Your credit report shapes your financial life, yet errors on it happen more often than you’d think. The Fair Credit Reporting Act gives you specific credit report dispute rights that most people never use.

At Hays Cauley, P.C., we help South Carolina residents reclaim control of their credit files. This guide shows you exactly what you can challenge and how to build a stronger case.

What You Can Dispute on Your Credit Report

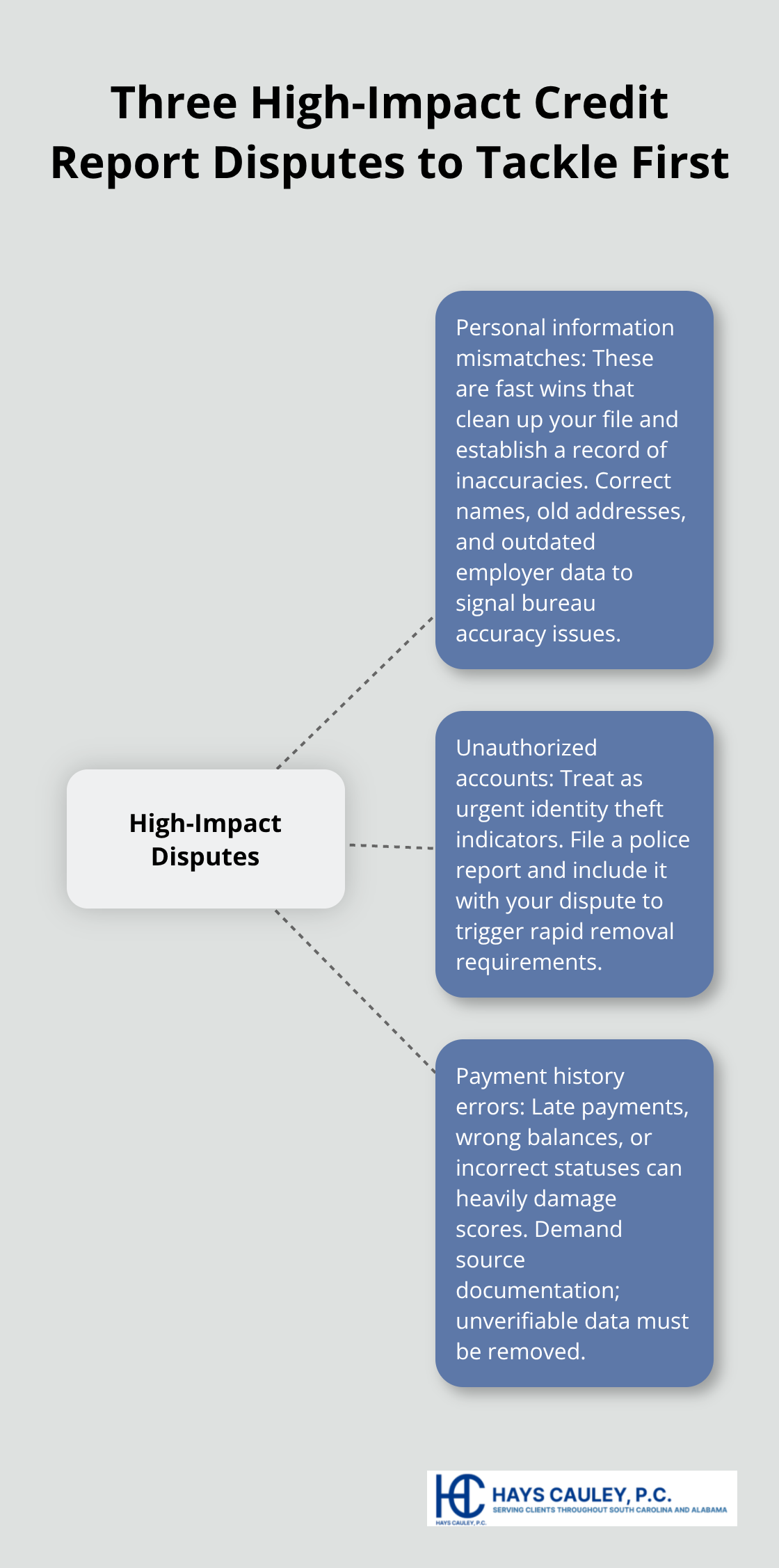

One in five Americans has an error on at least one credit report. Most people focus on disputing a single item, but your leverage comes from understanding exactly which errors courts and regulators take seriously. Personal information mismatches happen constantly and represent your easiest win. A name spelled differently, an address that hasn’t been yours in five years, or an employer you left a decade ago clutters your file and signals that the credit bureaus aren’t maintaining basic accuracy standards. When you dispute these details, credit bureaus rarely push back because correcting them costs nothing and helps their compliance record. Start here if your file contains outdated addresses or employer information, as these corrections establish a pattern that inaccuracies exist in your file.

Unauthorized accounts demand immediate action

Unauthorized accounts represent the most serious errors on your credit report because they indicate identity theft or fraud. A credit card, loan, or line of credit opened in your name that you never authorized creates immediate damage to your score and your financial reputation. The FCRA requires credit bureaus to remove fraudulent information quickly, often within four business days if you provide a police report or identity theft documentation. This speed matters because fraudulent accounts tank your credit score faster than almost any other error. File a police report immediately and submit that report with your dispute if you find unauthorized accounts. Furnishers and credit bureaus move much faster on disputed accounts when law enforcement documentation backs your claim.

Payment history errors give you real leverage

Incorrect payment statuses and balances represent the most common and most damaging errors on credit reports. A late payment reported as 30 days past due when you actually paid on time, a closed account still showing as open, or a balance that’s thousands of dollars higher than your actual debt directly crushes your credit score. These errors persist because furnishers often fail to update information when you make payments or close accounts. When you dispute payment history errors, request that the furnisher provide the source documentation proving their claim. Under FCRA standards clarified in cases like Suluki v. Credit One Bank, if the furnisher cannot verify the information is accurate, it must be removed from your report. This means unverifiable late payments, incorrect balances, and wrong account statuses cannot legally stay on your file. Documentation matters here: gather your own payment records, account statements, and any correspondence showing the correct information (these items form the foundation of your dispute package). The stronger your evidence, the faster bureaus and furnishers resolve these disputes in your favor.

How to build your dispute strategy

Your next step involves identifying which errors on your report fall into these three categories. Pull your credit reports from all three major bureaus and mark every item that doesn’t match your actual financial history. Personal information errors take the least effort to challenge, so start there and build momentum. Fraudulent accounts require police documentation but move through the system fastest. Payment history errors demand the most evidence but carry the most weight with regulators and courts. Once you’ve categorized your errors, you’re ready to file your disputes with the bureaus and furnishers.

How to File a Dispute with Credit Bureaus Serving South Carolina, including Greenville, Columbia and Charleston

Assemble Your Dispute Packet

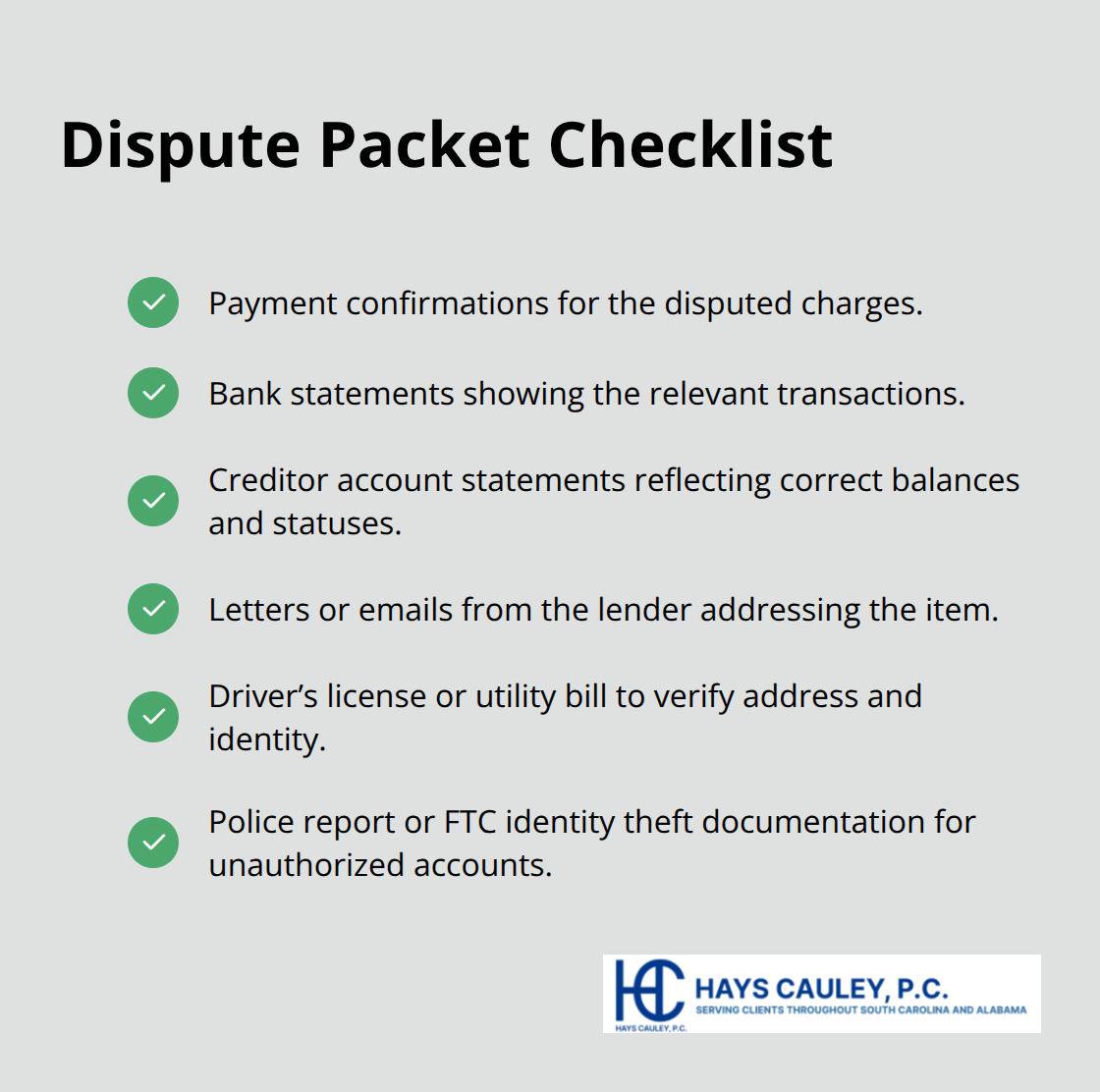

Your dispute packet determines whether credit bureaus and furnishers take your challenge seriously or dismiss it as frivolous. Collect copies of everything that proves your point: payment confirmations, bank statements showing transactions, account statements from the creditor, letters or emails from the lender, and any correspondence addressing the disputed item. For personal information errors, a driver’s license or utility bill establishes your correct address and identity. For unauthorized accounts, include your police report or identity theft documentation from the Federal Trade Commission.

The CFPB recommends using certified mail when submitting disputes directly to furnishers because it creates proof of delivery and dates your submission for the 30-day investigation window. Write your dispute clearly and specifically: identify the exact account number or personal detail you’re challenging, explain why it’s inaccurate, and state what correction you want made. Vague disputes saying something looks wrong get treated as frivolous and rejected without investigation.

File Through the Right Channel

When you file with a credit bureau like Equifax through myEquifax, you’ll receive a 10-digit confirmation code that tracks your dispute status. Courts and regulators scrutinize disputes that lack specificity, so your documentation must support every claim you make. You can also dispute items directly with the creditor or lender that reported the information, which sometimes produces faster results than going through the bureau first.

Track Your Dispute Actively

Monitor your dispute from submission through resolution rather than waiting passively for the 30-day deadline to pass. Check your dispute status within your myEquifax account or through the credit bureau’s online portal every two weeks. If you don’t hear back within 35 days, file a complaint with the Consumer Financial Protection Bureau, which tracks response times and violations. The CFPB received over 50,000 credit reporting complaints in 2023, many involving slow or inadequate dispute responses.

Challenge Denials With Evidence

If the bureau denies your dispute and claims the information was verified, request the specific evidence they used to verify it. Under the Suluki v. Credit One Bank ruling, furnishers cannot legally report information they cannot verify as accurate, so push back on denials that lack documentation. If a dispute goes nowhere, contact the furnisher directly and demand they provide their source documentation. Many furnishers fail to respond to direct disputes properly, which gives you grounds for escalation.

Document Everything for Next Steps

Document every communication, keep copies of all dispute letters and responses, and maintain records of dispute timelines. If disputes stall or furnishers ignore your challenges, you have legal options available. The next section covers your rights when disputes don’t resolve the way they should and what leverage you actually possess during the reinvestigation process.

What Leverage You Actually Have During Dispute Investigation

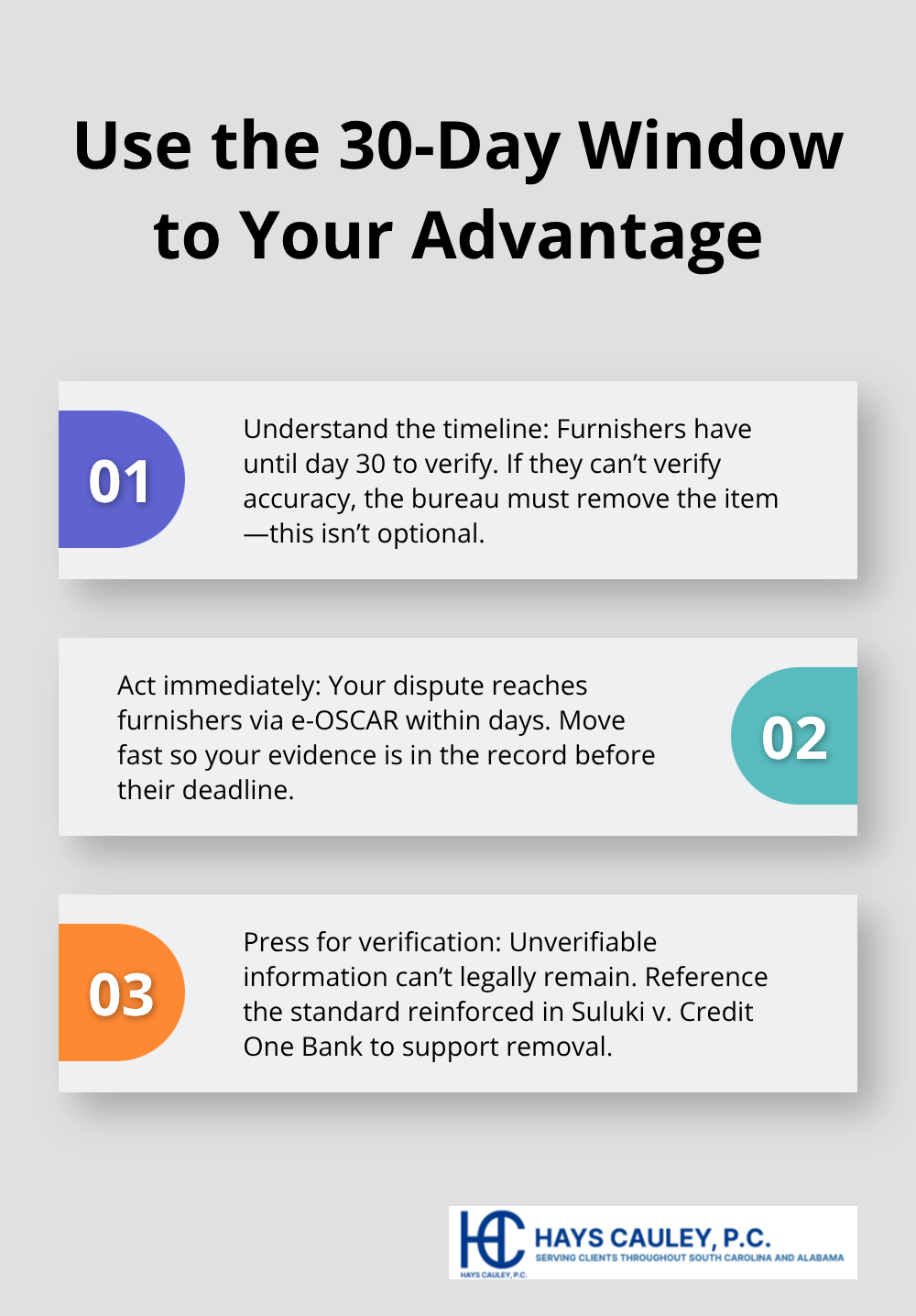

The 30-day investigation window that credit bureaus must follow is your most valuable asset, though most people waste it by sitting idle. When you file a dispute, the bureau forwards it to the furnisher through an automated system called e-OSCAR, which means your challenge reaches the data provider electronically within days. The furnisher then has until day 30 to respond, and here’s the critical part: if they cannot verify the information is accurate, they must tell the credit bureau to remove it. This isn’t optional.

The CFPB and FTC have made clear in regulatory guidance and court filings that unverifiable data cannot legally remain on your report, a standard reinforced in the Suluki v. Credit One Bank case.

Your leverage multiplies when you file direct disputes with furnishers at the same time you dispute with bureaus, because furnishers face pressure from two directions simultaneously. Send your direct dispute to the furnisher’s dispute department using certified mail, and send your bureau dispute through their official channel. Document the dates you sent both disputes because the furnisher’s 30-day clock starts when they receive your challenge, not when the bureau forwards it.

Access Your Free Reports Strategically

You receive one free credit report every 12 months from each of the three major bureaus through AnnualCreditReport.com, but this rule changes if you place a fraud alert on your file. An extended fraud alert, which lasts seven years, allows you to obtain two free credit reports within 12 months instead of one. If you suspect identity theft caused the errors on your report, place an extended fraud alert immediately and use those extra free reports to monitor for additional fraudulent accounts the furnishers may have missed.

Pull reports from all three bureaus at different intervals during your dispute, not all at once, so you can track exactly when corrections appear after the furnisher responds. Many disputes settle before day 30, so checking your report on day 20 often shows removals or corrections before the official deadline.

Submit a Statement When Disputes Fail

If a furnisher claims they verified the information and the bureau sides with them, the FCRA gives you the right to add a brief consumer statement to your file that appears in future reports and disclosures. This statement should be factual and direct: explain that you disputed the item, state why it’s inaccurate, and reference your dispute dates. Lenders and employers reviewing your report will see this statement alongside the disputed item, which signals that you challenged the information and the furnisher couldn’t verify it.

This matters more than most people realize because statements can influence credit decisions when the underlying data is questionable. Adding statements when disputes stall creates a record that weakens the credibility of the disputed item without requiring the furnisher to remove it immediately.

Final Thoughts

Your credit report dispute rights give you real power to fix errors that damage your financial life. The leverage comes from understanding that furnishers cannot legally report information they cannot verify, a standard the CFPB and FTC enforce aggressively. When you file disputes with both credit bureaus and furnishers simultaneously, document everything, and push back on denials with evidence, you force the system to work in your favor.

Start by pulling your credit reports from all three major bureaus and categorizing every error you find. Assemble your dispute packet with payment confirmations, bank statements, and account documentation before you file anything. Submit disputes through both the credit bureau and the furnisher using certified mail so you create proof of delivery and dates for the investigation timeline.

We at Hays Cauley, P.C. help South Carolina residents navigate credit reporting disputes and hold furnishers accountable when they refuse to verify inaccurate information. If you’ve filed disputes that went nowhere or discovered errors that credit bureaus claim are verified without evidence, contact us to discuss your options.