. This public record matters because it creates accountability and can influence whether regulators take enforcement action against repeat violators. If the company’s response is inadequate or dismissive, you can file a follow-up complaint or escalate the issue.

Pursue Legal Action for Damages

When a creditor or credit bureau violates FCRA rules, you have the right to sue for actual damages plus statutory damages of up to $1,000 per violation and attorney’s fees. This means even a single violation can justify hiring an attorney because the law requires the creditor to pay your legal costs if you win. Contact a consumer protection attorney when violations are serious, when the company ignores your complaints, or when you have clear documentation of repeated rule-breaking. We at Hays Cauley, P.C. represent South Carolina consumers in these situations and help recover damages that violators owe.

Final Thoughts

Your SC FCRA obligations give you real power to fight back against inaccurate credit reports and illegal debt collection practices. The law stands on your side when creditors misrepresent debts, ignore your disputes, or harass you with unwanted contact. Understanding these protections matters, but enforcement is what actually stops violations and recovers the damages you deserve.

The resources available to you are straightforward and free. You can pull your credit reports from AnnualCreditReport.com without paying anything, file complaints with the CFPB online at no cost, and sue for actual damages plus statutory damages up to $1,000 per violation (with creditors required to pay your attorney’s fees if you win). These remedies exist because Congress recognized that consumers need financial incentives to hold violators accountable.

We at Hays Cauley, P.C. help South Carolina consumers enforce their FCRA rights when violations occur. If you have documented violations, unclear credit report errors, or creditors ignoring your written requests to stop contact, contact us today to discuss your situation and explore whether legal action applies to your case.